|

市場調查報告書

商品編碼

1440233

太陽能:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Solar Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

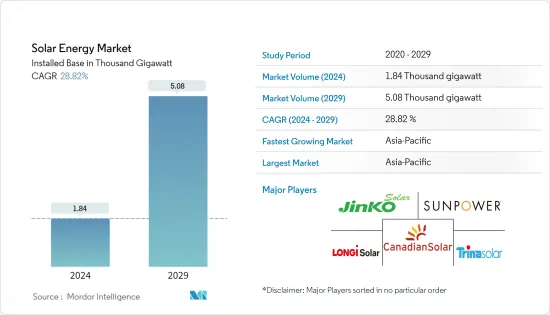

從裝置容量來看,太陽能市場規模預計將從2024年的1,840吉瓦成長到2029年的5,080吉瓦,預測期間(2024-2029年)年複合成長率為28.82%。

主要亮點

- 從中期來看,由於有利的政府政策以及太陽能板價格和安裝成本的下降,太陽能發電系統的採用不斷增加,可能會在預測期內支持全球太陽能市場的成長。

- 另一方面,擴大採用替代清潔能源(例如燃氣發電廠、陸上和離岸風電計劃)等因素可能會阻礙研究期間的市場成長。

- 儘管如此,太陽能發電設備成本的下降以及透過與能源儲存系統系統整合來增加離網太陽能的使用預計將在未來為市場創造一些機會。

- 在預測期內,亞太地區預計將成為太陽能市場最大且成長最快的地區。這是因為太陽能發電的安裝量正在增加。

太陽能市場趨勢

光伏(PV)預計將主導市場

- 太陽能發電系統使用由半導體材料(通常是矽)製成的太陽能電池板將陽光直接轉化為電能。當陽光照射到太陽能電池時,電子被激發,產生直流 (DC) 電流。使用家庭、企業和電網中的逆變器將直流電轉換為交流電 (AC)。

- 過去十年來,太陽能發電系統的成本迅速下降。這種成本降低是由技術進步、規模經濟和製造流程的改進所推動的。因此,與傳統能源來源相比,太陽能變得更具成本競爭力,並且更容易普及。

- 此外,由於人口成長、都市化以及包括交通在內的各部門的電氣化,全球電力需求持續增加。太陽能發電系統提供了可擴展的分散式解決方案,可滿足不斷成長的能源需求,特別是在電網基礎設施有限或不可靠的地區。

- 根據國際可再生能源機構的數據,2022年至2021年間,全球太陽能發電裝置容量增加了22%以上,而集中式太陽能發電系統僅成長了2%。這顯示太陽能發電比集中式太陽能發電系統的適應性越來越強。

- 此外,世界各國政府正在推出支持政策和財政獎勵,以鼓勵太陽能光電安裝。這些措施包括上網電價補貼、稅額扣抵、補貼和淨計量計劃。此類政策透過降低初始成本、提高投資收益和促進電網整合來鼓勵採用太陽能光電系統。

- 例如,澳洲制定了2030年82%的電力來自太陽能和風能等可再生能源的目標,太陽能發電有望為實現這一目標做出重大貢獻。

- 例如,2022年11月,X-Elio宣布打算在新南威爾斯州沃加沃加附近建造一座300兆瓦容量的太陽能發電場。此外,X-Elio正在開發另外兩個太陽能發電設施:位於新南威爾斯的Forest Glen太陽能發電場,容量為120兆瓦;以及位於維多利亞州的Wunghnu太陽能發電場,容量為80兆瓦,均已啟動。這些計劃是 X-Elio 目前在澳洲開發的超過 500 兆瓦可再生能源計劃的更廣泛投資組合的一部分。

- 因此,基於上述因素,預計公共事業部門將在預測期內主導太陽能市場。

預計亞太地區將主導市場

- 中國、印度和日本等亞太地區許多國家都實施了雄心勃勃的可再生能源目標和支持政策,以加速太陽能的採用。這些政策包括上網電價補貼、可再生能源組合標準、太陽能發電裝置補貼。強而有力的政府支持和穩定的政策框架為該地區太陽能市場的成長創造了有利的環境。

- 例如,根據國際可再生能源機構的數據,2021年至2022年間太陽能總裝置容量增加了110吉瓦以上。 2021年總裝置容量約為485吉瓦,2022年將達到597吉瓦,其中中國和印度占主要裝置容量。

- 此外,亞太國家人口快速成長、經濟不斷擴張,對電力的需求也不斷增加。太陽能為這種不斷成長的能源需求提供了可擴展且永續的解決方案。因此,該地區太陽能部署具有巨大的市場潛力。

- 此外,亞太地區的一些國家正在著手實施雄心勃勃的大型太陽能計劃。例如,中國擁有大型太陽能發電設施和太陽能園區,使其成為公用事業規模太陽能裝置的領導者。這些大型計劃增加了該地區的太陽能累積發電量,並使其成為全球太陽能市場的主導者。

- 2022年3月,阿里巴巴集團物流部門菜鳥網路開始使用中國保稅倉庫安裝的屋頂太陽能板產生的分散式太陽能作為業務用電。該公司在倉庫屋頂10萬平方公尺的地方安裝了太陽能發電系統,可儲存7.862MW的能量,每年發電超過800萬千瓦,足以為3000多個家庭供電。太陽能發電系統產生的電力足以為菜鳥倉庫業務提供電力,多餘的電力將併入電網。此外,菜鳥及其合作夥伴計劃在2023年於菜鳥保稅倉庫安裝屋頂太陽能發電系統,總合達50萬平方公尺。

- 亞太國家,尤其是中國,也正在成為光伏組件和系統的主要製造地。該地區受益於規模經濟、高效的供應鏈和具有競爭力的生產成本,顯著降低了太陽能系統的整體成本。這種成本優勢有助於亞太地區在全球太陽能市場上佔據主導地位。

- 因此,上述亞太地區預計將在預測期內主導太陽能市場。

太陽能產業概況

太陽能市場是分散的。市場主要企業包括(排名不分先後)阿特斯陽光電力、晶科能源、天合光能、SunPower Corporation、隆基綠能等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查範圍

- 市場定義

- 調查先決條件

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2028年太陽能發電裝置容量及預測

- 2022 年全球可再生能源結構

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進因素

- 政府激勵措施和政策

- 能源安全

- 抑制因素

- 與其他能源來源的競爭

- 促進因素

- 供應鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 科技

- 太陽能(光伏)

- 概述

- 到 2028 年太陽能 (PV)裝置容量及預測 (GW)

- 2022 年之前太陽能發電年出出貨量(GW)

- 2022 年按技術分類的太陽能出貨量佔有率 (%)

- 2022年光電模組平均售價(美元/瓦)

- 主要計劃資訊

- 聚光太陽能發電(CSP)

- 概述

- 2028年黃金週期間光熱發電(CSP)裝置容量及預測

- 到 2022 年太陽能熱運作中容量(GW)

- 太陽能裝置容量佔有率(%),按集熱器類型分類,2022 年

- 主要計劃資訊

- 太陽能(光伏)

- 區域市場分析{2028年之前的市場規模與需求預測(僅限區域)}

- 北美洲

- 美國

- 墨西哥

- 歐洲

- 德國

- 西班牙

- 義大利

- 英國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 奈及利亞

- 南非

- 中東和非洲

- 北美洲

第6章 競爭形勢

- 併購、合資、合作與協議

- 主要企業採取的策略

- 公司簡介

- Canadian Solar Inc.

- JinkoSolar Holding Co. Ltd.

- Trina Solar Co. Ltd.

- SunPower Corporation

- LONGi Green Energy Technology Co. Ltd.

- First Solar Inc.

- JA Solar Holding

- Abengoa SA

- Acciona SA

- Brightsource Energy Inc.

- Engie SA

- NextEra Energy Inc.

- ACWA Power

- Sharp Corporation

- REC Solar Holdings AS

- Hanwha Corporation

第7章市場機會與未來趨勢

- 能源儲存一體化

簡介目錄

Product Code: 71528

The Solar Energy Market size in terms of installed base is expected to grow from 1.84 Thousand gigawatt in 2024 to 5.08 Thousand gigawatt by 2029, at a CAGR of 28.82% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, favorable government policies and increasing adoption of solar PV systems, with the declining price of solar panels and installation cost, are likely to support the global solar energy market growth during the forecast period

- On the other hand, factors such as rising adoption of alternate clean power sources, such as gas-fired power plants, onshore and offshore wind projects are likely to hinder the market growth during the study period.

- Nevertheless, an increase in off-grid solar utilization due to the decreasing cost of solar PV equipment and integration with energy storage systems are expected to create several opportunities for the market in the future.

- Asia-Pacific region is expected to be the largest and fastest-growing region in the solar energy market during the forecast period. Due to its increasing solar installations.

Solar Energy Market Trends

Solar Photovoltaic (PV) Expected to Dominate the Market

- Solar PV systems convert sunlight directly into electricity using solar panels made up of semiconductor materials, typically silicon. When sunlight strikes the solar cells, it excites electrons, generating a flow of direct current (DC) electricity. This DC electricity is converted into alternating current (AC) using an inverter in homes, businesses, and the electrical grid.

- The cost of solar PV systems has declined rapidly over the past decade. This cost reduction is driven by technological advancements, economies of scale, and improved manufacturing processes. As a result, solar PV has become increasingly cost-competitive with conventional energy sources, making it more attractive for widespread adoption.

- Additionally, the global electricity demand is continuously increasing due to population growth, urbanization, and the electrification of various sectors, including transportation. Solar PV systems offer a scalable and decentralized solution to meet this growing energy demand, particularly in regions with limited or unreliable grid infrastructure.

- According to International Renewable Energy Agency, the global solar photovoltaics installed capacity increased by more than 22% between 2022 and 2021 compared to 2% for concentrated solar power systems. Signifying the increased adaption of solar photovoltaics over concentrated solar power systems.

- Moreover, governments worldwide have introduced supportive policies and financial incentives to promote solar PV installations. These measures include feed-in tariffs, tax credits, grants, and net metering programs. Such policies encourage the adoption of solar PV systems by reducing upfront costs, improving investment returns, and facilitating grid integration.

- For instance, Australia has set a goal of generating 82% of its electricity through renewable sources like solar PV and wind by 2030, and solar PV is expected to be a significant contributor to achieving this target.

- For instance, in November 2022, X-Elio unveiled its intention to construct a solar photovoltaics farm with a capacity of 300 MW near Wagga Wagga, New South Wales. Additionally, X-Elio has initiated the development of two other solar photovoltaics farms, namely the Forest Glen Solar Farm, with a capacity of 120 MW in New South Wales, and the WunghnuSolar Farm, with a capacity of 80 MW in Victoria. These projects form part of X-Elio's extensive portfolio, comprising more than 500 MW of renewable energy projects currently under development in Australia.

- Therefore, based on the abovementioned factors, the utility sector is expected to dominate the solar energy market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- Many countries in the Asia-Pacific region, such as China, India, and Japan, have implemented ambitious renewable energy targets and supportive policies to encourage solar energy adoption. These policies include feed-in tariffs, renewable portfolio standards, and subsidies for solar installations. Strong government support and stable policy frameworks have created a conducive environment for the region's solar energy market growth.

- For instance, according to the International Renewable Energy Agency, the total solar energy installed capacity between 2021 and 2022 grew by more than 110 GW. In 2021 the total installed capacity was around 485 GW, whereas in 2022, it reached 597 GW, with China and India holding major installed capacity.

- Furthermore, the Asia-Pacific countries have a rapidly growing population and expanding economies, leading to an increasing demand for electricity. Solar energy offers a scalable and sustainable solution to this growing energy demand. As a result, there is a strong market potential for solar energy deployment in the region.

- Moreover, several countries in the Asia-Pacific region have undertaken ambitious large-scale solar energy projects. For instance, China has been a leader in utility-scale solar installations, with extensive solar farms and solar parks. These large-scale projects have boosted the cumulative solar capacity in the region and positioned it as a dominant player in the global solar market.

- In March 2022, Alibaba Group's logistics arm Cainiao Network started to use distributed solar power generated by rooftop solar panels installed in its bonded warehouses in China to power its operations. The company had installed the PV power generation systems on 100,000 square meters of warehouse rooftops, which can store 7.862 MW of energy, with an annual power output of over 8 million kilowatts per hour, enough to power more than 3,000 homes. The power generated by the solar power system will be sufficient to power Cainiao's warehouse operations, and excess electricity will be diverted to the grid. Further, by 2023, Cainiao and its partners expect to install rooftop PV generation systems on Cainiao's bonded warehouses spanning a combined 500,000 square meters.

- Asia-Pacific countries, particularly China, have also emerged as major manufacturing hubs for solar PV components and systems. The region benefits from economies of scale, efficient supply chains, and competitive production costs, significantly reducing the overall cost of solar energy systems. This cost advantage has contributed to the dominance of the Asia-Pacific region in the global solar energy market.

- Therefore, the Asia-Pacific, as mentioned above region, is expected to dominate the solar energy market during the forecasted period.

Solar Energy Industry Overview

The solar energy market is fragmented. Some of the key players in the market (in no particular order) include Canadian Solar Inc., JinkoSolar Holding Co. Ltd, Trina Solar Co. Ltd, SunPower Corporation, and LONGi Green Energy Technology Co. Ltd. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Solar Energy Installed Capacity and Forecast, till 2028

- 4.3 Global Renewable Energy Mix, 2022

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Government Incentives and Policies

- 4.6.1.2 Energy Security

- 4.6.2 Restraints

- 4.6.2.1 Competition from Other Energy Sources

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGEMENTATION

- 5.1 Technology

- 5.1.1 Solar Photovoltaic (PV)

- 5.1.1.1 Overview

- 5.1.1.2 Solar Photovoltaic (PV) Installed Capacity and Forecast, in GW, till 2028

- 5.1.1.3 Annual Solar PV Shipments, in GW, till 2022

- 5.1.1.4 Share of Solar PV Shipments (%), by Technology, 2022

- 5.1.1.5 Average Selling Price of Solar PV Module, in USD/W, till 2022

- 5.1.1.6 Key Projects Information

- 5.1.2 Concentrated Solar Power (CSP)

- 5.1.2.1 Overview

- 5.1.2.2 Concentrated Solar Power (CSP) Installed Capacity and Forecast, in GW, till 2028

- 5.1.2.3 Solar Thermal Capacity in Operation, in GW, till 2022

- 5.1.2.4 Solar Thermal Installed Capacity Share (%), by Collector Type, 2022

- 5.1.2.5 Key Projects Information

- 5.1.1 Solar Photovoltaic (PV)

- 5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 Spain

- 5.2.2.3 Italy

- 5.2.2.4 United Kingdom

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Chile

- 5.2.4.4 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 Egypt

- 5.2.5.4 Nigeria

- 5.2.5.5 South Africa

- 5.2.5.6 Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Canadian Solar Inc.

- 6.3.2 JinkoSolar Holding Co. Ltd.

- 6.3.3 Trina Solar Co. Ltd.

- 6.3.4 SunPower Corporation

- 6.3.5 LONGi Green Energy Technology Co. Ltd.

- 6.3.6 First Solar Inc.

- 6.3.7 JA Solar Holding

- 6.3.8 Abengoa SA

- 6.3.9 Acciona SA

- 6.3.10 Brightsource Energy Inc.

- 6.3.11 Engie SA

- 6.3.12 NextEra Energy Inc.

- 6.3.13 ACWA Power

- 6.3.14 Sharp Corporation

- 6.3.15 REC Solar Holdings AS

- 6.3.16 Hanwha Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Energy Storage Integration

02-2729-4219

+886-2-2729-4219

太陽能系統市場:按組件、技術、來源、部署和最終用戶分類 - 2024-2030 年全球預測

太陽能系統市場:按組件、技術、來源、部署和最終用戶分類 - 2024-2030 年全球預測 太陽能全球市場規模、佔有率和成長分析:按技術和應用分類 - 產業預測(2024-2031)

太陽能全球市場規模、佔有率和成長分析:按技術和應用分類 - 產業預測(2024-2031) 全球太陽能組件市場規模、佔有率、成長分析(按類型、最終用途)- 產業預測,2024-2031 年

全球太陽能組件市場規模、佔有率、成長分析(按類型、最終用途)- 產業預測,2024-2031 年 到 2030 年太陽能市場預測 - 各產品類型、技術、提供的服務、太陽能組件、應用、最終用戶和地理位置的全球分析

到 2030 年太陽能市場預測 - 各產品類型、技術、提供的服務、太陽能組件、應用、最終用戶和地理位置的全球分析 全球太陽能光伏發電市場預測 最新資訊:2024年第一季

全球太陽能光伏發電市場預測 最新資訊:2024年第一季 南美的太陽能光伏發電系統的價格 2024年

南美的太陽能光伏發電系統的價格 2024年 2024 年太陽能世界市場報告

2024 年太陽能世界市場報告 光伏 (PV) 材料市場 - 2024 年至 2029 年預測

光伏 (PV) 材料市場 - 2024 年至 2029 年預測 全球商業和工業太陽能光伏組件市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測

全球商業和工業太陽能光伏組件市場研究報告 - 2024 年至 2032 年行業分析、規模、佔有率、成長、趨勢和預測 全球地面安裝太陽能光電市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球地面安裝太陽能光電市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

▼