|

市場調查報告書

商品編碼

1431042

全球半導體裝置:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Global Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

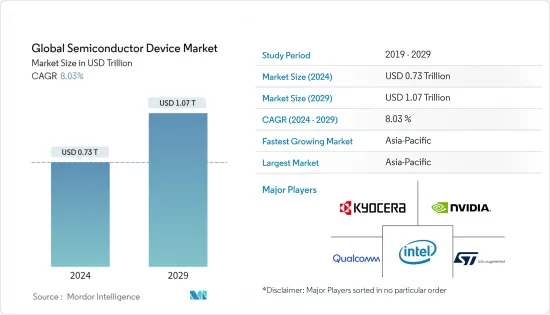

預計2024年全球半導體裝置市場規模將達7,300億美元,預計2029年將達到1.07兆美元,在預測期內(2024-2029年)複合年成長率為8.03%。

半導體產業正在經歷快速成長,半導體已成為所有現代技術的基本組成部分。該領域的進步和創新對所有下游技術產生直接影響。

主要亮點

- 半導體產業預計將應對人工智慧(AI)、自動駕駛、物聯網和5G等新興技術對半導體材料日益成長的需求,以及主要企業之間的競爭和持續的研發支出。預計在預測期內將繼續強勁成長。

- 這項研究涵蓋了供應商提供的各種半導體以及使用它們的行業。最終用戶行業的估計是基於半導體在該行業中服務的應用類型。

- 2020 年初,COVID-19 在全球範圍內的爆發嚴重擾亂了研究市場的供應鏈和生產。對於電路和晶片製造商來說,影響更為嚴重。由於人手不足,亞太地區許多包裝和檢驗工廠已經減少或關閉營運。這也造成了依賴半導體的最終產品公司瓶頸。

- 不過,根據半導體產業協會的數據,半導體產業自2020年第一季開始開始復甦。儘管面臨與冠狀病毒相關的物流課題,位於亞太地區的半導體工廠仍繼續以高產能正常運作。此外,2020年2月韓國等國家的晶片出口成長了9.4%,大多數半導體業務持續不間斷。 COVID-19 大流行增加了消費性電子和汽車行業的半導體需求,這主要是由於大流行後電動車的採用增加。

半導體裝置市場趨勢

積體電路佔據很大佔有率

- 智慧型手機、功能手機和平板電腦設備的普及正在推動市場發展。類比IC具有廣泛的應用,包括第三代和第四代 (3G/4G) 無線基地台和行動裝置電池。 RFIC(射頻 IC)是一種類比電路,通常工作在 3kHz 至 2.4GHz(3,000 赫茲至 24 億赫茲)以及大約 1 THz(1 兆赫茲)頻寬。廣泛應用於行動電話和無線設備。由於持續發展,該領域的類比IC市場預計將成長。

- 在整個IC市場中,邏輯IC是廣泛採用的組件,預計在預測期內將顯著成長。邏輯晶片廣泛應用於幾乎所有數位產品,從智慧型手機到算術邏輯單元(ALU)。近年來,汽車和智慧型手機產業的成長主要推動了邏輯半導體元件的成長。然而,由於 HPC 和 AI 等應用的成長,邏輯組件的範圍目前正在擴大。

- 市面上有不同類型的記憶體,包括 DRAM、SRAM、Nor Flash、NAND Flash、ROM 和 EPROM。半導體記憶體的應用包括電腦記憶體(個人電腦、筆記型電腦)、消費性設備(相機、行動電話)、商業 IT 應用(電信、資料中心)、傳統工業應用以及新興的物頻譜應用。發現電子資料儲存設備。汽車電子中擴大採用記憶體IC以及電子設備中記憶體記憶體晶片的不斷擴大使用是推動DRAM產品需求的主要因素。

- 對資料中心的需求增加也推高了對記憶體組件的需求。目前,北美地區的大型資料中心計劃正在推動對DRAM等記憶體的強勁需求。然而,根據衡量每個用戶資料中心空間的指標,中國網路資料中心的規模預計將成長至少美國的22倍,至少是日本目前規模的10倍。因此,DRAM擁有巨大的成長機會,正在影響半導體產業。

汽車產業佔較大市場佔有率佔有率

- 半導體晶片已成為現代汽車的重要組成部分,因為它們廣泛用於汽車的各種功能。汽車中使用的晶片可以採取型態,從包含單一電晶體的單一組件到控制複雜系統的複雜積體電路。例如,晶片安裝在汽車的 LED 燈元件中。 LED燈單元中的每個二極體都是一個發光的晶片。現代汽車中僅 LED 車頭燈就使用了大量晶片。車頭燈還需要一個控制單元才能發揮作用。

- 車輛安全性的提高以及對 ADAS(高級駕駛輔助系統)需求的不斷成長正在加速對半導體的需求。倒車相機、主動式車距維持定速系統、盲點偵測、變換車道輔助、安全氣囊部署和緊急煞車系統等智慧功能均由半導體技術實現。此外,ADAS 還包括用於基於視覺的功能的圖像和攝影機感測器、用於停車輔助等短距離功能的超音波感測器,以及用於在黑暗或霧中檢測物體的雷達和雷射雷達感測器,涵蓋了廣泛的感應器.

- 先進半導體解決方案供應商瑞薩電子於2022年3月宣布,將擴大與本田在ADAS領域的合作。迄今為止,本田在Legend搭載的「Honda SENSING Elite」中採用了瑞薩電子的汽車SoC(系統單晶片)「R-Car」和汽車MCU「RH850」。作為擴大合作夥伴關係的一部分,本田將在其全方位安全駕駛支援系統「Honda SENSING 360」中使用 R-Car 和 RH850。

- 電動車需求的成長預計將為所研究的市場帶來新的成長機會。電動車中使用的電子設備和感測器數量不斷增加,推動了對半導體晶片的需求。例如,根據國際能源總署 (IEA) 的數據,全球使用的純電動車 (BEV) 數量將從 2016 年的 120 萬輛增加到 2021 年的 1,130 萬輛。

- 此外,中國將在2021年成為電動車的主要生產國(資料來源:IEA)。歐洲地區的銷量在2020年的繁榮之後也繼續呈現強勁成長(成長65%至230萬輛),美國的銷量在經歷了兩年的下滑後也出現了成長。在預測期內,汽車產業預計將對所研究市場的成長產生重大影響,因為電動車銷量預計將遵循類似的成長模式。

半導體裝置產業概況

由於整合度的提高、技術進步和地緣政治局勢,全球半導體裝置市場正在波動。此外,只有在創新具有顯著的永續競爭優勢的市場中,競爭才會加劇。在此背景下,考慮到最終用戶對半導體製造公司品質的期望的重要性,品牌形象發揮著重要作用。由於市場上現有巨頭如英特爾公司、英偉達公司、京瓷公司、高通技術公司和意法半導體公司的存在,市場滲透率也很高。

創新水平、上市時間和性能是參與者在市場上脫穎而出的關鍵條件。整體而言,在預測期內,競爭公司之間的敵對行動正在緩慢成長。

- 2022 年 7 月 愛立信、高通科技公司和法國航太公司泰雷茲計畫將 5G 引入地球軌道衛星網路。在進行了包括多項研究和模擬在內的詳細研究後,該公司將開始測試和檢驗5G 非地面網路 (5G NTN),並專注於智慧型手機用例。

- 2022 年 3 月,英特爾宣布第一階段計劃,未來 10 年在歐盟投資約 800 億歐元,涵蓋整個半導體價值鏈,包括研發 (R&D)、製造和封裝技術。這項投資將包括約170億歐元,用於在德國建立大型半導體晶圓廠,在法國開發新的研發和設計設施,以及在義大利、愛爾蘭、波蘭和西班牙提供研發、製造和代工服務。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 科技趨勢

- 產業價值鏈分析

- 評估 COVID-19 對產業的影響

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

第5章市場動態

- 市場促進因素

- 擴大物聯網和人工智慧等技術的採用

- 5G的普及和5G智慧型手機需求的增加

- 市場課題

- 供應鏈中斷導致半導體晶片短缺

第6章市場區隔

- 依設備類型

- 離散半導體

- 光電子學

- 感應器

- 積體電路

- 模擬

- 邏輯

- 記憶

- Micro

- 微處理器 (MPU)

- 微控制器(MCU)

- 數位訊號處理器

- 依行業分類

- 汽車

- 通訊(有線和無線)

- 消費者

- 工業的

- 計算/資料存儲

- 依地區

- 美國

- 歐洲

- 日本

- 中國

- 韓國

- 台灣

- 世界其他地區

第7章 半導體代工現狀

- 依鑄造廠分類的鑄造業務銷售額和市場佔有率

- 半導體銷售 - IDM 與無晶圓廠

- 截至 2021 年 12 月年底,基於晶圓廠地點的晶圓產能

- 前五名半導體公司晶圓產能及依節點技術分類的晶圓產能趨勢

第8章 競爭形勢

- 公司簡介

- Intel Corporation

- Nvidia Corporation

- Kyocera Corporation

- Qualcomm Incorporated

- STMicroelectronics NV

- Micron Technology Inc.

- Xilinx Inc.

- NXP Semiconductors NV

- Toshiba Corporation

- Texas Instruments Inc.

- Taiwan Semiconductor Manufacturing Company(TSMC)Limited

- SK Hynix Inc.

- Samsung Electronics Co. Ltd

- Fujitsu Semiconductor Ltd

- Rohm Co. Ltd

- Infineon Technologies AG

- Renesas Electronics Corporation

- Advanced Semiconductor Engineering Inc.

- Broadcom Inc.

- ON Semiconductor Corporation

第9章 市場未來展望

The Global Semiconductor Device Market size is estimated at USD 0.73 trillion in 2024, and is expected to reach USD 1.07 trillion by 2029, growing at a CAGR of 8.03% during the forecast period (2024-2029).

The semiconductor industry is witnessing rapid growth, with semiconductors emerging as the basic building blocks of all modern technology. The advancements and innovations in this field are resulting in a direct impact on all downstream technologies.

Key Highlights

- The semiconductor industry is estimated to continue its robust growth during the forecast period to accommodate the increasing demand for semiconductor materials in emerging technologies, such as artificial intelligence (AI), autonomous driving, Internet of Things, and 5G, coupled with competition among key players and consistent spending on R&D.

- The study covers various semiconductors offered by the vendors and the industries utilizing them. The estimates for the end-user industries are derived based on the type of application the semiconductors provide in that industry.

- The outbreak of COVID-19 across the globe has significantly disrupted the supply chain and production of the studied market in the initial phase of 2020. For circuit and chipmakers, the impact was more severe. Due to labor shortages, many of the package and testing plants in the Asia-Pacific region reduced or even suspended operations. This also created a bottleneck for end-product companies that depend on semiconductors.

- However, according to the Semiconductor Industry Association, after Q1 of 2020, the semiconductor industry started the recovery. Despite logistical challenges related to the coronavirus, semiconductor facilities located in Asia-Pacific continued to function normally with high-capacity rates. Moreover, in various countries, such as South Korea, most semiconductor operations continued uninterrupted, and chip exports grew by 9.4% in February 2020. The COVID-19 pandemic has increased the demand for semiconductors across the consumer electronics and automotive sectors, mainly due to the growing adoption of EVs post-pandemic.

Semiconductor Device Market Trends

Integrated Circuit to Hold Significant Share

- The rising proliferation of smartphones, feature phones, and tablets is driving the market. Analog ICs are used in a wide range of applications, including third and fourth-generation (3G/4G) radio base stations and portable device batteries. RFICs (radio frequency ICs) are analog circuits that usually run in the frequency range of 3 kHz to 2.4 GHz (3,000 hertz to 2.4 billion hertz) circuits that would work at about 1 THz (1 trillion hertz). They are widely used in cell phones and wireless devices. As they are under development, the analog IC market in this segment is expected to grow.

- In the overall IC market, logic ICs are the widely adopted component and are expected to witness significant growth over the forecast period. Logic chips have a wide range of applications in almost every digital product ranging from smartphones to arithmetic-logic units (ALU). In recent years, the growth in the automotive and smartphone industry has mainly driven the growth of the logic semiconductor component. However, the growth in applications like HPC and AI is now expanding the scope of logic components.

- The market has different types of memory, such as DRAM, SRAM, Nor Flash, NAND Flash, ROM, and EPROM, among others. Semiconductor memory refers to various electronic data storage devices that find applications as computer memory in computers (PCs, laptops), consumer devices (cameras, phones), commercial IT applications (telecom, datacenters), traditional industrial applications, and the emerging spectrum of IoT applications. The increasing adoption of memory ICs in automobile electronics and the growing application of memory storage chips in electronic devices are the major factors driving the demand for DRAM products.

- The increasing demand for data centers is also boosting the demand for memory components. Currently, large data center projects in North America have contributed to the strong demand for memory, such as DRAM. However, according to the measure of data center space per user, China's internet data centers are poised to grow to at least 22 times that of the United States, or at least ten times the current space of Japan. Hence, DRAM has a significant opportunity for growth and thus is impacting the semiconductor industry.

Automotive Sector to hold a Significant Market Share

- Semiconductor chips have become an integral part of modern-day vehicles, owing to their widespread use in various functions of vehicles. Chips used in cars can take many forms ranging from single components containing a single transistor to intricate integrated circuits controlling a complex system. For instance, chips are found in the LED light elements of vehicles. Every single diode inside an LED light unit is a chip that emits light. LED headlights alone account for a vast number of chips in modern-day cars. The headlights also need control units to make them function.

- The growing need for better safety and advanced driver assistance systems (ADAS) in cars has accelerated the demand for semiconductors. Intelligent functions, like backup cameras, adaptive cruise control, blind-spot detection, lane change assist, airbag deployment, and emergency braking systems, are made possible through semiconductor technologies. Further, ADAS covers a broad array of sensors, including image and camera sensors for vision-based features, ultrasonic sensors for short-range features like parking assist, and radar and lidar sensors for object detection under dark or foggy conditions.

- In March 2022, Renesas Electronics Corporation, a supplier of advanced semiconductor solutions, announced the expansion of its collaboration with Honda in the field of ADAS. Previously, Honda adopted Renesas' R-Car automotive system on a chip (SoC) and RH850 automotive MCU for its Honda SENSING Elite system featured in the Legend. With the expansion of the partnership, Honda will use R-Car and RH850 in the Honda SENSING 360 omnidirectional safety and driver assistance system.

- The increasing demand for electric vehicles is expected to open new growth opportunities for the studied market. An increased number of electronic devices and sensors are used in electric vehicles, driving the demand for semiconductor chips. For instance, according to the International Energy Agency (IEA), the number of battery electric vehicles (BEV) in use has increased from 1.2 million in 2016 to 11.3 million in 2021 globally.

- Furthermore, China was the leading producer of electric vehicles in 2021 (Source: IEA). Sales in the European region also showed continued robust growth (up 65% to 2.3 million) after the 2020 boom, which also increased in the United States after two years of decline. With EV sales expected to follow a similar growth pattern, the automotive industry is expected to significantly impact the growth of the studied market during the forecast period.

Semiconductor Device Industry Overview

The Global Semiconductor Device Market is witnessing fluctuation with growing consolidation, technological advancement, and geopolitical scenarios. Further, in a market where the sustainable competitive advantage through innovation is considerably high, the competition will only increase. In such a situation, the brand identity plays a major role, considering the importance of quality that the end-users expect from a semiconductor manufacturing player. With the presence of large market incumbents, such as Intel Corporation, Nvidia Corporation, Kyocera Corporation, Qualcomm Technologies Inc., and STMicroelectronics NV, the market penetration levels are also high.

The level of innovation, time-to-market, and performance are the key terms by which the players differentiate themselves in the market. Overall, the intensity of competitive rivalry is moderately growing over the forecast period.

- July 2022 - Ericsson, Qualcomm Technologies Inc., and French aerospace company Thales are planning to take 5G out of this world and across a network of Earth-orbiting satellites. After having conducted detailed research, which includes multiple studies and simulations, the parties plan to enter smartphone-use-case-focused testing and validation of 5G non-terrestrial networks (5G NTN).

- March 2022 - Intel issued the first phase of its investment plans of approximately EUR 80 billion in the European Union over the next decade across the entire semiconductor value chain, including research and development (R&D), manufacturing, and packaging technologies. In this investment, the company plans to invest approximately EUR 17 billion in establishing a semiconductor fab mega-site in Germany, along with the development of a new R&D and design facility in France, and to invest in R&D, manufacturing, and foundry services in Italy, Ireland, Poland, and Spain.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of Technologies like IoT and AI

- 5.1.2 Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 5.2 Market Challenges

- 5.2.1 Supply Chain Disruptions Resulting in Semiconductor Chip Shortage

6 MARKET SEGMENTATION

- 6.1 By Device Type

- 6.1.1 Discrete Semiconductors

- 6.1.2 Optoelectronics

- 6.1.3 Sensors

- 6.1.4 Integrated Circuits

- 6.1.4.1 Analog

- 6.1.4.2 Logic

- 6.1.4.3 Memory

- 6.1.4.4 Micro

- 6.1.4.4.1 Microprocessors (MPU)

- 6.1.4.4.2 Microcontrollers (MCU)

- 6.1.4.4.3 Digital Signal Processors

- 6.2 By End-user Vertical

- 6.2.1 Automotive

- 6.2.2 Communication (Wired and Wireless)

- 6.2.3 Consumer

- 6.2.4 Industrial

- 6.2.5 Computing/Data Storage

- 6.3 By Geography

- 6.3.1 United States

- 6.3.2 Europe

- 6.3.3 Japan

- 6.3.4 China

- 6.3.5 Korea

- 6.3.6 Taiwan

- 6.3.7 Rest of the World

7 SEMICONDUCTOR FOUNDRY LANDSCAPE

- 7.1 Foundry Business Revenue and Market Shares by Foundries

- 7.2 Semiconductor Sales - IDM vs Fabless

- 7.3 Wafer Capacity by end of December 2021 based on Fab Location

- 7.4 Wafer Capacity by the Top Five Semiconductor Companies and an Indication Of Wafer Capacity By Node Technology

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Intel Corporation

- 8.1.2 Nvidia Corporation

- 8.1.3 Kyocera Corporation

- 8.1.4 Qualcomm Incorporated

- 8.1.5 STMicroelectronics NV

- 8.1.6 Micron Technology Inc.

- 8.1.7 Xilinx Inc.

- 8.1.8 NXP Semiconductors NV

- 8.1.9 Toshiba Corporation

- 8.1.10 Texas Instruments Inc.

- 8.1.11 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 8.1.12 SK Hynix Inc.

- 8.1.13 Samsung Electronics Co. Ltd

- 8.1.14 Fujitsu Semiconductor Ltd

- 8.1.15 Rohm Co. Ltd

- 8.1.16 Infineon Technologies AG

- 8.1.17 Renesas Electronics Corporation

- 8.1.18 Advanced Semiconductor Engineering Inc.

- 8.1.19 Broadcom Inc.

- 8.1.20 ON Semiconductor Corporation

9 FUTURE OUTLOOK OF THE MARKET

日本半導體裝置市場2024-2028

日本半導體裝置市場2024-2028 全自動探針台市場報告:2030 年趨勢、預測與競爭分析

全自動探針台市場報告:2030 年趨勢、預測與競爭分析 工業半導體裝置:市場佔有率分析、產業趨勢/統計、2024年至2029年成長預測

工業半導體裝置:市場佔有率分析、產業趨勢/統計、2024年至2029年成長預測 消費性半導體元件:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測

消費性半導體元件:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測 用於加工的半導體裝置-市場佔有率分析、產業趨勢與統計、2024年至2029年的成長預測

用於加工的半導體裝置-市場佔有率分析、產業趨勢與統計、2024年至2029年的成長預測 通訊業半導體元件:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測

通訊業半導體元件:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測 可程式邏輯裝置(PLD) 的全球市場 2024-2028

可程式邏輯裝置(PLD) 的全球市場 2024-2028 全球電子材料氣體(含氖、氙)市場分析(2023-2024年)

全球電子材料氣體(含氖、氙)市場分析(2023-2024年) 光敏半導體裝置市場報告:2030 年趨勢、預測與競爭分析

光敏半導體裝置市場報告:2030 年趨勢、預測與競爭分析 全自動探針站的全球市場:2018-2029年

全自動探針站的全球市場:2018-2029年