|

市場調查報告書

商品編碼

1438358

曳引機:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029)Tractors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

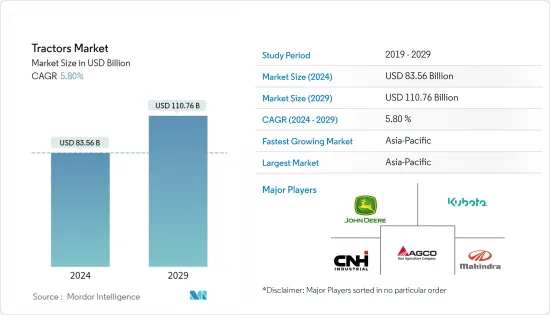

曳引機市場規模預計2024年為835.6億美元,預計到2029年將達到1107.6億美元,在預測期內(2024-2029年)年複合成長率為5.80%成長。

曳引機市場受到 2020 年第二季新型 COVID-19感染疾病爆發的負面影響,因為世界各地的封鎖擾亂了供應鏈並影響了全球曳引機的生產和銷售。然而,隨著經濟活動的恢復,隨著新產品的開發和推出,市場正在迅速復甦。曳引機需求的增加也促進了市場的成長。

從長遠來看,推動全球曳引機銷售成長的主要因素將是農業機械化率的提高(特別是在開發中國家)、農業勞動力成本上升、季節性勞動力短缺以及曳引機更換週期縮短。然而,該行業的一些知名企業正專注於市場上的併購和新產品開發。

主要亮點

- 2022 年 10 月,在 Kubota Connect 上,製造商向經銷商展示了新產品。 M7 系列 第四代久保田 M7 是該公司針對牲畜和飼料生產商的最大曳引機。

- 2021 年 9 月,TAFE 為印度西孟加拉邦和奧里薩邦推出了新的麥賽福格森 244 和 246 Dynatruck 版本曳引機。這些曳引機具有實用性高、技術先進、功率大的特性。

新興市場國家政府也鼓勵農民,以低利率向他們提供補貼和農業設備。農業設備和曳引機的需求預計將穩定成長。

主要亮點

- 根據美國農業部2021年預算,撥款33億美元支持提高美國農業競爭力和促進糧食安全的研究。該預算還將透過提供營運成本融資以及收購農場或維護現有農場的機會來幫助估計 35,000 名農民和牧場主。

隨著印度、中國和日本等主要新興經濟體透過提供農業設備補貼和降低信貸利率來鼓勵農民,以普及,亞太地區將繼續成長。預計未來五年將出現顯著成長年。這些發展可能會增加這些地區對曳引機的需求。

曳引機市場趨勢

未來五年,40馬力以下曳引機產業的成長預計將進一步加速

由於大馬力曳引機在困難地形中的卓越性能以及農場和非農業應用的多功能性,大馬力曳引機的行業趨勢在世界範圍內持續成長。印度和中國等主要曳引機市場近年來在 40 馬力以下細分市場中取得了積極成長。

小於 40 馬力的曳引機通常是緊湊型曳引機的代名詞。這些曳引機的引擎排氣量小於1,500 cc,佔用空間小,放置非常靈活。它們主要用於割草,但也可以執行其他基本農業任務,例如處理肥料。

然而,由於COVID-19感染疾病導致全球市場發生重大變化,2020年第一季緊湊型曳引機的需求大幅下降。一些地區的封鎖限制了人員流動並導致零售商店關閉。結果是市場滯後,銷售量大幅下降。

在大多數農業活動規模較大的國家中,亞太和非洲地區對40馬力以下曳引機的需求量大,主要用於農業活動。這是因為這些曳引機的低廉價格提高了廣大人口和人口中負擔得起的曳引機的購買率。農場規模。研究市場中的多個參與者正在推出他們的最新產品以佔領市場佔有率。

此外,尺寸緊湊、易於自訂以及即將推出的功率範圍內曳引機價格上漲近 50% 等因素預計將推動對這些曳引機的需求。在這個功率範圍內,有來自不同製造商的多種選擇和替代品,與高功率曳引機相比,為消費者提供了更多的議價能力。由於上述趨勢和發展,40 馬力以下曳引機市場預計將在未來幾年實現健康成長。

預計亞太地區將在預測期內引領市場

預計曳引機市場將由亞太地區主導,預計該地區在未來幾年發展最快。對農業機械化的興趣日益濃厚以及政府資助政策的增加預計將推動未來幾年的市場成長。

- 2021年10月,印度政府宣布將為總理基桑曳引機計劃下購買曳引機提供高達50%的補貼。根據該計劃購買曳引機的農民可以支付一半的價格享受優惠。

中國農業機械化協會等一些地區監管機構正在透過對合作社和個體農民進行有關在大型農場使用大馬力曳引機的好處的教育來促進農業機械化。向電動車的過渡也得到了政府的支持,政府支持企業開發永續產品。

- Monarch Tractor 是業界全電動自動曳引機製造商。 2021年11月,該公司及其農業電氣化聯盟合作夥伴獲得加州能源委員會(CEC)價值300萬美元的資金,用於加速包括曳引機在內的農業機械的電氣化,並展示農用設備電池的津貼。在野火造成停電期間保持關鍵電力負載運作。聯盟包括 Monarch Tractor、Gridtractor、Rhombus Energy Solutions、Current Ways 和 Polaris Energy Services。

農業規模化生產者和從事農業的新農村群體數量的擴大,促進了穩定市場需求的趨勢。在印度,農機領域大型客製化就業服務公司的引進,加速了農業機械化的進程。隨後向自動化技術的轉變預計將推動全部區域對曳引機的需求。所有上述因素預計將推動市場成長。

曳引機產業概況

曳引機市場適度整合,多個全球和地區參與者積極參與。 Mahindra & Mahindra、Tractor、Kubota Corporation、Farm Equipment Limited 和 HMT Limited 等領先公司已將合約和產品發布作為關鍵發展策略,以改善產品系列。

- 在 2022 年 11 月的 SIMA 2022 上,New Holland 首次推出了 T8 曳引機以及無人穀物車收割應用程式 Raven Autonomy。它採用了OMNiDRIVE,這是世界上第一個用於糧車收割的無人農業技術。尖端技術堆疊使農民能夠從收割機駕駛室監控、同步和操作無人駕駛曳引機。

- 2021 年 10 月,馬恆達推出了三款新型 YuvoTech+ 曳引機,配備了具有最高扭力和燃油效率的新時代先進技術。該曳引機有三種型號:Yuvo Tech+275(27.6 kW-37 HP)、Yuvo Tech+405(29.1kW 39 HP)和Yuvo Tech+415(31.33 kW-42 HP)。

- 2021 年 8 月,約翰迪爾推出了新型 6155MH 曳引機,該曳引機為犁耕機、犁耕機和牽引式收割機拖車提供所有經過現場驗證的性能和可靠性。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場挑戰

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔(市場規模)

- 按馬力

- 小於40HP

- 40HP~100HP

- 100HP以上

- 按下驅動器類型

- 兩輪驅動

- 四輪驅動/全輪驅動

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Deere and Company

- CNH Global NV(includes New Holland and Case IH)

- AGCO Corporation(includes Massey Ferguson, Valtra, Fendt, and Challenger)

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Limited

- Tractors and Farm Equipment Limited(TAFE)

- Kuhn Group(Subsidiary of Bucher Industries)

- Yanmar Company Limited

- Deutz-Fahr

The Tractors Market size is estimated at USD 83.56 billion in 2024, and is expected to reach USD 110.76 billion by 2029, growing at a CAGR of 5.80% during the forecast period (2024-2029).

The tractor market was impacted negatively by the outbreak of COVID-19, as the lockdowns in various parts of the world disrupted the supply chain during the second quarter of 2020, which impacted the production and sales of tractors globally. However, as the economies reopened, the market is recovering at a high rate, along with new product developments and launches. The increasing demand for tractors is also contributing to the growth of the market.

Over the long term, the key factors contributing to the increase in worldwide tractor sales are increasing farm mechanization rates, especially in developing nations, rising farm labor costs, seasonal labor shortages, and shorter tractor replacement cycles. However, some of the prominent players in the industry are focusing on mergers and acquisitions and new product development in the market. For instance,

Key Highlights

- In October 2022, At Kubota Connect, the manufacturer gave dealers a sneak peek at the new products. Series M7 Generation 4 The Kubota M7s are the company's largest tractors, aimed at livestock and forage producers.

- In September 2021, TAFE launched the new Massey Ferguson 244 and 246 Dynatrack versions of tractors specifically for West Bengal and Odisha states of India. These tractors are characterized by high utility, advanced technology, and high power.

Governments in emerging markets are also encouraging farmers in their countries and providing farm equipment at subsidized rates and low-interest rates. The demand for farm equipment and tractors is expected to grow at a healthy rate. For instance,

Key Highlights

- According to USDA 2021 Budget, USD 3.3 billion is allocated to support research to advance the competitiveness of US agriculture and promote food security. The budget also supports an estimated 35,000 farmers and ranchers by financing operating expenses and providing opportunities to acquire a farm or keep an existing one.

Asia-Pacific region is expected to witness significant growth in the next five years as emerging key economies like India, China, and Japan are encouraging farmers in their countries by offering subsidized farm equipment and low credit rates to encourage tractor adoption. Such developments are likely to drive the demand for tractors in these regions.

Tractor Market Trends

Below 40 HP Tractors Segment's Growth Expected to be Bolstered over the Next Five years

The industry trend toward bigger horsepower tractors continues to grow worldwide, owing to greater performance in difficult terrain and versatility in farm and non-farm applications. The major tractor markets like India and China are recording positive growth across less than 40 HP segments in recent years.

Less than 40 HP tractors are often synonymous with the term compact tractors. With an engine displacement of not more than 1,500 ccs, these tractors occupy less space and can be aligned with great flexibility. They are primarily used for mowing but can handle other basic farming tasks, like manure handling.

However, due to the significant volatility that caused the world market during the COVID-19 pandemic, demand for compact tractors fell dramatically in the first quarter of 2020. The imposition of lockdowns in several regions limited mobility and resulted in the closure of retail outlets. This resulted in a market delay, which, in turn, significantly reduced sales.

With the majority of countries that have huge agricultural activity, Asia-Pacific and African regions are witnessing high demand for less than 40 HP tractors, primarily for agricultural activities, as the low cost of these tractors increased the affordability rate among the highly populated small-scale farmers. Several players in the market studied are launching the latest products to gain market share. For instance,

- In August 2021, Kubota introduced its new LX Series, a range of multi-purpose compact tractors under 40 HP with two different models, namely the 35HP LX-351 Rear ROPS and LX-351 Cab. The new LX tractor features a Stage V engine with CRS, EGR, and DPF and is available in four different models. The LX-351 Rear ROPS and LX-351 Cab, with 35 hp and an HST 3-range transmission, and the LX-401 Rear ROPS and LX-401 Cab, featuring 40 hp and a 3-range HST transmission.

Further factors such as compact size, ease of customization, and nearly 50% more price for the next power range of tractors, are expected to enhance the demand for these tractors. In this power band, the bargaining power of consumers is high, compared to high-powered tractors, given the wide range of options and substitutes from different manufacturers. With the aforementioned trends and developments, it is expected that the Below 40HP tractors segment is likely to have healthy growth over the coming years.

Asia-Pacific Region Anticipated to Lead the Market During the Forecast Period

The tractor market is expected to be dominated by Asia-Pacific, and the region is predicted to develop at the highest rate over the coming years. The growing preference for farm mechanization and an increase in the number of government-funded policies are anticipated to promote the growth of the market in the next few years. For instance,

- In October 2021, the Indian government announced up to 50% subsidy on buying tractors under the PM Kisan Tractor Scheme. Farmers buying a tractor under the scheme can avail of the benefits and pay half the amount.

Several regional regulatory bodies, such as the China Agricultural Industry Mechanization Association, promote farm mechanization by educating co-operatives and individual farmers about the benefits of using high-horsepower tractors in larger farm areas. A shift toward EVs is also backed by the government, which is helping companies to develop sustainable products. For instance,

- Monarch Tractor is the manufacturer of the industry's fully electric autonomous tractor. In November 2021, the company and its Farm Electrification Consortium partners received a grant worth USD 3 million from the California Energy Commission (CEC) to accelerate the electrification of agricultural equipment, including tractors, and to demonstrate the ability of batteries in on-farm equipment to keep critical electrical loads running during power outages caused by wildfires. Monarch Tractor, Gridtractor, Rhombus Energy Solutions, Current Ways, and Polaris Energy Services make up the consortium.

The expansion in the number of large agricultural producers and new rural groups engaged in farming contributed to this tendency to stabilize the demand in the market. The introduction of large-scale bespoke hiring service enterprises in agricultural machinery in India fueled the rise in farm mechanization. The subsequent move to automated technologies is envisioned to drive the demand for tractors across the Asia-pacific region. All these aforementioned factors are expected to drive the growth of the market.

Tractor Industry Overview

The tractor market is moderately consolidated as it witnesses active engagement from several global and regional players. Major players such as Mahindra & Mahindra, Tractor, Kubota Corporation, Farm Equipment Limited, and HMT Limited are adopting agreements and product launches as key developmental strategies to improve the product portfolio of tractor products. For instance,

- In November 2022, At SIMA 2022, New Holland debuted the T8 tractor with Raven Autonomy, a driverless grain cart harvest application. It incorporates OMNiDRIVE, the world's first driverless agriculture technology for grain cart harvesting. The cutting-edge technology stack allows the farmer to monitor, synchronize, and operate a driverless tractor from the harvester's cab.

- In October 2021, Mahindra launched three new YuvoTech+ tractors that come equipped with the new-age advanced technology with the highest torque and fuel efficiency. The tractors are available in three models, namely Yuvo Tech+ 275 (27.6 kW-37 HP), Yuvo Tech+ 405 (29.1kW 39 HP), and Yuvo Tech+ 415 (31.33 kW-42 HP).

- In August 2021, John Deere introduced the new 6155MH Tractor that delivers all field-proven performance and reliability effective for cultivating, harrowing, or pulling harvester trailers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Challenges

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in USD billion)

- 5.1 By Horsepower

- 5.1.1 Below 40 HP

- 5.1.2 40 HP - 100 HP

- 5.1.3 Above 100 HP

- 5.2 By Drive Type

- 5.2.1 Two-wheel Drive

- 5.2.2 Four-wheel Drive/All-wheel Drive

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 Deere and Company

- 6.2.2 CNH Global NV (includes New Holland and Case IH)

- 6.2.3 AGCO Corporation (includes Massey Ferguson, Valtra, Fendt, and Challenger)

- 6.2.4 CLAAS KGaA mbH

- 6.2.5 Mahindra and Mahindra Corporation

- 6.2.6 Kubota Corporation

- 6.2.7 Escorts Limited

- 6.2.8 Tractors and Farm Equipment Limited (TAFE)

- 6.2.9 Kuhn Group (Subsidiary of Bucher Industries)

- 6.2.10 Yanmar Company Limited

- 6.2.11 Deutz-Fahr

2024-2032 年按馬力類型(40 馬力以下、40 馬力以上)、輪驅動(兩輪驅動、四輪驅動)、應用(農業、園藝等)和地區分類的低馬力曳引機市場

2024-2032 年按馬力類型(40 馬力以下、40 馬力以上)、輪驅動(兩輪驅動、四輪驅動)、應用(農業、園藝等)和地區分類的低馬力曳引機市場 全球電動曳引機市場:按推進力、容量、化學、混合曳引機、特徵、地區 - 預測(~2030 年)

全球電動曳引機市場:按推進力、容量、化學、混合曳引機、特徵、地區 - 預測(~2030 年) 曳引機實施全球市場規模、佔有率和成長分析:按產品 - 產業預測(2024-2031 年)

曳引機實施全球市場規模、佔有率和成長分析:按產品 - 產業預測(2024-2031 年) 全球曳引機市場規模、佔有率、成長分析,依類型(多用途曳引機、中耕作物曳引機)、依驅動方式(兩輪驅動(2WD)、四輪驅動(4WD))、依應用(農業、建築業) - 產業2024-2031 年預測

全球曳引機市場規模、佔有率、成長分析,依類型(多用途曳引機、中耕作物曳引機)、依驅動方式(兩輪驅動(2WD)、四輪驅動(4WD))、依應用(農業、建築業) - 產業2024-2031 年預測 全輪驅動曳引機市場- 按馬力(低於50 馬力、50 馬力至100 馬力、高於100 馬力)、按推進(內燃機、電動)、按操作(手動、自動)、按應用(農業、建築、園林綠化、政府)及預測,2024 - 2032

全輪驅動曳引機市場- 按馬力(低於50 馬力、50 馬力至100 馬力、高於100 馬力)、按推進(內燃機、電動)、按操作(手動、自動)、按應用(農業、建築、園林綠化、政府)及預測,2024 - 2032 公共事業曳引機:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

公共事業曳引機:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 曳引機機具市場報告:2030 年趨勢、預測與競爭分析

曳引機機具市場報告:2030 年趨勢、預測與競爭分析 電動曳引機市場,按電池類型、傳動系統技術、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

電動曳引機市場,按電池類型、傳動系統技術、按應用、國家和地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 全輪驅動曳引機市場:按操作、馬力、應用分類 - 2024-2030 年全球預測

全輪驅動曳引機市場:按操作、馬力、應用分類 - 2024-2030 年全球預測 大型推土機的全球市場:按鏟刀類型、運作重量、引擎功率和應用分類 - 2024-2030 年預測

大型推土機的全球市場:按鏟刀類型、運作重量、引擎功率和應用分類 - 2024-2030 年預測