|

市場調查報告書

商品編碼

1274857

衛星通訊業者押注D2D、IoT、雲端以進行下一次大型發射:合作夥伴關係緩解了運營商的動盪,但在嚴峻的前景下,只有基本面強大的衛星經營者才能成功並聚集資本Satellite Players Bet on Direct-to-Device (D2D), IoT, and Cloud for Next Big Liftoff: Partnerships will Allay Disruption Fears among Telcos, yet only Fundamentally Strong Satellite Businesses will Thrive and Attract Capital amid Gloomy Outlook |

||||||

本報告提供對衛星通訊業者來說新的成長市場的3個市場相關調查,對傳統通訊市場的影響,通訊業者的衛星夥伴關係的商機,衛星通訊業者所面臨的主要課題考察。

視覺

範圍

對像企業

|

|

目錄

- 摘要

- 衛星通訊業者,著眼於多樣化,以阻止日益激烈的競爭、宏觀不確定性和利基焦點問題

- 在Direct-to-device(D2D),IoT,雲端基礎的服務中出現變革的機會

- 電信業者需要擔心嗎

- 克服監管障礙和確保持續的資本流動對於衛星運營商來說將是棘手的

- 附錄

This brief report explores three potential new growth markets for satellite operators who are looking to overcome intense competition, tough macro conditions, and the niche nature of their market. The report also discusses the impact on the traditional telecom market, revenue opportunity for telcos from satellite partnerships, and key challenges confronting satellite operators.

VISUALS

Satellite operators are being forced to expand their addressable markets in the near term, courtesy several factors: rising competition, with the emergence of players such as SpaceX along with several upstarts including AST SpaceMobile and Lynk; a tough funding climate resulting from a grim economic outlook and rising interest rates; and, market concentration risks arising from the current focus on satellite broadband internet. To address the situation, operators are raising stakes in new pursuits and developing new offerings. MTN Consulting expects three new potential addressable markets to provide transformational opportunities for satellite operators in the next 2-4 years. These include Direct-to-device (D2D), Internet of Things (IoT), and cloud-based services. Looking at these market opportunities, a thought may arise whether satellite operators are trying to disrupt the traditional telecom market. But the reality is that telcos will continue to be the primary service provider for wireless access. Telcos are also going to benefit from partnerships with satellite operators as they will aid in providing an enhanced experience for telco customers, reinforced by ubiquitous coverage. For satellite operators though, navigating the regulatory hurdles and ensuring constant capital flow are key concerns; several players from the current herd will vanish in the next 3-5 years.

COVERAGE:

Companies mentioned:

|

|

Table of Contents

- Summary

- Satellite operators eye diversification to deter rising competition, macro uncertainty, and niche focus concerns

- Transformational opportunities emerge in Direct-to-device (D2D), IoT, and cloud-based services

- Should telcos worry?

- Navigating regulatory hurdles and ensuring constant capital flow will prove tricky for satellite operators

- Appendix

List of Figures

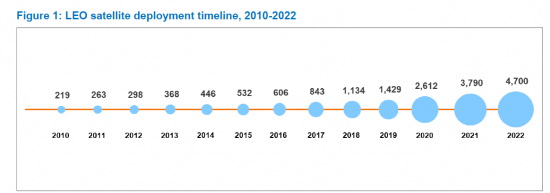

- Figure 1: LEO satellite deployment timeline, 2010-2022

- Figure 2: Illustration of OQ Technology's operating model

- Figure 3: D2D revenue opportunity for telcos (US$B)

- Figure 4: Private investments in the space economy, 2015-22 (US$B)

5G NTN 市場 - 按組件(硬體、軟體、服務)、按平台、按應用、按位置(城市、農村、偏遠、孤立)、按最終用途(海事、航太和國防、政府、採礦)和預測, 2024 - 2032

5G NTN 市場 - 按組件(硬體、軟體、服務)、按平台、按應用、按位置(城市、農村、偏遠、孤立)、按最終用途(海事、航太和國防、政府、採礦)和預測, 2024 - 2032 在軌衛星服務(第七版)

在軌衛星服務(第七版) 5G NTN 市場報告:2030 年趨勢、預測與競爭分析

5G NTN 市場報告:2030 年趨勢、預測與競爭分析 2024 年 5G NTN 全球市場報告

2024 年 5G NTN 全球市場報告 2024-2028年NTN 5G全球市場

2024-2028年NTN 5G全球市場 5G NTN 全球市場:按組件、按最終用途行業、按應用、按定位、按平台、按地區 - 預測至 2028 年

5G NTN 全球市場:按組件、按最終用途行業、按應用、按定位、按平台、按地區 - 預測至 2028 年 全球衛星服務市場(2023-2028):按類型(LEO、MEO、GEO)、通訊(語音、數據)、解決方案、應用、細分市場(消費者、商業、工業、政府)、產業

全球衛星服務市場(2023-2028):按類型(LEO、MEO、GEO)、通訊(語音、數據)、解決方案、應用、細分市場(消費者、商業、工業、政府)、產業 衛星營運商的財務 KPI:第 13 版

衛星營運商的財務 KPI:第 13 版 5G NTN 市場:按零件、用途、最終用戶分類,地點:2023-2032 年全球機會分析和產業預測

5G NTN 市場:按零件、用途、最終用戶分類,地點:2023-2032 年全球機會分析和產業預測 全球衛星服務市場:按類型、最終用途、地區—考慮到 COVID-19 影響的市場規模和趨勢以及到2028預測

全球衛星服務市場:按類型、最終用途、地區—考慮到 COVID-19 影響的市場規模和趨勢以及到2028預測