|

市場調查報告書

商品編碼

1433009

HPC 軟體 -市場佔有率分析、產業趨勢與統計、成長預測 (2024-2029)HPC Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

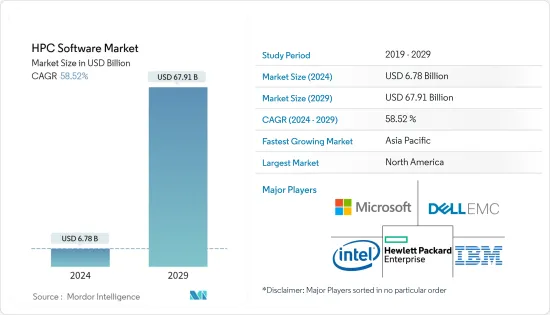

HPC 軟體市場規模預計到 2024 年為 67.8 億美元,預計到 2029 年將達到 679.1 億美元,在預測期內(2024-2029 年)複合年成長率為 58.52%。

人工智慧(AI)、物聯網(IIoT)投資的增加以及電子設計自動化(EDA)的工程需求等因素正在預測期內推動市場發展。

主要亮點

- 如果沒有合適的工具和先進技術,對短產品開發週期 (PLC) 的快速成長的需求和持續品質維護的需求將幾乎不可能即時滿足。

- 包括德國、美國、英國、日本和中國在內的世界各國正在認知到這些技術作為經濟成長關鍵驅動力的重要性,而 HPC 正在支持這些努力,同時保持成本和性能效率。成為軟體的潛在市場。

- 汽車、離散製造和醫療機器人等行業擴大採用高效能運算 (HPC) 系統和電腦輔助工程 (CAE) 軟體進行高保真建模和模擬。

- 此外,雲端基礎的HPC 解決方案因其經濟高效的計量收費模式而越來越受歡迎。政府機構、研究機構和大學是雲端基礎的HPC 解決方案的主要受益者。

HPC軟體市場趨勢

雲端基礎的高效能運算軟體推動成長

- 該地區的公司決定透過雲端租用 HPC 應用程式來解決複雜的數學建模問題。因此,雲端高效能運算(HPC)近年來經歷了快速成長。

- 雲端 HPC 提供了一種可擴展且經濟高效的方法來處理大量資料和運行複雜的應用程式。雲端處理供應商正在投資研發以推出新軟體來滿足企業的需求。

- 例如,2023 年 2 月,亞馬遜網路服務 (AWS) 的調查團隊宣布了一個新的軟體框架,用於在量子計算硬體上運行電磁模擬。它的開發是為了利用 AWS 上提供的雲端基礎的高效能運算 (HPC) 產品和服務。

- 雲端 HPC 供應商透過保持有競爭力的成本、快速創新和擴展其產品組合獲得了豐厚的回報。

- 例如,2023年5月,全球技術和HPC供應商CGG宣布推出愛爾蘭製藥軟體公司CGG,利用人工智慧(AI)大幅提高開發新藥已簽署協議,成為Biosimulytics 的獨家HPC 雲端合作夥伴。

- 2022 年 11 月,洛克希德馬丁公司和微軟宣布擴大戰略合作關係,以支持國防部 (DOD) 的技術進步。該協議預計將重點關注雲端創新、數位轉型和其他先進技術創新。主要供應商的這些以雲端為中心的合作夥伴關係預計將推動對雲端 HPC 的需求。

亞太地區是一個快速成長的地區

- 亞太地區是中國、日本、印度等大型新興經濟體的所在地。這些經濟體正在大力投資高效能運算以加速經濟發展。此外,製造業和醫療保健等各行業也擴大使用仿真,也推動了對 HPC 的需求。

- 該地區強大的製造業以及對物聯網和人工智慧等 HPC 驅動技術的投資,使其成為雲端 HPC 供應商利潤豐厚的市場。

- 供應商正在進行大量投資,以支持亞太地區強勁的製造業。為了降低製造成本並維持在全球市場的競爭力,越來越依賴模擬和雲端運算來提高業務效率。

- 中國、日本、韓國、印度和澳洲在未來幾年為 HPC 軟體提供了巨大的潛力。中國政府承諾在半導體產業投資470億美元,並減少製造和設計中的非國產設備,最終將在預測期內增加該國高效能運算技術的潛力,創造空間。

- 2022年4月,富士通宣布推出富士通計算即服務(CaaS),這是一個新的服務組合,透過雲端提供對商業用途的尖端計算技術的訪問,加速數位轉型(DX)。 `。該公司計劃於 2022 年 10 月開始向日本市場提供這些新服務。

HPC軟體產業概況

一些區域和全球參與者憑藉高效能運算軟體解決方案的技術專長主導了市場。全球高效能運算軟體市場預計將會整合。 Amazon Web Services Inc.、ANSYS, Inc.、Dassault Systemes、Dell EMC、Google Inc.、Hewlett Packard Enterprise Development LP、IBM Corporation、Intel Corporation、Microsoft Corporation、Oracle Corporation 是當前市場的一些主要參與者。所有這些參與者都參與制定競爭策略,例如聯盟、新產品創新和市場擴張,以獲得全球高效能運算軟體市場的主導地位。

2023 年 5 月,IBM 宣布 Cadence Design Systems, Inc. 將利用高效能運算 (HPC) 和 IBM Cloud HPC 來協助快速開發晶片和系統設計軟體。 Cadence 在其 HPC混合雲解決方案中引入了整合的 IBM Spectrum LSF,使其能夠靈活地管理本地和雲端中的運算密集型工作負載。

2023 年 5 月,Quantum Machines 宣布與 ParTec 合作,推出共同開發的通用軟體解決方案,將量子電腦緊密整合到高效能運算 (HPC) 環境中。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進與市場約束因素介紹

- 市場促進因素

- 雲端基礎的高效能運算軟體推動成長

- 虛擬技術創新

- IT產業的擴張與多元化

- 市場限制因素

- 高可用性雲端模型中的資料安全問題

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 買家/消費者的議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 依部署類型

- 本地

- 雲

- 依工業用途

- 航太/國防

- 能源/公共產業

- BFSI

- 媒體與娛樂

- 製造業

- 生命科學與醫療保健

- 設計與工程

- 其他工業應用

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第6章 競爭形勢

- 公司簡介

- Amazon Web Services Inc.

- ANSYS, Inc.

- Dassault Systemes

- Dell EMC

- Google Inc.

- Hewlett Packard Enterprise Development LP

- IBM Corporation

- Intel Corporation

- Microsoft Corporation

- Oracle Corporation

第7章 投資分析

第8章 市場機會及未來趨勢

The HPC Software Market size is estimated at USD 6.78 billion in 2024, and is expected to reach USD 67.91 billion by 2029, growing at a CAGR of 58.52% during the forecast period (2024-2029).

Factors such as rising investments in the Artificial Intelligence (AI), the Industrial Internet of Things (IIoT), and engineering demand for Electronic Design Automation (EDA) are driving the market over the forecast period.

Key Highlights

- The surging demand for short product development cycles (PLCs) and a need to maintain persistent quality becomes nearly impossible to address in real time without using the right tools and advanced technologies.

- Countries across the globe, including Germany, the United States, the United Kingdom, Japan, and China, among others, have recognized the importance of such technologies as a significant driver of economic growth and are potential markets for HPC software, which support these initiatives while maintaining cost and performance efficiencies.

- The adoption of high-performance computing (HPC) systems with computer-aided engineering (CAE) software for high-fidelity modeling simulation is rising among various industries, such as automotive, discrete manufacturing, and healthcare robotics.

- Moreover, cloud-based HPC solutions are gaining traction due to their cost-effective pay-as-you-go pricing model. Predominantly, government agencies, research institutions, and universities are likely to benefit from cloud-based HPC solutions.

HPC Software Market Trends

Cloud Based High-Performance Computing Software is Driving the Growth

- Enterprises across regions are deciding to rent HPC applications via the cloud to solve complex mathematical modeling problems, as they see benefits beyond costs. As a result, cloud high-performance computing (HPC) has seen an uptick in the past few years.

- Cloud HPC offers scalable and cost-effective ways to process a large amount of data and run complex applications. Cloud computing providers are investing in research and development to introduce new software to meet the needs of businesses.

- For instance, in February 2023, Researchers at Amazon Web Services (AWS) launched a new software framework that can be used to create electromagnetic simulations on quantum computing hardware. It was developed to leverage the cloud-based high-performance computing (HPC) products and services available on AWS.

- Cloud HPC providers gain significant returns by maintaining competitive costs, rapid innovation, and portfolio expansions.

- For instance, in May 2023, CGG, a global technology, and HPC provider, announced that it signed a contract to be the exclusive HPC cloud partner of Biosimulytics, an Irish pharma software company that uses artificial intelligence (AI) to dramatically improve the speed, cost, novelty, and success rate in new drug development.

- In November 2022, Lockheed Martin and Microsoft announced the expansion of their strategic relationship to support the advancement of technology for the Department of Defense (DOD). The agreement was expected to focus on Classified Cloud innovations, Digital Transformation, and other advanced technological innovations. Such cloud-focused partnerships by the major vendors are expected to boost the demand for cloud HPC.

Asia-Pacific is the Fastest Growing Region

- The region is home to several large and emerging economies, including China, Japan, and India. These economies are heavily investing in HPC to accelerate their economic development. Moreover, the growing use of simulation in various industries, including manufacturing, healthcare, and others, drives the demand for HPC.

- The region's strong manufacturing industry and investments in technologies driving HPC, such as IoT and AI, will likely make it a lucrative market for cloud HPC vendors.

- Vendors have made significant investments to cater to Asia-Pacific's robust manufacturing sector, which increasingly relies on simulation and cloud computing to lower production costs and improve operational effectiveness to maintain their competitiveness in the global market.

- Specifically, China, Japan, South Korea, India, and Australia are creating huge potential for HPC software in the coming years. The Chinese government has declared to invest USD 47 billion in its semiconductor industry to cut out non-indigenous devices in manufacturing and design, which will eventually create potential space for high-performance computing technology in the country for the forecast period.

- In April 2022, Fujitsu announced the launch of its new service portfolio, "Fujitsu Computing as a Service (CaaS)," to accelerate digital transformation (DX) by offering access to the most advanced computing technologies via the cloud for commercial use. The company was expected to begin delivery of these new services to the Japanese market in October 2022.

HPC Software Industry Overview

Some regional and global players dominate the market with their technological expertise in high-performance computing software solutions. The global market for high-performance computing software is expected to be consolidated in nature. Amazon Web Services Inc., ANSYS, Inc., Dassault Systemes, Dell EMC, Google Inc., Hewlett Packard Enterprise Development LP, IBM Corporation, Intel Corporation, Microsoft Corporation, and Oracle Corporation are some of the major players in the current market. All these players are involved in competitive strategic developments such as partnerships, new product innovation, and market expansion to gain leadership positions in the global high-performance computing software market.

In May 2023, IBM announced Cadence Design Systems, Inc. is leveraging high-performance computing (HPC) with IBM Cloud HPC to help develop its chip and system design software faster. Cadence can flexibly manage its compute-intensive workloads on-premises and in the cloud with the integrated IBM Spectrum LSF deployed in a hybrid cloud solution for HPC.

In May 2023, Quantum Machines announced its partnership with ParTec to launch a co-developed universal software solution for tightly integrating quantum computers into high-performance computing (HPC) environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Cloud Based High-Performance Computing Software is Driving the Growth

- 4.3.2 Innovation in Virtualization Technology

- 4.3.3 Expansion and Diversification of IT Industry

- 4.4 Market Restraints

- 4.4.1 Data Security Concerns in High Availability Cloud Model

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Buyers/Consumers

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Deployment Type

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Industrial Application

- 5.2.1 Aerospace & Defense

- 5.2.2 Energy & Utilities

- 5.2.3 BFSI

- 5.2.4 Media & Entertainment

- 5.2.5 Manufacturing

- 5.2.6 Life-science & Healthcare

- 5.2.7 Design & Engineering

- 5.2.8 Other Industrial Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amazon Web Services Inc.

- 6.1.2 ANSYS, Inc.

- 6.1.3 Dassault Systemes

- 6.1.4 Dell EMC

- 6.1.5 Google Inc.

- 6.1.6 Hewlett Packard Enterprise Development LP

- 6.1.7 IBM Corporation

- 6.1.8 Intel Corporation

- 6.1.9 Microsoft Corporation

- 6.1.10 Oracle Corporation

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

雲端高效能運算 (HPC):市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年)

雲端高效能運算 (HPC):市場佔有率分析、產業趨勢與統計、成長預測(2024-2029 年) AI加速器晶片市場:現況分析與預測(2023-2030)

AI加速器晶片市場:現況分析與預測(2023-2030) 高效能運算:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測

高效能運算:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測 全球高效能運算市場

全球高效能運算市場 英國高效能運算市場規模、佔有率和趨勢分析報告:2023-2030 年按組件、部署、最終用途和細分市場分類的趨勢

英國高效能運算市場規模、佔有率和趨勢分析報告:2023-2030 年按組件、部署、最終用途和細分市場分類的趨勢 雲端高效能運算市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件(硬體、軟體和服務)、部署類型、工業應用、地區和競爭細分

雲端高效能運算市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按組件(硬體、軟體和服務)、部署類型、工業應用、地區和競爭細分 到 2030 年資料處理單元 (DPU) 市場預測:按組件、類型、資料中心類型、產品類型、用途、最終用戶和地區進行的全球分析

到 2030 年資料處理單元 (DPU) 市場預測:按組件、類型、資料中心類型、產品類型、用途、最終用戶和地區進行的全球分析 高效能運算 (HPC) 市場,按組件、部署、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

高效能運算 (HPC) 市場,按組件、部署、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測 人工智慧 HPC 雲端市場報告:2030 年趨勢、預測與競爭分析

人工智慧 HPC 雲端市場報告:2030 年趨勢、預測與競爭分析 到 2030 年高效能運算市場預測:按組件、運算類型、資料類型、部署、組織規模、伺服器等級、最終用戶和區域進行的全球分析

到 2030 年高效能運算市場預測:按組件、運算類型、資料類型、部署、組織規模、伺服器等級、最終用戶和區域進行的全球分析