|

市場調查報告書

商品編碼

1445440

用於行動裝置的 MEMS - 市場佔有率分析、產業趨勢與統計、成長預測(2024 年 - 2029 年)MEMS for Mobile Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

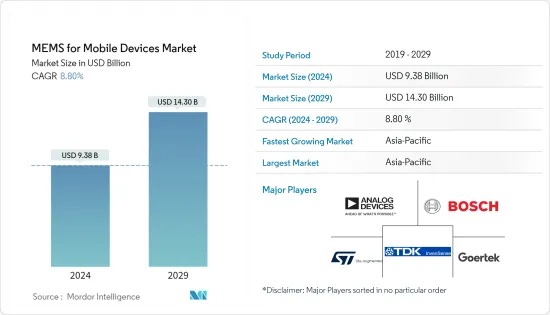

行動裝置MEMS市場規模預計到2024年將達到93.8億美元,預計到2029年將達到143億美元,在預測期內(2024-2029年)CAGR為8.80%。

隨著智慧型手機中加速計和陀螺儀需求的增加,行動裝置市場的MEMS預計將在預測期內顯著成長。例如,到 2022 年,全球行動用戶總數預計將達到 84 億左右。根據愛立信的預測,這一數字還將進一步增加。

主要亮點

- 研究市場的特點是 MEMS 裝置的功耗呈現降低趨勢。此外,不斷變化的消費者需求,例如更快的充電速度、更短的充電時間和更好的充電最佳化,推動了智慧行動裝置中對感測器的需求。這些設備的功耗更低,因此充電速度更快。

- 此外,隨著智慧型手機擴大用於影像應用,MEMS 感測器使得光學影像穩定 (OIS) 和電子影像穩定 (EIS) 的使用成為可能。這些廣泛的特性和創新功能進一步促進了預測期內智慧行動裝置 MEMS 感測器的成長。

- 5G 商業化推動了所研究市場的全球趨勢。例如,向 5G 的過渡加速了對先進行動裝置的需求。根據2022年11月發布的愛立信移動報告,到2028年底,5G行動用戶預計將達到50億。此外,5G人口覆蓋率預計將達到85%,而5G網路預計將承載約70%的行動用戶。交通。由於 5G 需要更多的頻段,此類事件預計也將推動對 RF MEMS 的需求,從而引發對 RF 濾波器的需求。

- MEMS 公司很少有機會使用 MEMS 製造設施或鑄造廠來進行原型和設備製造。此外,大多數預計受益於該技術的組織目前不具備支援 MEMS 製造所需的能力和能力,這直接影響了製造標準化。預計這將阻礙市場的成長。

- COVID-19 對行動裝置市場的影響不大。此外,這場流行病改變了人們對當前全球製造業供應鏈的看法,可能會促使價值鏈更加本地化和進一步區域化,以盡量減少在不久的將來類似的風險。

行動裝置 MEMS 市場趨勢

越來越多的小型化趨勢被接受以推動市場

- 設備的小型化是推動行動裝置中MEMS需求的主要因素之一。隨著終端設備尺寸的縮小,製造商不斷尋找升級技術以獲得效益的方法。隨著行動裝置上感測器數量的增加,需要更小的 MEMS 來滿足設計因素。行動裝置具有接近感應器、加速度計、陀螺儀、指紋感應器、環境光感應器、指南針、霍爾效應感應器、氣壓計等感應器。

- 此外,微型化和聲學特性的改進使得 MEMS 麥克風能夠促進透過智慧型手機視訊分享資訊。 MEMS 麥克風對於主動降噪也很有用,例如在長途飛行中或當您想不受干擾地聽音樂時。

- 全球供應商都致力於進一步縮小 MEMS 的尺寸,以提高其獲得的成本效益。此外,MEMS 感測器製造商正在努力縮小 MEMS 的尺寸,以滿足更小型行動裝置的需求。例如,為了滿足更小型行動裝置的需求,採用 1.5 x 0.8 x 0.55 mm CSP(晶片級封裝)的 SiT15xx MEMS 振盪器與標準 2.0 x 1.2 mm SMD 相比,佔地面積減少了 85% XTAL 封裝。與 XTAL 不同,SiT15xx 系列具有獨特的輸出,可直接驅動晶片組的 XTAL-IN 引腳。

- 在傳統感測器無法有效運作的領域,需要開發具有超小尺寸和高靈敏度的下一代微型加速度計。此外,不斷縮小加速度計的進程促使封裝更小,最終降低了成本。

- 使用石墨烯的基於奈米機電系統 (NEMS) 的加速度計所佔用的晶片面積比傳統矽 MEMS 加速度計小幾個數量級,同時保持有競爭力的靈敏度。設備小型化的趨勢推動了行動裝置中使用的 MEMS 市場。增加更多功率並降低成本和空間的需求仍將是市場創新者的關鍵因素。市場創新者正在依靠這種趨勢為他們的設備添加更多功能,以滿足高效能需求的消費者。

亞太地區預計將出現顯著成長

- 亞太地區一直是最重要的智慧型手機市場之一,這主要歸功於高度發展的電信業和龐大的客戶群。此外,該地區正在加大對先進行動網路的投資。中國、印度、日本、澳洲、新加坡和韓國等國家擴大投資開發國內電信市場,預計這也將推動該地區的市場發展。

- 此外,公司在該地區設立生產中心是因為原料容易取得,而且設立和支付工人的成本較低。

- 印度、中國、韓國和新加坡等國家對手機和其他消費性電子產品的需求不斷成長,鼓勵許多公司在亞太地區設立工廠。

- 根據中國政府提供的最新數據,中國用戶正蜂擁購買昂貴的新型 5G 手機。 2021年中國5G手機出貨量突破2.66億部,較去年成長63.5%。中國資訊通訊研究院(CAICT)的數據顯示,5G手機佔出貨量的75.9%。

- 由於指紋技術可以輕鬆快速地解鎖智慧型手機,因此對 MEMS 感測器的需求不斷成長。指紋認證比依賴密碼和個人識別碼的傳統技術更安全。指紋感測技術在智慧型手機和平板電腦等消費性電子產品中變得越來越普遍。這是因為它很受歡迎並且具有獨特的品質,例如能夠識別每個人的山脊、山谷和小點。

用於行動裝置的 MEMS 產業概述

MEMS 市場充斥著大型供應商,這些供應商能夠進行後向和前向整合,並擁有顯著的創收能力。市場競爭程度中等偏高,在未來幾年可能會變得更糟。

2022 年 10 月,Bosch Sensortec 宣布推出首款 IMU 設備 BMI323,包含 I3C 介面以及 I2C 和 SPI 介面。 BMI323 是一款六軸加速度計和陀螺儀,專為消費品中的運動敏感應用而設計。 BMI323 在高性能模式下(同時使用陀螺儀和加速計)的電流消耗為 790 A,而 BMI160 的電流消耗為 925 A,減少了近 15%。

2022 年 5 月,Analog Devices, Inc. (ADI) 發布了三軸 MEMS 加速度計。與上一代 (ADXL362) 相比,ADXL367 加速度計將功耗降低了一倍,同時將雜訊性能提高了高達 30%。新型加速度計還具有更長的現場時間,從而延長了電池壽命,同時降低了維護頻率和成本。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- 評估 COVID-19 對市場的影響

第 5 章:市場動態

- 市場促進因素

- 小型化趨勢的接受度不斷提高

- 對高性能設備的需求不斷成長

- 市場限制

- 高度複雜的製造流程和嚴苛的周期時間

- 缺乏標準化的製造流程

第 6 章:市場區隔

- 依感測器類型

- 指紋感應器

- 加速度計感測器

- 陀螺儀

- 壓力感測器

- 聲波感測器

- 麥克風

- 其他類型的感測器

- 依地理

- 北美洲

- 歐洲

- 亞太

- 拉丁美洲

- 中東和非洲

第 7 章:競爭格局

- 公司簡介

- Analog Devices Inc.

- Bosch Sensortec GmbH

- STMicroelectronics NV

- InvenSense Inc. (TDK)

- Goertek Inc.

- Knowles Corporation

- Murata Manufacturing

- AAC Technologies

- MEMSIC Inc.

- BSE Co. Ltd

第 8 章:投資分析

第 9 章:市場的未來

The MEMS for Mobile Devices Market size is estimated at USD 9.38 billion in 2024, and is expected to reach USD 14.30 billion by 2029, growing at a CAGR of 8.80% during the forecast period (2024-2029).

With an increase in demand for accelerometers and gyroscopes in smartphones, the MEMS for mobile devices market is expected to grow significantly during the forecast period. For instance, in 2022, the total number of mobile subscriptions globally is expected to reach around 8.4 billion. It is poised to increase further, according to Ericsson forecasts.

Key Highlights

- The studied market has been marked by a trend toward lower power consumption of MEMS devices. Also, changing consumer needs, like faster charging speeds, shorter charging times, and better charging optimization, drive the need for sensors in smart mobile devices. These devices are made to use less power, which makes them charge much faster.

- Moreover, as smartphones are increasingly being used for image applications, the usage of optical image stabilization (OIS) and electronic image stabilization (EIS) is enabled by MEMS sensors. This broad set of features and innovative functions further augments MEMS sensor growth for smart mobile devices in the forecast period.

- Global trends in the market studied are boosted by the commercialization of 5G. For instance, the transition toward 5G accelerates the demand for advanced mobile devices. According to the Ericsson Mobility Report released in November 2022, 5G mobile subscriptions are anticipated to reach 5 billion by the end of 2028. Further, 5G population coverage is projected to reach 85%, while 5G networks are expected to carry around 70% of mobile traffic. Such events are also expected to drive the demand for RF MEMS, owing to the higher number of bands that 5G demands, triggering the demand for RF filters.

- MEMS companies have minimal access to MEMS fabrication facilities or foundries for prototypes and device manufacture. Also, most organizations expected to benefit from this technology do not currently have the required capabilities and competencies to support MEMS fabrication, directly impacting fabrication standardization. This is expected to hinder the market's growth.

- The effect of COVID-19 on the mobile device market has been moderate. Moreover, the pandemic changed the perception of the current global supply chain in manufacturing, potentially leading to more localized value chains and further regionalization to minimize similar risks in the near future.

MEMS for Mobile Devices Market Trends

Increasing Acceptance of Miniaturization Trend to Drive the Market

- The miniaturization of devices is one of the major factors driving the demand for MEMS in mobile devices. With the size of end devices shrinking, manufacturers continuously look for ways to upgrade their technology to reap benefits. As the number of sensors on a mobile device increases, the need for smaller MEMS is required to fulfill design factors. Mobile devices have sensors like proximity sensors, accelerometers, gyroscopes, fingerprint sensors, ambient light sensors, compasses, hall effect sensors, barometers, and others.

- Furthermore, miniaturization and improvements in their acoustic properties have enabled MEMS microphones to facilitate the sharing of information through smartphone videos. MEMS microphones are also useful for active noise cancellation, like on long-distance flights or when you want to listen to music without being disturbed.

- Vendors worldwide are focusing on reducing the size of MEMS further to enhance the cost benefits it reaps. Furthermore, the manufacturers of MEMS sensors are pushing to reduce the size of MEMS to meet the need for smaller mobile devices. For instance, in order to support the demand for even smaller mobile devices, the SiT15xx MEMS oscillators available in 1.5 x 0.8 x 0.55 mm CSPs (chip-scale packages) reduce footprint by as much as 85% compared to standard 2.0 x 1.2 mm SMD XTAL packages. Unlike XTALs, the SiT15xx family has a unique output that directly drives the chipset's XTAL-IN pin.

- In areas where traditional sensors cannot efficiently operate, developing next-generation micro-accelerometers with ultra-small dimensions and high sensitivity is required. Also, the constant process of making accelerometers smaller has led to smaller packages and, in the end, lower costs.

- Nano Electromechanical Systems (NEMS)-based accelerometers using graphene occupy orders of magnitude smaller die areas than conventional silicon MEMS accelerometers while retaining competitive sensitivities. Such trends in the miniaturization of devices drive the market for MEMS used in mobile devices. The need to add more power and reduce cost and space will remain a key factor for innovators in the market. Market innovators are banking on such trends to add more functionalities to their devices for high-performance-demanding consumers.

Asia Pacific is Expected to Witness Significant Growth

- The Asia-Pacific region has been one of the most significant markets for smartphones, primarily due to the highly developing telecom sector and large customer base. Furthermore, the region is increasingly investing in advanced mobile networks. Countries such as China, India, Japan, Australia, Singapore, and South Korea are increasingly investing in developing their domestic telecom markets, which are also expected to drive the market in the region.

- Also, companies set up their production centers in the area because raw materials are easy to get and there are low costs to set up and pay workers.

- Growing demand for mobile phones and other consumer electronics products from countries such as India, China, the Republic of Korea, and Singapore is encouraging many companies to set up factories in the Asia-Pacific region.

- According to the most recent figures given by the Chinese government, Chinese subscribers are flocking to buy pricey new 5G cellphones. China's 5G phone shipments surpassed 266 million units in 2021, an increase of 63.5 percent over the previous year. Data from the China Academy of Information and Communications Technology (CAICT) shows that 75.9% of all mobile phones shipped were 5G.

- There is a growing need for MEMS sensors because of the ease and speed with which fingerprint technology allows smartphones to be unlocked. Fingerprint authentication is more secure than traditional techniques, which rely on passwords and personal identification numbers. Fingerprint sensing technology is becoming more common in consumer electronics like smartphones and tablets. This is because it is popular and has unique qualities, like being able to recognize each person's ridges, valleys, and small points.

MEMS for Mobile Devices Industry Overview

The MEMS market is riddled with large-scale vendors that are capable of both backward and forward integration and command significant revenue generation capabilities. The level of competition in the market is moderately high, and it is likely to get worse in the years to come.

In October 2022, Bosch Sensortec announced its first IMU device, the BMI323, to include the I3C interface and the I2C and SPI interfaces. The BMI323 is a six-axis accelerometer and gyroscope designed for motion-sensitive applications in consumer goods. The BMI323 has a current consumption of 790 A in high-performance mode, using both the gyroscope and the accelerometer, compared to 925 A on the BMI160, representing a nearly 15% reduction.

In May 2022, Analog Devices, Inc. (ADI) released a three-axis MEMS accelerometer. The ADXL367 accelerometer reduces power consumption twice compared to the previous generation (ADXL362) while improving noise performance by up to 30%. The new accelerometer also has a longer field time, which increases battery life while decreasing maintenance frequency and cost.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Acceptance of Miniaturization Trend

- 5.1.2 Increasing Demand for High-Performance Devices

- 5.2 Market Restraints

- 5.2.1 Highly Complex Manufacturing Process and Demanding Cycle Time

- 5.2.2 Lack of Standardized Fabrication Process

6 MARKET SEGMENTATION

- 6.1 By Type of Sensor

- 6.1.1 Fingerprint Sensor

- 6.1.2 Accelerometer Sensor

- 6.1.3 Gyroscope

- 6.1.4 Pressure Sensor

- 6.1.5 BAW Sensor

- 6.1.6 Microphones

- 6.1.7 Other Types of Sensors

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia-Pacific

- 6.2.4 Latin America

- 6.2.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Analog Devices Inc.

- 7.1.2 Bosch Sensortec GmbH

- 7.1.3 STMicroelectronics NV

- 7.1.4 InvenSense Inc. (TDK)

- 7.1.5 Goertek Inc.

- 7.1.6 Knowles Corporation

- 7.1.7 Murata Manufacturing

- 7.1.8 AAC Technologies

- 7.1.9 MEMSIC Inc.

- 7.1.10 BSE Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

全球 MEMS 市場:按感測器類型(慣性感測器、壓力感測器、麥克風)、致動器類型(光學、高頻)、產業(汽車、CE 產品、工業)、地區 - 預測(截至 2029 年)

全球 MEMS 市場:按感測器類型(慣性感測器、壓力感測器、麥克風)、致動器類型(光學、高頻)、產業(汽車、CE 產品、工業)、地區 - 預測(截至 2029 年) 中國的微機電系統(MEMS)市場

中國的微機電系統(MEMS)市場 全球醫療MEMS市場

全球醫療MEMS市場 電子機械系統市場至2030年的預測:按感測器類型、致動器類型、製造方法、材料、最終用戶和地區的全球分析

電子機械系統市場至2030年的預測:按感測器類型、致動器類型、製造方法、材料、最終用戶和地區的全球分析 MEMS -市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測

MEMS -市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測 微機電系統感測器市場,按產品類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

微機電系統感測器市場,按產品類型、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測 全球微機電系統市場規模研究與預測,按類型、按應用和區域分析,2023-2030

全球微機電系統市場規模研究與預測,按類型、按應用和區域分析,2023-2030 微機電系統市場 - 2018-2028F 全球產業規模、佔有率、趨勢、機會與預測,按產品類型、材料、按應用、地區細分

微機電系統市場 - 2018-2028F 全球產業規模、佔有率、趨勢、機會與預測,按產品類型、材料、按應用、地區細分 電子機械系統 (MEMS) 技術:目前與未來市場

電子機械系統 (MEMS) 技術:目前與未來市場 RF(無線電頻率)MEMS的全球市場 2023-2027

RF(無線電頻率)MEMS的全球市場 2023-2027