|

市場調查報告書

商品編碼

1444895

現場服務管理 (FSM) - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029 年)Field Service Management (FSM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

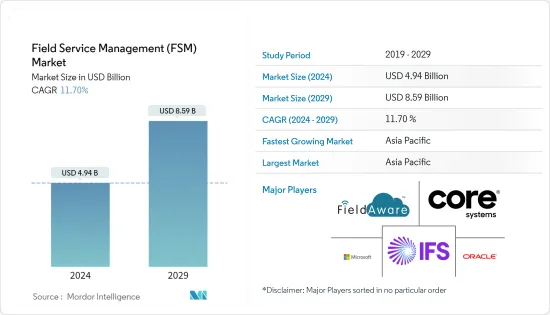

現場服務管理市場規模預計到 2024 年為 49.4 億美元,預計到 2029 年將達到 85.9 億美元,在預測期內(2024-2029 年)CAGR為 11.70%。

現場服務管理公司面臨巨大的壓力,需要有效領導團隊並確保安全遵守風險較高的 COVID-19 爆發。沒有溝通不良或不信任的空間。根據《哈佛商業評論》報道,疫情爆發前,美國組織信任度平均值僅 70%。鑑於壓力情況會加劇恐懼和不信任,此時專注於培養組織內部的信心就顯得尤為重要。

主要亮點

- 供應商實施各種定價策略以在競爭激烈的市場環境中生存。軟體供應商正在採用技術進步帶來的以客戶為中心的定價策略。 FSM 產業的一些供應商專注於根據客戶的需求和價值認知提供基於價值的定價模型。軟體解決方案的定價是基於解決方案的差異化特徵以及為客戶提供的增值功能。

- 在預測期內,由於對更好、更快服務的需求不斷成長,對軟體即服務 (SaaS) 相對於傳統本地軟體的偏好將大幅增加。隨著雲端運算在現場服務管理市場的成長,許多企業正在轉向基於雲端的FSM解決方案。這些解決方案減輕了 IT 部門的負擔,並允許外部服務提供者為其使用者提供支援和維護。

- 市場上的主要參與者都專注於策略性收購,以增強其能力並保持競爭力。例如,2021 年 12 月,美國和加拿大基於 SaaS 的車隊管理軟體和補充解決方案的重要供應商 GPS Insight 宣布收購基於行動雲端的現場服務解決方案提供商 FieldAware。此次收購擴大了 GPS Insight 的現場服務和車隊追蹤能力,使他們能夠透過更強大、更全面的數位平台,提供營運洞察和成本節約能力,更好地為各種規模的客戶提供服務。

- 此外,2021 年6 月,ServicePower 和普華永道企業諮詢(普華永道提供擔保、諮詢和稅務服務的公司網路的一部分)宣佈建立合作夥伴關係,為歐洲各地的製造組織提供聯合現場服務管理產品。這兩個組織最初將專注於歐洲市場。根據該協議,ServicePower 將提供日程最佳化、行動應用程式、面向客戶的入口網站、報告和分析。這種情況增加了整個歐洲的 FMS 市場機會。

- 市場上的供應商正在擴大他們的服務,這提高了他們在市場上的知名度和成長機會。例如,2022 年 5 月,領先的現場服務管理 (FSM) 軟體公司 ServicePower 宣布其服務現已在法國推出。該現場服務管理專家確認了其在歐洲的擴張以及協助零售商、保險公司、消費電子公司和家庭服務公司為其客戶提供量身定做的一流體驗,同時實現顯著營運效率的雄心。

- 原始設備製造商正在採用工業物聯網 (IIoT) 來提供新服務,這需要現代 FSM 系統來管理現場服務交付,從而導致對 FSM 解決方案的需求增加。此外,機器學習提供了新的競爭優勢來源。成功執行這項任務需要現代 FSM 解決方案。現場服務管理解決方案的採用率越來越高,因為它可以在不增加現場員工規模的情況下提高員工生產力並簡化業務流程。

- 在 COVID-19 之後,由於疫情限制了行業專業人士和利益相關者遠端管理其現場工作,因此先前估計的 FSM 在最終用戶區隔市場的成長預計將會上升。 COVID-19 大流行導致車間內採取社交距離措施的工人有限,這將進一步促進採用。

- 此外,由於對時間和具有成本效益的解決方案的需求不斷成長,現場服務管理行業在過去幾年中經歷了快速成長。多項研究表明,由於普遍的人口狀況,美國和歐洲等成熟市場將出現現場服務勞動力短缺的情況,這反過來又導致組織更加重視後端自動化和利用先進技術實現遠端監控。

現場服務管理市場趨勢

服務合約管理將佔據重要市場佔有率

- 依賴外部承包商或第三方服務提供者進行現場工作的企業也需要與企業業務相同的功能。儘管如此,客戶的詳細資訊和可見性在這裡更為重要。部分或全部外包現場服務可以幫助公司降低勞動成本並擴大業務。將工作分配給承包商後,多家公司無法知道服務何時交付、需要多長時間,甚至問題是否已解決,直到他們開始收到客戶投訴。用於外包服務的 FSM 軟體主要提供承包商服務交付的可見性,使第三方技術人員與組織的內部員工無法區分。

- 這些公司現在已經能夠透過 FSM 軟體解決方案中的供應商入口網站來管理其承包商和相關的管理任務。就像傳統的現場工作人員一樣,承包商也需要即時存取工作訂單資訊、零件可用性以及快速報告服務交付情況和提交索賠的能力。需要現場技術人員的客戶呼叫也可以由公司分派給其技術人員或當地服務合作夥伴。此外,這些入口網站可以存在於公司主介面之外,以便公司資料保持安全,同時允許每個人存取他們需要的內容。

- 提供與外部員工的這種雙向互動主要使服務公司能夠向承包商發出最後一刻的時間表變更,主要是向客戶提供有關技術人員到達時間的最新資訊,監控工作訂單以確保SLA 合規性,甚至創造機會用於最佳化調度和規劃。

- 市場上的供應商一直在提供創新的解決方案來滿足客戶的需求。例如,Mize Inc. 提供其服務合約管理軟體和解決方案,幫助第三方管理員 (TPA)、製造商 (OEM)、零售商和通路合作夥伴設定、銷售、管理、追蹤和分析各種服務計劃。

- 此外,雲端整合合約管理解決方案因其高資料安全性、可擴展性和更好的資料管理功能而在各個組織中採用,允許公共和私營部門多個行業的組織起草、談判、簽署、在一個集中位置批准、追蹤和續約合約。

亞太地區將見證顯著成長

- 預計亞太地區的現場服務管理市場將顯著成長。快速成長歸因於該地區擁有許多中小企業,它們高度參與開發和採用現場服務及其管理解決方案。隨著現場服務和行動角色的範圍越來越廣泛,行動工作人員的角色在該地區比以前更加普遍,支援技術專案採用行動應用程式,這將推動亞太地區的市場。

- 在中國、印度、新加坡、日本和韓國等發展中國家,透過客戶滿意度提供差異化服務的需求日益成長。這些期望可能會成長,使用現場服務管理軟體的組織必須確保改善現場工作人員和客戶之間的溝通,確保有效率地提供服務。

- 此外,主要由於大規模工業化,現場服務管理市場在該地區正在興起。隨著地理區域的擴大和客戶群的擴大,該地區的現場服務管理市場預計將呈現穩定成長。該地區技術用戶數量的成長進一步推動了現場服務管理市場的成長。

- 印度是亞太地區現場服務管理解決方案、雲端運算和人工智慧 (AI) 的重要市場之一。中小企業擴大採用雲端和人工智慧,以及所有最終用戶對人工智慧技術的投資增加,是推動市場的重要因素。 Yotta 調查顯示,37% 的印度企業在雲端擁有數位化基礎設施,預計到 2022 年,超過 60% 的企業將透過雲端採用。此外,市場在自動化、機器對機器通訊、雲端運算等領域的擴張製造、雲端AI直接帶動現場服務管理平台的需求。因此,對 FSM 解決方案的需求不斷增加。

- 例如,2022 年7 月,Pune India Birlasoft Ltd(一家數位和IT 服務公司,隸屬於價值28 億美元的多元化CK Birla Group)透過利用SAP 的RISE 將其數位環境轉變為雲,加強了與SAP 的關係。隨著企業採用「雲端優先」策略,Birlasoft 將能夠大幅加速客戶的轉型之旅。

現場服務管理產業概述

現場服務管理 (FSM) 市場格局仍然相當分散。有許多預先包裝 FSM 軟體解決方案供應商,但沒有一家 FSM 供應商主導全球市場或任何區域市場。一些參與者正在市場上建立合作夥伴關係、擴張和合作,以增加他們的市場佔有率。

- 2022 年 5 月 - 現場服務管理 (FSM) 軟體公司 ServicePower 宣布法國市場已對其服務開放。這位現場服務管理專家透過幫助企業提供客製化的消費者體驗,同時實現顯著的營運效率,確認了其在歐洲的發展。此外,由於結合了最佳化演算法和人工智慧功能,ServicePower 平台將提供一系列有用的解決方案,用於處理與保固、維修和更換物品相關的客戶需求。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- 產業價值鏈分析

- 主要 FSM 用例分析(用於遠端協助的 AR/VR 的出現、專注於客戶保留和服務的預測性維護、逐步向後端自動化過渡)

- 買家的主要考慮因素和當務之急

- COVID-19 對現場服務業的影響

- 技術簡介

第 5 章:市場動態

- 市場促進因素

- 越來越重視最大限度地提高工作效率

- 行動性和基於雲端的解決方案的採用等技術趨勢

- 創造新的銷售機會

- 市場課題

- 資料機密性問題、實施/整合問題和授權成本

第 6 章:市場區隔

- 部署類型

- 本地

- 雲

- 組織規模

- 中小企業

- 大型企業

- FSM 軟體與服務類型

- 調度、調度和路線最佳化

- 服務合約管理

- 工單管理

- 使用者管理

- 庫存管理

- 其他軟體(計費、發票和保固管理)

- 服務

- 最終用戶

- Allied FM(硬 - 建築和 HVAC,軟 - 景觀美化和清潔)

- 資訊科技和電信

- 醫療保健和生命科學

- 能源和公用事業

- 油和氣

- 製造業

- 其他最終用戶(交通、房地產等)

- 地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 歐洲其他地區

- 亞太地區

- 世界其他地區

- 北美洲

第 7 章:競爭格局

- 公司簡介

- Field Aware US, Inc.

- Oracle Corporation (OFSC)

- IFS AB

- ServiceMax Inc.

- ServicePower, Inc.

- Coresystems (SAP SE)

- Microsoft Corporation (Dynamics 365 for Field Service)

- Accruent LLC (Fortive Corp)

- Mize, Inc.

- Salesforce.com, Inc. (Field Service Cloud)

- Zinier, Inc.

- Trimble Inc.

- The simPRO Group Pty Limited

- Kirona Solutions Limited

第 8 章:投資分析

第 9 章:未來展望

The Field Service Management Market size is estimated at USD 4.94 billion in 2024, and is expected to reach USD 8.59 billion by 2029, growing at a CAGR of 11.70% during the forecast period (2024-2029).

Field service management firms are experiencing immense pressure to effectively lead teams and ensure safety compliance with the outbreak of COVID-19, where the risks are running high. There is no space for miscommunication or distrust. According to Harvard Business Review, before the pandemic, the U.S. average for organizational trust was only 70%. Seeing as stressful situations exacerbate fear and distrust, it is even more critical at this point to focus on developing confidence within the organization.

Key Highlights

- Vendors implement various pricing strategies to survive in the competitive market environment. The software vendors are adopting customer-centric pricing strategies enabled by technological advancements. Several vendors in the FSM industry are focusing on providing value-based pricing models depending on the customers' needs and value perceptions. The software solution pricing is based on the differentiating characteristics of the solution and the value-added features given to the customers.

- The preference for software-as-a-service (SaaS) over traditional on-premise software is set to increase considerably during the forecast period, aided by the growing demand for better and faster service. With the growth of cloud computing in the field service management market, many enterprises are switching to cloud-based FSM solutions. These solutions ease the burden on the I.T. department and allow the external service providers to offer support and maintenance to their users.

- The key players in the market are focusing on strategic acquisitions to enhance their capabilities and stay competitive. For instance, In December 2021, GPS Insight, a significant provider of SaaS-based fleet management software and complementary solutions in the United States and Canada, announced the acquisition of FieldAware, the provider of mobile, cloud-based field service solutions. The acquisition expands GPS Insight's field services and fleet tracking capabilities, allowing them to better serve customers of all sizes through a more robust and comprehensive digital platform with operational insights and cost savings capabilities.

- Moreover, in June 2021, ServicePower and PwC Enterprise Advisory, part of the PwC network of firms providing assurance, advisory, and tax services, announced a partnership that delivers a joint field service management offering to manufacturing organizations across Europe. The two organizations will initially focus on the European market. With this agreement, ServicePower will Provide schedule optimization, Mobility application, Customer facing portal, Reporting, and analytics. Such instances increases the FMS market opportunities across the Europe.

- The vendors in the market are expanding their services, which results in increasing their visibilty and growth opportunities in the market. For instance In May 2022, ServicePower, a leading Field Service Management (FSM) software company, has announced that its services are now available in France. The field service management specialist confirms its expansion in Europe and its ambition to assist retailers, insurance companies, consumer electronics companies, and home service companies in providing tailored first-class experiences to their customers while achieving significant operational efficiencies.

- The original equipment manufacturers are adopting the industrial Internet of things (IIoT) for new services, which require a modern FSM system to manage the field service delivery leading to an increased demand for FSM solutions. Additionally, machine learning provides new sources of competitive advantage. The successful execution of this requires modern FSM solutions. There has been an increasing adoption of field service management solutions, as it improves workforce productivity and streamlines the business process without increasing the size of the field-based workforce.

- In the wake of COVID-19, the previously estimated growth of FSM across end-user segments is expected to rise as the pandemic restricts the industry professionals and stakeholders from managing their fieldwork remotely. The COVID-19 pandemic has resulted in limited workers on the floor to have social distancing measures, which will further boost the adoption.

- Also, the field service management industry has witnessed rapid growth over the last few years, buoyed by the increasing demand for time and cost-effective solutions. Several studies have revealed that there would be a shortage of field service workforce in mature markets such as the U.S. and Europe due to the prevalent demographic conditions, which has, in turn, led to organizations placing a higher emphasis on back-end automation and the use of advanced technologies to enable remote monitoring.

Field Service Management Market Trends

Service Contract Management to Hold Significant Market Share

- Businesses relying on outside contractors or third-party service providers for fieldwork also require the same functionality as enterprise businesses. Still, the client details and visibility are even more important here. Outsourcing field services, partial or full, can help companies reduce labor costs and expand their operations. After a job is assigned to a contractor, multiple companies had no way to know when service is delivered, how long it took, or if the issue is even resolved until they started receiving customer complaints. The FSM software for outsourced services primarily provides visibility into the contractor service delivery making third-party technicians indistinguishable from an organization's internal workforce.

- The companies have now become able to manage their contractors and related administrative tasks through vendor portals within the FSM software solution. Just as with traditional field workers, contractors also need real-time access to the work order information, parts availability, and the ability to report back quickly on service delivery and submit claims. The customer calls requiring a technician on-site can also be dispatched by a company to its technicians or a local service partner. Moreover, these portals can exist outside the main company interface so that the company data remains secure while allowing everyone to access what they need.

- Providing this two-way interaction with the outside employees primarily enables service companies to issue last-minute schedule changes to the contractors, majorly providing updates to their customers about technician arrival times, monitor work orders in order to ensure SLA compliance, and even create opportunities for optimized scheduling and planning.

- Vendors in the market have been offering innovative solutions to satisfy their client's needs. For example, Mize Inc. provides its service contract management software and solutions to help third-party administrators (TPAs), manufacturers (OEMs), retailers, and channel partners to set up, sell, administer, track, and analyze various service programs.

- Additionally, the adoption of cloud-integrated contract management solutions across various organizations due to its benefit in high data security, scalability, and better data management features, which allow organizations from multiple industries in the public and private sectors to draft, negotiate, sign, approve, track, and renew contracts in one centralized location.

Asia Pacific to Witness Significant Growth Rate

- The Asia Pacific is expected to witness significant field service management market growth. The rapid growth rate is attributed to the region being home to many SMEs, which are highly involved in developing and adopting field services and their management solutions. With an increasingly wide range of field services and mobile roles available, the role of the mobile worker is more prevalent than before in the region, supporting the adoption of mobile apps for technical projects, which would drive the market in the APAC region.

- In developing countries, including China, India, Singapore, Japan, and South Korea, the increasing need to differentiate services through customer satisfaction is now more prevalent. These expectations will likely grow, and organizations using field service management software must ensure improved communication between field staff and customers, ensuring services are delivered efficiently.

- Additionally, the field service management market has an emerging scope in the region, majorly due to large-scale industrialization. The region is expected to exhibit steady growth in the field service management market with enhanced geographic zones and a high client base. The growth in the number of technology users in the region further propels the growth of the field service management market.

- India is one of the significant markets in the Asia pacific Region for field service management solutions, cloud computing, and artificial intelligence (AI). Growing cloud and AI adoption among SMEs and increased investments in AI technology by all end-users are significant factors driving the market. According to a Yotta survey, 37% of Indian enterprises had their digital infrastructure in the cloud, with more than 60% expected to be adopted through the cloud by 2022. Furthermore, the market's expansion in automation, machine-to-machine communication, cloud manufacturing, and cloud AI directly drives the demand for field service management platforms. As a result, the demand for FSM solutions is increasing.

- For instances, In July 2022, Pune India Birlasoft Ltd, a digital and IT services company and part of the USD 2.8 billion diversified CK Birla Group, strengthened its relationship with SAP by leveraging RISE with SAP to transform its digital landscape onto the cloud. With enterprises adopting a 'Cloud-First' strategy, Birlasoft will be able to accelerate their clients' transformation journeys significantly.

Field Service Management Industry Overview

The Field Service Management (FSM) market landscape remains quite fragmented. Various vendors of pre-packaged FSM software solutions exist, but no single FSM vendor dominated the global market or any regional markets. Several players are forming partnerships, expansions, and collaborations in the market to increase their market share.

- May 2022 - A Field Service Management (FSM) software company ServicePower has announced that the French market has been made open to its services. The field service management specialist affirms its European development by empowering businesses to provide customized consumer experiences while realizing significant operational efficiencies. Additionally, the ServicePower platform would offer a range of useful solutions for handling client demands connected to warranty, repair, and exchange of items due to the incorporation of optimization algorithms and the usage of artificial intelligence capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Analysis of Major FSM Use-cases (Emergence of AR/VR for Remote Assistanc, Focus on Predictive Maintenance for Customer Retention and Service, Gradual Transition Toward Back-end Automation)

- 4.5 Key Considerations and Imperatives for Buyers

- 4.6 Impact of COVID-19 on Field Service Industry

- 4.7 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing emphasis on maximizing work efficiency

- 5.1.2 Technological trends such as mobility and adoption of cloud-based solutions

- 5.1.3 Creation of new sales opportunities

- 5.2 Market Challenges

- 5.2.1 Data confidentiality concerns, Implementation/Integration Issues, and Licensing Costs

6 MARKET SEGMENTATION

- 6.1 Deployment Type

- 6.1.1 On-premises

- 6.1.2 Cloud

- 6.2 Organisation Size

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 FSM Software and Service Type

- 6.3.1 Scheduling, Dispatch & Route Optimization

- 6.3.2 Service Contract Management

- 6.3.3 Work Order Management

- 6.3.4 Customer Management

- 6.3.5 Inventory Management

- 6.3.6 Other Software (Billing, Invoicing and Warranty Management)

- 6.3.7 Services

- 6.4 End-User

- 6.4.1 Allied FM (Hard - Building and HVAC and Soft - Landscaping & Cleaning)

- 6.4.2 IT and Telecom

- 6.4.3 Healthcare and Lifesciences

- 6.4.4 Energy and Utilities

- 6.4.5 Oil and Gas

- 6.4.6 Manufacturing

- 6.4.7 Other End-Users (Transportation, Real Estate, etc.)

- 6.5 Geography

- 6.5.1 North America

- 6.5.1.1 United States

- 6.5.1.2 Canada

- 6.5.2 Europe

- 6.5.2.1 United Kingdom

- 6.5.2.2 Germany

- 6.5.2.3 France

- 6.5.2.4 Rest of Europe

- 6.5.3 Asia Pacific

- 6.5.4 Rest of the World

- 6.5.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Field Aware US, Inc.

- 7.1.2 Oracle Corporation (OFSC)

- 7.1.3 IFS AB

- 7.1.4 ServiceMax Inc.

- 7.1.5 ServicePower, Inc.

- 7.1.6 Coresystems (SAP SE)

- 7.1.7 Microsoft Corporation (Dynamics 365 for Field Service)

- 7.1.8 Accruent LLC (Fortive Corp)

- 7.1.9 Mize, Inc.

- 7.1.10 Salesforce.com, Inc. (Field Service Cloud)

- 7.1.11 Zinier, Inc.

- 7.1.12 Trimble Inc.

- 7.1.13 The simPRO Group Pty Limited

- 7.1.14 Kirona Solutions Limited

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK

全球現場服務管理市場:按產品(解決方案、服務)、部署型態(本地、雲端)、組織規模、產業(製造、運輸與物流、建築與房地產)、地區 - 預測 2028 年

全球現場服務管理市場:按產品(解決方案、服務)、部署型態(本地、雲端)、組織規模、產業(製造、運輸與物流、建築與房地產)、地區 - 預測 2028 年 2024-2032 年現場部隊自動化市場(按組件、部署模式、組織規模、垂直產業和地區分類)

2024-2032 年現場部隊自動化市場(按組件、部署模式、組織規模、垂直產業和地區分類) 現場服務管理市場:按提供的服務、功能、部署類型、最終用戶產業 - 2024-2030 年全球預測

現場服務管理市場:按提供的服務、功能、部署類型、最終用戶產業 - 2024-2030 年全球預測 現場服務管理市場 - 成長、未來前景、競爭分析,2023-2031 年

現場服務管理市場 - 成長、未來前景、競爭分析,2023-2031 年 2024 年現場服務管理全球市場報告

2024 年現場服務管理全球市場報告 現場服務管理市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

現場服務管理市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 現場服務管理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模型、企業規模、垂直行業、地區和競爭細分,2018-2028 年

現場服務管理市場 - 全球產業規模、佔有率、趨勢、機會和預測,按組件、部署模型、企業規模、垂直行業、地區和競爭細分,2018-2028 年 現場服務管理市場 - 按部署模型、按企業規模、按組件、垂直行業、預測 2023 - 2032 年

現場服務管理市場 - 按部署模型、按企業規模、按組件、垂直行業、預測 2023 - 2032 年 現場服務管理 (FSM) 市場規模、佔有率、趨勢分析報告:按組件、按部署、按公司、按最終用途、按地區、按細分市場、預測,2023-2030 年

現場服務管理 (FSM) 市場規模、佔有率、趨勢分析報告:按組件、按部署、按公司、按最終用途、按地區、按細分市場、預測,2023-2030 年 現場部隊自動化的全球市場

現場部隊自動化的全球市場