|

市場調查報告書

商品編碼

1430575

電容器 -市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Capacitor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

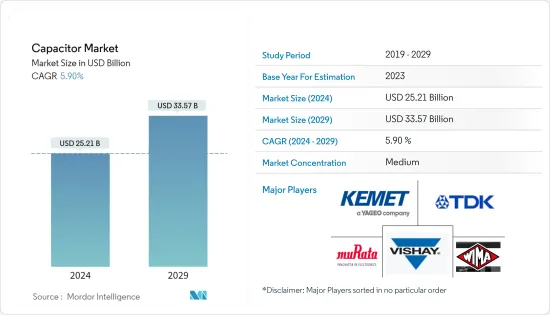

預計2024年電容器市場規模為252.1億美元,預計2029年將達到335.7億美元,在預測期間(2024-2029年)年複合成長率為5.90%。

主要亮點

- PCB 的小型化以及半導體和電路架構的進步為包括智慧型手機在內的各種應用對電容器的需求增加鋪平了道路。

- 隨著通訊基地台變得更小並使用更高的頻寬,由於基板可安裝的組件數量以及組件尺寸和動作溫度的限制,設計變得更加困難。由於成本低且尺寸小,諸如電容器之類的被動元件越來越成為此類應用的首選。

- 5G 智慧型手機的普及及其不斷增加的功能刺激了對進一步小型化和更高密度電子電路的需求。例如,高通、聯發科等多家廠商已經發布了支援5G的晶片組,多家智慧型手機廠商正在使用它們。此前,5G 支援僅限於旗艦手機,但現在中階智慧型手機也支援 5G,並將更便宜的晶片組推向市場。這些努力增加了對陶瓷電容器的需求。

- 其中,積層陶瓷電容(MLCC)是許多電子設備中必不可少的元件,廣泛應用於穿戴式裝置和智慧型手機(智慧型手機配備了約900至1,100個積層陶瓷電容)。此外,物聯網、5G 和電動車等新技術高度依賴 MLCC 的可用性來滿足更高的效率需求。這迫使製造商調整其產品線和生產能力,以滿足這些技術的要求。

- 可再生應用的數量不斷增加,特別是依賴太陽能的手錶和顯示燈等小型設備,為 EDLC 創造了許多應用領域。此外,電雙層電容器與小型電池結合使用,作為電腦記憶體的備用電源。製造商提供基於奈米碳管或石墨烯的電容器,因為它們成本高且擴充性有限。不斷發展的綠色能源應用、提具成本效益以及在多個行業擴展新應用正在推動雙層電容器的進步。

- 為了減小電容器尺寸,製造商正在調整和使用電壓範圍和最佳介電分佈的不同組合,以滿足快速成長的需求。物聯網、消費性電子產品和電動車 (EV) 領域的重大產品開發推動了對電容器的需求,因此這些行業的新進展可能會受到電容器供不應求期間可用性的限制。前置作業時間可能從幾個月到一小時不等。在某些情況下是一年。

電容器市場趨勢

陶瓷電容器佔最大市場佔有率

- 陶瓷電容器因其高可靠性和低製造成本而在大多數電氣設備中最常使用。這些電容器用於多個行業,主要由非極性陶瓷或瓷盤組成。陶瓷材料也是良好的電介質,因為它們具有低電導率並有效支援靜電場。

- 向自動駕駛汽車和 ADAS(高級駕駛輔助系統)等先進車輛的轉變正在推動每輛車使用 MLCC。因此,製造商正在透過與更高電容陶瓷電容器相關的產品創新來應對這些趨勢。

- 例如,2022年2月,村田製作所宣布推出MLCC“NFM15HC435D0E3”,該產品有三個端子,電容為4.3F。此電容器專為汽車應用而設計,可提供 ADAS(高級駕駛員輔助系統)和自動駕駛功能中使用的高性能處理器所需的雜訊抑制和卓越去耦功能。這表明汽車行業對陶瓷電容器的需求正在成長。然而,由於 COVID-19 的持續影響,供應鏈預計將受到干擾,儘管規模較小。

- 此外,電動車對MLCC的需求也在增加。這是因為,由於駕駛輔助功能和全自動駕駛系統等功能的增加,大多數電動車使用了近 10,000 個 MLCC。根據國際能源總署 (IEA) 預測,2022 年全球電動車 (EV) 銷量將激增 60%。這一里程碑意味著銷量首次突破 1,000 萬台,較 2021 年的 660 萬台大幅成長。此外,電動車的高普及和各國政府設定的內燃機引擎的完全淘汰日期可能會推動汽車產業 MLCC 的成長。

- 此外,快速數位化和小型化將顯著增加對 MLCC 的需求,使製造商難以最佳化生產。此外,由於 1825、1206 和 0805 的供應已變得有限,最終用戶正專注於採用較小尺寸的 MLCC,例如 0201 和 0402 尺寸;用戶有望擺脫供應鏈困難。

亞太地區在整個預測期主導市場

- 亞太地區是最重要的電容器市場之一。中國汽車工業正在崛起,在全球汽車市場中發揮越來越重要的作用。政府認為汽車工業,包括汽車零件產業,是國家的支柱產業之一。中國政府預計,到2025年,中國汽車產量將達3,500萬輛。因此,整個全部區域的電容器需求預計將進一步增加。

- 電動車越來越受歡迎,中國被認為是採用電動車的主要國家之一。中國的「十三五」規劃促進了混合動力汽車和電動車等環保交通解決方案的發展,預計將發展該國的交通運輸業。

- 中國的電動車預計將於 2022 年進入全國市場,遠遠領先中國政府的 2025 年預測,數十家競爭對手的新車型吸引了新買家並鼓勵車主轉換電動車。我們正在實現我們的目標普及率達20%。

- 根據中國小客車協會(CPCA)預測,2023年中國小客車銷售量預計將達到2,350萬輛。其中約850萬輛為新能源汽車,新能源汽車普及預計為36%。中國是全球最大的汽車市場。預計這將加速電容器在該國的採用。

- 該地區的市場投資也有所增加。例如,2022 年 1 月,領先的被動元件和子系統設計商和製造商 Excelia 宣布已完成愛爾康電子的多數股權收購。 Alcon Electronics 是一家印度設計和製造公司,主要向可再生能源、醫療影像處理、感應加熱設備、發電和鐵路等終端市場提供目錄和自訂設計的薄膜電解電容器。愛爾康電子為電力電子應用提供各種薄膜電容器和螺絲端子電解電容器。

電容器產業概況

電容器市場是一個半固定市場。市場競爭激烈,全球各大廠商眾多。電容器市場上有一些老字型大小企業進行了大量投資。這些公司利用策略合作計劃來增加市場佔有率和盈利。市場上的知名供應商包括村田製作所、TDK Corporation、KEMET Corporation、Vishay Intertechnology, Inc. 和 WIMA GmbH &Co.KG。

- 2023年11月,ROHM開發了新的矽電容器陣容-BTD1RVFL系列。這些設備在智慧型手機和穿戴式裝置行業中越來越受歡迎。憑藉我們在矽半導體加工方面的豐富經驗,我們實現了更小的尺寸和更高的性能。透過利用薄膜技術,與目前市場上的多層陶瓷電容器 (MLCC) 相比,該公司的矽電容器以更薄的外形提供了更大的電容。

- 2023年4月,京瓷公司宣布其電子元件部門開發出新型EIA0201尺寸電容器(MLCC)。電容器尺寸為 0.6 毫米 x 0.3 毫米。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 價值鏈分析

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 市場宏觀經濟分析

第5章市場動態

- 市場促進因素

- 電動車的普及將推動電容器的需求

- 電訊和電子產業擴大採用電容器

- 市場限制因素

- 先進電容器開發技術力要求

第6章市場區隔

- 按類型

- 陶瓷電容器

- 鉭電容

- 電解電容器

- 紙質和塑膠薄膜電容器

- 超級電容/EDLC

- 按最終用戶產業

- 車

- 工業的

- 航太/國防

- 能源

- 通訊/伺服器/資料存儲

- 消費性電子產品

- 醫療保健

- 按地區

- 南美洲/北美洲

- 歐洲、中東/非洲

- 亞太地區(不包括日本和韓國)

- 日本、韓國

第7章 競爭形勢

- 公司簡介

- Murata Manufacturing Co., Ltd.

- KEMET Corporation

- TDK Corporation

- Vishay Intertechnology, Inc.

- WIMA GmbH & Co. KG

- Panasonic Corporation

- KYOCERA AVX Components Corporation

- WIMA GmbH & Co. KG

- Cornell Dubilier Electronics Inc.

- Yageo Corporation

- Lelon Electronics Corp

- United Chemi-Con(Nippon Chemi-Con Corporation)

- Wurth Elektronik eiSos GmbH & Co. KG

- Eaton Corporation PLC

- Honeywell International Inc.

第8章 市場機會及未來趨勢

The Capacitor Market size is estimated at USD 25.21 billion in 2024, and is expected to reach USD 33.57 billion by 2029, growing at a CAGR of 5.90% during the forecast period (2024-2029).

Key Highlights

- PCB miniaturization and advancements in semiconductor and circuit architectures paved the way for the rise in demand for capacitors in various applications, including smartphones.

- As communication base stations become increasingly smaller and use higher frequency bands, designing is becoming more difficult owing to the limited number of components mounted on the substrate and restrictions on the size and operating temperature of components. Due to their lower cost and small size, passive components like capacitors are increasingly preferred for these applications.

- The widespread adoption of 5G smartphones and their increasing functionality stoke demand for further miniaturization and higher electronic circuitry density. For instance, several manufacturers, such as Qualcomm and MediaTek, are introducing chipsets that support 5G, which multiple smartphone manufacturers use. Previously, 5G support was confined to only flagship mobiles; now, mid-level smartphones also support 5G to introduce cheaper chipsets in the market. Such initiatives are increasing the need for ceramic capacitors.

- Among the applications, multilayer ceramic capacitors (MLCC) are essential components of many electronic devices and are widely used in wearable devices and smartphones (approximately 900 to 1100 multilayer ceramic capacitors are installed in smartphones). Moreover, new technologies, like IoT, 5G, and EVs, are highly dependent on the availability of MLCCs, as these fulfill higher efficiency needs. This has driven manufacturers to align their product lines and production capacities to meet the requirements of these technologies.

- Renewable applications such as solar energy-dependent watches and display lights, among other small devices, have increased and have created many application areas for EDLC. In addition, electric double-layer capacitors are used as backup sources of memory in computers and are used together with small batteries. Manufacturers provide these capacitors based on carbon nanotubes and graphene due to the high costs and their limited scalability. Due to evolving green energy applications, improving price-performance ratios, and growing new applications across several industries, there are advancements in double-layer capacitors.

- To reduce the size of the capacitors, the manufacturers are adopting and using various combinations, such as voltage range and optimal dielectric spread, to fulfill the surging needs. As the demand for capacitors is fueled by significant product development in the IoT, consumer electronics, and electric vehicles (EV), any new advancements in these industries have become limited by the capacitor's availability during the shortage, with lead times extending from several months to a year in some cases.

Capacitor Market Trends

Ceramic Capacitors to Hold the Largest Market Share

- Ceramic capacitors are one of the most commonly used in most electrical instruments, as they offer reliability and are cheaper to manufacture. These capacitors are used in multiple industries and primarily consist of ceramic or porcelain discs that exist in a non-polarized form. The ceramic material is also an excellent dielectric due to its poor conductivity and its efficient support of electrostatic fields.

- The shift towards sophisticated vehicles, such as self-driving vehicles and ADAS (Advanced Driver Assistance Systems), is driving the use of MLCCs per vehicle. Therefore, manufacturers are involved in product innovation related to higher capacitance for ceramic capacitors to cater to such a trend.

- For instance, in February 2022, Murata Manufacturing Co., Ltd. announced the launch of the NFM15HC435D0E3 MLCC, designed with 3 terminals to provide a capacitance of 4.3 F. The capacitor is designed for automotive applications to attain results on noise removal and superior decoupling that are required for high-performance processors employed in advanced driver assistance systems and autonomous driving functions. This indicates the growing demand for ceramic capacitors in the automotive industry. However, with the impact of the constant COVID-19 pandemic, the supply chain is expected to be disrupted on a small scale.

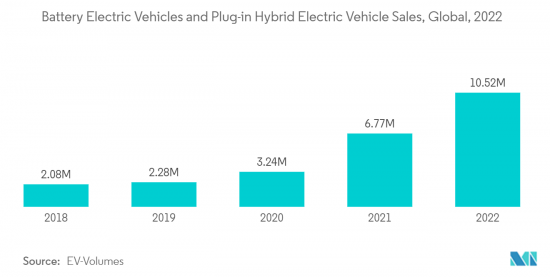

- Moreover, the demand for MLCC in electric vehicles is also increasing, as most of the EVs use close to 10,000 MLCC due to increased features like driver assistance functions and fully autonomous systems. As per the International Energy Agency (IEA), there has been a noteworthy 60% surge in global electric vehicle (EV) sales in 2022. This milestone achievement marks the first time sales have exceeded 10 million units, showing remarkable growth from the 6.6 million units sold in 2021. Further, the high adoption of EVs and the complete phase-out dates of ICE engines set by various governments will drive the growth of MLCC in the automotive sector.

- The demand for MLCCs is also going to increase considerably due to rapid digitalization and miniaturization, and the manufacturers are going to find it hard to optimize their production. Moreover, end users are focusing on incorporating smaller formats of MLCCs, such as the 0201 or 0402 sizes, to make them future-proof, as the availability of 1825, 1206, and 0805 is becoming limited, and the use of smaller formats is expected to insulate the end users from supply chain difficulties.

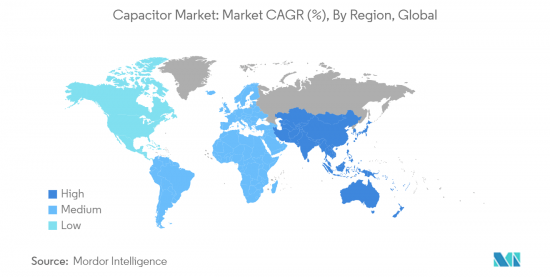

Asia-Pacific Region will Dominate the Market Throughout the Forecast Period

- The Asia-Pacific region is one of the most prominent markets for capacitors. The automotive industry is increasing in China, and the country plays an increasingly important role in the global automotive market. The government views its automotive industry, including the auto parts sector, as one of the country's pillar industries. The government of China estimates that China's automobile output is expected to reach 35 million units by 2025. Consequently, the demand for capacitors is anticipated to increase further across the region.

- The popularity of EVs is growing, and China is regarded as one of the dominant adopters of electric vehicles. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric cars, for advancements in the country's transportation sector.

- China's electric cars are on their way to reaching the 20% nationwide penetration goal in 2022, well ahead of the Chinese government's 2025 forecast, due to new models by dozens of competitors attracting new buyers and encouraging owners to switch to electric vehicles.

- According to the China Passenger Car Association (CPCA), sIt is anticipated that China's passenger car sales will amount to 23.5 million units in 2023. Among these, approximately 8.5 million units are projected to be NEVs, with an expected NEV penetration rate of 36%. China is the leading world's largest vehicle market. This is anticipated to boost the adoption of capacitors in the country.

- The region is also witnessing increasing investments in the market. For instance, in January 2022, Exxelia, a leading designer and manufacturer of passive components and subsystems, announced that it completed the majority acquisition of Alcon Electronics. Alcon Electronics is an Indian designer and manufacturer of catalog and custom-designed film and aluminum electrolytic capacitors, primarily serving the renewable energy, medical imaging, induction heating equipment, power generation, and railway end markets. Alcon Electronics provides a wide range of film and screw-terminal aluminum electrolytic capacitors for power electronic applications.

Capacitor Industry Overview

The capacitor market is a semi-consolidated market. The market is competitive with the presence of various large-scale manufacturers in the market across the globe. The capacitor market has long-standing established players who have made significant investments. These companies leverage strategic collaborative initiatives to increase their market share and profitability. Some of the prominent vendors in the market include Murata Manufacturing Co., Ltd., TDK Corporation, KEMET Corporation, Vishay Intertechnology, Inc., and WIMA GmbH & Co. KG, among others.

- November 2023: ROHM has developed the BTD1RVFL series, a new line of silicon capacitors. These devices are gaining popularity in the smartphone and wearable device industries. Due to their extensive experience in silicon semiconductor processing, the company has achieved higher performance in a more compact design. By utilizing thin-film technology, their silicon capacitors offer a greater capacitance in a thinner form compared to the current multilayer ceramic capacitors (MLCCs) available in the market.

- April 2023: Kyocera Corporation announced that the company's Electronic Components Division developed a new capacitor (MLCC) with EIA 0201 size, with a capacitance of 10 microfarads, which the company claims to be the industry's highest among MLCCs in the 0201 case size. The dimensions of the capacitor are 0.6 mm x 0.3 mm.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Buyers

- 4.3.2 Bargaining Power of Suppliers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Macro-Economic Analysis of the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Adoption of EVs to Boost the Demand for Capacitors

- 5.1.2 Increasing Adoption of Capacitors in the Telecom and Electronics Industry

- 5.2 Market Restraints

- 5.2.1 Requirement of Technical Competence for Developing Advanced Capacitors

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Ceramic Capacitors

- 6.1.2 Tantalum Capacitors

- 6.1.3 Aluminum Electrolytic Capacitors

- 6.1.4 Paper and Plastic Film Capacitors

- 6.1.5 Supercapacitors/EDLCs

- 6.2 By End-user Industry

- 6.2.1 Automotive

- 6.2.2 Industrial

- 6.2.3 Aerospace and Defense

- 6.2.4 Energy

- 6.2.5 Communications/Servers/Data Storage

- 6.2.6 Consumer Electronics

- 6.2.7 Medical

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe, Middle East and Africa

- 6.3.3 Asia Pacific (Excl. Japan and South Korea)

- 6.3.4 Japan and South Korea

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Murata Manufacturing Co., Ltd.

- 7.1.2 KEMET Corporation

- 7.1.3 TDK Corporation

- 7.1.4 Vishay Intertechnology, Inc.

- 7.1.5 WIMA GmbH & Co. KG

- 7.1.6 Panasonic Corporation

- 7.1.7 KYOCERA AVX Components Corporation

- 7.1.8 WIMA GmbH & Co. KG

- 7.1.9 Cornell Dubilier Electronics Inc.

- 7.1.10 Yageo Corporation

- 7.1.11 Lelon Electronics Corp

- 7.1.12 United Chemi-Con (Nippon Chemi-Con Corporation)

- 7.1.13 Wurth Elektronik eiSos GmbH & Co. KG

- 7.1.14 Eaton Corporation PLC

- 7.1.15 Honeywell International Inc.

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球電容器組市場規模、佔有率、成長分析,依類型(自動、固態接觸器)、依應用(電氣網路、工業)- 2024-2031 年產業預測

全球電容器組市場規模、佔有率、成長分析,依類型(自動、固態接觸器)、依應用(電氣網路、工業)- 2024-2031 年產業預測 2030 年電容器市場預測:按產品類型、實施類型、電壓、應用、最終用戶和地區進行的全球分析

2030 年電容器市場預測:按產品類型、實施類型、電壓、應用、最終用戶和地區進行的全球分析 全球三相電力電容器市場評估:依產品類型、額定電壓、應用、最終用戶、地區、機會、預測(2017-2031)

全球三相電力電容器市場評估:依產品類型、額定電壓、應用、最終用戶、地區、機會、預測(2017-2031) 混合電容器市場:按產品類型、按應用分類:2023-2032 年全球機會分析與產業預測

混合電容器市場:按產品類型、按應用分類:2023-2032 年全球機會分析與產業預測 鋰離子電容器和其他電池超級電容器混合動力(BSH)儲能:市場詳細分析.路線圖.技術詳細分析.製造商評估.下一次成功(2024-2044)

鋰離子電容器和其他電池超級電容器混合動力(BSH)儲能:市場詳細分析.路線圖.技術詳細分析.製造商評估.下一次成功(2024-2044) 彈性表面波延遲線市場報告:2030 年趨勢、預測與競爭分析

彈性表面波延遲線市場報告:2030 年趨勢、預測與競爭分析 抑制電容器市場報告:2030 年趨勢、預測與競爭分析

抑制電容器市場報告:2030 年趨勢、預測與競爭分析 聚合物鉭電容器市場報告:2030 年趨勢、預測與競爭分析

聚合物鉭電容器市場報告:2030 年趨勢、預測與競爭分析 開關電容轉換器市場報告:2030 年趨勢、預測與競爭分析

開關電容轉換器市場報告:2030 年趨勢、預測與競爭分析 電解電容器市場 - 2019-2029 年按產品類型(鋁、鉭、鈮)、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測

電解電容器市場 - 2019-2029 年按產品類型(鋁、鉭、鈮)、地區和競爭細分的全球行業規模、佔有率、趨勢、機會和預測