|

市場調查報告書

商品編碼

1438253

加工油:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Process Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

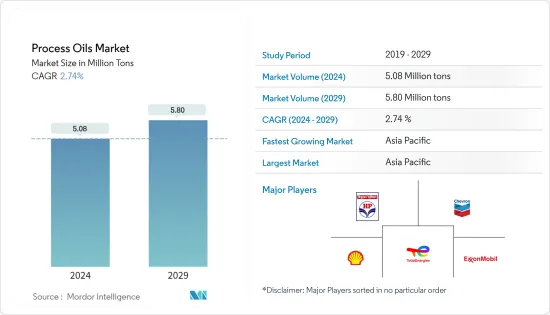

預計2024年加工油市場規模為508萬噸,預計2029年將達到580萬噸,在預測期(2024-2029年)複合年成長率為2.74%。

冠狀病毒感染疾病(COVID-19)大流行對 2020 年市場產生了負面影響。然而,市場已達到疫情前的水平,預計未來幾年將穩定成長。

主要亮點

- 短期內,推動市場成長的主要因素是聚合物生產需求的增加。橡膠油用量的快速增加也可能增加未來幾年對加工處理油的需求。

- 然而,由於嚴格的法規,PAHs 和 DAEs 的使用量減少可能會阻礙研究期間的市場成長。

- 儘管如此,生物基橡膠加工油的探索和電動汽車加工油需求的加速可能很快就會成為全球市場成長機會的因素。

- 預計亞太地區將主導市場,並且在預測期內也可能呈現最高的複合年成長率。

加工油市場趨勢

橡膠應用主導市場

- 橡膠加工處理油是使用高揮發性汽油生產的,並使用蒸餾過程分離煤油餾分。

- 天然和合成加工油加工油都在商業性用於製造多種橡膠產品,例如橡皮筋、玩具和輪胎。

- 它們也用於橡膠混合物的混合過程中,以增加填料的分散性並增強混合物的流動性能。

- 全球橡膠工業的擴張正在推動橡膠加工油在各種應用產業的使用。典型的橡膠應用包括輪胎、建築材料、白色家電、生物醫學和紡織品。

- 中國是世界上最大的輪胎生產國。根據中國國家統計局數據,2021年中國輪胎產量為90,246萬條,較2020年增加約9,500萬條。

- 根據馬來西亞橡膠理事會的數據,2022年上半年全球橡膠產量約1,390萬噸,比去年同期的約1,410萬噸下降1.5%。

- 基於以上因素,橡膠油作為加工油的應用預計將佔據市場主導地位。

亞太地區主導市場

- 由於印度和中國等國家對紡織品和個人保健產品的廣泛需求,亞太地區是一個潛力巨大的地區。

- 自1994年以來,中國一直是全球最大的紡織品服裝出口國,以OEM製造加工為主,主導全球中價格分佈市場。同時,歐盟繼續主導世界奢侈品市場和高品質紡織產品。

- 根據OICA統計,2021年中國汽車產量為2,608萬輛,比2020年的2,522萬輛成長3%。預計這將對預測期內的加工油市場產生正面影響。

- 目前,與已開發國家和其他新興經濟體相比,印度個人保健產品的普及相對較低。

- 然而,隨著經濟環境的改善和印度公民購買力的增強,個人保健產品在該國的採用預計將會增加。

- 據NIPFA India稱,印度美容和個人護理行業目前價值268億美元,預計未來三年將成長至372億美元。預計印度市場的成長將在研究期間推動加工油市場的發展。

- 根據OICA統計,2021年印度汽車工業成長30%,產量約439萬輛。汽車產業的快速成長將對所研究的市場產生正面影響。

- 由於上述因素,亞太地區加工油市場預計將在預測期內主導全球市場。

加工油業概況

加工油市場本質上是部分一體化的。市場上主要企業包括雪佛龍公司、埃克森美孚、惠普潤滑油公司、加拿大皇家殼牌公司和道達爾公司。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 聚合物產量增加

- 抑制因素

- 汽車業下滑

- 更嚴格的法規減少 PAH 和 DAE 的使用

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 類型

- 芳香

- 石蠟基

- 環烷烴

- 目的

- 橡皮

- 聚合物

- 個人護理

- 纖維

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- Chevron Corporation

- Ergon Inc.

- Exxon Mobil Corporation

- HollyFrontier Refining &Marketing LLC

- HP Lubricants

- Idemitsu Kosan Co. Ltd

- LUKOIL

- Nynas AB

- ORGKHIM Biochemical Holding

- Panama Petrochem Ltd

- PetroChina

- PETRONAS Lubricants International

- Phillips 66 Company

- Repsol

- Royal Dutch Shell PLC

- ENEOS Corporation

第7章市場機會與未來趨勢

The Process Oils Market size is estimated at 5.08 Million tons in 2024, and is expected to reach 5.80 Million tons by 2029, growing at a CAGR of 2.74% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market in 2020. However, the market reached pre-pandemic levels and is expected to grow steadily in the coming years.

Key Highlights

- Over the short term, the primary factor driving the market's growth is the increasing demand for polymer production. The surge in the use of rubber oils is also likely to augment the demand for process oils in the coming years.

- However, declining usage of PAH and DAE due to stringent regulations is likely to hinder the market's growth during the studied period.

- Nevertheless, research in bio-based rubber process oils and the accelerating demand for process oils in electric vehicles can soon be the factors behind growth opportunities for the global market.

- The Asia-Pacific region is expected to dominate the market and is also likely to witness the highest CAGR during the forecast period.

Process Oils Market Trends

Rubber Applications to Dominate the Market

- Rubber process oil is manufactured using petroleum after the more volatile petrol, and heating oil fractions are separated using the distillation process.

- Both natural and synthetic process oils are commercially used in producing several rubber products, including rubber bands, toys, and tires.

- They are also used in the mixing process for rubber compounds as they increase the dispersion of fillers and enhance the flow characteristics of the mixture.

- The expansion of the global rubber industry is promoting the use of rubber process oils across various application industries. Some typical rubber applications include tires, construction materials, white goods, biomedical, and textiles.

- China is the largest tire-producing country in the world. According to the National Bureau of Statistics of China, tire production in China in 2021 was 902.46 million units, an increase of around 95 million units compared to 2020.

- According to Malaysian Rubber Council, the global rubber production in the first half of 2022 was around 13.9 million metric tons, with a decline of 1.5% from the corresponding period of the previous year, where about 14.1 million metric tons were produced.

- Based on the factors above, the rubber oil application for process oils is expected to dominate the market.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is an area of immense potential due to the extensive demand for textiles and personal care products in countries such as India and China.

- China continued to be the biggest textile and apparel exporter in the world since 1994. The country dominates the global low-to-medium-end market by mainly engaging in OEM manufacturing and processing. At the same time, the European Union continues to dominate the global upmarket and high-quality textiles.

- According to OICA, automotive production in China in 2021 was at 26.08 million units, with a 3% growth from 25.22 million units in 2020. It is anticipated to positively impact the process oil market during the forecast period.

- Presently, the penetration of personal care products in India is comparatively low compared to developed and other developing economies.

- However, the improving economic environment and the increasing purchasing power of the Indian population are expected to increase the adoption of personal care products in the country.

- According to NIPFA India, the Indian beauty and personal care industry is currently worth USD 26.8 billion and is anticipated to grow to USD 37.2 billion over the next three years. The growth of the Indian market is expected to boost the development of the process oil market during the studied period.

- According to OICA, the automotive industry in India observed a growth of 30% in 2021 and produced around 4.39 million units. Rapid growth in the Automotive sector would positively impact the studied market.

- Due to the factors above, the market for process oils in the Asia-Pacific region is expected to dominate the global market during the forecast period.

Process Oils Industry Overview

The process oils market is partially consolidated in nature. Some of the major players in the market are Chevron Corporation, ExxonMobil Corporation, HP Lubricants, Royal Dutch Shell Plc, and Total.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Polymer Production

- 4.2 Restraints

- 4.2.1 Declining Automotive Sector

- 4.2.2 Declining Usage of PAH and DAE due to Stringent Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Force Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Aromatic

- 5.1.2 Paraffinic

- 5.1.3 Naphthenic

- 5.2 Application

- 5.2.1 Rubber

- 5.2.2 Polymers

- 5.2.3 Personal Care

- 5.2.4 Textile

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chevron Corporation

- 6.4.2 Ergon Inc.

- 6.4.3 Exxon Mobil Corporation

- 6.4.4 HollyFrontier Refining & Marketing LLC

- 6.4.5 HP Lubricants

- 6.4.6 Idemitsu Kosan Co. Ltd

- 6.4.7 LUKOIL

- 6.4.8 Nynas AB

- 6.4.9 ORGKHIM Biochemical Holding

- 6.4.10 Panama Petrochem Ltd

- 6.4.11 PetroChina

- 6.4.12 PETRONAS Lubricants International

- 6.4.13 Phillips 66 Company

- 6.4.14 Repsol

- 6.4.15 Royal Dutch Shell PLC

- 6.4.16 ENEOS Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Research in Bio-based Rubber Process Oils

- 7.2 Rising Demand for Process Oils in Electric Vehicles

2024 年橡膠加工油世界市場報告

2024 年橡膠加工油世界市場報告 2030 年石油加工市場預測:按產品類型、精製類型、技術、應用和地區分類的全球分析

2030 年石油加工市場預測:按產品類型、精製類型、技術、應用和地區分類的全球分析 橡膠加工油:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測

橡膠加工油:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測 2024 年加工油全球市場報告

2024 年加工油全球市場報告 全球加工油市場

全球加工油市場 加工油市場:按類型(芳香族、環烷烴、非致癌性)、按功能(變形劑、增量油、塑化劑)、按用途- 2023-2030 年全球預測

加工油市場:按類型(芳香族、環烷烴、非致癌性)、按功能(變形劑、增量油、塑化劑)、按用途- 2023-2030 年全球預測 工藝油市場 - 2018-2028F全球行業規模、佔有率、趨勢、機會和預測,按類型、功能、應用、生產技術、區域、競爭分類

工藝油市場 - 2018-2028F全球行業規模、佔有率、趨勢、機會和預測,按類型、功能、應用、生產技術、區域、競爭分類 橡膠加工油的全球市場

橡膠加工油的全球市場 橡膠加工油的全球市場:COVID-19影響分析(各用途,各類型,各國,各地區),產業分析,市場規模,市場佔有率,預測(2023年~2030年)

橡膠加工油的全球市場:COVID-19影響分析(各用途,各類型,各國,各地區),產業分析,市場規模,市場佔有率,預測(2023年~2030年) 2023-2030 年全球橡膠加工油市場

2023-2030 年全球橡膠加工油市場