|

市場調查報告書

商品編碼

1406116

白車身:市場佔有率分析、產業趨勢與統計、2024-2029 年成長預測Automotive Body-in-White - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

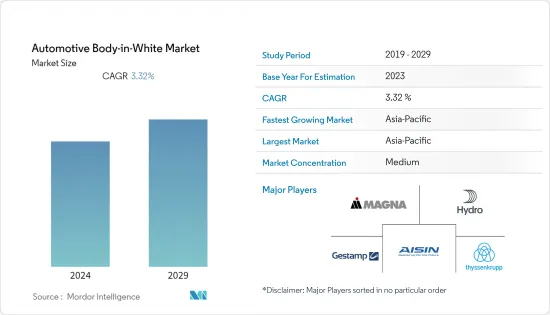

汽車白車身市場規模預計為991.2億美元。

預計五年內將達到 1,167 億美元,預測期內複合年成長率為 3.32%。

主要亮點

- 從長遠來看,嚴格的環境和排放法規以及汽車中擴大採用輕量材料以提高燃油效率預計將在預測期內推動市場需求。

- 過去十年固體雷射光源的發展為白車身組裝提供了新的焊接解決方案。特別是,提高電力效率(降低成本)以及將光纖與長工作距離相結合(工具彈性)的能力提供了新的可能性。

- 例如,柯馬在2023年4月透露,已為海看汽車技術的車架線提供高度智慧型的焊接解決方案。此解決方案可確保新能源汽車的多車型生產、高JPH(每小時作業數)並切實減少生產損失。用於海燦杭州生產工廠。可在4個不同平台之間任意遷移,並與現有生產平台完全相容,批量生產循環效率60 JPH的純電動車A06和SUV Z03。該解決方案是對柯馬開放式框架技術的改進,可實現靈活、精確的白車身結構和虛擬試運行。

- 此外,對新合金和高效製造技術的持續研究和開發,以及對生產過程中自動化和機器人的投資增加,將為市場參與者提供新的機會。除此之外,白車身是每輛車的必備結構。因此,汽車產業的開拓也有望刺激全球白色家電市場的成長。

- 例如,NDR Auto Component Limited 在 2023 年 6 月強調了座椅金屬零件和裝飾件(裝飾罩)的重要性。該公司的研發團隊目前正在研究這些領域的多個產品系列。該公司的金屬零件團隊生產小客車座椅框架、小客車白車身(BIW)零件和兩輪車零件。

- 預計亞太地區在預測期內成長最快,其次是歐洲和北美。由於印度和中國等國家採取的政府舉措,促進製造業發展並促進該市場的成長,預計亞太地區將呈現樂觀成長。

汽車白車身市場趨勢

對輕型車的需求不斷成長推動汽車白色家電市場

- 在白車身市場,鋁、鎂合金、纖維增強塑膠(FRP)等輕量材料的開發正在取得進展,使得生產用於輕型車的白車身產品成為可能。影響輕量材料技術的其他因素是客戶主導的要求,例如造型、美觀、NVH(噪音、振動、聲振粗糙度)方面的降低和舒適度。

- 省油車需求增加的主要動力是實施更嚴格的排放氣體和安全法規。因此,為了遵守更嚴格的廢氣和燃油效率法規,一些汽車製造商專注於減輕車輛的整體重量並提高燃油效率,而另一些汽車製造商則結成聯盟和合作夥伴關係以穩定自己的市場地位。

- 例如,2022年9月,開發電動作業車及其電池和動力來源的Atris Motor Vehicles與全球頂級汽車鋼材製造商安賽樂米塔爾建立了合作夥伴關係。安賽樂米塔爾的 S-in Motion 皮卡車模型、駕駛室和貨箱設計將有助於設計 XT,這是一款面向農民、建設業工人和車隊所有者的全電動皮卡車。安賽樂米塔爾開發了 S-in-Motion,這是一系列輕鋼解決方案,旨在為製造商製造更輕、更安全、更生態的車輛。 Atris 利用安賽樂米塔爾的白車身 CAD 工程資訊來改善 XT 的續航里程,同時減輕重量和成本。

- 2023 年 3 月,蘭博基尼公佈了該公司首款高性能電動車(HPEV) 超級跑車 LB744 的關鍵細節。這款令人難以置信的車輛作為世界上第一輛高性能電動車 (HPEV) 取得了開創性的成就。它採用插電式混合配置,巧妙地將輕質高功率鋰離子電池放置在底盤中央的傳動通道內。與先前的 V12 引擎相比,這種創新方法不僅可以減少排放氣體,還可以提高性能。革命性的 L545 引擎容量為 6.5 升,是蘭博基尼有史以來生產的最輕、最強大的 12 缸引擎。總重量僅218公斤,比Aventador輕了17公斤。

- 2023 年 8 月,為慶祝成立 60 週年,保時捷推出了一款特別版 911,旨在最大限度地提高駕駛樂趣。保時捷 911 S/T 限量生產 1,963 輛,提供輕量化設計和純粹、純粹的駕駛體驗。 911 GT3 RS 的高轉速 518bhp 引擎首次透過手排變速箱和輕型離合器傳遞到道路上。

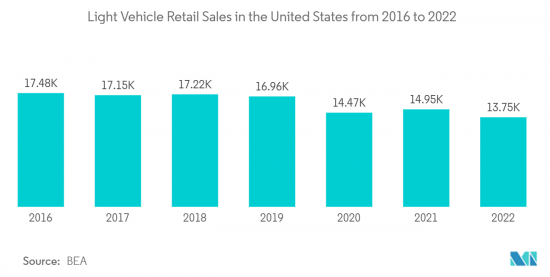

- 此外,美國汽車業預計到 2022 年將銷售約 1,375 萬輛輕型汽車。該統計數據包括零售的約 290 萬輛小客車和近 1,090 萬輛輕型卡車。

- 因此,隨著製造商專注於引入創新技術和製造流程以從競爭對手中脫穎而出,汽車白車身市場預計將在預測期內顯著成長。

預計亞太地區在預測期內成長最快

- 預計亞太地區將在預測期內做出重大貢獻。汽車產量的成長以及政府對鼓勵電動車的政策和舉措的日益重視舉措會在預測期內提振白車身市場。印度和中國等主要國家的崛起預計將補充亞太地區的市場開拓。

- 例如,2023年上半年,印度電動車零售超過70萬輛。根據Vahan統計,截至2023年6月的整體銷售量為721,971輛,是EV India 2022年銷售量的73%。各國政府正在透過投資基礎設施和為首次購買電動車的人提供補貼,鼓勵從傳統燃油汽車過渡到綠色燃油汽車。

- 由於幾家主要企業正在進行大量投資並與其他參與者推出合資企業以滿足不斷成長的需求,預計市場在預測期內將保持高度競爭。

- 例如,2022年7月,蒂森克虜伯股份公司宣布擴大在中國的汽車車身業務。該公司將投資800萬歐元(940萬美元)在江蘇省崑山市設立蒂森克虜伯汽車裝備(蘇州)有限公司,該工廠預計於2022年12月開始營運。該工廠將是一座白車身工廠,將為中國汽車製造商製造模具和設備。

- 由於上述趨勢和發展,亞太市場預計在預測期內將以健康的速度成長。

汽車白車身產業概況

隨著區域和全球產業巨頭的出現,汽車白車身市場正在經歷適度的整合。主要參與者包括 Magna International Inc.、Norsk Hydro ASA、Gestamp Automation SA、Aisin Seiki 和 ThyssenKrupp AG。

這些公司擁有強大的全球和區域分銷網路,並正在策略性地擴大其在該市場的產品供應。這些公司正在積極尋求合作、簽約、達成協議以鞏固自己的地位。

例如,繼 2022 年 12 月與 Norsk Hydro ASA (Hydro) 建立技術合作夥伴關係後,Mercedes-Benz於 2023 年 5 月宣布了其低碳技術計畫的舉措成果。這種創新材料在梅廷根專業鑄造成專為白車身設計的先進結構部件。它用於各種車輛(包括 EQS、EQE、S 級、E 級、GLC 和 C 級)的避震塔等安全關鍵元件。此外,EQE 型號還採用低二氧化碳鋁製縱向構件。

2022 年 11 月,柯馬為新款阿爾法羅密歐 Tonale 推出了多功能白色車身 (BIW) 製造解決方案。這種增強的生產設置包含 20 條生產線,使製造商能夠靈活地以最多四種不同變體的隨機組合組裝中型 Tonale 模型,同時保持最佳吞吐量。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 日益成長的減重需求正在推動汽車車體市場的發展

- 市場抑制因素

- 製造白車身結構的材料成本急劇上升預計將限制市場成長

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 車型

- 小客車

- 商用車

- 推進類型

- 內燃機

- 電動車

- 材料類型

- 鋁

- 鋼

- 複合材料

- 其他材料

- 材料連接技術

- 焊接

- 咬合

- 雷射硬焊

- 加盟

- 其他材料連接技術

- 地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 歐洲其他地區

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 南美洲

- 中東/非洲

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Magna International Inc.

- Norsk Hydro ASA

- Gestamp Automocion SA

- Aisin Seiki Co. Limited

- Thyssenkrupp AG

- ABB Corporation

- TECOSIM Group

- Tata Steel Limited

- Dura Automotive Systems

- Tower International

- CIE Automotive

- Benteler International

- Kuka AG

第7章 市場機會及未來趨勢

The automotive body-in-white market size is estimated at USD 99.12 billion. It is expected to reach USD 116.70 billion over the period of five years, registering a CAGR of 3.32% during the forecast period.

Key Highlights

- Over the long term, stringent environmental regulations and emission norms, along with the rising adoption of lightweight materials in vehicles to achieve fuel efficiency, are expected to propel the market demand during the forecast period.

- The development of solid-state laser sources in the past decade has offered new welding solutions for BIW assembly. In particular, improved electrical efficiency (cost reductions) and the capability to combine optic fibers and long working distances (tool flexibility) offer new possibilities.

- For instance, in April 2023, Comau revealed that it had provided a highly intelligent welding solution for Hycan Automotive Technology Co., Ltd.'s frame line. It guarantees multi-model production of new energy cars, high JPH (Jobs per Hour), and a tangible decrease in production losses. It is used at the Hycan Hangzhou production facility. It can transition between four distinct platforms at random, is completely compatible with existing production platforms, and is mass-producing pure electric A06 automobile and SUV Z03 at 60 JPH cycle efficiency. The solution is built on a modified version of Comau's Opengate frame technology, which allows for flexible high-precision body-in-white construction and virtual commissioning.

- Moreover, ongoing R&D on new alloys and efficient manufacturing techniques and increasing investments in automation and robots in the production process are likely to offer new opportunities for players in the market. Apart from this, the body in white is an integral structure for all automobiles. Hence, the development of the automobile sector will also add to the growth of the global body-in-white market.

- For instance, in June 2023, NDR Auto Component Limited emphasized the importance of metal components and cosmetic components (trim cover) in the seat. The company's R&D team is now working on numerous product portfolios in these areas. Its metal components team is working on the creation of passenger vehicle seat frames, passenger car body-in-white (B-I-W) parts, and two-wheeler components.

- The Asia-Pacific region is anticipated to have significant growth, followed by Europe and North America during the forecast period. Asia-Pacific is expected to witness optimistic growth due to the government initiatives adopted in countries like India and China, promoting manufacturing and contributing to the growth of this market.

Automotive Body-in-White Market Trends

Growing Demand for Light-weight Vehicles to Drive the Automotive Body-in-White Market

- The body-in-white market is seeing advancements in lightweight material developments such as aluminum, magnesium alloy, and fiber-reinforced plastics (FRP), which are enabling the production of the body in white for lighter vehicles. The other influencing factors for lightweight materials technology are customer-driven requirements like styling, aesthetic appearance, reduced NVH (noise, vibration, harshness) aspects, and comfort.

- The primary driving force behind the rising demand for fuel-efficient vehicles is the implementation of stringent emission and safety regulations. Accordingly, to comply with stricter emissions and fuel economy standards, while some automobile manufacturers are focusing on reducing the overall weight of the car and enhancing fuel efficiency, others are entering into collaborations, partnerships, etc., to stabilize their position in the market.

- For instance, in September 2022, Atlis Motor Vehicles, which is developing an electric work vehicle as well as the batteries and motors that will power it, struck a cooperation partnership with ArcelorMittal, the world's top producer of automotive steels. ArcelorMittal's S-in motion pickup truck model, as well as cab and box designs, will be used by Atlis to assist in driving the design of the XT, a purpose-built, totally electric pickup truck meant to serve people and fleet owners working in agriculture and construction. ArcelorMittal created S-in-Motion, a series of lightweight steel solutions for manufacturers looking to construct lighter, safer, and more ecologically friendly automobiles. Atlis will use ArcelorMittal's body in white CAD engineering information to cut weight and cost while improving the range of its XT.

- In March 2023, Lamborghini unveiled key details about the LB744, marking the company's inaugural high-performance electrified vehicle (HPEV) supercar. This extraordinary automobile represents a pioneering achievement as the world's first high-performance electrified vehicle (HPEV). It features a plug-in hybrid configuration, with a lightweight, high-power lithium-ion battery ingeniously positioned within the transmission tunnel at the center of the chassis. This innovative approach is designed to not only reduce emissions but also enhance performance when compared to its predecessor, the V12. The groundbreaking L545 engine boasts a 6.5-liter capacity, making it Lamborghini's lightest and most potent 12-cylinder engine to date. In total, it weighs a mere 218 kilograms, which is 17 kilograms lighter than the Aventador unit.

- In August 2023, Porsche introduced a special edition 911 designed for maximum driving enjoyment on its 60th anniversary. Produced in a limited run of 1,963 cars, the Porsche 911 S/T offers a lightweight design and a pure, undiluted driving experience. For the first time, the 911 GT3 RS's 518 hp, high-revving engine is delivered to the road via a manual transmission and lightweight clutch.

- Further, the car sector in the United States will sell around 13.75 million light vehicle units in 2022. This statistic comprises around 2.9 million passenger automobiles and a little under 10.9 million light trucks sold at retail.

- Therefore, with manufacturers focusing on adopting innovative technologies and manufacturing processes to stand unique from their competitors, the automotive body-in-white market is expected to accumulate notable growth during the forecast period.

Asia-Pacific Region Likely to Exhibit Fastest Growth During the Forecast Period

- The Asia-Pacific region is expected to contribute significantly over the forecast period. Growing automotive production and increasing government focus on designing policies and initiatives encouraging electric vehicles are likely to boost the body-in-white market during the forecast period. The rising prominence of major countries like India and China is anticipated to supplement the development of the market in the Asia-Pacific region.

- For instance, in the first half of 2023, retail sales of electric vehicles in India surpassed 700,000 units. According to Vahan statistics, overall sales as of June 2023 were 721,971 units, which is already 73% of India EV Inc.'s record sales in the Year 2022. The government is investing in the development of infrastructure and incentivizing first electric vehicle buyers with subsidies to encourage people to shift from conventional fuel vehicles to green fuel vehicles.

- With several key players investing heavily and entering joint ventures with other players to cater to the growing demand, the market is likely to remain highly competitive during the forecast period.

- For instance, in July 2022, Thyssenkrupp AG announced an expansion of its automobile body business in China. It spent EUR 8 million (USD 9.4 million) in Kunshan, Jiangsu Province, to establish thyssenkrupp Automotive Equipment (Suzhou) Co., Ltd. This facility is scheduled to begin operations in December 2022. It will be a body-in-white factory that will manufacture dies and equipment for Chinese automakers.

- With the aforementioned trends and developments, it is expected that the market in the Asia-Pacific region will grow at a healthy rate during the forecast period.

Automotive Body-in-White Industry Overview

The automotive body-in-white market exhibits a moderate level of consolidation, owing to the presence of both regional and global industry giants. Key players include Magna International Inc., Norsk Hydro ASA, Gestamp Automocion SA, Aisin Seiki, and Thyssenkrupp AG.

These firms boast robust global and regional distribution networks and are strategically engaged in expanding their product offerings within this market. They actively seek collaborations, enter contracts, and forge agreements to fortify their positions.

For instance, in May 2023, Mercedes-Benz, following its technical collaboration with Norsk Hydro ASA (Hydro) in December 2022, unveiled the initial outcomes of its low-carbon technology initiative. This innovative material is expertly cast into advanced structural components designed for body-in-white applications at Mettingen. It finds application in safety-critical elements, such as shock towers, for a range of vehicles, including EQS, EQE, S-Class, E-Class, GLC, and C-Class models. Moreover, the EQE model will feature low-CO2 aluminum longitudinal members.

In November 2022, Comau introduced a versatile Body-In-White (BIW) manufacturing solution for the all-new Alfa Romeo Tonale. This enhanced production setup incorporates 20 lines, enabling the manufacturer to flexibly assemble its mid-size Tonale model in a randomized combination of up to four distinct variants while maintaining optimal throughput.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand for Lightweight Vehicles to Drive the Automotive Body-in-White Market

- 4.2 Market Restraints

- 4.2.1 High Cost of Materials to Manufacture BIW Structures is Expected to Limit Market Growth.

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Value in USD)

- 5.1 Vehicle Type

- 5.1.1 Passenger Vehicles

- 5.1.2 Commercial Vehicles

- 5.2 Propulsion Type

- 5.2.1 IC Engines

- 5.2.2 Electric Vehicles

- 5.3 Material Type

- 5.3.1 Aluminum

- 5.3.2 Steel

- 5.3.3 Composites

- 5.3.4 Other Material Types

- 5.4 Material Joining Technique

- 5.4.1 Welding

- 5.4.2 Clinching

- 5.4.3 Laser Brazing

- 5.4.4 Bonding

- 5.4.5 Other Material Joining Techniques

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Rest of the World

- 5.5.4.1 South America

- 5.5.4.2 Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles *

- 6.2.1 Magna International Inc.

- 6.2.2 Norsk Hydro ASA

- 6.2.3 Gestamp Automocion SA

- 6.2.4 Aisin Seiki Co. Limited

- 6.2.5 Thyssenkrupp AG

- 6.2.6 ABB Corporation

- 6.2.7 TECOSIM Group

- 6.2.8 Tata Steel Limited

- 6.2.9 Dura Automotive Systems

- 6.2.10 Tower International

- 6.2.11 CIE Automotive

- 6.2.12 Benteler International

- 6.2.13 Kuka AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年汽車白車身市場(按材料類型、車輛類型、推進類型、材料連接技術和地區分類)

2024-2032 年汽車白車身市場(按材料類型、車輛類型、推進類型、材料連接技術和地區分類) 2024 年車身本體全球市場報告

2024 年車身本體全球市場報告 2024-2028年全球車身套件市場

2024-2028年全球車身套件市場 2024年全球汽車車身市場報告

2024年全球汽車車身市場報告 汽車車體套件:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

汽車車體套件:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 汽車車體電子市場:依解決方案、車身特性、應用分類 - 2024-2030 年全球預測

汽車車體電子市場:依解決方案、車身特性、應用分類 - 2024-2030 年全球預測 白車身(BIW)市場:全球與區域分析(2023-2033)

白車身(BIW)市場:全球與區域分析(2023-2033) 2024 年汽車車身、沖壓金屬和其他零件全球市場報告

2024 年汽車車身、沖壓金屬和其他零件全球市場報告 汽車車身的全球市場報告 2023年

汽車車身的全球市場報告 2023年 白車身市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按車輛類型、推進類型、材料類型、材料連接技術、按地區、按競爭細分

白車身市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按車輛類型、推進類型、材料類型、材料連接技術、按地區、按競爭細分