|

市場調查報告書

商品編碼

1438277

可食用薄膜與塗料:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Edible Films and Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

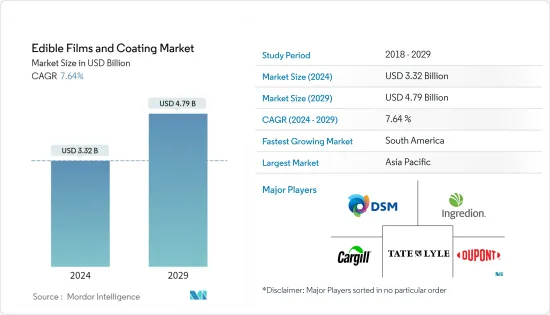

2024年食用薄膜和塗料市場規模估計為33.2億美元,預計到2029年將達到47.9億美元,在預測期間(2024-2029年)以7.64%的複合年增長率增長。

主要亮點

- 在食品上使用可食用塗層的優點是它們可以作為二氧化碳、脂質、水分、氧氣和香氣的屏障。提高食品品質並延長產品保存期限。使用可食用薄膜和塗層的主要優點之一是,一些活性成分可以合併到聚合物基質中並與食品一起服用,從而提高安全性,甚至改善營養和感官特性。可食用塗層可由大豆蛋白、小麥麵筋、乳清、明膠等製成。

- 由於植物來源食品的好處和健康意識,消費者對植物性食品的需求不斷增加。食品製造商正在加強延長保存期限並改進現有的包裝技術,以確保微生物安全並保護食品免受外部因素的影響。技術機構和研究人員正在創新新技術,利用多種成分開發可食用薄膜。

- 例如,2022年9月,印度理工學院古瓦哈蒂開發了一種可食用塗層,可延長水果和蔬菜的保存期限。該塗層由微藻類萃取物和多醣的混合物製成。海洋微藻類Dunaliella tertiolecta 以其抗氧化特性而聞名,被用作多種生物活性化合物,如類胡蘿蔔素、蛋白質和多醣。因此,製造商的新產品創新預計將有助於可食用薄膜和塗料市場的成長。

可食用薄膜和塗料市場趨勢

對自然資源可食用包裝材料的需求不斷增加

- 傳統的食品包裝材料具有許多缺點,例如環境影響、污染、製造要求和處置。對替代包裝材料和形式的需求顯著增加。

- 與永續性、道德、食品安全、食品品質和產品成本相關的問題對於現代消費者來說都是購買食品時越來越重要的因素,而食品包裝法律規章有助於解決這些問題,其中許多是被迫的。所有這些因素都極大地促進了食品包裝行業對可食用薄膜和塗料的需求不斷成長。這些可食用薄膜是從天然有機產品中提取的。

- 例如,小麥麵筋、乳清蛋白、玉米醇溶蛋白、蠟、纖維素衍生物、果膠等是利用水果、堅果、穀物和蔬菜生產的可食用薄膜。此外,製造商正在透過使用不同的蛋白質型態在可食用包裝領域進行創新。

- 例如,2022 年 6 月,一位名叫 Benedetto Marelli 的科學家推出了一家名為 Mori 的生技Start-Ups,利用絲蛋白。這些蛋白質用於包裹花園蔬菜、嫩牛排、新鮮雞肉和其他生鮮食品食品和包裝食品。

亞太地區繼續主導全球市場

- 中國和日本是該地區可食用薄膜和塗料市場的主要消費者。在中國,黃原膠是最常用的食品食用塗料之一,對多醣薄膜和塗料產生了很高的需求。

- 然而,正在進行研究以發現該地區的其他可食用塗層來源,預計這些來源可以延長產品的保存期限並保持更長時間的新鮮。此外,印度等國家的意識不斷提高,預計將在預測期內帶來非常有前景的市場前景。

- 2021年4月,BASF在香港推出Joncryl HPB(高性能阻隔劑)。該公司表示,這種特殊產品是一種水性液體阻隔塗料,在現代包裝趨勢和自然資源保護中發揮重要作用。這次新推出背後的策略是擴大公司業務。

可食用薄膜和塗料行業概述

可食用薄膜和塗料市場由全球和區域市場公司區隔。經營可食用薄膜和塗料市場的主要企業包括杜邦公司、泰萊公司、嘉吉公司、Koninklijke DSM NV 和 Ingredion 公司。可食用薄膜和塗料是包裝行業一個不斷成長的市場,隨著消費者從常規消費品中尋求此類選擇,預計需求將會成長。未來幾年市場將出現更多創新,產業可能會出現併購。最近出現了新品牌,並因其提供的產品而受到廣泛關注。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 成分類型

- 蛋白質

- 多醣

- 脂質

- 複合材料

- 應用

- 乳製品

- 麵包店/糖果零食

- 水果和蔬菜

- 肉類、家禽、魚貝類

- 其他用途

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 市場佔有率分析

- 最採用的策略

- 公司簡介

- Tate &Lyle PLC

- DuPont de Nemours Inc.

- DOHler Group Se

- Koninklijke DSM NV

- Cargill, Incorporated

- Ingredion Incorporated

- RPM International, Inc.(Mantrose-Haeuser Co. Inc.)

- Nagase &Co Ltd

- Sumitomo Chemical Co. Ltd

- Sufresca

- Pace International, LLC

- AgroFresh Solutions, Inc.

- Akorn Technology, Inc.

第7章市場機會與未來趨勢

The Edible Films and Coating Market size is estimated at USD 3.32 billion in 2024, and is expected to reach USD 4.79 billion by 2029, growing at a CAGR of 7.64% during the forecast period (2024-2029).

Key Highlights

- The benefit of using edible coating on food products is that it acts as a barrier for carbon dioxide, lipids, moisture, oxygen, and aromas. It improves food quality and extends the shelf life of products. One major advantage of using edible films and coatings is that several active ingredients can be incorporated into the polymer matrix and consumed with food, thus, enhancing safety or even nutritional and sensory attributes. The edible coatings can be made from soybean protein, wheat gluten, whey, gelatin, and many more.

- Demand for plant-based food products is increasing among consumers because of their benefits and health consciousness. The food product manufacturers have increased their efforts to increase the shelf life and improve the existing packaging technology, ensuring the microbial safety and preservation of food from the influence of external factors. Technological institutes and researchers are innovating new technologies to develop edible films with the use of different components.

- For instance, in September 2022, the Indian Institute of Technology, Guwahati, developed an edible coating to extend the shelf life of fruits and vegetables. The coating is made from a mix of microalgae extract and polysaccharides. The marine microalgae Dunaliella tertiolecta, known for its antioxidant properties, is used for its various bioactive compounds such as carotenoids, proteins, and polysaccharides. Thus, new product innovations from manufacturers are expected to contribute to the market growth of the edible films and coatings market.

Edible Films & Coatings Market Trends

Increasing Demand for Edible Packaging from Natural Resources

- Traditional food packaging materials have many shortcomings like environmental effects, pollution, manufacturing requirements, and wastage. The need for alternative packaging materials and packaging formats has increased at a significant level.

- Issues about sustainability, ethics, food safety, food quality, and product costs are all becoming increasingly important factors for modern-day consumers at the time of purchasing food products, and food packaging legislative regulations enforce a number of these issues. All these factors have largely contributed to the rising demand for edible films and coatings in the food packaging industry. These edible films are extracted from natural and organic products.

- For instance, wheat gluten, whey protein, corn zein, waxes, cellulose derivatives, and pectins are some edible films manufactured using fruits, nuts, grains, and vegetables. Additionally, manufacturers are innovating in the edible packaging space by using various protein forms.

- For instance, in June 2022, a scientist named Benedetto Marelli launched a biotech startup called Mori to use silk proteins. These proteins are used to coat garden vegetables, tenderized steaks, fresh poultry, and other perishable and packaged foods.

Asia-Pacific Continues to Dominate the Global Market

- China and Japan are the major consumers of the region's edible films and coatings market. In China, xanthan gum is one of the most commonly used edible coatings in food products, giving rise to the high demand for polysaccharide-based films and coatings.

- However, research to discover other sources of edible coatings is being conducted in the region, which is expected to extend the shelf life and prolong the freshness of products. Moreover, the rising awareness in countries like India is projected to lead to a very promising market scenario in the forecast period.

- In April 2021, BASF launched Joncryl HPB (High-Performance Barrier) in Hong Kong. According to the firm, this specific product is a water-based liquid barrier coating that plays an important role in the latest packaging trends and the conservation of natural resources. The strategy behind this new launch was to expand the company's business.

Edible Films & Coatings Industry Overview

The edible films and coating market is fragmented with global and regional market players. The major players operating in the edible films and coatings market include DuPont de Nemours Inc, Tate & Lyle, Cargill, Incorporated, Koninklijke DSM N.V., and Ingredion Incorporated. Edible film and coatings are a growing market within the packaging segment, where the demand is expected to upscale as consumers seek such options from their regular consumables. The market is poised to witness more innovations over the coming years, and the industry may expect mergers and acquisitions. New brands have emerged recently and have gained significant traction based on their offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ingredient Type

- 5.1.1 Protein

- 5.1.2 Polysaccharides

- 5.1.3 Lipids

- 5.1.4 Composites

- 5.2 Application

- 5.2.1 Dairy products

- 5.2.2 Bakery and Confectionery

- 5.2.3 Fruits and Vegetables

- 5.2.4 Meat, Poultry, and Seafood

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Most Adopted Strategies

- 6.3 Company Profiles

- 6.3.1 Tate & Lyle PLC

- 6.3.2 DuPont de Nemours Inc.

- 6.3.3 DOHler Group Se

- 6.3.4 Koninklijke DSM N.V.

- 6.3.5 Cargill, Incorporated

- 6.3.6 Ingredion Incorporated

- 6.3.7 RPM International, Inc. (Mantrose-Haeuser Co. Inc.)

- 6.3.8 Nagase & Co Ltd

- 6.3.9 Sumitomo Chemical Co. Ltd

- 6.3.10 Sufresca

- 6.3.11 Pace International, LLC

- 6.3.12 AgroFresh Solutions, Inc.

- 6.3.13 Akorn Technology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

可食用薄膜和塗料市場:按成分類型、應用分類 - 2024-2030 年全球預測

可食用薄膜和塗料市場:按成分類型、應用分類 - 2024-2030 年全球預測 食用薄膜和塗層全球市場報告 2024年

食用薄膜和塗層全球市場報告 2024年 2023-2028 年按材料類型(脂質、多醣、蛋白質、界面活性劑等)、來源(植物、動物)、最終用戶(食品和飲料、藥品等)和地區分類的可食用包裝市場報告

2023-2028 年按材料類型(脂質、多醣、蛋白質、界面活性劑等)、來源(植物、動物)、最終用戶(食品和飲料、藥品等)和地區分類的可食用包裝市場報告 可食用包裝市場 - 依原料、包裝製程、最終用途及預測 2023 - 2032 年

可食用包裝市場 - 依原料、包裝製程、最終用途及預測 2023 - 2032 年 2023-2028 年按成分類型(蛋白質、脂質、複合材料)、應用(乳製品、烘焙和糖果、水果和蔬菜、肉類、家禽和海鮮等)和地區分類的食用薄膜和塗層市場報告

2023-2028 年按成分類型(蛋白質、脂質、複合材料)、應用(乳製品、烘焙和糖果、水果和蔬菜、肉類、家禽和海鮮等)和地區分類的食用薄膜和塗層市場報告 可食用包裝市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029

可食用包裝市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029 食品·醫藥品可食包裝的全球市場:預測(2023年~2032年)

食品·醫藥品可食包裝的全球市場:預測(2023年~2032年) 可食用包裝市場:按來源(動物、植物)、按原料(脂質、多醣、海藻和藻類)、按包裝工藝/系統、按最終用戶 - 2023-2030 年全球預測

可食用包裝市場:按來源(動物、植物)、按原料(脂質、多醣、海藻和藻類)、按包裝工藝/系統、按最終用戶 - 2023-2030 年全球預測 可食用包裝市場規模、份額和趨勢分析報告:按原產地、按材料、按包裝類型、按最終用途、按地區、細分市場趨勢,2023-2030

可食用包裝市場規模、份額和趨勢分析報告:按原產地、按材料、按包裝類型、按最終用途、按地區、細分市場趨勢,2023-2030 2022-2029年全球食用包裝市場規模研究與預測,按材料類型(脂類、多醣、蛋白質、複合膜、表面活性劑),按終端用戶(食品和飲料、藥品)和區域分析

2022-2029年全球食用包裝市場規模研究與預測,按材料類型(脂類、多醣、蛋白質、複合膜、表面活性劑),按終端用戶(食品和飲料、藥品)和區域分析