|

市場調查報告書

商品編碼

1441686

PET 包裝:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)PET Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

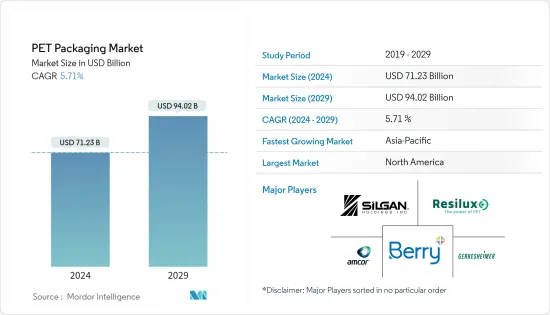

2024年PET包裝市場規模預計為712.3億美元,預計到2029年將達到940.2億美元,在預測期內(2024-2029年)複合年成長率為5.71%成長。

對環保包裝的需求不斷成長以及 PET 的優越性能預計將在預測期內推動市場成長。

主要亮點

- 包裝產業在環保技術方面不斷取得長足進步,以滿足客戶對更永續的社會的需求。客戶越來越認知到高性能包裝可以延長產品的保存期限。對環保的消費後包裝選擇的需求日益成長,尤其是 PET(聚對苯二甲酸乙二酯)包裝解決方案。

- 與玻璃相比,PET 的重量可減輕高達 90%,因此運輸起來更經濟實惠。近年來,PET塑膠瓶擴大被笨重且易碎的玻璃瓶所取代,為礦泉水等飲料提供可重複使用的包裝。

- PET 在公司和產品中使用的一些進展和趨勢表明人們對 PET 和市場成長的關注。 PET 有多種用途,由於其透明度和內置二氧化碳屏障,它可以輕鬆吹製成瓶子或成型為片材。可以使用著色劑、紫外線阻隔劑、氧氣阻隔劑/清除劑和其他添加劑來增強 PET 的性能,以製造出符合品牌要求的瓶子。

- 此外,PET 容器通常用於包裝網球、果汁、沙拉醬、食用油、花生醬、液體洗手劑和蘇打水等產品。 PET 主要用於製造在美國銷售的單份和兩公升瓶裝碳酸飲料和水。外帶已調理食品容器由優質 PET 製成,可在烤箱或微波爐中加熱。

- 大多數水和無酒精飲品容器均由高度可回收的聚對聚對苯二甲酸乙二酯(PET) 製成。然而,隨著全球瓶子使用量的增加,收集和回收瓶子以防止對海洋造成損害的嘗試已經落後。例如,一項研究一次性使用瓶子與可重複使用瓶子的有效性的研究發現,當寶特瓶的回收含量為 40% 至 60% 時,與原生材料製成的瓶子相比,排放量排放了32 %,甚至減少了約48%。碳酸飲料。

- COVID-19感染疾病一次性包裝供應商帶來了極大的緩解。許多國家已逐漸禁止這些包裝並推廣可重複使用的包裝,但疫情的爆發改變了消費者和政府的行為。由於COVID-19感染疾病,對能量飲料和保健食品的需求急劇增加。這些產品大多數採用 PET 等一次性塑膠包裝。

PET包裝市場趨勢

瓶子經歷顯著成長

- 聚對苯二甲酸乙二酯(PET)因其對水蒸氣、氣體、稀酸、油和醇的高阻隔性能而常用於食品包裝。此外,PET 易於回收、相當彈性且防碎。據地球日組織者稱,美國每分鐘購買一百萬個寶特瓶。美國人平均每年喝 167 個塑膠水瓶。該地區對包裝飲用水的需求不斷成長,促使 PET 塑膠頂部和機殼的市場不斷成長。

- PET衍生PE,與其他類型的塑膠相比具有優異的剛度。此外,它還保持堅固的保護結構並具有出色的防潮性。用於製造液體和飲料的寶特瓶。 PET 用於製造一次性塑膠容器,也用於包裝冷凍食品和即食食品。 PET 是首選,因為它提供健康的油屏障並有助於防止可能損害材料的化學物質。

- 電子商務領域的擴張也為全球市場的擴張做出了重大貢獻。許多品牌擴大採用寶特瓶和罐,因為從物流的角度來看,它們更容易攜帶。此外, 寶特瓶重量輕,不需要小心搬運,這大大降低了運輸成本。因此,在預測期內,人們對網路購物的傾向不斷成長,預計市場需求將得到支持。

- 由於世界各地對食品和飲料的需求不斷增加,用於製造瓶子和罐子的PET的需求預計將大幅增加。此外,醫療保健產業對寶特瓶乾洗手劑包裝的需求日益成長。此外,由於COVID-19的影響持續存在,並且一些國家的冠狀病毒感染疾病人數持續上升,預計對乾洗手劑瓶的需求將保持高位,這可能會刺激用於包裝乾洗手劑的寶特瓶的擴張。

- PET 在公司和產品中的應用方面的一些進展和趨勢表明人們對 PET 及其市場佔有率的關注日益增加。 PET 有多種用途,由於其透明度和內置二氧化碳屏障,它可以輕鬆吹製成瓶子或成型為片材。可以使用著色劑、紫外線阻隔劑、氧氣阻隔劑/清除劑和其他添加劑來增強 PET 的性能,以製造出符合品牌要求的瓶子。

亞太地區市場顯著成長

- 中國是全球最大的聚對苯二甲酸乙二酯(PET)市場之一。過去幾年,由於原料供應充足且製造成本低廉,中國PET等工程塑膠的產量不斷成長。中國對寶特瓶的需求持續成長。顯然,軟性飲料對於 PET 在中國的潛力有多重要。這很大程度上受到瓶裝水產業及其主要企業(如康師傅和農夫山泉)以及中國瓶裝水消費量逐年大幅增加的影響。

- 由於 PET 與目前使用的傳統包裝聚合物相比具有優勢,因此 PET 產品在包裝領域(PET 容器、瓶子等)的使用不斷增加。由於出口和國內消費的增加,中國食品飲料行業和消費品等行業對包裝材料的需求不斷增加。

- 印度生產多種塑膠,如聚丙烯(PP)、聚對苯二甲酸乙二酯(PET)和聚氯乙烯(PVC)。印度擁有龐大的PET產能,可滿足國內大部分市場需求。但國內市場PET消費量也存在地區差異。印度北部和西部地區擁有大量的最終用戶公司和龐大的分銷網路,佔據了 PET 使用量的大部分。

- 在印度,隨著攜帶式食品消費趨勢的增加,對用 PET 和金屬罐等材料包裝的小型一次性產品的需求正在迅速增加。由於消費者注重預算並追求金額,PET 等軟包裝材料在全國範圍內仍然廣泛使用。

- 然而,消費者開始傾向於具有環保品質的替代包裝材料。玻璃和鋁由於其環境友好性和高可回收性而在該地區具有很高的接受率。因此,越來越多的客戶開始不再使用塑膠。

PET包裝產業概況

PET 包裝市場競爭激烈,由 Amcor Ltd、Gerresheimer AG、Berry Global Group Inc.、Silgan Holdings Inc. 和 Resilux NV 等幾家大公司組成。目前,在市場佔有率方面佔據主導地位的大公司寥寥無幾。這些擁有最大市場佔有率的市場領導致力於擴大其國際消費群。這些公司利用戰術性合資企業來增加市場佔有率和盈利。

- 2022 年 1 月:Sonoco 銷售 CPET(結晶聚對苯二甲酸乙二酯)熱成型塑膠托盤,因為該公司面臨關鍵原料、運輸、包裝、勞動力和其他直接和間接成本空前的通貨膨脹,並計劃將碗的價格提高9%。

- 2022 年 1 月:Berry 和 TotalEnergies 宣佈建立合作夥伴關係,以減少送往垃圾垃圾掩埋場的廢棄物並提高食品包裝的循環性。 Berry 將獲得 Total Energy 認證的環狀聚合物,以增強消耗後塑膠廢棄物的回收利用,而使用目前的方法通常很難回收這些廢棄物。因此,貝瑞將能夠在食品、飲料和保健產品的包裝中使用更多的再生塑膠。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場概況

- 市場促進因素與限制因素介紹

- 市場促進因素

- PET的優異性能

- 對環保包裝的需求不斷成長

- 市場限制因素

- 部分地區塑膠使用法規

- 價值鏈分析

- 產業吸引力波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 依產品類型

- 瓶子和罐子

- 袋子和小袋

- 托盤

- 蓋子/蓋子和蓋子

- 其他產品類型

- 依包裝

- 死板的

- 靈活的

- 依最終用戶產業

- 食品和飲料

- 藥品

- 個人護理和化妝品行業

- 工業產品

- 家庭用品

- 其他最終用戶產業

- 依地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 北美洲

第6章 競爭形勢

- 公司簡介

- Amcor Ltd

- Resilux NV

- Gerresheimer AG

- Berry Global Group Inc.

- Silgan Holdings Inc.

- Graham Packaging Company

- GTX Hanex Plastic Sp. zoo

- Dunmore Corporation

- Comar LLC

- Sonoco Products Company

- Huhtamaki OYJ

- Nampak Limited

第7章 投資分析

第8章市場機會與未來趨勢

The PET Packaging Market size is estimated at USD 71.23 billion in 2024, and is expected to reach USD 94.02 billion by 2029, growing at a CAGR of 5.71% during the forecast period (2024-2029).

The increasing demand for environment-friendly packaging and the outstanding properties of PET are expected to drive market growth over the forecast period.

Key Highlights

- The packaging sector keeps making significant strides in environment-friendly technologies to satisfy customer demand for a more sustainable society. Customers increasingly know that high-performance packaging may lengthen a product's shelf life. It has increased the need for environment-friendly end-of-life packaging options, particularly PET (polyethylene terephthalate) packaging solutions.

- PET can result in weight reductions of up to 90% compared to glass, making shipping more affordable. As they provide reusable packaging for beverages like mineral water, PET plastic bottles have increasingly replaced bulky, brittle glass bottles in recent years.

- Several advancements and trends in how companies and products use PET indicate the attention on PET and the market's growth. PET has many uses and is easily blown into bottles or shaped into sheets thanks to its clarity and built-in CO2 barriers. PET characteristics can be enhanced with colorants, UV blockers, oxygen barriers/scavengers, and other additives to create bottles that meet a brand's requirements.

- Additionally, PET containers are often used for packaging goods, including tennis balls, juice, salad dressing, cooking oil, peanut butter, liquid hand soap, and soda. PET is primarily used to make single-serving and two-liter bottles of carbonated soft drinks and water distributed throughout the nation, including the United States. Containers for take-home prepared meals that may be warmed in the oven or microwave are made of exceptional grades of PET.

- Most water and soft drink containers are constructed of highly recyclable polyethylene terephthalate (PET). However, attempts to collect and recycle the bottles to prevent them from damaging the oceans are falling behind as their use increases globally. For instance, if a PET bottle had 40%-60% recycled content, its emissions would be decreased by 32%-48% compared to one made from virgin material, according to a study examining the effects of single-use and reusable bottles for carbonated soft drinks.

- The COVID-19 pandemic provided significant relief to single-use packaging vendors. Although many countries were slowly banning these packaging and promoting reusable packaging, the outbreak changed consumer and government behavior. Due to the COVID-19 pandemic, the demand for nutritional drinks and healthy food increased exponentially. Most of these products are packaged with single-use plastic, such as PET.

Pet Packaging Market Trends

Bottles to Have Significant Growth

- The high barrier qualities of polyethylene terephthalate (PET) against water vapor, gases, diluted acids, oils, and alcohols make it a common material for food packing. Additionally, PET is easy to recycle, reasonably flexible, and shatterproof. According to Earth Day organizers, one million plastic bottles are purchased in the United States every minute. The average American drinks in 167 plastic water bottles annually. Due to the region's growing need for packaged drinking water, there is an increasing market for PET plastic tops and enclosures.

- PET, derived from PE, offers excellent stiffness compared to other types of plastic. Additionally, it keeps a robust protective structure and possesses extraordinary moisture resistance abilities. Plastic bottles for liquids or beverages are produced using it. PET is used to make disposable plastic containers that are also used for packaging frozen or ready-to-eat foods. PET is well-liked because it provides a sound oil barrier, which helps the material fend off chemicals that could harm it.

- The expanding e-commerce sector also contributes substantially to the market's expansion worldwide. Numerous brands are employing PET more frequently because it is simple to carry PET bottles and jars from a logistics perspective. Additionally, because PET bottles are lightweight and don't need to be handled carefully, the cost of transportation is greatly diminished. Therefore, it is projected that the market demand will be supported over the forecast period by people's growing propensity for online shopping.

- The demand for PET for creating bottles and jars is anticipated to increase significantly due to the rising demand for food and beverage items worldwide. Additionally, the packaging of hand sanitizers in PET bottles saw a rise in need in the healthcare sector. In addition, the demand for hand sanitizer bottles is anticipated to stay high as COVID-19's effects persist and certain countries continue to see an increase in coronavirus cases, which will fuel the expansion of PET bottles for hand sanitizer packaging.

- Several advancements and trends in how companies and products use PET demonstrate the focus on PET and the expansion of its market share. PET has many uses and is easily blown into bottles or shaped into sheets thanks to its clarity and built-in CO2 barriers. PET characteristics can be enhanced with colorants, UV blockers, oxygen barriers/scavengers, and other additives to create bottles that meet a brand's requirements.

Asia-Pacific to Witness Significant Growth in the Market

- China is among the largest polyethylene terephthalate (PET) markets worldwide. For the past few years, the country's growing production of engineering plastics, such as PET, has been aided by the plentiful availability of raw materials and low cost of manufacture. The demand for PET bottles in China is constantly rising. It is obvious how critical soft drinks are to PET's chances in China. It is significantly influenced by the bottled water industry and its key players, like Master Kong and Nongfu Spring, as well as the significant rise in bottled water consumption in China yearly.

- Due to PET's benefits over the currently utilized traditional packaging polymers, the usage of PET goods in the packaging sector (PET containers, bottles, etc.) is increasing. Due to rising exports and domestic consumption, packing materials are in higher demand in China from sectors including the food and beverage industry, consumer goods, and others.

- A variety of plastics, including polypropylene (PP), polyethylene terephthalate (PET), polyvinyl chloride (PVC), and others, are produced in India. India has a massive capability for producing PET, and most of the domestic market's needs are met. However, regional differences also exist in the domestic market's consumption of PET. Due to numerous end-user businesses and a vast distribution network, the North and West of India account for most PET use.

- The demand for single-serve and small-sized goods packaged in materials like PET and metal cans has surged in India as the country adopts an on-the-go food consumption trend. Because consumers are budget aware and look for products that provide value for money, flexible packaging materials like PET are still widely used nationwide.

- However, consumers have started gravitating toward alternate packaging materials because they have eco-friendly qualities. Due to their eco-friendliness and high capacity for recycling, glass and aluminum have seen significant acceptance rates in the area. As a result, customers are turning away from plastic in more significant numbers.

Pet Packaging Industry Overview

The PET packaging market is highly competitive and consists of several major players, such as Amcor Ltd, Gerresheimer AG, Berry Global Group Inc., Silgan Holdings Inc., and Resilux NV. Few big firms presently control the market in terms of market share. These market leaders with the largest market share are concentrating on growing their international consumer base. These businesses use tactical joint ventures to raise their market share and profitability.

- January 2022: Sonoco company planned to raise the prices for CPET (crystallized polyethylene terephthalate) thermoformed plastic trays and bowls by 9%, as the company faced unprecedented inflation in critical raw materials, as well as transportation, packaging, labor, and other direct and indirect manufacturing costs.

- January 2022: Berry and TotalEnergies announced their collaboration to reduce trash going to landfills and increase the circularity of food packaging. Berry will receive certified circular polymers from TotalEnergies owing to enhanced recycling of post-consumer plastic waste, which is usually challenging to recycle using current methods. As a result, Berry will be able to employ more recycled plastic in the packaging of its food and beverage items and its healthcare products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Outstanding Properties of PET

- 4.3.2 Rising Demand for Environment-friendly Packaging

- 4.4 Market Restraints

- 4.4.1 Regulations Against the Use of Plastics in Some Regions

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Types

- 5.1.1 Bottles and Jars

- 5.1.2 Bags and Pouches

- 5.1.3 Trays

- 5.1.4 Lids/Caps and Closures

- 5.1.5 Other Product Types

- 5.2 By Packaging

- 5.2.1 Rigid

- 5.2.2 Flexible

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceuticals

- 5.3.3 Personal Care and Cosmetic Industry

- 5.3.4 Industrial Goods

- 5.3.5 Household Products

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Amcor Ltd

- 6.1.2 Resilux NV

- 6.1.3 Gerresheimer AG

- 6.1.4 Berry Global Group Inc.

- 6.1.5 Silgan Holdings Inc.

- 6.1.6 Graham Packaging Company

- 6.1.7 GTX Hanex Plastic Sp. z.o.o.

- 6.1.8 Dunmore Corporation

- 6.1.9 Comar LLC

- 6.1.10 Sonoco Products Company

- 6.1.11 Huhtamaki OYJ

- 6.1.12 Nampak Limited

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年 PET 包裝市場報告(按包裝類型、形式、包裝類型、填充技術、最終用戶和地區)

2024-2032 年 PET 包裝市場報告(按包裝類型、形式、包裝類型、填充技術、最終用戶和地區) 2024 年 PET 包裝全球市場報告

2024 年 PET 包裝全球市場報告 PET 包裝市場 - 按包裝類型(硬包裝、軟包裝)、按產品類型(瓶子和罐子、袋子和小袋、蓋子和瓶蓋、托盤)、按行業垂直和預測,2023 - 2032 年

PET 包裝市場 - 按包裝類型(硬包裝、軟包裝)、按產品類型(瓶子和罐子、袋子和小袋、蓋子和瓶蓋、托盤)、按行業垂直和預測,2023 - 2032 年 PET 包裝市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、包裝類型、最終用戶、地區和競爭細分

PET 包裝市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按類型、包裝類型、最終用戶、地區和競爭細分 PET 包裝市場:按產品類型、按包裝、按最終用戶行業、按地區

PET 包裝市場:按產品類型、按包裝、按最終用戶行業、按地區 PET包裝市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

PET包裝市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測 全球PET包裝市場分析2022-2032年:按類型,飲料包裝,包裝型,最終用途,灌裝技術,地區,主要國家/地區預測,主要公司,COVID-19情況

全球PET包裝市場分析2022-2032年:按類型,飲料包裝,包裝型,最終用途,灌裝技術,地區,主要國家/地區預測,主要公司,COVID-19情況