|

市場調查報告書

商品編碼

1445971

醫用包裝薄膜:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Medical Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

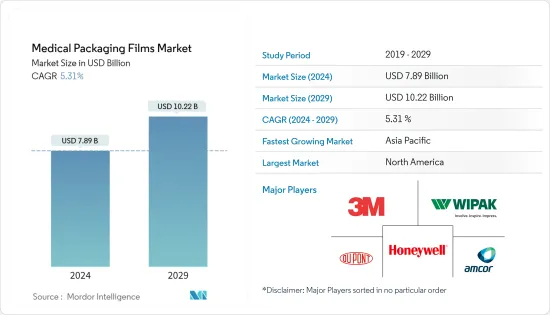

2024年醫用包裝薄膜市場規模預計為78.9億美元,預計到2029年將達到102.2億美元,在預測期內(2024-2029年)成長5.31%,年複合成長率為

市場規模反映了包裝薄膜產品在醫療包裝行業中跨應用的價值,並經過實質計算。包裝薄膜由聚乙烯、聚丙烯、雙向拉伸聚對聚對苯二甲酸乙二酯、聚亞苯醚、聚氯乙烯、EVOH、聚苯乙烯(PS)、尼龍等塑膠材料製成,並根據市場研究範圍考慮了各種金屬。

主要亮點

- 世界各國政府正在對醫療和藥品產品及解決方案進行大量投資,以控制損害並防止 COVID-19 大流行的潛在復發。例如,根據健康指標與評估研究所(IHME)2021年9月發布的數據,2019年全球人均醫療支出為1,129美元,預計2050年將增加至1,515美元。創新包裝和先發製人的措施預計將成為醫療產業的常態,從而推動對醫療包裝薄膜的需求。

- 研究的市場是包裝產業中快速成長的部分,在供應鏈安全問題、不斷變化的監管要求和供需失衡等挑戰中,許多因素加速了成長。在預測期內,由於各個市場參與者採取多項措施來限制塑膠材料的使用,生質塑膠薄膜的佔有率預計將增加。然而,由於所研究市場的需求性質,與塑膠薄膜的其他最終用戶產業相比,這些努力對以永續包裝薄膜取代塑膠薄膜的影響較小,這可能會維持市場成長。

- 由於治療癌症等慢性疾病的藥物的增加以及對治療藥物的小袋、袋子和小袋的需求不斷增加,預計該市場將顯著成長。此外,人口老化和糖尿病發病率預計將為市場擴張提供新的機會。

- 市場成長的主要挑戰包括原料價格波動、持續的永續性舉措(例如用生物分解性材料取代塑膠包裝產品)以及在塑膠包裝中增加使用消費後回收(PCR)塑膠,例如強制使用。通常,原料成本佔該行業銷售額的 55-60%。因此,盈利對原物料價格波動更加敏感。軟包裝薄膜的主要投入成本是粗衍生品,本質上是不穩定的。

- 在 COVID-19 大流行期間,包裝薄膜製造商面臨著大量持續近一到兩年的長期問題。封鎖的影響包括供應鏈中斷、勞動力短缺、難以獲得製造過程中使用的原料、導致最終產品產量激增並超出預算的價格波動以及運輸問題。

醫用包裝薄膜市場趨勢

對生質塑膠材料和可回收包裝材料的需求不斷成長推動醫療包裝薄膜市場

- 生質塑膠已在市場上使用,並正在研究以減少對環境的影響。由於塑膠在工業上的廣泛使用,廢棄物量急劇增加。因此,在醫療應用中使用生物分解性塑膠有助於環境保護。

- 醫用袋因其保護醫療產品、便於運輸、品牌宣傳等主要優點而廣泛應用於醫療應用,特別是在需要大量、低成本包裝時。這些袋子通常用於存放急救套件、藥品和醫療設備。小袋可用於存放工具和化學品。

- 此外,包裝薄膜製造商正致力於使用可回收材料創新醫療包裝解決方案,以提高其產品的永續性。例如,2021 年 11 月,永續包裝解決方案提供商 Coveris 推出了基於 Flexopeel T 和 Formpeel T 品牌單膜的用於醫療包裝的可回收單 PE 薄膜。該公司將杜邦的無塗層 Tyvek 1073B 與 Coveris 的 PE 樹脂基單體結構薄膜相結合。

- 隨著包裝產品製造商準備生質塑膠作為聚合物塑膠的替代品,包裝行業對生質塑膠材料不斷成長的需求正在推動市場研究。出於永續性考慮,生質塑膠的使用預計將減少禁令的影響,並減少醫療包裝中聚合物塑膠包裝的使用。根據歐洲生物塑膠公司統計,2021年全球軟包裝用生質塑膠產能為66.5萬噸。

- 研究市場中的主要企業正在推出新產品,以應對不斷變化的消費者偏好並保持與市場需求的相關性。例如,加拿大包裝和藥物分配器公司 Jones Healthcare Group 於 2021 年 12 月透過為藥局提供永續包裝產品擴大了 Qube 和 FlexRx 藥物依從性產品線。該公司推出了由生物材料製成的 Qube Pro、FlexRx One 和 FlexRx Reseal泡殼包裝。 PET 是一種經醫學核准的生質塑膠。

亞太地區預計將成為成長最快的市場

- 亞太地區的成長率是受訪市場中最高的,這主要是由於中國、印度、印尼和馬來西亞等新興經濟體的中產階級人口不斷成長、可支配收入以及對醫療保健和藥品的需求預期。該地區藥品生產的快速成長極大地推動了該地區阻隔膜市場的成長。

- 亞洲腎臟病率不斷上升,需要開發新的治療方法,包括改善治療的先進設備。由於糖尿病和高血壓的增加,亞洲腎臟病的盛行率正在增加。此外,人們越來越重視延長醫療設備和產品的保存期限以及消除細菌和病毒污染的可能性,這增加了醫療保健產業對包裝薄膜的需求。

- 醫用包裝薄膜解決方案可為包裝產品帶來降低成本、永續性和安全性等優勢,這就是為什麼我們看到中國和印度等人口眾多的新興國家的醫用包裝薄膜顯著成長。此外,由於強大的工業基礎、對永續包裝解決方案不斷成長的需求以及主要製造商在該地區的存在,預計亞太地區在金額和數量方面將領先所研究的市場。

- 對植入式設備的需求不斷成長以及醫療保健市場的快速成長也推動了對醫用包裝薄膜的需求。由於中國和印度等開發中國家對植入式設備的需求不斷成長以及公眾意識的不斷提高,該市場不斷擴大。

- 隨著醫療保健產業的擴張,中國醫療設備市場正以驚人的速度成長。這個特殊產業是中國成長最快的產業之一。由於動態監管,該行業正以兩位數的成長率成長,其中近 70% 由醫院採購貢獻。傳統上,中國醫療設備市場以其大量的低階耗材、機械治療設備和輔助設備而聞名。所需的高階耗材傳統上國內不生產,採購嚴重依賴進口。

- 目前,醫療器械正在轉向國產高價值、高風險的醫療設備,預計將推動中國醫療包裝薄膜市場的發展。此外,人口老化是中國高階設備需求增加的驅動力之一。根據世界衛生組織(WHO)預測,到2040年,中國60歲以上人口的比例預計將達到28%。預計不斷成長的人口將變得越來越富有,並且能夠比以前在醫療保健服務上花費更多。

醫用包裝薄膜產業概況

醫用包裝薄膜市場本質上是分散的,Honeywell、3M、Amcor等主要企業正在採取各種策略,如新產品發布、合資、合作、收購等來利用這個市場,我們已經擴大了我們的基礎的操作。

- 2022 年 4 月 - Amcor 作為開發和製造負責任包裝解決方案的全球領導者之一,宣佈在其藥品包裝產品組合中添加永續高屏蔽層壓板。新的低碳、可回收包裝選項在兩個方面提供支援:支援製藥公司的可回收目標,同時滿足產業所需的高阻隔阻隔性和性能要求。

- 2022 年 1 月——內容回收產品和高阻隔保護包裝領域的領先公司 Kloeckner Pentaplast 進行了大量投資,以進一步改進其永續產品,並擴大其在北美地區的廢舊內容回收(PCR)宣布計劃擴大PET產能。在消費者健康和藥品食品包裝市場提供創新。本公司具備生產能力,其產量20%以上為PCR材料。此次擴建將增加一條擠出生產線和兩台熱成型機,總合提供 15,000 噸新的 rPET 或 PET 產能。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭公司之間的敵意強度

- 產業價值鏈分析

- 評估 COVID-19 對市場的影響

第5章市場動態

- 市場促進因素

- 對生質塑膠和可回收包裝材料的需求不斷增加

- 醫療設施支出增加主要是因為慢性病的增加

- 市場限制因素

- 原物料價格波動

第6章市場區隔

- 材料類型

- 塑膠薄膜

- PE

- PP

- PVC

- PC

- 金屬膜

- 塑膠薄膜

- 目的

- 袋袋

- 管子

- 其他

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介

- Honeywell International Inc.

- 3M Company

- Wipak Oy

- Amcor Plc

- DuPont de Nemours, Inc.

- Renolit Medical

- PolyCine GmbH

- Glenroy, Inc.

- Toray Industries, Inc.

- Klockner Pentaplast Group

- Dunmore Corporation

- Covestro AG

第8章投資分析

第9章市場機會與未來趨勢

The Medical Packaging Films Market size is estimated at USD 7.89 billion in 2024, and is expected to reach USD 10.22 billion by 2029, growing at a CAGR of 5.31% during the forecast period (2024-2029).

The market size reflects the value of packaging film products across medical packaging industry applications and is computed in the real term. Packaging films are made from plastic materials, such as polyethylene, polypropylene, biaxially oriented polyethylene terephthalate, polyphenylene ether, polyvinyl chloride, EVOH, polystyrene (PS), nylon, and various metals are considered as per the scope of the market study.

Key Highlights

- Governments worldwide are heavily investing in medical and pharmaceutical products and solutions in damage control and the prevention of any potential resurgence of the COVID-19 pandemic. For instance, according to the Institute for Health Metrics and Evaluation (IHME), published in September 2021, the global per capita health expenditure was USD 1,129 in 2019, and it is projected to increase to USD 1,515 by 2050. Innovative packaging and preemptive measures are expected to become the norm in the medical industry, driving the demand for medical packaging films.

- The market studied is a burgeoning segment of the packaging sector, with many drivers accelerating the growth amid the challenges in the form of supply chain security woes, changing regulatory demands, and supply and demand imbalances. During the forecast period, bioplastic films are expected to increase their share on account of several initiatives taken by various market entities to curb the use of plastic materials. However, owing to the severe nature of the market studied, these initiatives are likely to have less impact on replacing plastic films with sustainable packaging films compared to other end-user industries of plastic films, thereby sustaining the market growth.

- The market is expected to experience significant growth, owing to the increase in therapeutics for chronic illnesses, such as cancer and the increasing demand for pouches, bags, and sachets for therapeutic medicines. Additionally, the aging population and the incidence of diabetes are projected to present new opportunities for market expansion.

- Some of the major challenges for the market growth are the volatility of raw material prices, the ongoing drive for sustainability, which includes replacing plastic-based packaging products with biodegradable materials, and mandates of using post-consumer recycled (PCR) plastics in plastic packaging. Usually, raw material costs are attributed to 55-60% of sales in this industry. Therefore, profitability is vulnerable to volatility in raw material prices. The key input cost for flexible packaging film is crude derivatives, which have been inherently volatile.

- During the COVID-19 pandemic, packaging film manufacturers were flooded with a pool of issues that lasted long for nearly one or two years. Some of the effects of lockdown included supply chain disruptions, labor shortages, lack of availability of raw materials used in the manufacturing process, fluctuating prices that caused the production of the final product to inflate and go beyond budget, transportation problems, etc.

Medical Packaging Films Market Trends

Increasing Demand for Bioplastic Material and Recyclable Packaging Material Drives the Medical Packaging Films Market

- Bioplastics are being used in the market studied to reduce environmental impact. The amount of waste increased dramatically due to the extensive use of plastics in the industry. Thus, using biodegradable plastic in medical applications contributes to environmental protection.

- Medical bags are widely used in medical applications, particularly when low-cost packaging in large quantities is required, owing to the primary benefits, such as medical product protection, ease of transportation, and brand promotion. These bags are frequently used to store first aid kits, medications, and medical equipment. Pouches can be used to store tools or liquid medications.

- Moreover, packaging film manufacturers are focusing on innovating medical packaging solutions with recyclable materials to achieve greater sustainability in their product offerings. For instance, in November 2021, Coveris, a sustainable packaging solution provider, launched recyclable mono-PE film based on mono films branded Flexopeel T and Formpeel T for medical packaging. The company combined an uncoated Tyvek 1073B from DuPont and a mono-structure film from Coveris, based on PE resins.

- The increasing demand for bioplastic material in the packaging segment has been driving the market study, as packaging product producers have alternatives for polymer-based plastic in the form of bioplastic. Using bioplastic reduced the impacts of bans and an anticipated reduction in polymer plastic-based packaging usage in medical packaging, owing to sustainability concerns. According to European Bioplastics, in 2021, the global production capacity of bioplastics for flexible packaging was 665,000 metric tons.

- Key players in the market studied are launching new products to cater to changing consumer preferences and stay relevant to market demand. For instance, the Canadian packaging and medication dispenser company Jones Healthcare Group expanded the Qube and FlexRx medication adherence product lines for pharmacies with sustainable packaging products in December 2021. The company launched Qube Pro, FlexRx One, and FlexRx Reseal blister packs made of Bio-PET, a bioplastic that received medical approval.

Asia Pacific is Expected to be the Fastest Growing Market

- The Asia Pacific is expected to expand with the highest growth rate in the market studied, majorly due to the increasing middle-class population, disposable incomes, and demand for medical and pharmaceutical products in developing economies such as China, India, Indonesia, and Malaysia. The booming pharmaceutical production in the region is significantly driving the growth of the barrier film market in the region.

- The increasing prevalence of kidney disease in Asia necessitated the development of new therapies, including sophisticated devices to improve treatment. The prevalence of kidney disease in Asia is increasing due to increasing rates of diabetes and hypertension. Furthermore, the emphasis on extending the shelf life of medical devices and products and eliminating the possibility of bacterial or viral contamination increased the demand for packaging film in the medical and healthcare industries.

- As medical packaging film solutions offer benefits, like cost savings, sustainability, and safety of packaged products, significant growth has been seen for medical packaging films from populated developing countries, such as China and India. Moreover, the Asia-Pacific region is anticipated to lead the market studied in terms of value and volume due to the solid industrial base, increased demand for sustainable packaging solutions, and the presence of key manufacturers in the region.

- The demand for medical packaging films is also fueled by the increasing demand for implantable devices and the booming healthcare market. The market expanded due to the escalating demand for implantable devices and increasing public awareness in developing nations like China and India.

- Along with the expanding healthcare sector, China's medical device market is increasing at an incredible pace. This specific sector is one of the fastest-increasing sectors in China. The sector is increasing at a double-digit growth rate, driven by dynamic regulations, nearly 70% of which was contributed to by hospital procurement. Traditionally China's medical devices market is well known for large volumes of low-end consumables, mechanotherapy devices, and aids. There has been large dependence on imports for procuring required high-end consumables as they were not traditionally manufactured in the country.

- Currently, there has been a shift toward domestically made high-value and high-risk medical devices, which are expected to drive the Chinese medical packaging film market. Moreover, the aging population is one of the driving factors for the increase in demand for high-end Chinese devices. According to the World Health Organization (WHO), the population aged more than 60 years is expected to reach 28% in China by 2040. This increasing demographic, which is increasingly affluent, is expected to be able to spend more on healthcare services than before.

Medical Packaging Films Industry Overview

The Medical Packaging Films Market is fragmented in nature, and the major players such as Honeywell, 3M, Amcor, etc. have used various strategies such as new product launches, joint ventures, partnerships, acquisitions, and others to increase their footprints in this market.

- April 2022 - Amcor, one of the global leaders in developing and producing responsible packaging solutions, announced the addition of sustainable high shield laminates to its pharmaceutical packaging portfolio. The new low carbon, recycle-ready packaging options deliver on two fronts, providing the high barrier and performance requirements needed for the industry while supporting pharmaceutical companies' recyclable objectives.

- January 2022 - Klockner Pentaplast, a leading company in recycled content products and high-barrier protective packaging, announced its plans to expand its post-consumer recycled content (PCR) PET capacity in the North America region with a significant investment to further increase its sustainable innovation offering in consumer health and pharmaceutical food packaging markets. The company has the capacity, with more than 20% of its volumes made from PCR material. The expansion is set to add an extrusion line and two thermoformers, providing a total of 15,000 metric tons of new rPET or PET capacity.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat Of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Demand for Bioplastic and Recyclable Packaging Material

- 5.1.2 Increased Spending on Healthcare Facilities, Primarily Owing to Increase in Chronic Diseases

- 5.2 Market Restraints

- 5.2.1 Fluctuation in the Prices of Raw Materials

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Plastic Film

- 6.1.1.1 PE

- 6.1.1.2 PP

- 6.1.1.3 PVC

- 6.1.1.4 PC

- 6.1.2 Metallic Film

- 6.1.1 Plastic Film

- 6.2 Application

- 6.2.1 Bags & Pouches

- 6.2.2 Tubes

- 6.2.3 Other Applications

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Honeywell International Inc.

- 7.1.2 3M Company

- 7.1.3 Wipak Oy

- 7.1.4 Amcor Plc

- 7.1.5 DuPont de Nemours, Inc.

- 7.1.6 Renolit Medical

- 7.1.7 PolyCine GmbH

- 7.1.8 Glenroy, Inc.

- 7.1.9 Toray Industries, Inc.

- 7.1.10 Klockner Pentaplast Group

- 7.1.11 Dunmore Corporation

- 7.1.12 Covestro AG

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

無菌醫療包裝:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

無菌醫療包裝:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 無菌醫療包裝市場:按類型、材料、滅菌方法、應用分類 - 全球預測 2024-2030

無菌醫療包裝市場:按類型、材料、滅菌方法、應用分類 - 全球預測 2024-2030 醫用包裝薄膜市場(產品類型:高阻隔薄膜、共擠薄膜和成型薄膜;材料類型:塑膠、鋁和氧化物)- 全球產業分析、規模、佔有率、成長、趨勢和預測,2023 年- 2031

醫用包裝薄膜市場(產品類型:高阻隔薄膜、共擠薄膜和成型薄膜;材料類型:塑膠、鋁和氧化物)- 全球產業分析、規模、佔有率、成長、趨勢和預測,2023 年- 2031 無菌醫療包裝的全球市場(~2028):按材料(塑膠、金屬、紙和紙板、玻璃)、類型(熱成型托盤、無菌瓶和容器、預填充吸入器)、滅菌方法、應用和地區

無菌醫療包裝的全球市場(~2028):按材料(塑膠、金屬、紙和紙板、玻璃)、類型(熱成型托盤、無菌瓶和容器、預填充吸入器)、滅菌方法、應用和地區 醫用管材包裝市場(製程類型:擠壓管、熱成型管、熱縮管、增強管、雷射加工管)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測

醫用管材包裝市場(製程類型:擠壓管、熱成型管、熱縮管、增強管、雷射加工管)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測 無菌醫療包裝市場(材料類型:塑膠、紙張、箔片、非織物、泡棉板;應用:醫療一次性用品、醫療設備)-全球產業分析、規模、佔有率、成長、趨勢和預測,2023-2031

無菌醫療包裝市場(材料類型:塑膠、紙張、箔片、非織物、泡棉板;應用:醫療一次性用品、醫療設備)-全球產業分析、規模、佔有率、成長、趨勢和預測,2023-2031 醫用包裝薄膜的全球市場(~2028):依材料(聚乙烯、聚丙烯、聚氯乙烯、聚醯胺)、類型(熱成型薄膜、高阻隔薄膜、氣相沉積沉澱)、應用(袋、管)和地區

醫用包裝薄膜的全球市場(~2028):依材料(聚乙烯、聚丙烯、聚氯乙烯、聚醯胺)、類型(熱成型薄膜、高阻隔薄膜、氣相沉積沉澱)、應用(袋、管)和地區 無菌醫療包裝市場:依材料、依產品、依應用、依地區

無菌醫療包裝市場:依材料、依產品、依應用、依地區 無菌醫療包裝的全球市場

無菌醫療包裝的全球市場 醫用包裝薄膜市場:按類型、材料和用途- 2023-2030 年全球預測

醫用包裝薄膜市場:按類型、材料和用途- 2023-2030 年全球預測