|

市場調查報告書

商品編碼

1432982

射線照相檢查設備:市場佔有率分析、產業趨勢、成長預測(2024-2029)Radiography Test Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

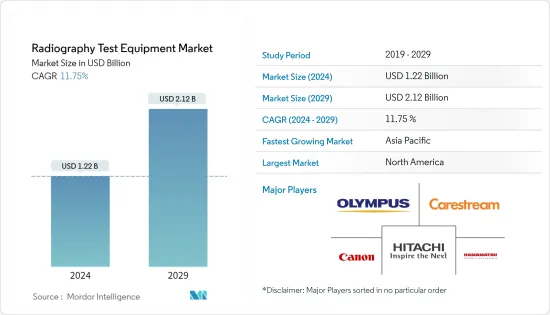

射線檢測設備市場規模預計到 2024 年為 12.2 億美元,預計到 2029 年將達到 21.2 億美元,在預測期內(2024-2029 年)複合年成長率為 11.75%。

冠狀病毒(COVID-19) 大流行正在影響全球生活的方面。這帶來了市場環境的一些變化,並對市場的製造業和汽車產業產生了重大影響。印度統計和規劃部 (MOSPI) 的數據顯示,COVID-19 對建築業、製造業和採礦業總付加價值的影響分別為 -13.3%、-6.3% 和 -14.7%。因此,這些行業成長放緩正在減少對影響市場成長的 X 光檢測設備製程活動的需求。

主要亮點

- 主要由於遵守高行業標準和安全法規,航太和汽車行業的需求不斷成長,正在推動射線照相檢查解決方案的採用。

- 從類比技術到數位技術的轉變為NDT應用的工業X光檢測市場注入了新的活力,將X光檢測系統的範圍擴展到傳統應用之外。

- 公司越來越注重降低與輻射相關的風險,並更喜歡攜帶性解決方案。例如,三星在Note 7醜聞後採用X光檢查來檢查電池。

- BP Macondo 災難、聖布魯諾管線爆炸和 BP德克薩斯城煉油廠爆炸等事件進一步強調了安全和環境永續性的必要性。

- 與超音波系統的激烈競爭、高輻射風險以及缺乏操作使用伽馬射線的 X光設備(特別是數位 X光設備)的熟練人員。相對較高的實施成本預計也會阻礙市場的成長。

射線照相檢測設備的市場趨勢

航太應用佔據大部分市場需求

- 射線檢測設備主要用於軍用和民航機的生產和維護,屬於航太領域。

- 航太應用包括檢測厚的、形狀複雜的金屬和非金屬的內部缺陷,以及關鍵航太零件、結構和組件的品質。

- 對安全標準的日益重視、更短的服務間隔、更低的排放目標、新材料和新製程的出現是推動航太X光透視市場的關鍵因素。

- 在航太領域,傳統射線照相擴大被數位射線照相所取代,除了一些關鍵的高解析度成像應用外,數位射線照相預計將完全主導市場。

- 根據國家航空航太和國防承包商認證計劃 (NADCAP) 制定的通用約束性認證標準的出現也促進了這一轉變。

北美佔據主要市場佔有率

- 該地區是市場主要企業的所在地,加上廣泛的研究和開發活動,促使無損檢測的廣泛採用。

- 由於美國是最早採用製造自動化的國家之一,在試點的一些領域使用自動化解決方案將使工人從艱苦、危險、重複和單調的任務中解放出來,並希望這有助於解決缺乏的問題。

- NTS 在北美設有 28 個實驗室,提供符合 FDA、產品安全和其他重要認證的自訂測試,幫助醫療器材與設備製造商更快地將產品推向市場。測試範圍從大型設備到植入人體的小型植入,都需要穩健的測試方法。例如,該公司提供聽力植入、標準射線照相和電腦斷層掃描 (CT) 的組件分析。

- 此外,石油和天然氣產業佔加拿大國內生產毛額的大部分資本投資和出口。有吸引力的省級激勵措施鼓勵鑽探、增加長水平井和頁岩資源多級壓裂的實施,是加拿大石油和天然氣行業的主要驅動力。

射線照相檢驗設備產業概況

主要企業包括 YXLON International、GEMeasurement and Control、Nikon Metrology、Teledyne DALSA、Hamamatsu Photonics、 Canon和 Hitachi。市場高度分散,主要參與者之間的競爭非常激烈,因為公司在研發方面投入巨資,以確保其設備的精確度無法估量。因此,市場集中度較低。

- 2020 年 3 月 - GTMA 有興趣在醫療領域業務,因為預計需要即時應對 COVID- 叢集大流行,以及全球對醫療設備和其他製造業的需求持續中長期成長。公司已經成立。

- 2020年12月-印度政府計劃建立三個大型電力和清潔能源設備製造區,以有吸引力的價格向土地和電力、新能源和可再生能源等公司提供獎勵。政府的此類舉措預計將鼓勵對設備的投資並增加對測試設備(包括 X 光透視設備)的需求。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- COVID-19 對市場的影響

- 市場促進因素

- 可攜式X光成像設備的出現

- 市場課題

- 由於使用伽馬射線和 X光,輻射風險較高

- 對高技能人才的需求

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 科技

- X光底片攝影

- 電腦放射線照相術

- 直接放射線照相

- CT檢查

- 最終用戶產業

- 航太/國防

- 能源/電力

- 建造

- 油和氣

- 車

- 製造業

- 其他最終用戶產業

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東/非洲

第6章 競爭形勢

- 主要供應商簡介

- Hitachi Ltd

- Canon Inc.

- Carestream Health Inc

- Hamamatsu Photonics KK

- Olympus Corporation

- Vidisco Ltd

- Nikon Metrology Inc.

- Teledyne Dalsa Inc.

- GE Measurement and Control

- YXLON International GmbH(COMET Group)

第7章供應商市場佔有率分析

第8章投資分析

第9章 市場機會及未來趨勢

The Radiography Test Equipment Market size is estimated at USD 1.22 billion in 2024, and is expected to reach USD 2.12 billion by 2029, growing at a CAGR of 11.75% during the forecast period (2024-2029).

The Coronavirus (COVID-19)pandemic has affected every aspect of life globally. This has brought along several changes in market conditions and affected the manufacturing and automotive sector for the market majorly. According to the Ministry of Statistic and Program Institute (MOSPI) India, the impact of COVID-19 on Gross value-added on the construction, manufacturing, and mining sector has accounted for -13.3%,-6.3%, and -14.7%, respectively. Thus, the decline in the growth of these industries has reduced the demand for the radiography test equipment process activities that impact the market growth.

Key Highlights

- Increase in demand from aerospace and automotive sectors, primarily due to conformance to high industry standards and safety regulations is boosting the adoption of radiography testing solutions.

- The shift from analog to digital technology has given the industrial radiography market a new lease of life for NDT applications, broadening the scope of X-ray inspection systems beyond traditional applications.

- Companies are increasingly focusing on reducing radiation-related risks, and preferring portability solutions, which has prompted companies to revamp their product portfolio. For instance, Samsung has adopted radiography to test their batteries after the much-publicized Note 7 fiasco.

- Incidents, like the BP Macondo disaster, the San Bruno pipeline explosion, and the BP Texas City refinery explosion, have further emphasized on the need for safety, environmental sustainability, therefore governmental agencies and regional bodies like ASME & ISO have taken stringent measures to assure safety and regulatory compliances.

- Intense competition from ultrasonic systems, high risk of radiation, lack of skilled personnel, to handle radiography equipment which uses gamma rays (especially in digital radiography). Also, relatively high deployment costs are expected to hinder the growth of the study market.

Radiography Test Equipment Market Trends

Application in Aerospace to Account for a Significant Portion of the Market Demand

- Radiography test equipment, mainly used in manufacturing and maintenance of military and civil aircraft, are considered under the scope of the aerospace segment.

- Applications in aerospace, include detection of internal defects in thick and complex shapes, in metallic and non-metallic shapes, quality of critical aerospace components, structures, and assemblies.

- Increasing emphasis on safety standards, decreasing service intervals, low emission targets, and the advent of new materials and process are the major factors driving the radiography market in the aerospace segment.

- Conventional radiography is being increasingly replaced with digital radiography in aerospace, and the latter is expected to completely overshadow the market, except for some critical high-resolution imaging applications.

- This shift has also been fuelled by the advent of common binding standard for the common accreditation, in accordance with the National Aerospace and Defense Contractors Accreditation Program (NADCAP).

North America to Account for Significant Market Share

- The region is home to some of the major players in the market, coupled with the extensive research and development activities that have resulted in the wide-scale adoption of non-destructive testing.

- As the United States is one of the early adopters of manufacturing automation, the use of automated solutions in some regions of testing is expected to address the issue of lack of skilled personnel, by releasing workers from hard and dangerous, repetitive, and monotonous work.

- NTS with 28 labs in North America, provides custom testing to meet FDA, product safety, and other essential certifications to bring products to market quickly to medical device and equipment manufacturers. The testing varies from bigger devices to smaller implants that are then implanted in the human body and thus need robust testing methods. For instance, the company provides component analysis, standard radiography, and computer tomography (CT) of hearing implants.

- Furthermore, the Canadian GDP is majorly dominated by the oil and gas sector to capital investments and exports. Attractive provincial incentives to encourage drilling and increased implementation of long horizontal wells and multistage fracturing in shale resources are the major drivers for the Canadian oil and gas industry.

Radiography Test Equipment Industry Overview

The major companies like YXLON International, GE Measurement and Control, Nikon Metrology Inc., Teledyne Dalsa Inc., Hamamatsu Photonics K.K., Canon Inc., Hitachi Ltd, among others. The market is fragmented due to the intense competition among the major players since they are investing significantly in the R&D for immeasurable accuracy in their equipment. Therefore, the market concentration will be low.

- March 2020 - The GTMA formed a cluster of member companies interested in working in the medical sector, anticipating the need for an immediate response to the COVID-19 pandemic and ongoing medium/long-term growth in the global requirement for medical devices and other manufacture.

- December 2020 - The Indian government planned to set up three large manufacturing zones for power and clean energy equipment by offering companies incentives such as land and electricity at attractive prices, power, and new and renewable energy. Such initiatives by the government are expected to boost the investment in equipment, leading to the growing demand for equipment testing, including radiography testing equipment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Impact of COVID-19 on the Market

- 4.3 Market Drivers

- 4.3.1 Advent of Portable Radiography Equipment

- 4.4 Market Challenges

- 4.4.1 High Risk of Radiation Since it Uses Gamma Rays and X-Rays

- 4.4.2 Requirement of Highly Skilled Personnel

- 4.5 Industry Value Chain Analysis

- 4.6 Porters Five Force Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Film Radiography

- 5.1.2 Computed Radiography

- 5.1.3 Direct Radiography

- 5.1.4 Computed Tomography

- 5.2 End-user Vertical

- 5.2.1 Aerospace and Defense

- 5.2.2 Energy and Power

- 5.2.3 Construction

- 5.2.4 Oil and Gas

- 5.2.5 Automotive

- 5.2.6 Manufacturing

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Vendor Profiles

- 6.1.1 Hitachi Ltd

- 6.1.2 Canon Inc.

- 6.1.3 Carestream Health Inc

- 6.1.4 Hamamatsu Photonics KK

- 6.1.5 Olympus Corporation

- 6.1.6 Vidisco Ltd

- 6.1.7 Nikon Metrology Inc.

- 6.1.8 Teledyne Dalsa Inc.

- 6.1.9 GE Measurement and Control

- 6.1.10 YXLON International GmbH (COMET Group)

7 VENDOR MARKET SHARE ANALYSIS

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

射線照相檢查設備市場:按技術、最終用戶產業分類 - 2024-2030 年全球預測

射線照相檢查設備市場:按技術、最終用戶產業分類 - 2024-2030 年全球預測 X 光檢測系統技術市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、成像技術、尺寸、產品類型、最終用戶、地區、競爭細分,2018-2028 年

X 光檢測系統技術市場 - 全球產業規模、佔有率、趨勢、機會和預測,按產品、成像技術、尺寸、產品類型、最終用戶、地區、競爭細分,2018-2028 年 X 光檢測系統的全球市場:按技術、尺寸、產業、地區 - 預測(至 2028 年)

X 光檢測系統的全球市場:按技術、尺寸、產業、地區 - 預測(至 2028 年) X 光檢測系統市場:按組件、影像技術、尺寸、行業 - 2023-2030 年全球預測

X 光檢測系統市場:按組件、影像技術、尺寸、行業 - 2023-2030 年全球預測 電子和半導體市場的 X光檢測系統,按組件、成像技術、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測

電子和半導體市場的 X光檢測系統,按組件、成像技術、按應用、國家和地區 - 2023-2030 年行業分析、市場規模、市場佔有率和預測 全球 X 射線檢測系統市場 - 2023-2030

全球 X 射線檢測系統市場 - 2023-2030 全球射線照相檢查裝置市場

全球射線照相檢查裝置市場 全球 X 射線檢測設備市場 - 預測 2023-2028

全球 X 射線檢測設備市場 - 預測 2023-2028 X光檢查裝置的全球市場

X光檢查裝置的全球市場 全球 X 射線檢測設備市場-行業趨勢和預測(至 2030 年)

全球 X 射線檢測設備市場-行業趨勢和預測(至 2030 年)