|

市場調查報告書

商品編碼

1435789

汽車泡沫:市場佔有率分析、產業趨勢、成長預測(2024-2029)Automotive Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

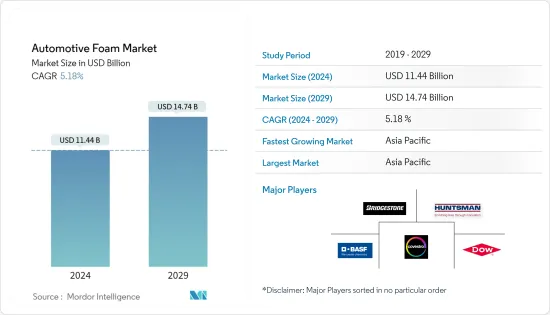

預計2024年汽車泡棉市場規模為114.4億美元,預計到2029年將達到147.4億美元,在預測期內(2024-2029年)成長5.18%,複合年成長率成長。

2020年,冠狀病毒感染疾病(COVID-19)的傳播和封鎖對汽車產業產生了負面影響,導致銷售和產量下降。然而,隨著封鎖的放鬆和經濟的成長勢頭,該行業能夠在 2021-2022 年恢復成長勢頭。

主要亮點

- 日益重視汽車泡棉的永續生產和日益成長的汽車減重需求等因素預計將在預測期內推動市場發展。

- 然而,環境友善生物泡沫的供應和歐洲主要經濟體汽車產量的下降預計將阻礙預測期內的市場成長。

- 電動車需求的成長和其他因素預計將在預測期內為市場帶來機會。

- 亞太地區主導了市場,印度和中國等國家的需求不斷成長。

汽車泡棉市場趨勢

室內應用主導市場

- 在汽車內裝應用中,汽車泡棉主要用於儀表板、底盤零件、電纜覆蓋層、頭枕、方向盤、排擋輪圈、座椅、保險桿、門飾等。

- 對於這些應用,聚氨酯泡棉在世界各地最常使用。這種泡棉具有隔熱性能、緩衝性能、窗戶密封性能和隔音性能等優點。

- 由於這些泡棉重量輕,因此可以幫助減輕車輛的整體重量、提高燃油效率並減少排放氣體。這些泡棉具有隔音性能,可降低車內噪音水平,使駕駛更加舒適。因此,聚氨酯泡棉在內燃機和電動車的各種內裝應用中越來越受到製造商的歡迎。

- 根據國際工業組織(OICA)的數據,2022年全球汽車產量與前一年同期比較成長6%,總合生產85.01輛汽車。因此,這種趨勢可能會增加對泡沫的需求,以減輕車輛重量並提高效率。

- 根據EV Volumes的數據,2022年全球純電動車(BEV)和插電式混合(PHEV)總合銷量總計1,050萬輛,與前一年同期比較去年同期成長60%。

- 根據國際能源總署(IEA)預測,在新的政策情境下,預計2030年全球電動車銷售將達到1.25億輛(不包括兩輪/三輪車)。

- 因此,汽車產業的這種趨勢可能會增加預測期內對內裝應用泡棉的需求。

亞太地區主導市場

- 由於中國、印度和東南亞國協等國家聚氨酯消費量的增加,亞太地區在全球汽車泡沫市場中佔據主導地位。

- 根據中國工業協會預測,2022年中國汽車企業產量為2702萬輛,與前一年同期比較2021年的2609萬輛年成長3.4%,銷量成長2.1%。% 至 2,686 台,達到 10,000 台。

- 此外,中國還是全球最大的電動車市場。根據中國工業協會統計,2023年2月純電動和插電式混合動力車產量為55.2萬輛,較1月的42.5萬輛成長30%,市佔率可望帶動成長。

- 印度也是一些世界上最大的汽車製造商的所在地。印度品牌股權基金會(IBEF)預計,到2027年,印度小客車市場規模預計將達到548.4億美元,2022年至2027年複合年成長率將超過9%。

- 根據OICA統計,2022年國內汽車總產量為545萬輛,但2021年則上升至439萬輛,與前一年同期比較增加24%。

- 因此,該地區汽車行業的這種趨勢預計將在預測期內推動汽車泡棉市場。

汽車泡棉產業概況

汽車泡沫市場已部分整合,主要企業佔據了相當大的市場佔有率。主要企業包括(排名不分先後) BASF SE、Dow、Huntsman International LLC.、Covestro AG 和 Bridgestone Corporation。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 越來越關注汽車泡棉的永續生產

- 減肥需求日益增加

- 其他司機

- 抑制因素

- 歐洲主要國家汽車產量下降

- 環境友善生物形態的可用性

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 類型

- 聚氨酯泡棉(PUF)

- 軟質聚氨酯泡棉

- 硬質聚氨酯泡棉

- 發泡聚丙烯

- 聚酯泡沫

- 其他

- 聚氨酯泡棉(PUF)

- 目的

- 內部的

- 外部的

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)分析/市場排名分析

- 主要企業策略

- 公司簡介

- BASF SE

- Bridgestone Corporation

- Covestro AG

- Dow

- Huntsman Corporation

- Recticel

- Rogers Corporation

- Saint-Gobain

- Vita(Holdings)Limited

- Woodbridge Foam Corporation

第7章 市場機會及未來趨勢

The Automotive Foam Market size is estimated at USD 11.44 billion in 2024, and is expected to reach USD 14.74 billion by 2029, growing at a CAGR of 5.18% during the forecast period (2024-2029).

In the year 2020, the breakdown of Covid-19 and the imposition of lockdowns negatively affected the automotive industry causing a decline in sales and production. However, the easing of lockdowns and economies gaining momentum helped the industry to gain back momentum in the years 2021 and 2022.

Key Highlights

- Factors such as growing emphasis on the sustainable production of automotive foams and the growing need for weight reduction in vehicles are expected to drive the market over the forecast period.

- However, the availability of eco-friendly bio-foams and the decline in automotive production in major economies of Europe is expected to hinder the market growth over the forecast period.

- The growing demand from electric vehicles and other factors are expected to act as an opportunity for the market over the forecast period.

- Asia-Pacific dominated the market with an increased demand from countries like India, China, and others.

Automotive Foam Market Trends

Interior Applications to Dominate the Market

- In interior applications, automotive foams are mainly used for dashboards, chassis components, cable sheathing, headrests, steering wheels, gear knobs, seats, bumpers and door trims, and others.

- For these applications, polyurethane foam is the most used foam worldwide. This foam provides benefits like insulation properties, cushioning, window encapsulation, and acoustical properties.

- As these foams are lightweight, they help in reducing the total weight of the car, which can improve fuel efficiency and reduce emissions. By providing acoustical insulation properties, these foams help in reducing noise levels inside the car, making the car more pleasurable to drive. Hence, polyurethane foams have gained popularity amongst manufacturers for various interior applications in ICEs and EVs.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), in the year 2022, the production of vehicles increased globally by 6% with a total of 85.01 units manufactured as compared to the previois year. Hence, such trends are likely to increase the demand for foams to reduce the weight of vehicles and increase efficiency.

- According to EV Volumes, in the year 2022, the total sales of Battery Electric Vehicles (BEVs) and plug-in Hybrid Electric Vehicles (PHEVs) were 10.5 million worldwide, registering a growth of 60% as compared with the previous year.

- According to the International Energy Agency (IEA), global electric vehicle sales are expected to reach 125 million in 2030, as per the New Policies Scenario (excluding two/three-wheelers).

- Hence, such trends in the automotive industry are likely to increase the demand for foams used in interior applications over the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region dominates the global market for automotive foams owing to the growing polyurethane consumption in countries such as China, India, and ASEAN Countries.

- According to the China Association of Automobile Manufacturers (CAAM), Chinese carmakers produced 27.02 million units in 2022, up by 3.4% Y-o-Y compared to 26.09 million units in 2021, while sales rose by 2.1% to 26.86 million units.

- Further, China is the biggest market for electric vehicles in the world. According to the China Association of Automobile Manufacturers (CAAM), in February 2023, the production of BEVs and PHEVs was 552 thousand while in the month of January, it was 425 thousand registering a growth of 30% which is likely to drive the market growth for automotive foams.

- India is also home to some of the world's largest automakers. According to the Indian Brand Equity Foundation (IBEF), the Indian passenger car market is expected to reach USD 54.84 billion by 2027 while registering a CAGR of over 9% between 2022-27.

- According to OICA, the total production of vehicles in the country in the year 2022 was 5.45 million units while in the year 2021, it was 4.39 million units registering a growth of 24% year-on-year.

- Hence, such trends in the automotive industry in the region is expected to drive the market for automotive foams during the forecast period.

Automotive Foam Industry Overview

The automotive foam market is partially consolidated, with top players accounting for a considerable share of the market. Some of the major companies include (not in any particular order) BASF SE, Dow, Huntsman International LLC., Covestro AG, and Bridgestone Corporation among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Emphasis on the Sustainable Production of Automotive Foams

- 4.1.2 Growing Need for Weight Reduction

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Declining Automotive Production in Major Economies of Europe

- 4.2.2 Availability of Eco-Friendly Bio-Foams

- 4.3 Industry Value Chain Analysis

- 4.4 Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Polyurethane Foams(PUFs)

- 5.1.1.1 Flexible Polyurethane Foam

- 5.1.1.2 Rigid Polyurethane Foam

- 5.1.2 Expanded Polypropylene Foam

- 5.1.3 PET Foam

- 5.1.4 Other Types

- 5.1.1 Polyurethane Foams(PUFs)

- 5.2 Application

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis **/Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 Bridgestone Corporation

- 6.4.3 Covestro AG

- 6.4.4 Dow

- 6.4.5 Huntsman Corporation

- 6.4.6 Recticel

- 6.4.7 Rogers Corporation

- 6.4.8 Saint-Gobain

- 6.4.9 Vita (Holdings) Limited

- 6.4.10 Woodbridge Foam Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand from Electric Vehicles

- 7.2 Other Opportunities

碳泡沫:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

碳泡沫:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 2024 年消費泡沫全球市場報告

2024 年消費泡沫全球市場報告 全球工業泡沫市場 (2024)

全球工業泡沫市場 (2024) 泡沫發泡市場報告:2030 年趨勢、預測與競爭分析

泡沫發泡市場報告:2030 年趨勢、預測與競爭分析 工業泡沫市場:按泡沫類型、樹脂類型、應用分類 - 2024-2030 年全球預測

工業泡沫市場:按泡沫類型、樹脂類型、應用分類 - 2024-2030 年全球預測 工程泡沫市場:按形狀、材料和最終用戶分類 - 2024-2030 年全球預測

工程泡沫市場:按形狀、材料和最終用戶分類 - 2024-2030 年全球預測 發泡市場:按產品類型、應用和最終用途 - 2024-2030 年全球預測

發泡市場:按產品類型、應用和最終用途 - 2024-2030 年全球預測 高性能泡棉市場:按類型、材料和最終用戶分類 - 2024-2030 年全球預測

高性能泡棉市場:按類型、材料和最終用戶分類 - 2024-2030 年全球預測 發泡全球市場報告 2024

發泡全球市場報告 2024 2024 年汽車泡棉全球市場報告

2024 年汽車泡棉全球市場報告