|

市場調查報告書

商品編碼

1403930

VaaS(視訊即服務):市場佔有率分析、產業趨勢與統計、2024 年至 2029 年成長預測VaaS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

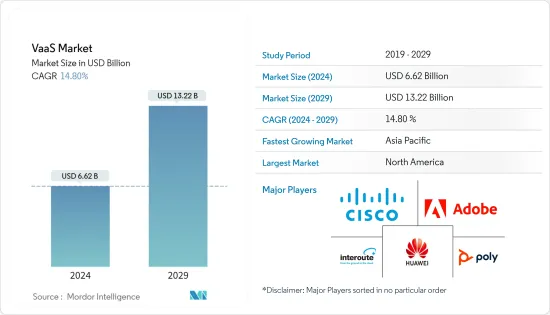

VaaS(視訊即服務)市場規模預計2024年為66.2億美元,預計2029年將達到132.2億美元,複合年成長率預計為14.80%。

視訊即服務(VaaS)是雲端基礎的視訊通訊服務,允許用戶透過網路進行視訊會議、視訊通話和即時視訊串流。 VaaS 供應商提供必要的基礎設施、軟體和工具,使企業和個人能夠透過視訊進行溝通。

主要亮點

- 雲端架構提供的可擴展性、彈性和經濟性正在推動需求從本地視訊會議 (VC) 和協作解決方案向雲端基礎的解決方案的重大轉變。雲端基礎的解決方案的普及正在加速對視訊即服務 (VaaS) 的需求。 VaaS 讓參與者在任何有網路連線的地方進行協作,從而節省時間和差旅成本。 VaaS 還提供會議轉錄服務,並可以協助產品演示、財務審查和其他類型的會議。

- VaaS 讓參與者輕鬆地即時共用和協作處理文件和簡報,從而提高生產力和效率。一些視訊會議解決方案供應商引入了各種商業模式,以更好地服務客戶。解決方案提供者專注於提供專門客製化的解決方案,以滿足多個企業的需求。雲端基礎的解決方案的使用也在增加,增加身臨其境型遠距臨場系統、語音和臉部辨識、高畫質音訊和視訊以及人工智慧 (AI) 等新功能的支出也在增加。技術進步、創新以及新的 VaaS 解決方案供應商的進入將進一步加劇市場參與企業之間的競爭,使中小型企業更容易獲得經濟實惠的雲端為基礎的混合雲的協作和風險投資解決方案。

- 此外,VaaS還可用於醫療保健領域的多種應用,包括遠端醫療服務、遠端醫療、視訊諮詢和醫學教育。視訊會議允許醫生和醫務人員與患者即時互動,無論他們身在何處。此外,醫務人員可以利用視訊會議接受遠端培訓並與其他專業人員即時協作,提高為患者提供的護理品質。

- 市場參與企業正在策略性地部署先進的 VaaS,以擴大其影響力並獲得市場佔有率。例如,國際視訊技術供應商 Pexip 於 2022 年 10 月推出了 Pexip 的視訊平台即服務。透過這項服務,該公司希望透過創造創新的新產品並將影片涵蓋其工作流程來幫助大公司進行創新。 (VPaaS) 已推出。 Pexip 的組織結構現在由分佈在美洲、歐洲、中東、非洲和亞太地區的擁有專業技術和商業資源的新業務部門組成,以支持公司對影片創新的關注。客戶和公民參與、醫療保健和視訊擴增實境是團隊重點關注的三個最大成長領域。

- 此外,國防部門還有一些視訊即服務應用程式。視訊監控就是其中之一,其中攝影機用於安全目的。此外,政府和國防部門還可以使用視訊會議進行溝通和協作。國防部門還可以使用雲端服務來儲存和存取關鍵任務資料。此外,軍事和國防通訊業可以利用創新的數位應用和服務。國防部門受到各種宏觀經濟趨勢的影響,包括政府支出、經濟成長和全球經濟狀況。各國增加軍事和國防費用可能會擴大研究目標市場,並為開發滿足多樣化需求的新產品創造機會。根據SIPRI的數據,2022年軍費開支為8,770億美元,美國位居軍事開支最高國家之首。這約佔同年世界軍費總額(總計2.2兆美元)的40%。中國以估計 2,920 億美元的軍事開支位居第二,俄羅斯緊隨其後,位居第三。

- 另一方面,高昂的採購和整合成本以及對資料安全和隱私的擔憂正在限制所研究市場的成長。由於設備故障或惡劣的天氣/環境條件,會發生一些誤報。資料安全和隱私問題預計將因服務整合不良和缺乏系統同步而受到阻礙。

視訊即服務市場趨勢

混合雲端領域可望推動市場需求

- 與其他雲端服務相比,混合雲近年來整體成長顯著。混合雲允許企業擴展其運算資源。它還減少了花費大量資金來滿足短期需求高峰的需要,這在您需要為敏感資料或應用程式釋放本地資源時非常有用。使用雲端服務的企業只需為暫時使用的資源付費,無需購買、編程和維護額外的資源和設備。這使您能夠減少不產生收益的成本。

- 當處理和運算需求波動時,混合雲允許公司將本地基礎設施擴展到公有雲並處理溢出,而無需將所有資料暴露給第三方資料中心。事實證明,這些創新有助於解決最終用戶因資料安全問題而不願遷移到此解決方案的痛點。上市公司利用公有雲的彈性和運算能力來執行基本的、非敏感的運算任務,同時將關鍵業務程序和資料保留在本地並在公司防火牆後面安全地受到保護。為了開發混合雲,服務供應商努力建構本地私有雲和共享網路共用的公有雲的組合。

- 此外,當用戶希望在一個平台上利用私有雲和公有雲解決方案及服務時,混合雲具有成本效益。此外,混合雲很容易遷移到多重雲端,並且不需要客戶投資額外的硬體元件。與私有雲或公有雲不同,混合雲將所有控制權留給組織,並且不由第三方或提供者管理。因此,政府機構和銀行部門不必擔心敏感資產或工作負載的安全。

- 安全性已成為混合雲發展的關鍵問題,近年來該領域的投資大幅增加。提供混合雲解決方案的公司專注於安全性。解決方案提供者提供整合安全服務,透過提供多層安全和監控來滿足消費者的需求。例如,麥克菲、惠普和思科正在致力於開發先進的安全系統來保護混合雲端上儲存的資料。隨著市場的不斷成長和企業擴展其混合雲功能,安全性越來越受到關注。用戶正在依賴第三方混合雲端安全解決方案提供者來進一步提高其能力。

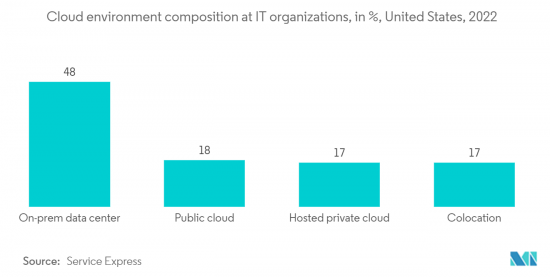

- 根據 Service Express 報道,2022 年美國的一項民調發現,本地資料中心平均佔受調查組織IT基礎設施環境的 48%。公共雲端佔18%,主機代管和託管私有雲端均佔17%。雲端的大量使用可能會促使市場參與企業在雲端部署其解決方案。

預計北美將佔據最大的市場佔有率

- 美國是全球最大經濟體,也是北美地區VaaS(視訊即服務)的重要市場。彈性、舒適性、內容個人化、多樣化內容的可得性和內容量是推動影片即服務採用的主要驅動力。隨著智慧型手機通訊速度的大幅提高,該國正迅速從 4G 轉向 5G。

- 隨著 5G 速度的提高,對高解析度影片的需求預計也會增加。 5G 預計將實現更快、更可靠的影片串流,以及高畫質影片和 XR 服務等新影片服務。此外,5G 的引入預計將影響企業視訊監控和視訊串流產業,從而導致連網型生態系統快速成長。 5G將對VaaS(視訊即服務)市場產生重大影響,為消費者帶來新的服務和改善的體驗。

- 此外,由於許多公司突然轉向在家工作文化,Zoom、Microsoft Teams 和 Google Workspace 的視訊軟體和服務需求激增。積極使用這些網站的人數顯著增加。根據報道,2022 年 1 月 Microsoft Teams 的月有效用戶為 2.7 億,比 2021 年 7 月增加了 2,000 萬。

- 該地區的主要行業參與企業不斷增強其產品供應,以保持競爭並滿足最終用戶不斷變化的需求。這就是為什麼我們將 VaaS 與人工智慧、深度學習和機器學習等先進技術相結合。此外,視訊即服務 (VaaS) 市場的參與企業正在採用先進的基於人工智慧的 VaaS,以提供一種自足式的方式來即時監控和增強視訊內容服務。例如,美國通訊技術開發商 Zoom Video Communications, Inc. 最近在其 VaaS(視訊即服務)中添加了端到端解決方案,該解決方案已向全球免費和付費用戶提供.我們宣布增加加密功能。此外,將這些先進技術整合到 VaaS 中可以顯著提高準確性並減少誤報。預計這些因素將在未來幾年為該行業創造新的機會。

- 2023 年 3 月,Amazon Web Services (AWS) 宣布推出 Amazon Interactive Video Service (Amazon IVS),這是一種託管直播解決方案,使開發人員能夠創建互動式視訊體驗。開發人員目前正在使用 Amazon IVS 為各種行業創建應用程式,包括社交網路、電子商務和健身。自Amazon IVS推出以來,協作直播已成為重要趨勢。 Twitch 等公司正在推出 Guest Star 等工具,幫助主播吸引觀眾參與直播視訊節目,讓節目更加精彩、更具互動性。

VaaS(影片即服務)產業概述

隨著全球參與企業不斷創新其服務以為用戶提供具有成本效益的服務,VaaS(視訊即服務)市場變得支離破碎,導致市場競爭之間的激烈競爭。主要參與企業包括思科系統公司、華為技術有限公司、Adobe系統公司和寶利通。

- 2022年7月-浙江行動、精友科技、華為聯合推出全新呼叫解決方案New Calling。為了重新定義現有的呼叫服務,為個人用戶和企業客戶提供卓越的語音和視訊通話質量,該解決方案採用「1平台+3功能+N服務」的架構模型。 New Calling系統在核心語音網路上建構New Calling平台與統一媒體功能,實現超高畫質視訊通話、智慧型視訊通話、互動式視訊通話三大競爭通話功能。

- 2022年3月-全球行動網際網路通訊、企業和客戶技術解決方案的主要供應商中興通訊宣布推出優質視訊平台2.0(PVP2.0)大視訊解決方案Did。 「新生態」的PVP2.0解決方案可以提供以營運商為中心的ATV啟動器,讓營運商可以根據需要採用自己喜歡的業務展示方式。營運商可以快速有效地整合第三方功能和應用程式,例如 Google Assistant 和 Google Ads。透過對融合視訊平台的支持,營運商可以將服務擴展到更多新市場並創造商業合作機會。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

- 評估宏觀經濟趨勢對市場的影響

第5章市場動態

- 市場促進因素

- 增加對雲端基礎視訊服務的投資

- 賦能數位化勞動力

- 市場抑制因素

- 創建和檢驗影片內容的高成本

第6章市場區隔

- 按平台

- 應用程式管理

- 設備管理

- 網路管理

- 按設備

- 行動裝置

- 企業運算

- 按服務

- 管理

- 專業的

- 按部署模型

- 公共雲端

- 私有雲端

- 混合雲端

- 按最終用戶產業

- 政府/國防

- BFSI

- 醫療保健

- 資訊科技/通訊

- 媒體與娛樂

- 製造業

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第7章競爭形勢

- 公司簡介

- Cisco Systems, Inc.

- Huawei Technologies Co., Limited

- Adobe Systems

- Interoute Communications Limited

- Polycom, Inc.

- Avaya, Inc.

- Vidyo, Inc.

- BlueJeans Network

- Applied Global Technologies, LLC

- AVI-SPL, Inc.

第8章投資分析

第9章 市場機會及未來趨勢

The VaaS Market size is estimated at USD 6.62 billion in 2024, and is expected to reach USD 13.22 billion by 2029, growing at a CAGR of 14.80% during the forecast period (2024-2029).

Video as a Service (VaaS) is a cloud-based video communication service that allows users to conduct video conferences, video calls, and live video streaming over the Internet. VaaS providers offer the necessary infrastructure, software, and tools to enable businesses and individuals to communicate through video.

Key Highlights

- Due to the high scalability, flexibility, and affordability provided by the cloud architecture, there is a discernible movement in demand away from on-premises video conferencing (VC) and collaboration solutions to cloud-based solutions. The popularity of cloud-based solutions has accelerated the demand for video as a service (VaaS). It saves time and travel expenses, as participants can collaborate from anywhere with an Internet connection. It also provides meeting transcription services, which can assist with product presentations, financial reviews, and other types of meetings.

- VaaS enhances productivity and efficiency, as participants can easily share and collaborate on documents and presentations in real time. Several video conferencing solutions vendors have implemented various business models to better serve their clients. Solution providers are putting their efforts into providing solutions specifically tailored to satisfy the needs of multiple enterprises. The use of cloud-based solutions is also increasing, as are the expenditures made to add new capabilities like immersive telepresence, voice and face recognition, HD audio and video, and artificial intelligence (AI). There will likely be more competition among the market players due to advancements in technology, innovations, and the entry of new VaaS solution providers, which would facilitate small and medium businesses to utilize affordable hybrid cloud-based collaboration and VC solutions.

- Further, VaaS can have various uses in the healthcare sector, such as remote healthcare services, telemedicine, video consultations, medical education, etc. With video conferencing, physicians and medical staff can interact with patients in real time, regardless of their physical location, which can be beneficial for patients who may have difficulty traveling. Additionally, medical staff can receive remote training and collaborate with other professionals in real time using video conferencing, which can improve the quality of care provided to patients.

- The market players are strategically deploying advanced VaaS to expand their presence and capture the market share. For instance, in October 2022, Pexip, an international provider of video technology, launched Pexip's Video Platform as a Service. With the service, the company hopes to empower big businesses to create innovative new products, incorporate video into workflows, and innovate. (VPaaS). Pexip's organizational structure, which currently comprises a new business unit with dedicated technical and commercial resources throughout the Americas, EMEA, and APAC, supports the company's focus on video innovation. Customer and citizen engagement, healthcare, and video-enabled extended reality are claimed to be the three major growth areas that this team is focusing on.

- Additionally, there are several uses of video as a service in the defense sector. Video surveillance is one such use, where cameras are used for security purposes. Additionally, video conferencing can be used by the government and defense sector for communication and collaboration. The defense sector can also use cloud services to store and access mission-critical data. Furthermore, innovative digital applications and services can be leveraged by the military and defense communication industry. The defense sector is influenced by various macroeconomic trends such as government spending, economic growth, and global economic conditions. The increasing spending of the various countries on military and defense would create an opportunity for the studied market to grow and develop new products to cater to a diverse range of needs. According to SIPRI, With USD 877 billion allocated to the military in 2022, the United States leads the ranking of countries with the largest military spending. That equated to approximately 40% of overall global military spending that year, which totaled USD 2.2 trillion. With an estimated USD 292 billion spent, China was the second-highest military spender, with Russia coming in third.

- On the other side, high acquisition and integration costs and data security and privacy concerns restrain the growth of the studied market. Several false alarms are triggered as a result of malfunctioning equipment and unfavorable weather or environmental conditions. Data security and privacy issues are anticipated to be a roadblock due to the service's poor integration or lack of system synchronization.

Video-as-a-Service Market Trends

The Hybrid Cloud Segment is Anticipated to Drive the Market Demand

- The hybrid cloud has seen significant overall growth in recent years compared to other cloud services, as it provides several benefits to organizations with large data volumes. Companies can scale computing resources by using a hybrid cloud. It also reduces the need to invest large sums of money to handle short-term surges in demand, which is useful when the company has to free up local resources for sensitive data or applications. Companies that use cloud services must pay only for the resources they use momentarily rather than purchasing, programming, and maintaining extra resources and equipment that sit dormant for long periods. This assists businesses in reducing costs that do not generate revenue.

- When processing and computing demand fluctuates, hybrid cloud computing enables businesses to scale out their on-premises infrastructure to the public cloud to address any overflow without exposing all of their data to third-party data centers. These innovations have proved beneficial in addressing the worries of end-users who were previously unwilling to migrate to this solution due to concerns about data security. Organizations benefit from the public cloud's flexibility and computing capacity for basic and non-sensitive computing tasks while keeping business-critical programs and data on-premises and secure behind a company firewall. To develop a hybrid cloud, service providers strive to create a combination of on-premise private cloud and public cloud that share a network connection.

- Further, a hybrid cloud is cost-effective when the user wishes to use both private and public cloud solutions or services on a single platform. In addition, the hybrid cloud allows an easy transition to the multi-cloud and does not require the customers to invest in an additional hardware component. Unlike private and public clouds, in the hybrid cloud, all the control is given to the organization and is not managed by a third party or the provider. Therefore, government organizations and banking sectors need not worry about the security of sensitive assets or workloads.

- The investment in this space has also grown exponentially over the past few years, as security is becoming one of the significant challenges for the growth of the technology. Companies offering hybrid cloud solutions are focusing heavily on security. Solution providers are offering integrated security services to cater to the consumer's requirements by providing multilayer security and monitoring. For example, McAfee, HP, and Cisco are working towards the development of high-level security systems to protect the data stored on hybrid clouds. With the market size growing significantly and companies expanding their hybrid cloud capabilities, the focus on security is increasing. Users rely on third-party hybrid cloud security solution providers to improve their abilities further.

- According to Service Express, an average of 48% of surveyed organizations' IT infrastructure environments were on-premises data centers, according to a 2022 poll in the United States. The public cloud accounted for 18%, while colocation and hosted private cloud both accounted for 17%. Such massive usage of the cloud would push the market players to deploy their solutions to the cloud.

North America is Anticipated to Hold the Largest Market Share

- The United States is the largest economy in the world and has been a significant market for Video as a Service in the North America region. The flexibility, comfort, content personalization, availability of diverse content, and content volume have primarily driven the adoption of Video as a Service. With smartphone transmission speeds increasing dramatically, the country is witnessing an early transition from 4G to 5G.

- With increased rates of 5G, higher-resolution videos are expected to witness an uptick in demand. It is expected that 5G will enable faster and more reliable video streaming, as well as new video services such as HD video and XR services. Moreover, the introduction of 5G is anticipated to affect video surveillance for businesses and the video streaming industry, leading to rapid growth in the connected ecosystem. 5G would have a significant impact on the Video as a Service market, allowing for new and improved services and experiences for consumers.

- Further, Zoom, Microsoft Teams, and Google Workspace have all seen a spike in demand for video software and services as a result of the abrupt shift of many firms to a work-from-home culture. The number of individuals who are actively using these sites is significantly increasing. Microsoft Teams reported 270 million monthly active users in January 2022, an increase of 20 million from July 2021.

- Major industry players in the region are constantly enhancing their product offerings to maintain a competitive edge and suit the evolving needs of end customers. Therefore, they combine VaaS with advanced technologies like AI, deep learning, and machine learning. Additionally, VaaS market players embrace advanced AI-based VaaS to offer a self-contained way to monitor and enhance video content services in real time. For instance, the American company Zoom Video Communications, Inc., which develops communications technology, recently announced the addition of end-to-end encryption capabilities to its already-available video-as-a-service offerings for free and premium users worldwide. Additionally, integrating these sophisticated technologies into VaaS can lead to significant improvements in accuracy and a decrease in false alarms. These factors are anticipated to present new chances for the industry in the coming years.

- In March 2023, Amazon Interactive Video Service (Amazon IVS), a managed live streaming solution enabling developers to create interactive video experiences, was introduced by Amazon Web Services (AWS). Currently, developers create apps for various industries, such as social networking, e-commerce, and fitness, using Amazon IVS. Since the introduction of the Amazon IVS, collaborative live streaming has been a significant trend. Companies like Twitch have introduced tools like Guest Star that let streamers draw viewers into live video shows, resulting in more exciting and interactive programming.

Video-as-a-Service Industry Overview

The video as a service market is fragmented as the global players are innovating their services to provide cost-benefit offers to the users, which gives a high rivalry to the market competitors. Key players are Cisco Systems, Inc., Huawei Technologies Co., Adobe Systems, Polycom, Inc., etc. Recent developments in the market are -

- July 2022 - New Calling, a brand-new calling solution, was jointly launched by Zhejiang Mobile, Jingyou Technology, and Huawei. To redefine current call services and offer great audio and video call quality to individual users as well as business customers, this solution uses the "1 platform + 3 capabilities + N services" architectural model. The New Calling system allows three competitive calling capabilities-UHD video calling, intelligent video calling, and interactive video calling-by creating the New Calling Platform and Unified Media Function on top of the core voice network.

- March 2022 - ZTE Corporation, a significant global supplier of telecommunications, enterprise, and customer technology solutions for the mobile internet, announced the debut of its Premium Video Platform 2.0 (PVP2.0) big video solution. The PVP2.0 solution for "New Ecosystem" can offer an operator-centric ATV launcher, allowing operators to adopt their preferred service display styles as necessary. Operators can rapidly and efficiently incorporate third-party features and apps like Google Assistant and Google Ads. With the support of a converged video platform, it enables operators to expand their service into more new markets, creating opportunities for business partnerships.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of Macro Economic Trends on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Investment on Cloud-Based Video Services

- 5.1.2 Enabling Digital Workforce

- 5.2 Market Restraints

- 5.2.1 High Cost of Video Content Creation and Validity

6 MARKET SEGMENTATION

- 6.1 By Platform

- 6.1.1 Application Management

- 6.1.2 Device Management

- 6.1.3 Network Management

- 6.2 By Device

- 6.2.1 Mobility Devices

- 6.2.2 Enterprise Computing

- 6.3 By Service

- 6.3.1 Managed

- 6.3.2 Professional

- 6.4 By Deployment Model

- 6.4.1 Public Cloud

- 6.4.2 Private Cloud

- 6.4.3 Hybrid Cloud

- 6.5 By End-user Industry

- 6.5.1 Government and Defense

- 6.5.2 BFSI

- 6.5.3 Healthcare

- 6.5.4 IT & Telecom

- 6.5.5 Media & Entertainment

- 6.5.6 Manufacturing

- 6.5.7 Other End-user Industries

- 6.6 Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Latin America

- 6.6.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems, Inc.

- 7.1.2 Huawei Technologies Co., Limited

- 7.1.3 Adobe Systems

- 7.1.4 Interoute Communications Limited

- 7.1.5 Polycom, Inc.

- 7.1.6 Avaya, Inc.

- 7.1.7 Vidyo, Inc.

- 7.1.8 BlueJeans Network

- 7.1.9 Applied Global Technologies, LLC

- 7.1.10 AVI-SPL, Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年 VaaS(視訊即服務)全球市場報告

2024 年 VaaS(視訊即服務)全球市場報告 視訊即服務市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按部署模式和行業垂直

視訊即服務市場規模和預測、全球和地區佔有率、趨勢和成長機會分析報告範圍:按部署模式和行業垂直 2024-2028 年全球 VaaS(視訊即服務)市場

2024-2028 年全球 VaaS(視訊即服務)市場 影片即服務市場報告:至2030年的趨勢、預測與競爭分析

影片即服務市場報告:至2030年的趨勢、預測與競爭分析 視訊即服務市場:按元件、應用程式、雲端部署模式和產業分類 - 2023-2030 年全球預測

視訊即服務市場:按元件、應用程式、雲端部署模式和產業分類 - 2023-2030 年全球預測 物聯網中的視頻:趨勢、用例和連接技術

物聯網中的視頻:趨勢、用例和連接技術 Video-as-a-Service的全球市場

Video-as-a-Service的全球市場 VaaS (Video as a Service) 的全球市場 - 產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測

VaaS (Video as a Service) 的全球市場 - 產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測