|

市場調查報告書

商品編碼

1443919

服務機器人:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Service Robotics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

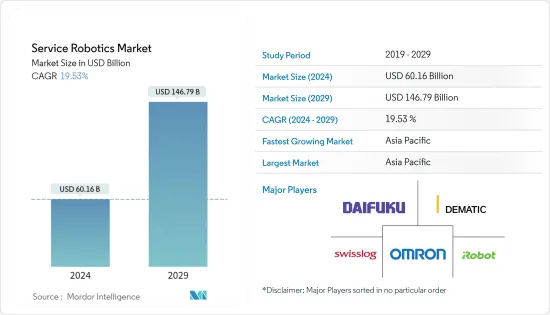

服務機器人市場規模預計到 2024 年為 601.6 億美元,預計到 2029 年將達到 1,467.9 億美元,預測期(2024-2029 年)年複合成長率為 19.53%。

服務機器人因其能夠提供準確和高品質的服務、減少人為錯誤並降低營運成本而受到很高的需求。此外,技術創新帶來的服務機器人能力的快速普及也是推動市場成長的關鍵因素之一。

主要亮點

- 由於技術進步和更實惠的機器人的開發,服務機器人,無論是個人(例如家庭使用、娛樂應用)還是專業用途(例如國防、安全、醫療支持),都越來越受到公眾的普及。變得非常受歡迎。消費者。國際機器人聯盟(IFR)資料顯示,2021年專業服務機器人銷售成長約37%。

- 感知、互動和操作方面的創新使服務機器人更具吸引力。技術和其他組件的提供者一直在推動機器人生態系統的發展。例如,ABB 最近與瑞士新興企業SevenSense 建立了策略合作夥伴關係,利用人工智慧 (AI) 和 3D 視覺映射等技術為 ABB 的新型自主移動機器人 (AMR) 產品提供支援。

- 日本和中國等多個國家的人口老化也推動了醫療技術領域的成長,從而為該地區的服務機器人創造了巨大的市場。例如,根據日本政府2022年9月公佈的資料,日本75歲及以上的人口數量首次超過總人口的15%。這些趨勢鼓勵企業投資老年人產品,為服務機器人提供者創造了巨大的機會。

- 服務機器人通常用於個人/家庭用途,例如吸塵和清潔地板、幫助老年人和娛樂。不過,一些供應商現在開始考慮新的案例,包括在酒店和機場休息室向顧客運送食物和飲料、在酒店辦理入住和退房服務,甚至運輸行李等,重點是設計機器人來執行任務例如,服務機器人的需求不斷增加。

- 然而,服務機器人的認知度低和成本高等因素,特別是在發展中地區,對所研究市場的成長構成了挑戰。此外,操作這些機器人還需要一些技術知識,這對市場成長構成了重大挑戰。

- 冠狀病毒感染疾病(COVID-19)大流行的爆發對所研究市場的成長產生了各種影響。在早期階段,大多數國家實施了大規模封鎖,嚴重擾亂了供應鏈,使機器人製造商難以提高產量。然而,需求正在上升,特別是在醫療保健和個人應用領域,並且預計在預測期內將持續下去。

服務機器人市場趨勢

專業使用機器人佔領大量市場佔有率

- 專業機器人包括野外機器人、國防安全機器人、醫療輔助機器人(MAR)、公共助理機器人、電氣工業機器人、建築機器人等。數位技術和自動化解決方案在這些領域的日益滲透正在增加對專業機器人的需求。

- 例如,在建設產業,正在引入服務機器人來克服人事費用高、人手不足和事故等問題。它還有助於建造更可靠的建築物,因為人為錯誤的可能性較小。 3D列印和拆除機器人等技術將進一步成為機器人引入建築領域的催化劑。

- 外骨骼機器人用作公關機器人。大多數的公關機器人都是用來幫助客戶尋找產品或完成任務。這些機器人正在零售業中部署,以引導商店和服務業、銀行、購物中心、家庭娛樂中心等場所的顧客。

- 商務用機器人的主要應用領域包括交通、餐旅服務業、醫療、專業清潔和農業。去年,交通運輸業是專業機器人的主要消費者之一。例如,根據 IFR 的數據,2021 年售出約 121,000 台專業服務機器人,其中三分之一以上用於運輸貨物和貨物。

- 服務機器人用於各種醫療和保健應用,包括診斷系統、機器人輔助手術和治療以及復健系統。 COVID-19感染疾病的爆發在推動各行業對機器人的需求方面發揮了重要作用。例如,根據IFR 2021,2021年醫療機器人銷售成長23%,出貨達到14,823台。

亞太地區將呈現顯著的成長率

- 由於擁有龐大的消費群,亞太地區是全球成長最快的地區之一,其中中國、日本、韓國和印度等國家對服務機器人的需求尤其強勁。除其他事項外。例如,根據IFR的數據,2021年亞洲專業機器人的銷售量成長了約30%。

- 地方政府也是區域機器人市場發展的重要因素。例如,印度計劃投資軍用機器人,並準備在未來幾年部署先進的機器人士兵。這點從2022年1月全印度機器人協會(AIRA)宣布開始國產國防機器人就可以看出來。

- 該地區其他國家也出現了類似的趨勢。例如,中國政府對國內機器人產業制定了雄心勃勃的計畫。政府已將機器人產業確定為高階發展的優先領域之一,與人工智慧(AI)和自動化並列,以推動製造業的轉型和複雜化。這一推動可望提高中國製造機器人的全球市場佔有率。

- 此外,亞洲金融服務公司的目標是增加股東股息,精簡成本以維持盈利,並擁有新工具來吸引客戶,例如服務機器人。

- 日本和中國等一些主要國家的老年人口也出現了顯著成長。根據聯合國經濟社會事務部和中國國家統計局測算,2050年,60歲以上人口比例預計將增加至38.81%左右。預計這些趨勢將推動對服務機器人的需求。在國內。

服務機器人產業概況

由於領先公司在市場上佔有重要地位,服務機器人市場適度整合。然而,隨著需求的增加,新參與企業也不斷進入市場,競爭和市場正走向分散階段。供應商正在採取各種策略,包括產品創新、合作、收購等,以進一步加強其在市場上的影響力。主要參與者包括DAIFUKU CO. LTD.、Dematic Corp.、Swisslog Holding AG 和 iRobot Corporation。

2022 年 9 月,加拿大機器人公司 Avidbots 在 C 輪資金籌措中籌集了 7,000 萬美元。該公司主要研發自主清潔機器人,並開發了Neo 2,這是一款專為倉庫、機場、商場等商業環境設計的掃地機器人。

2022年9月,領先的B2B技術解決方案供應商Jacky's Business Solutions在Gitex活動上展示了最新版本的Temi Robot(V3)。該公司在中東推出了這款新型個人援助機器人,採用機器人即服務(RaaS)經營模式。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 競爭公司之間的敵意強度

- 替代品的威脅

- 評估 COVID-19 對產業的影響

第5章市場動態

- 市場促進因素

- 由於充滿活力的行業和機器人創新,對自動化解決方案的需求增加

- 醫療保健領域對專業機器人的需求不斷增加

- 市場限制因素

- 安裝和維護高成本

第6章市場區隔

- 按應用領域

- 專業的

- 野外機器人

- 專業清潔

- 檢查/維護

- 建造和拆除

- 物流系統(製造/非製造)

- 醫療機器人

- 救援和安全機器人

- 防禦機器人

- 水下系統(民用/通用)

- 動力人類體外骨骼

- 公關機器人

- 個人/國內

- 家務機器人

- 娛樂機器人

- 對老年人和殘障人士的支持

- 專業的

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 世界其他地區

第7章 競爭形勢

- 公司簡介

- Daifuku Co. Ltd

- Dematic Corp.

- Swisslog Holding AG(KUKA)

- Seegrid Corporation

- Omron Corporation

- JBT Corporation

- SSI Schaefer AG

- Grenzebach GmbH &Co. KG

- Smith &Nephew PLC

- Stryker Corp.

- Intuitive Surgical Inc.

- Knightscope Inc.

- Kollmorgen Corporation

- Brokk AB

- Husqvarna AB

- Construction Robotics LLC

- iRobot Corporation

- Ecovacs Robotics

- Neato Robotics

- Transbotics Corporation

- Medtronic PLC

- Northrop Grumman

- BAE Systems

- UBTECH Robotics Inc.

- SMP Robotics Systems Corp.

- Vision Robotics Corporation

- Naio Technologies SAS

第8章投資分析

第9章 市場未來展望

The Service Robotics Market size is estimated at USD 60.16 billion in 2024, and is expected to reach USD 146.79 billion by 2029, growing at a CAGR of 19.53% during the forecast period (2024-2029).

Service robots offer several features, such as delivering precise and high-quality service and helping users reduce human mistakes and operational expenses, due to which their demand has increased. Additionally, the rapid proliferation of service robot capabilities owing to technological innovations is also among the key factors driving the market's growth.

Key Highlights

- Service robots, both personal (for household, entertainment applications, etc.) and professional (for defense, security, medical assistance, etc.), are gaining significant popularity as technological improvement and the development of affordable robots have significantly enhanced their penetration among general consumers. According to data from the International Federation of Robotics (IFR), sales of professional service robots increased by about 37% in 2021.

- Technological innovations concerning cognition, interaction, and manipulation, have made service robotics more appealing. Technology and other component providers have moved the robotics ecosystem forward. For instance, recently, ABB entered into a strategic partnership with Switzerland-based start-up Sevensense to enhance ABB's new Autonomous Mobile Robotics (AMR) offering with techn ologies such as artificial intelligence (AI) and 3D vision mapping.

- The aging population of several countries, including Japan and China, is also driving the growth in the medical technology sector, thus, creating a massive market for service robotics in the region. For instance, according to the Japanese government's data released in September 2022, for the first time, Japan's over 75s accounted for over 15% of the population. Such trends encourage companies to invest in products for the elderly, which is a massive opportunity for the service robot providers.

- Service robots are usually deployed for personal/household purposes, like vacuum and floor cleaning, elderly assistance, and entertainment. However, several vendors have now started exploring new cases and are focusing on designing robots to perform tasks, such as delivering food and drinks to customers at hotels and airport lounges, handling check-in and check-out services at hotels, and even carrying luggage, which is boosting the demand for service robots.

- However, the factors such as low awareness, especially in developing regions, and the higher cost of service robots are challenging the growth of the studied market. Furthermore, a certain degree of technical know-how is also required to operate these robots, which is a significant challenge for the market's growth.

- The outbreak of the COVID-19 pandemic has had a mixed impact on the growth of the studied market. During the initial phase, the widespread lockdown imposed across most countries significantly disrupted the supply chain, making it difficult for the robot manufacturers to carry out production at full scale. However, the demand has witnessed an upward trend, especially in the healthcare and personal application segment, which is expected to sustain during the forecast period.

Service Robotics Market Trends

Professional Use of Robots to Account for a Significant Share in the Market

- Professional robots consist of field robots, defense, and security robots, medical assisting robots (MAR), public assistant robots, electrical industry robots, and robots for construction purposes. The increasing penetration of digital technologies and automation solutions across these sectors drives the demand for professional robots.

- For instance, service robots are deployed in the construction industry to overcome heavy labor costs, shortages, and accidents. It also helps construct more reliable buildings since there is less chance of human error. Technologies like 3D printing and demolition robots further act as catalysts in adopting robots in the construction sector.

- Exoskeleton robots are used as public relations robots. Most public relations robots are used to assist customers in finding an item or completing a task. These robots are deployed in retail to guide customers around a store and in the hospitality industry, banks, shopping malls, family entertainment centers, and more.

- Major application areas for professional robots are transportation, hospitality, medical, professional cleaning, and agriculture. Transportation was among the leading consumer of professional robots in the aforementioned year. For instance, according to IFR, about 121,000 professional service robots were sold in 2021 - more than one out of every three built were targeted for the transportation of cargo and goods.

- Service robots are used in medical and healthcare for various applications, including diagnostic systems, robot-assisted surgery or therapy, rehabilitation systems, etc. The outbreak of the COVID-19 pandemic played an important role in driving the demand for robots across the sector. For instance, according to IFR 2021, a 23% growth in the sales of medical robots was recorded in 2021, with the number of shipments touching 14,823 units.

Asia Pacific to Exhibit a Significant Growth Rate

- The Asia Pacific is one of the fastest-growing regions in the world, owing to the presence of a large consumer base, among which the demand for service robots is increasing, especially in countries such as China, Japan, South Korea, and India, among others. For instance, according to IFR, in 2021, the sales of professional robots grew by about 30% in Asia.

- Regional governments are also a significant factor in developing a regional robotics market. For instance, India plans to invest in military robotics, and the country is preparing to deploy advanced robotic soldiers in the next few years. This is evident from the fact that in January 2022, the All India Robotics Association (AIRA) announced the beginning of indigenous manufacturing of defense robots.

- A similar trend has been observed across other countries of the region as well. For instance, the Chinese government has ambitious plans for the country's robotics industry. The government has listed the robotics industry, along with artificial intelligence (AI) and automation, as one of the priority sectors for high-end development to push forward the transformation and upgradation of the manufacturing industry. This push is expected to raise the global market share of Chinese-made robots.

- Further, financial services companies in Asia are looking to streamline costs to boost dividends to shareholders, maintain profitability, and have a new tool at their disposal that appeals to customers, for example, service robots.

- Some major countries, such as Japan, China, etc., are also witnessing significant growth in the aged population. According to the estimation of UN DESA and the National Bureau of Statistics of China (NBSC), the percentage of the population aged 60 and above is expected to grow to about 38.81% by 2050. Such trends are expected to drive the demand for service robots in the country.

Service Robotics Industry Overview

The Service Robotics market is moderately consolidated, as major players have a significant market presence. However, with the demand growing, new players are also entering the market, driving competition and the market toward a fragmented stage. Vendors are adopting various strategies to consolidate further their market presence, including product innovation, partnerships, acquisitions, etc. Some major players include Daifuku Co. Ltd, Dematic Corp., Swisslog Holding AG, and iRobot Corporation.

In September 2022, Avidbots, a robotics company based in Canada, raised USD 70 million in the Series C funding round. The company primarily develops autonomous cleaning robots and has built Neo 2, a robotic floor cleaner designed for commercial environments such as warehouses, airports, and shopping malls.

In September 2022, Jacky's Business Solutions, a leading B2B technology solutions provider, announced a showcase of its latest iteration of Temi Robot (V3) at the Gitex event. The company launched this new personal assistance robot in the Middle East with Robot-as-a-service (RaaS) business model.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 Assessment of COVID-19 impact on the industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Automated Solutions from Dynamic Industries and Robot Innovations

- 5.1.2 Increased Demand for Professional Robots in Healthcare

- 5.2 Market Restraints

- 5.2.1 High Cost of Installation and Maintenance

6 MARKET SEGMENTATION

- 6.1 By Field of Application

- 6.1.1 Professional

- 6.1.1.1 Field Robots

- 6.1.1.2 Professional Cleaning

- 6.1.1.3 Inspection and Maintenance

- 6.1.1.4 Construction and Demolition

- 6.1.1.5 Logistics Systems (Manufacturing and Non-manufacturing)

- 6.1.1.6 Medical Robots

- 6.1.1.7 Rescue and Security Robots

- 6.1.1.8 Defense Robots

- 6.1.1.9 Underwater Systems (Civil/General)

- 6.1.1.10 Powered Human Exoskeletons

- 6.1.1.11 Public Relation Robots

- 6.1.2 Personal/Domestic

- 6.1.2.1 Robots for Domestic Tasks

- 6.1.2.2 Entertainment Robots

- 6.1.2.3 Elderly and Handicap Assistance

- 6.1.1 Professional

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia Pacific

- 6.2.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daifuku Co. Ltd

- 7.1.2 Dematic Corp.

- 7.1.3 Swisslog Holding AG (KUKA)

- 7.1.4 Seegrid Corporation

- 7.1.5 Omron Corporation

- 7.1.6 JBT Corporation

- 7.1.7 SSI Schaefer AG

- 7.1.8 Grenzebach GmbH & Co. KG

- 7.1.9 Smith & Nephew PLC

- 7.1.10 Stryker Corp.

- 7.1.11 Intuitive Surgical Inc.

- 7.1.12 Knightscope Inc.

- 7.1.13 Kollmorgen Corporation

- 7.1.14 Brokk AB

- 7.1.15 Husqvarna AB

- 7.1.16 Construction Robotics LLC

- 7.1.17 iRobot Corporation

- 7.1.18 Ecovacs Robotics

- 7.1.19 Neato Robotics

- 7.1.20 Transbotics Corporation

- 7.1.21 Medtronic PLC

- 7.1.22 Northrop Grumman

- 7.1.23 BAE Systems

- 7.1.24 UBTECH Robotics Inc.

- 7.1.25 SMP Robotics Systems Corp.

- 7.1.26 Vision Robotics Corporation

- 7.1.27 Naio Technologies SAS

8 INVESTMENT ANALYSIS

9 FUTURE OUTLOOK OF THE MARKET

全球服務機器人市場:市場規模、佔有率、成長分析 - 按類型、應用、產業預測(2024-2031)

全球服務機器人市場:市場規模、佔有率、成長分析 - 按類型、應用、產業預測(2024-2031) 2024 年服務機器人世界市場報告

2024 年服務機器人世界市場報告 2024年專業服務機器人全球市場報告

2024年專業服務機器人全球市場報告 專業服務機器人市場:按組件、環境和應用分類 - 2024-2030 年全球預測

專業服務機器人市場:按組件、環境和應用分類 - 2024-2030 年全球預測 全球商業服務機器人市場評估:按機器人類型、配置、控制、產業、地區、機會、預測(2016-2030)

全球商業服務機器人市場評估:按機器人類型、配置、控制、產業、地區、機會、預測(2016-2030) 服務機器人市場:按類型、按應用分類:全球機會分析與產業預測,2023-2032年

服務機器人市場:按類型、按應用分類:全球機會分析與產業預測,2023-2032年 服務機器人市場 - 按組件(機器人、週邊設備)、按機器人(專業、個人家庭、娛樂)和預測,2023 年 - 2032 年

服務機器人市場 - 按組件(機器人、週邊設備)、按機器人(專業、個人家庭、娛樂)和預測,2023 年 - 2032 年 全球服務機器人市場

全球服務機器人市場 服務機器人市場:按組件(硬體、軟體)、操作環境(空中、地面、海上)、用途- 2023-2030 年全球預測

服務機器人市場:按組件(硬體、軟體)、操作環境(空中、地面、海上)、用途- 2023-2030 年全球預測 服務機器人的全球市場(各類型),服務機器人廠商/供應商分析,主要加入企業的機器人部門銷售額,及最近的發展-至2027年的預測

服務機器人的全球市場(各類型),服務機器人廠商/供應商分析,主要加入企業的機器人部門銷售額,及最近的發展-至2027年的預測