|

市場調查報告書

商品編碼

1438400

專案物流 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Project Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

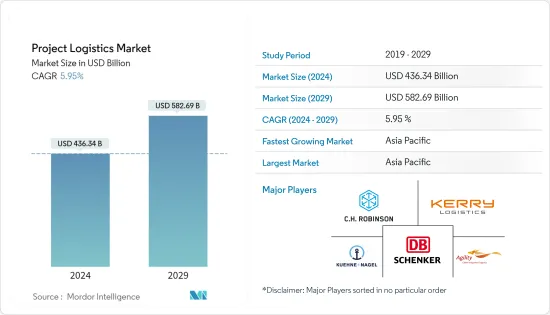

專案物流市場規模預計到2024年為4,363.4億美元,預計到2029年將達到5,826.9億美元,在預測期內(2024-2029年)CAGR為5.95%。

專案物流是指對專案全過程中的貨物、材料、資訊的綜合管理和協調。大型貨物的運輸需要專門的設備、基礎設施和經驗豐富的人員。處理獨特尺寸的貨物對運輸商來說是一個持續的課題,但托運人和服務提供者越來越擅長處理超大和超重的貨物。製造的複雜性也增加了難度,因為零件和模組化包裝在不同地點生產,然後運送到最終目的地,需要精心規劃。近年來,運輸提供者參與規劃過程的早期階段的趨勢日益明顯。

亞太地區在專案物流市場處於領先地位,預計成長率最高。基礎設施投資對亞太國家經濟發展發揮重要作用,一些國家優先發展本國基礎設施。

全球專案物流網路 (GPLN) 等一些知名組織專門從事全球範圍內的專案物流。 GPLN 成員處理廣泛的工業項目,包括基礎設施和能源項目,提供運輸、包裝/裝箱以及重型、超大和超限貨物的起重等服務。

在 2020-21 年 COVID-19 大流行最嚴重期間,專案物流領域對空運的需求很高,用於在全球範圍內運輸必需品。

專案物流市場趨勢

增加再生能源的使用為專案物流公司帶來機會

根據國際能源總署的最新報告,由於政策支持力度加大、化石燃料價格上漲以及對能源安全的擔憂等因素,預計2023年全球再生能源發電容量將增加三分之一。

這一成長動能明年也將持續,全球再生能源發電總量將達到4500吉瓦,相當於中國和美國發電量的總和。到 2023 年,全球再生能源發電量預計將增加 107 吉瓦,這是有史以來最大的絕對增幅,達到 440 吉瓦以上。

這種擴張正在全球主要市場進行,其中歐洲、美國、印度和中國處於領先地位。尤其是中國,預計 2023 年和 2024 年將佔全球再生能源新增裝置容量的近 55%。

預計2023年風電裝置將出現顯著復甦,預計較上年成長近70%。這是在該行業經歷了一段充滿課題的緩慢成長時期之後發生的。成長的改善可歸因於因中國的 COVID-19 限制以及歐洲和美國的供應鏈問題而推遲的項目的完成。

然而,2024 年的成長程度將取決於政府是否能夠提供更多政策支援來解決與許可和拍賣設計相關的障礙。與太陽能光電產業不同,風力渦輪機供應鏈的擴張速度不夠快,無法跟上中期內不斷成長的需求。這主要是由於大宗商品價格上漲和供應鏈困難影響了製造商的獲利能力。

這種再生能源需求涵蓋了專案物流,因為機器和其他零件非常巨大,需要單獨運輸,然後在現場組裝。

不斷成長的模組化建築推動市場

對永續基礎設施的需求正在推動高效、環保的建築技術的發展。傳統的施工方法可能不再足以滿足永續基礎設施的要求。模組化為傳統施工方法的不靈活性提供了解決方案。透過採用模組化施工,施工成本可降低40%,並且現場準備和模組化預製活動可以同時進行。

向模組化(異地)施工方法的轉變創造了一個新的市場,特別是對於勞動力成本較低且預製區土地充足的發展中國家。在支援永續基礎設施發展方面,預製方法可以顯著節省材料,例如與類似規模的傳統施工方法相比,可減少 60% 的鋼材、56% 的混凝土和 77% 的模板。

然而,模組化預製概念仍存在課題,例如規模經濟性以及運輸超過 ISO 貨櫃尺寸的模組化組件的複雜性。這種異地建設模式也為特定地理區域內的國際貿易開闢了機會,這取決於每個國家的競爭優勢。國際自由貿易的發展為新的貿易聯繫提供了更廣泛的商機和潛力。國際和區域貿易也增加了工程、採購和施工(EPC)項目的海外貿易。海外EPC專案採用模組化建設的決定,影響了專案貨物運輸的發展以及專案物流的整體投資,包括境內外的物流成本。國內物流成本包括製造成本(加工費、預拌混凝土、散裝材料、螺紋鋼、鋼材)。相較之下,海外物流成本包括船舶租賃費率、燃油定價、貨幣兌換、距離、體積尺寸、保險和清關。

項目物流行業概況

專案物流市場較為分散,既有全球參與者,也有中小型本地參與者。大多數全球物流公司都有專門的專案貨運部門來滿足市場需求和需求。本地企業也不斷增強在機隊規模、服務產品、服務業和技術方面的能力。全球製造商正在工廠現場(場外)生產大型和超大型零件,這給重型貨物運輸公司帶來了巨大的複雜性。擁有高資本和資產的全球公司可以投資升級機隊並從這種情況中受益。另一方面,區域和本地參與者也提出了更好的行業解決方案,以支援客戶在預定時間內執行專案的需求。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究成果

- 研究假設

- 研究範圍

第 2 章:研究方法

- 分析方法

- 研究階段

第 3 章:執行摘要

第 4 章:市場概覽

- 當前的市場狀況

- 市場動態

- 促進要素

- 再生能源專案對專案物流的需求不斷增加

- 增加基礎建設投資

- 限制

- 高初始資本投資

- 促進要素

- 產業吸引力-波特五力分析

- 產業價值鏈分析

- 政府法規和舉措

- 全球物流業(概述、LPI 分數、主要貨運統計數據等)

- 焦點 - 多式聯運在專案貨物中的作用

- 見解 - 零售石油和天然氣物流行業

- 重型和大尺寸貨物的回顧和評論

- 聚焦預製件產業-專案物流公司在運輸中的作用

- 深入了解用於運輸重型貨物的客製化拖車製造商

- 聚焦合約物流與綜合物流需求

第 5 章:市場區隔

- 服務

- 運輸

- 轉發

- 庫存管理和倉儲

- 其他加值服務

- 最終用戶

- 石油和天然氣、採礦和採石業

- 能源與電力

- 建造

- 製造業

- 其他最終用戶

- 地理

- 亞太

- 美洲

- 歐洲

- 中東和非洲

第 6 章:競爭格局

- 公司簡介

- Rhenus Logistics

- Bollore Logistics

- Agility Logistics

- EMO Trans

- Hellmann Worldwide Logistics

- Kuehne + Nagel International AG

- CH Robinson Worldwide Inc.

- Ceva Logistics

- NMT Global Project Logistics

- Rohlig Logistics

- Ryder System Inc.

- Expeditors International of Washington Inc.

- Megalift Sdn Bhd

- Dako Worldwide Transport GmbH

- CKB Logistics Group

- SAL Heavy Lift GmbH

- DB Schenker

- Kerry Logistics

- Deutsche Post DHL*

- Other Players in the Market

- FLS Transportation Services, Crowley Logistics, Highland Forwarding Inc., Kinetix International Logistics, Cole International Inc., Hisiang Logistics Co. Ltd, Sea Cargo Air Cargo Logistics Inc., and Bati Group

第 7 章:市場機會與未來趨勢

第 8 章:附錄

- 依活動分類的 GDP 分佈 - 主要國家

- 資本流動洞察 - 主要國家

- 經濟統計 - 運輸和倉儲業以及對經濟的貢獻(主要國家)

- 全球主要項目清單(石油和天然氣、建築、基礎設施開發等)

- 貨運統計(方式、產品類別等)*

第 9 章:免責聲明

The Project Logistics Market size is estimated at USD 436.34 billion in 2024, and is expected to reach USD 582.69 billion by 2029, growing at a CAGR of 5.95% during the forecast period (2024-2029).

Project logistics encompasses the comprehensive management and coordination of goods, materials, and information throughout the entire process of a project. The transportation of large-sized cargo requires specialized equipment, infrastructure, and experienced personnel. Dealing with cargo of unique dimensions poses a constant challenge for transporters, but shippers and service providers are becoming more adept at handling oversized and heavyweight shipments. The complexity of manufacturing also contributes to the difficulty, as parts and modular packages are produced in various locations and then shipped to their final destinations, necessitating meticulous planning. In recent years, there has been a growing trend of involving transportation providers in the early stages of the planning process.

The Asian-Pacific region leads the market in project logistics and is expected to experience the highest growth rate. Infrastructure investment has played a significant role in the economic development of Asia-Pacific countries, with some nations prioritizing the advancement of their domestic infrastructure.

Several established organizations, such as the Global Project Logistics Network (GPLN), specialize in project logistics on a global scale. GPLN members handle a wide range of industrial projects, including infrastructure and energy projects, providing services such as transportation, packing/crating, and the lifting of heavy, oversized, and out-of-gauge cargo.

During the height of the COVID-19 pandemic in 2020-21, air freight was in high demand within the project logistics sector for the transportation of essential items worldwide.

Project Logistics Market Trends

Increasing Usage of Renewable Energies Boosts Opportunities for Project Logistics Companies

According to the latest update from the International Energy Agency, global renewable power capacity is expected to increase by a third in 2023 due to factors such as growing policy support, higher fossil fuel prices, and concerns about energy security.

This growth will continue next year, with the world's total renewable electricity capacity reaching 4,500 gigawatts, equivalent to the combined power output of China and the United States. In 2023, global renewable capacity is projected to increase by 107 gigawatts, the largest absolute increase ever recorded, reaching over 440 gigawatts.

This expansion is happening in major markets worldwide, with Europe, the United States, India, and China leading the way. China, in particular, is expected to account for nearly 55% of global renewable power capacity additions in both 2023 and 2024.

Wind power installations are expected to experience a significant recovery in 2023, with a projected increase of nearly 70% compared to the previous year. This comes after a challenging period of slow growth in the industry. The improved growth can be attributed to the completion of projects that were delayed due to COVID-19 restrictions in China and supply chain issues in Europe and the United States.

However, the extent of growth in 2024 will depend on whether governments can offer more policy support to address obstacles related to permitting and auction design. Unlike the solar PV sector, the wind turbine supply chains are not expanding quickly enough to keep up with the growing demand in the medium term. This is primarily due to escalating commodity prices and difficulties in the supply chain, which are impacting the profitability of manufacturers.

This renewable energy requirement incorporates project logistics as the machines and other parts are so huge that they are shipped separately and then assembled at the site.

Growing Modular Construction Driving The Market

The need for sustainable infrastructure is driving the development of construction technology that is efficient and environmentally friendly. The traditional construction method may no longer be sufficient to meet the requirements of sustainable infrastructure. Modularization offers a solution to the inflexibility of conventional construction methods. By using modular construction, the cost of construction can potentially be reduced by 40%, and activities can be carried out simultaneously on site preparation and modular prefabrication.

The shift towards modular (offsite) construction methods creates a new market, particularly for developing countries that have low labor costs and ample land for prefabrication areas. In terms of supporting sustainable infrastructure development, prefabrication methods can lead to significant material savings, such as 60% less steel, 56% less concrete, and 77% less formwork compared to conventional construction methods of a similar scale.

However, there are still challenges with the modular prefabrication concept, such as the economics of scale and the complexity of transporting modular components that exceed the size of ISO containers. This offsite construction model also opens up opportunities for international trade within specific geographical regions, depending on each country's competitive advantages. The growth of international free trade provides broader business opportunities and potential for new trading connections. International and regional trade also increases the overseas trading of engineering, procurement, and construction (EPC) projects. The decision to use modular construction for overseas EPC projects impacts the development of project cargo movement and the overall investment in project logistics, including domestic and overseas logistics costs. Domestic logistics costs include manufacturing costs (fabrication, ready-mix concrete, bulk materials, rebar, and steel materials). In contrast, overseas logistics costs include vessel charter rates, bunker pricing, currency exchange, distance, volumetric sizing, insurance, and customs clearance.

Project Logistics Industry Overview

The project logistics market is fragmented, with the presence of global players and small- and medium-sized local players. Most global logistics players have a special project cargo division to meet the market needs and demand. Local players are also increasingly enhancing their capabilities in terms of fleet size, service offerings, industries served, and technology. Global manufacturers are making large and oversized components in the factory sites (off-site), which creates huge complexities for heavy cargo haulage companies. Global companies with high capital and assets can invest in upgraded fleets and benefit from this scenario. On the other hand, regional and local players are also coming up with better industry solutions to support the client's needs in executing the projects in the scheduled time.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.1.1 Increasing Demand For Project Logistics From Renewable Energy Projects

- 4.2.1.2 Increasing Investments In Infrastructure

- 4.2.2 Restraints

- 4.2.2.1 High Initial Capital Investment

- 4.2.1 Drivers

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4 Industry Value Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Global Logistics Sector (Overview, LPI Scores, Key Freight Statistics, Etc.)

- 4.7 Spotlight - Role of Multimodal Transport in Project Cargo

- 4.8 Insights - Retail Oil and Gas Logistics Sector

- 4.9 Review and Commentary on Heavy and Large Dimension Shipments

- 4.10 Focus on the Prefabrication Industry - Role of Project Logistics Companies in Transportation

- 4.11 Insights into Customized Trailer Manufacturers for Moving Heavy Cargo

- 4.12 Spotlight on the Demand for Contract Logistics and Integrated Logistics

5 MARKET SEGMENTATION

- 5.1 Service

- 5.1.1 Transportation

- 5.1.2 Forwarding

- 5.1.3 Inventory Management and Warehousing

- 5.1.4 Other Value-added Services

- 5.2 End User

- 5.2.1 Oil and Gas, Mining, and Quarrying

- 5.2.2 Energy and Power

- 5.2.3 Construction

- 5.2.4 Manufacturing

- 5.2.5 Other End Users

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.2 Americas

- 5.3.3 Europe

- 5.3.4 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Rhenus Logistics

- 6.2.2 Bollore Logistics

- 6.2.3 Agility Logistics

- 6.2.4 EMO Trans

- 6.2.5 Hellmann Worldwide Logistics

- 6.2.6 Kuehne + Nagel International AG

- 6.2.7 C.H. Robinson Worldwide Inc.

- 6.2.8 Ceva Logistics

- 6.2.9 NMT Global Project Logistics

- 6.2.10 Rohlig Logistics

- 6.2.11 Ryder System Inc.

- 6.2.12 Expeditors International of Washington Inc.

- 6.2.13 Megalift Sdn Bhd

- 6.2.14 Dako Worldwide Transport GmbH

- 6.2.15 CKB Logistics Group

- 6.2.16 SAL Heavy Lift GmbH

- 6.2.17 DB Schenker

- 6.2.18 Kerry Logistics

- 6.2.19 Deutsche Post DHL*

- 6.3 Other Players in the Market

- 6.3.1 FLS Transportation Services, Crowley Logistics, Highland Forwarding Inc., Kinetix International Logistics, Cole International Inc., Hisiang Logistics Co. Ltd, Sea Cargo Air Cargo Logistics Inc., and Bati Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

8 APPENDIX

- 8.1 GDP Distribution, by Activity - Key Countries

- 8.2 Insights into Capital Flows - Key Countries

- 8.3 Economic Statistics - Transport and Storage Sector, and Contribution to Economy (Key Countries)

- 8.4 List of Major Global Projects (Oil and Gas, Construction, Infrastructure Development, Etc.)

- 8.5 Freight Statistics (Mode, Product Category, Etc.)*

9 DISCLAIMER

計劃物流市場:按服務、最終用戶分類 - 2023-2030 年全球預測

計劃物流市場:按服務、最終用戶分類 - 2023-2030 年全球預測 專案物流的全球市場 2024-2028

專案物流的全球市場 2024-2028 全球項目物流市場

全球項目物流市場 2030 年項目物流市場預測:按服務、最終用戶和地區分類的全球分析

2030 年項目物流市場預測:按服務、最終用戶和地區分類的全球分析 2022-2029年全球項目物流市場規模研究和預測,按服務、終端用戶和區域分析

2022-2029年全球項目物流市場規模研究和預測,按服務、終端用戶和區域分析