|

市場調查報告書

商品編碼

1408451

工業邊緣運算 -市場佔有率分析、產業趨勢/統計、2024-2029 年成長預測Industrial Edge Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

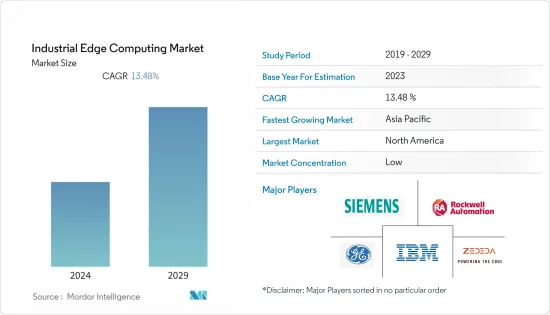

本會計年度工業邊緣運算市場規模預估為438.4億美元,預估未來五年將達到825億美元,預測期內複合年成長率為13.48%。

主要亮點

- 企業對邊緣運算的需求不斷成長,因為他們了解邊緣運算在改變製造業方面的巨大潛力。邊緣運算使公司能夠利用 IT 和 OT 融合、即時資料處理和高級分析的力量來提高製造效率、降低成本並改善業務成果。

- 工廠自動化、物聯網的使用以及汽車和物流等各種最終用戶行業中連網型設備的應用等不斷上升的趨勢正在創造市場需求。

- Industrial Edge 可讓您透過向雲端發送更少的資料來節省網路頻寬。本地處理資料還可以最大限度地減少雲端處理和儲存成本。當運算和儲存分散時,資料外洩或網路攻擊導致整個網路癱瘓的風險就會降低。 Industrial Edge 還結合了 IT 和營運技術 (OT),以實現複雜的資料分析和重大營運改進。 OT 和業務系統之間的即時、事件驅動的互動有助於最大限度地發揮工業自動化的價值。

- 工業邊緣運算還具有節省成本的優勢。將資料傳輸資料集中式資料集的成本很高,因此您可以透過將此類資料儲存在邊緣並在使用後進行處理來降低成本。邊緣運算還可以更輕鬆地追蹤製造車間中各個器材與設備的實施情況。這些資料可協助製造商最佳化設備效能,同時降低成本和危險情況。

- 很少有組織有能力在遠端位置安裝冗餘的高階伺服器、儲存和網路設備。相反,您可以在沒有冗餘元件(例如電源或硬碟)的商用伺服器上安裝所需的應用程式。更糟的是,邊緣定位可能沒有伺服器機房或其他用於 IT 設備的環境控制空間。缺乏足夠的電力、冗餘、冷卻和通風可能是該行業面臨的挑戰。

- 汽車產業正試圖從 COVID-19 時代的收入損失中恢復過來。製造業之間日益激烈的競爭正在推動後競爭時代對工業邊緣運算的需求,因為他們擴大選擇市場上可用的新技術。邊緣運算解決方案提供者也與製造商合作,產生新的想法和獨特的解決方案。這些因素使工業邊緣運算解決方案提供者和製造商能夠實現快速、實際的現金流效益。

工業邊緣運算市場趨勢

石油和天然氣產業預計將高速成長

- 當前全球油氣市場的不確定性加劇了油氣產業的競爭。這迫使公司降低營運成本和資本支出。此外,邊緣運算和物聯網 (IoT) 等技術的興起正在為產業帶來數位轉型。

- 物聯網的變革潛力尚未被開發,因為該行業在數位化和自動化方面需要趕上製造業等其他產業。公司必須利用這項變化來提高生產力、降低成本並在當今的市場中保持競爭力。

- 由於石油和天然氣價格持續波動,企業開始轉向像邊緣基礎設施編配的領導者ZEDEDA這樣的公司,利用資料的力量和提高機械化程度來最佳化流程並在競爭中試圖獲得優勢。透過減少設備故障、安全問題和保持法規遵從性,從石油鑽井平台、油井、煉油廠等邊緣的條件提供有用、可操作的見解,可以節省數百萬美元。然而,這些環境可能非常偏遠且現場工作人員有限,因此應對這些挑戰需要一種能夠簡化邊緣基礎設施處理和保護所需工具的設計。

- 邊緣運算透過降低網路頻寬和資料中心成本來節省成本。透過邊緣運算最大限度地減少計劃外停機也可以帶來顯著的好處。麻省理工學院斯隆管理學院的一項研究發現,液化天然氣 (LNG) 設施每天的停機成本為 2500 萬美元,而典型的中型液化天然氣設施每年大約會停機五次。我確實是這樣。邊緣運算透過減輕IT基礎設施的處理負擔來防止代價高昂的停機。

- 石油和天然氣海上結構每天都會產生大量資料。根據思科的報告,石油鑽井平台每天產生 2 Terabyte的資料。然而,由於海上石油和天然氣行業的遠端性質,如果沒有邊緣運算解決方案的支持,就無法探索或利用這些資料進行決策。

- 施耐德電機最近的一篇部落格強調了減少延遲的重要性,這是離岸組織採用邊緣平台的一個引人注目的因素。零接觸邊緣運算有助於即時資料組織並增強通訊、儲存和分析功能。這有助於做出更資訊、更及時的關鍵業務決策。

亞太地區預計將佔據較大佔有率

- 亞洲的主要新興市場包括印度、中國、菲律賓、印尼和越南。此外,馬來西亞、新加坡、泰國等國家也引起了廣泛關注。這些國家正在經歷顯著的消費者成長、快速的技術採用和數位轉型。例如,到 2025 年,菲律賓的網路經濟預計每年成長 30%。預計到 2026 年,印度將擁有 10 億智慧型手機用戶,Google預測越南將成為未來十年成長最快的網路經濟體之一。

- 然而,隨著亞洲新興市場越來越多的人同時連接和存取數位服務,本地網路的壓力越來越大。公共網路擁塞已成為新興亞洲企業最關心的問題,導致延遲和抖動等問題,可能對使用者體驗產生負面影響。隨著消費者越來越需要隨時隨地可靠、快速的數位服務,無法滿足這些期望的企業可能會影響收益。

- 此外,政府為增強數位化提供的資金增加以及企業對資料處理和儲存的需求不斷增加也促進了市場的成長。智慧城市中新的物聯網應用的興起將產生大量資料。對靠近資料來源的經濟高效的資料分析和處理的需求不斷成長,導致了雲端運算的採用,推動了該領域的成長。

- 亞洲多重雲端平台的發展正在刺激電腦工程領域高技能勞動力的成長。專注於數位工具和技術的企業,以及新加坡和印度等國家之間在數位健康、智慧城市和基於 IT 的基礎設施等領域的基於技術的合作,正在展示邊緣運算如何在亞洲企業中佔據一席之地。我們如何收集的範例。透過利用邊緣運算平台,亞洲企業可以緩解因消費者激增而造成的基礎設施瓶頸。值得注意的是,新加坡的多重雲端平台已成為企業組織效益的基準。

- 例如,2022 年 9 月,Bharti Airtel 和 IBM 合作部署了 Airtel 的邊緣運算平台。這項措施使汽車和製造業等各行業的大公司能夠加速創新解決方案。印度最大的汽車製造商馬魯蒂SUZUKI計劃使用 Edge 平台來提高工廠車間品質檢查的效率和準確性。馬魯蒂鈴木希望透過建立這個平台來改善品管並確保邊緣資料安全。

- 作為一個組織,Nife 幫助企業建立未來的經營模式,提供強大的數位體驗,增加額外的安全層。基於邊緣運算平台的模型可以快速擴展並具有全局擴展因子,從而在擴展到新的離岸市場時節省成本。這些因素使本地邊緣運算公司受益匪淺,使其能夠在全球多重雲端服務中有效競爭。

- 為了滿足不斷成長的需求,公司經常實施自動化策略以維持生產環境的高效率。因此,與三大油氣領域相比,下游領域的自動化普及相對較高。

工業邊緣運算產業概況

工業邊緣運算市場的特徵是分散化和競爭激烈。目前主導市場的一些主要企業包括西門子、ZEDEDA、通用電氣公司和羅克韋爾自動化。通用電氣 (GE) 等公司以其在航太和製造等各行業提供邊緣運算解決方案的專業知識而聞名,並在市場中佔據重要地位。這些供應商採取了關鍵的競爭策略,包括收購、與產業參與企業結盟以及推出新產品和服務。市場最近的顯著發展包括:

2022年11月,羅克韋爾自動化宣布開發結合邊緣應用生態系統的編配與智慧型邊緣管理平台。該舉措基於開放的行業標準和零信任安全原則,旨在加速工業客戶的數位轉型之旅。隨著工業設備製造商擴大接受數位轉型,該公司希望透過分析、人工智慧 (AI) 和製造執行系統 (MES) 等創新來擴大其數位轉型工作。這種方法提供了對接近工業資料來源的即時情報的存取。

2023年8月,ABB與專注於邊緣到雲端加速平台的Pratexo合作並進行了策略性投資。此次合作將使 ABB 客戶能夠部署基於邊緣的網路和解決方案架構,以提供即時洞察。重點是要增強資料隱私和安全性,減少傳輸到雲端的資料量,並在斷網時也能進行操作。此次戰略合作是推動工業領域邊緣運算解決方案的重要一步。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵對關係

- 產業價值鏈分析

- COVID-19 市場影響評估

第5章市場動態

- 市場促進因素

- 工業領域對自動化的需求不斷增加

- 組織從雲端運算和儲存系統轉向邊緣運算

- 市場抑制因素

- 向老化勞動力引入新技術會暴露技能差距

第6章市場區隔

- 按成分

- 硬體

- 軟體

- 服務

- 按行業分類

- 製造業

- 油和氣

- 礦業

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 中美洲和南美洲

- 中東/非洲

第7章 競爭形勢

- 公司簡介

- IBM Corporation

- Rockwell Automation

- Siemens

- General Electric Company

- Honeywell International

- Huawei Technologies

- Microsoft Corporation

- SAP SE

- Intel Corporation

第8章投資分析

第9章 市場機會及未來趨勢

The industrial edge computing market size is estimated at USD 43.84 billion in the current year and is expected to reach USD 82.50 billion in the next five years, registering a CAGR of 13.48% during the forecast period.

Key Highlights

- The need for edge computing is growing among businesses because they understand the tremendous potential of edge computing in transforming the manufacturing industry. Edge computing enables organizations to leverage the power of IT and OT convergence, real-time data processing, and advanced analytics to drive efficiencies, reduce costs, and improve business outcomes in manufacturing.

- The increasing trend of factory automation, usage of IoTs, and the application of connected devices across various end-user industries such as automobile and logistics are creating a demand for the market.

- The industrial edge allows organizations to conserve network bandwidth by reducing the data sent to the cloud. Organizations can also minimize cloud computing and storage costs by processing data locally. When computing and storage are decentralized, there's less risk that data will be compromised or a cyberattack will take down the entire network.The industrial edge also combines IT with operational technology (OT), allowing complex data analysis and significant operation improvements. Real-time, event-driven interactions between OT and business systems help maximize industrial automation's value.

- Industrial edge computing also provides cost-reduction benefits. Transferring large data sets of temporary or unimportant data to a centralized cloud is cost-prohibitive, so keeping such data at the edge and discarding it after use lowers the cost. Edge computing also makes tracking individual devices or equipment implementation on a shop floor easy. This data will assist the manufacturer in optimizing equipment performance while decreasing costs and hazardous circumstances.

- Few organizations can afford to establish redundant high-end servers, storage, and networking equipment in remote locations. Instead, they may install required applications on commodity servers that don't have redundant components (such as power supplies and hard drives). Worse still, edge locations may not contain a server room or other environmentally controlled space for IT equipment. The lack of adequate power, redundancy, cooling, or ventilation can be a challenge for the industry.

- The automotive industry is set to recover from the loss of revenue from the COVID-19 years. Manufacturing companies are opting for new technologies available in the market, and the rising competition in these companies has fueled the demand for industrial edge computing in post-COVID times. Edge computing solution providers also produce new ideas and signature solutions in collaboration with manufacturers. These factors result in rapid and tangible cash flow benefits for industrial edge computing solution providers and manufacturers.

Industrial Edge Computing Market Trends

Oil and Gas sector is expected to grow at a higher pace

- The current uncertainty around the global market for oil and natural gas has boosted the highly competitive nature of the oil and gas industry. This has pressured companies to reduce their operating costs and capital expenditures. Also, the industry is transforming digitally due to the rise of technologies such as edge computing and the Internet of Things (IoT).

- The industry needs to catch up to other sectors, such as manufacturing when it comes to digitalization and automation, so the potential for IoT to be transformative remains to be explored. Companies must leverage this change to increase their productivity and cut costs, enabling them to stay competitive in today's market.

- As oil and gas prices remain volatile, companies are looking to companies like ZEDEDA, the leader in edge infrastructure orchestration, to leverage the power of data and increased mechanization to optimize processes and gain a competitive edge. Pulling convenient actionable insights from edge conditions like oil rigs, wells, and refineries can save millions by reducing equipment failure and safety issues and maintaining regulatory compliance. These conditions, however, can be very remote and may have limited on-site staff, so managing these challenges requires tools designed to simplify handling and securing edge infrastructure.

- Edge computing introduces cost savings by lowering the network bandwidth and reducing data center costs. Minimizing unplanned downtime through edge computing can also lead to significant payoffs. An MIT Sloan study found that a single day of downtime for a liquefied natural gas (LNG) facility can cost USD 25 million, with a typical midsize LNG facility going down about five times a year. Edge computing prevents costly shutdowns by reducing the processing burden on IT infrastructure.

- Offshore oil and gas structures produce an extraordinary amount of data daily. According to a Cisco report, an oil rig can create two terabytes of data daily. Still, due to the remote area of the offshore oil and gas industry, this data is only examined and leveraged for decision-making with support from edge computing resolutions.

- A recent blog from Schneider Electric underscores the significance of latency reduction as a compelling factor driving offshore organizations to adopt edge platforms. Zero-touch edge computing facilitates real-time data organization, enhancing communication, storage, and analysis capabilities. This, in turn, contributes to more informed and timely business-critical decision-making.

Asia- Pacific is anticipated to hold the significant share

- Asia's top emerging markets encompass India, China, the Philippines, Indonesia, and Vietnam. Additionally, countries like Malaysia, Singapore, and Thailand are attracting significant attention. These economies are undergoing substantial growth in their consumer classes, rapid technological adoption, and digital transformation. For instance, the Philippines is experiencing a 30% annual growth in its Internet economy through 2025. India is projected to have 1 billion smartphone users by 2026, and Google predicts that Vietnam will be one of the fastest-growing Internet economies in the next decade.

- However, as more individuals across Asia's emerging markets simultaneously connect and access digital services, there is a growing strain on local networks. Public internet congestion has become a top concern for companies in emerging Asia, resulting in issues such as latency and jitter, which can adversely affect user experiences. In an era where consumers increasingly expect reliable and fast digital services anytime, anywhere, businesses failing to meet these expectations risk impacting their bottom line.

- Furthermore, increased government funding to enhance digitization and the growing demand for businesses to process and store data contribute to market growth. The rise of emerging IoT applications in smart cities generates vast amounts of data. The increasing need for cost-effective data analysis and processing near the data source has led to the adoption of cloud computing, driving segment growth.

- The development of multi-cloud platforms in Asia has spurred the growth of a high-skilled workforce in computer engineering. Businesses focused on digital tools and techniques, as well as technology-based collaboration between countries like Singapore and India in areas such as digital health, smart cities, and IT-based infrastructure, are examples of how edge computing is gaining traction in Asian enterprises. By using edge computing platforms, Asian organizations can alleviate infrastructure bottlenecks caused by the surge in consumers. Notably, Singapore's multi-cloud platform serves as a benchmark for its benefits to business organizations.

- For instance, in September 2022, Bharti Airtel and IBM partnered to deploy Airtel's edge computing platform. This initiative enables large enterprises across various industries, including automotive and manufacturing, to accelerate innovative solutions. Maruti Suzuki, India's largest carmaker, plans to use the edge platform to enhance efficiency and accuracy in quality inspections on the factory floor. By establishing this platform, Maruti Suzuki expects to improve quality control and ensure data security at the edge.

- Nife, as an organization, assists enterprises in building future business models that offer robust digital experiences with an added layer of security. Models based on edge computing platforms are rapidly scalable and possess a global scaling factor, which can result in cost savings when expanding into new offshore markets. These factors are significantly benefiting local edge computing enterprises, allowing them to compete effectively in multi-cloud services on a global scale.

- In response to increasing demand, companies often implement automation strategies to maintain high efficiency in their production environments. Consequently, compared to all three oil and gas streams, automation penetration is relatively high in the downstream sector.

Industrial Edge Computing Industry Overview

Its fragmentation and competitive nature characterize the industrial edge computing market. Currently, key players dominating the market include Siemens, ZEDEDA, General Electric Company, and Rockwell Automation, among others. Companies like General Electric (GE), renowned for their expertise in delivering edge computing solutions across various industries, including aerospace and manufacturing, hold substantial market positions. These vendors employ key competitive strategies, such as acquisitions, partnerships with industry players, and the introduction of new products and services. Notable recent developments in the market include:

In November 2022, Rockwell Automation announced the development of an orchestration and intelligent edge management platform coupled with an edge application ecosystem. This initiative is based on open industry standards and zero trust security principles, aimed at accelerating the digital transformation journey for industrial customers. As industrial manufacturers increasingly embrace digital change, the company seeks to amplify digital transformation efforts through innovations in analytics, artificial intelligence (AI), Manufacturing Execution Systems (MES), and other technologies. This approach allows them to access real-time intelligence closer to the source of industrial data.

In August 2023, ABB made a strategic investment by partnering with Pratexo, a company specializing in edge-to-cloud acceleration platforms. This collaboration empowers ABB's customers to deploy edge-based networks and solution architectures that provide real-time insights. Importantly, it offers enhanced data privacy and security, reduces the volume of data transferred to the cloud, and enables operations even when disconnected from the internet. This strategic partnership represents a significant step in advancing edge computing solutions within the industrial sector.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand For Automation in the Industrial Sector

- 5.1.2 Organizations shifting from cloud computing and storage systems to edge computing

- 5.2 Market Restraints

- 5.2.1 Introduction of a new technology to an ageing workforce exposes the skills gap

6 MARKET SEGMENTATION

- 6.1 By Component

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By End-user Vertical

- 6.2.1 Manufacturing

- 6.2.2 Oil and Gas

- 6.2.3 Mining

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Latin Amerca

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Rockwell Automation

- 7.1.3 Siemens

- 7.1.4 General Electric Company

- 7.1.5 Honeywell International

- 7.1.6 Huawei Technologies

- 7.1.7 Microsoft Corporation

- 7.1.8 SAP SE

- 7.1.9 Intel Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

人工智慧邊緣運算市場:按組件、資料來源、應用程式和最終用戶分類 - 2024-2030 年全球預測

人工智慧邊緣運算市場:按組件、資料來源、應用程式和最終用戶分類 - 2024-2030 年全球預測 全球邊緣運算市場規模、佔有率、成長分析(按類型、最終用戶)- 產業預測,2024-2031 年

全球邊緣運算市場規模、佔有率、成長分析(按類型、最終用戶)- 產業預測,2024-2031 年 邊緣人工智慧軟體全球市場規模、佔有率、成長分析:按組件、資料來源分類 - 產業預測(2024-2031)

邊緣人工智慧軟體全球市場規模、佔有率、成長分析:按組件、資料來源分類 - 產業預測(2024-2031) 2024 年邊緣 AI 軟體全球市場報告

2024 年邊緣 AI 軟體全球市場報告 多接取邊緣運算全球市場規模、佔有率和成長分析:按解決方案、最終用途 - 產業預測 (2024-2031)

多接取邊緣運算全球市場規模、佔有率和成長分析:按解決方案、最終用途 - 產業預測 (2024-2031) 全球多接入邊緣運算市場 2024-2031

全球多接入邊緣運算市場 2024-2031 邊緣運算:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

邊緣運算:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 安全存取服務邊際市場:按服務提供、組織規模和應用分類:2023-2032 年全球機會分析和產業預測

安全存取服務邊際市場:按服務提供、組織規模和應用分類:2023-2032 年全球機會分析和產業預測 醫療保健邊緣運算市場:按組件、應用程式和最終用戶分類 - 2024-2030 年全球預測

醫療保健邊緣運算市場:按組件、應用程式和最終用戶分類 - 2024-2030 年全球預測 2024 年超大規模邊緣運算全球市場報告

2024 年超大規模邊緣運算全球市場報告