|

市場調查報告書

商品編碼

1403937

FPSO:市場佔有率分析、產業趨勢與統計、2024年至2029年成長預測FPSO - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

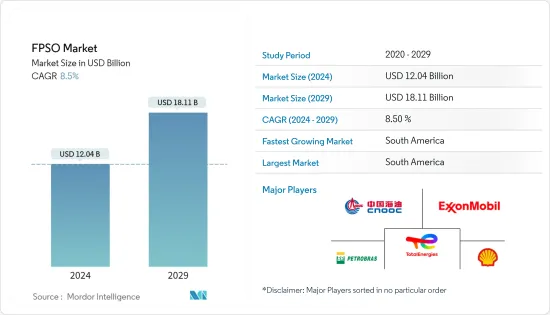

FPSO市場規模預計到2024年為120.4億美元,預計到2029年將達到181.1億美元,在預測期內(2024-2029年)複合年成長率為8.5%。

預計到年終FPSO市場規模將達111億美元,預計未來五年將達到166.9億美元,預測期內複合年成長率超過8.5%。

主要亮點

- 從中期來看,預計在預測期內,深水和超深水探勘和生產活動的增加將推動 FPSO 市場的發展。

- 另一方面,高昂的初期成本預計將阻礙預測期內的市場成長。

- 然而,FPSO系統的技術進步和創新預計將為FPSO市場帶來重大機會。

- 由於該地區海上活動的增加,南美洲預計將成為 FPSO 市場的主導地區。

FPSO市場趨勢

承包商擁有的 FPSO 預計將主導市場

- FPSO採購方式主要有三種:新建、現有船舶改造、現有裝置搬遷。在這些選項中,重新部署帶來了一些挑戰,因為 FPSO 是針對特定領域進行高度客製化的。因此,營運商在很大程度上青睞新建和改造方法,並且在過去二十年中往往依賴具有專業知識的第三方承包來提供這些服務。

- 承包商擁有的 FPSO 比營運商擁有的 FPSO 和固定平台具有成本優勢。專門從事 FPSO 設計、建造和營運的承包可以實現規模經濟並最佳化船隊運轉率,從而降低營運商的成本。這使得承包擁有的 FPSO 對於尋求經濟高效解決方案的營運商來說成為一個有吸引力的選擇。

- 承包商擁有的 FPSO 通常是可租賃的,為營運商提供了油田開發的彈性。租賃允許營運商以最少的領先資本投資獲得和部署FPSO,有利於規模較小的營運商和生產情況不確定的計劃。

- 隨著海上活動的增加,探勘和生產活動的成本以及將FPSO相關業務外包給承包的成本不斷增加。這使得營運商能夠將 FPSO 營運委託給專業承包商,並將資源和注意力集中到可以創造最大價值的領域。

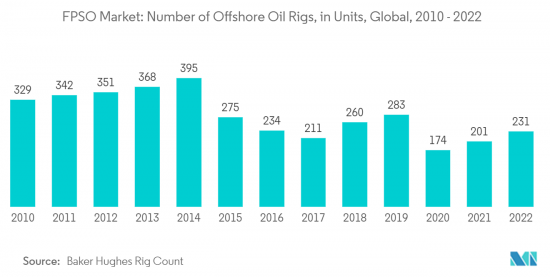

- 例如,根據貝克休斯鑽井平台統計, 年終海上鑽井平台數量約231座,與前一年同期比較增加約14.9%,海上探勘和生產活動增加,FPSO需求增加。

- 2023年5月,日本FPSO供應商MODEC訂單Equinor的一份FPSO訂單,為巴西海岸坎波斯盆地的BM-C-33區塊提供FPSO。除了交付預計於2027年完工的FPSO外,MODEC還將在其原油生產的第一年為Equinor提供FPSO的營運和維護服務。 Equinor 隨後將接手 FPSO 的營運責任。

- 因此,鑑於上述情況,承包商擁有的 FPSO 預計將在預測期內主導市場。

南美洲預計主導市場

- 預計南美洲地區對全球FPSO市場影響最大。特別是近年來,FPSO 的需求大幅成長,巴西和圭亞那成為該市場的主要企業。

- 南美洲擁有大量石油和天然氣蘊藏量,特別是巴西和圭亞那。這些蘊藏量位於深海或超深海,需要FPSO進行高效率生產、儲存和裝運。這些地區大規模發現和生產的潛力正在推動對 FPSO 的需求。

- 例如,2022年11月,Diamond Offshore贏得了巴西國家石油公司Ocean College超深水半潛式鑽井平台的鑽井專案合約。合約為期四年,並可選擇再延長四年。合約期限為四年,合約總價值預計約為4.29億美元,其中包括外包費用和服務費用。

- 此外,南美洲鹽下蘊藏量豐富,特別是巴西的桑托斯盆地和坎波斯盆地。這些蘊藏量位於厚厚的鹽層之下,為探勘和生產帶來了技術挑戰。 FPSO 非常適合這些惡劣環境,因為它們可以在深水中安全運作並滿足鹽下油田複雜的加工要求。

- 因此,鑑於上述幾點,南美地區預計將在預測期內主導FPSO市場。

FPSO產業概況

FPSO 市場是半靜態的。市場上的主要企業(排名不分先後)包括巴西石油公司(Petrobras)、中海油、TotalEnergies SE、埃克森美孚公司和殼牌公司。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 研究場所

第2章調查方法

第3章執行摘要

第4章市場概況

- 介紹

- 2028年之前的市場規模與需求預測(單位:美元)

- FPSO運作狀況(按地區/操作員)(2022年)

- 最新趨勢和發展

- 政府法規政策

- 市場動態

- 促進因素

- 海上石油和天然氣探勘和生產活動增加

- 能源需求增加

- 抑制因素

- 初期成本高

- 促進因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 所有權

- 企業擁有

- 供應商擁有

- 水深

- 淺水

- 深海

- 超深海

- 按地區分類的市場分析{2028 年之前的市場規模和需求預測(僅按地區)}:日本

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 挪威

- 英國

- 俄羅斯

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 澳洲

- 印尼

- 其他亞太地區

- 南美洲

- 巴西

- 阿根廷

- 委內瑞拉

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 阿爾及利亞

- 其他中東/非洲

- 北美洲

第6章競爭形勢

- 併購、合資、聯盟、協議

- 主要企業策略

- 公司簡介

- FPSO Contractors

- Modec Inc.

- SBM Offshore NV

- BW Offshore Limited

- Teekay Offshore Partners LP

- Bluewater Holding BV

- Saipem SpA

- Petrofac Limited

- FPSO Operators

- Petroleo Brasileiro SA(Petrobras)

- CNOOC Ltd

- TotalEnergies SE

- ExxonMobil Corp.

- Chevron Corporation

- Shell PLC

- BP PLC

- FPSO Contractors

第7章 市場機會及未來趨勢

- 技術進步與創新

The FPSO Market size is estimated at USD 12.04 billion in 2024, and is expected to reach USD 18.11 billion by 2029, growing at a CAGR of 8.5% during the forecast period (2024-2029).

The FPSO market is estimated to be at USD 11.10 billion by the end of this year and is projected to reach USD 16.69 billion in the next five years, registering a CAGR of over 8.5% during the forecast period.

Key Highlights

- Over the medium term, the increasing exploration and production activities in deep and ultradeep water depths are expected to drive the FPSO market during the forecasted period.

- On the other hand, the high upfront cost is expected to hinder the market's growth during the forecasted period.

- Nevertheless, the technological advancements and innovation in FPSO systems are expected to create huge opportunities for the FPSO market.

- South America is expected to be a dominant region for the FPSO market due to the increasing offshore activities in the region.

FPSO Market Trends

Contractor-owned FPSO Expected to Dominate the Market

- There are three primary methods for procuring FPSOs: new build, conversion of an existing vessel, and redeployment of an existing unit. Among these options, redeployment poses several challenges due to the highly customized nature of the FPSO for a specific field. As a result, operators have predominantly favored the new build and conversion approaches, often relying on third-party contractors with specialized expertise for these services over the past two decades.

- Contractor-owned FPSOs offer cost advantages over operator-owned FPSOs or fixed platforms. Contractors, who specialize in designing, constructing, and operating FPSOs, can achieve economies of scale and optimize their fleet utilization, resulting in reduced operator costs. This makes contractor-owned FPSOs an attractive option for operators seeking cost-effective solutions.

- Contractor-owned FPSOs are typically available for lease, providing operators greater flexibility in field development. Leasing allows operators to access and deploy FPSOs with minimal upfront capital investments, benefiting smaller operators or projects with uncertain production profiles.

- With the increasing offshore activities, the cost of exploration and production activities and outsourcing the FPSO-related activities to contractors. This allows operators to allocate their resources and attention to areas where they can create the most value, leaving the FPSO operations to specialized contractors.

- For instance, according to Baker Hughes Rig Count, at the end of 2022, there were around 231 offshore rigs, the offshore rigs witnessed about 14.9% campared to previous year, signifying an increase in offshore exploration and production activities, consequently driving the demand for FPSOs.

- In May 2023, MODEC, a Japanese FPSO supplier, secured a contract from Equinor to supply an FPSO vessel for the BM-C-33 block in the Campos Basin offshore Brazil. In addition to delivering the FPSO, expected to be completed by 2027, MODEC will provide Equinor with operations and maintenance services for the first year of the FPSO's oil production. Subsequently, Equinor plans to take over the operational responsibilities of the FPSO.

- Therefore as per the points mentioned above, the Contractor-owned FPSO is expected to dominate the market during the forecasted period.

South America Expected to Dominate Market

- The South American region is anticipated to exert the highest influence on the global FPSO market. Particularly, Brazil and Guyana have emerged as key players in this market, experiencing a significant surge in demand for FPSOs in recent years.

- South America has significant offshore oil and gas reserves, particularly in Brazil and Guyana. These reserves are located in deepwater and ultra-deepwater areas, requiring FPSOs for efficient production, storage, and offloading. The potential for large-scale discoveries and production in these regions drives the demand for FPSOs.

- For instance, in November 2022, Diamond Offshore secured a drilling program contract from Petrobras in Brazil for its ultra-deepwater semi-submersible rig, Ocean Courage. The contract spans four years, with an unpriced option to extend for another four years. The firm term of the contract is estimated to be valued at around USD 429 million, which includes a mobilization fee and provision of services.

- Moreover, South America has extensive pre-salt reserves, especially in Brazil's Santos and Campos Basins. These reserves are located beneath thick layers of salt, presenting technical challenges for exploration and production. FPSOs are well-suited for these challenging environments, as they can safely operate in deepwater and handle the complex processing requirements of pre-salt fields.

- Therefore, as per the above points, the South American region is expected to dominate the FPSO market during the forecasted period.

FPSO Industry Overview

The FPSO market is semi consolidated. Some of the major players in the market (in no particular order) include Petroleo Brasileiro SA (Petrobras), CNOOC Ltd, TotalEnergies SE, Exxon Mobil Corp., and Shell PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 FPSOs in Operation, by Region and Operator, 2022

- 4.4 Recent Trends and Developments

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.1.1 Increasing Offshore Oil and Gas Exploration and Production Activities

- 4.6.1.2 Growing Demand for Energy

- 4.6.2 Restraints

- 4.6.2.1 High Upfront Costs

- 4.6.1 Drivers

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ownership

- 5.1.1 Operator-owned

- 5.1.2 Contractor-owned

- 5.2 Water Depth

- 5.2.1 Shallow Water

- 5.2.2 Deep Water

- 5.2.3 Ultra-deep Water

- 5.3 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Norway

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Netherland

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Australia

- 5.3.3.4 Indonesia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Venezuela

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Nigeria

- 5.3.5.4 Algeria

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 FPSO Contractors

- 6.3.1.1 Modec Inc.

- 6.3.1.2 SBM Offshore NV

- 6.3.1.3 BW Offshore Limited

- 6.3.1.4 Teekay Offshore Partners LP

- 6.3.1.5 Bluewater Holding BV

- 6.3.1.6 Saipem SpA

- 6.3.1.7 Petrofac Limited

- 6.3.2 FPSO Operators

- 6.3.2.1 Petroleo Brasileiro SA (Petrobras)

- 6.3.2.2 CNOOC Ltd

- 6.3.2.3 TotalEnergies SE

- 6.3.2.4 ExxonMobil Corp.

- 6.3.2.5 Chevron Corporation

- 6.3.2.6 Shell PLC

- 6.3.2.7 BP PLC

- 6.3.1 FPSO Contractors

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements and Innovation