|

市場調查報告書

商品編碼

1432582

汽車照明:市場佔有率分析、產業趨勢、成長預測(2024-2029)Automotive Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

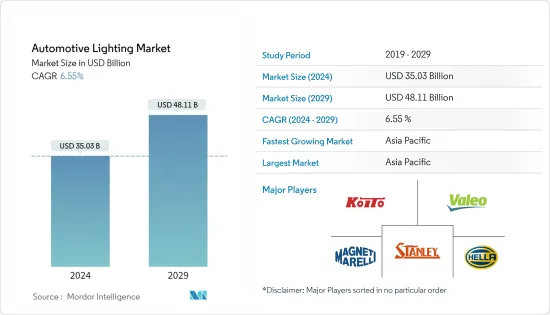

汽車照明市場規模預計到2024年為350.3億美元,預計到2029年將達到481.1億美元,在預測期內(2024-2029年)複合年成長率為6.55%。

全球汽車和 SUV 銷量自 2017 年約 9,435 萬輛的峰值以來一直在下降,並將於 2020 年降至略低於 7,700 萬輛。在全球經濟放緩和各主要經濟體出現冠狀病毒大流行的背景下,預計該行業將進入下行趨勢。

汽車製造商對將 LED 燈整合到他們的車輛中表現出極大的興趣,因為它們比鹵素燈或 HID 燈消耗更少的電力並且具有更長的使用壽命。此外,LED 燈耐用、堅固,並具有高品質發光二極體,優於所有其他照明技術。

汽車製造商正在開發新的照明技術,並專注於車頭燈等關鍵照明零件。我們建立合作夥伴關係以在市場競爭中獲得優勢。車頭燈是為夜間駕駛提供安全環境的主要因素。例如,大眾汽車與海拉合作開發了IQ.LIGHT LED頭燈。新款途銳豪華級 SUV 配備 IQ.LIGHT-LED 矩陣頭燈,配備 256 個 LED。

汽車照明市場趨勢

對車內舒適性和豪華功能的需求不斷成長

汽車產業正處於一場以新技術與傳統汽車製造融合為特徵的技術革命之中。隨著電動車的日益流行,汽車照明製造商正在開發新的照明技術來取代傳統的舊照明。電動車製造商正在推出具有最佳內裝的新車型。例如,2020年9月,Lucid Motors推出了Lucid Air,這是一款豪華電動轎車,基於Lucid獨特的空間概念理念,提供全尺寸豪華級內裝。

未來室內照明的發展將主要由安全、通訊、舒適和造型需求所驅動。光投影、智慧 LED、微型 LED、智慧功能表面、雷射照明、按需 3D 光圖案的引導材料以及具有隱藏照明效果的區域背光是一些新的照明技術。

機艙燈越來越受歡迎。主要包括閱讀燈和儀表板燈。車內燈具有多種應用,包括閱讀燈、車內環境照明系統以及採用最佳化導光技術的車頂模組。此外,儘管需求低於 LED 燈,但自我調整照明系統正呈現正成長率。

亞太地區推動汽車照明市場

從地區來看,汽車照明市場以亞太地區為主導,其次是歐洲和北美。推動這些地區市場成長的關鍵因素是:

- 豪華車的需求和銷售增加

- 汽車產量增加

- 由於物流業(主要是由於該地區電子商務行業的成長)和建築業的成長,商用車的銷售和需求增加

- 由於中階消費者可支配收入增加,低價汽車銷售增加

- 事故數量增加,尤其是在夜間

歐洲被認為是實施車輛安全標準的領先地區,重點關注乘客和行人的安全。本土汽車製造商和汽車零件供應商持續投資安全技術研發。隨著汽車產業技術的快速進步,歐洲地區有望在全球汽車照明市場中發揮重要作用。該地區擁有許多主要製造商,包括 Hella KGaA Hueck &Co.、飛利浦、OSRAM Licht AG、法雷奧、Zizala、羅伯特博世和 ZKW。

汽車照明產業概況

汽車照明市場相當整合,主要企業包括 Koito Manufacturing、法雷奧集團、Magneti Marelli、Stanley Electric、Hella、Lumax Industries、Zizila Lichtsysteme、Osram 和 Tungsram。公司正在建立合資企業並擴大其全球影響力。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場挑戰

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家/消費者的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭公司之間敵對關係的強度

第5章市場區隔

- 按車型

- 小客車

- 商用車

- 按應用程式類型

- 室內照明

- 環境照明

- 腳坑燈

- 頂燈

- 引導照明

- 外部照明

- 頭燈

- 霧燈

- 尾燈

- 日間行車燈 (DRL)

- 槳燈

- 高位煞車燈

- 室內照明

- 依技術

- 鹵素

- 氙

- LED

- 其他技術

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 世界其他地區

- 巴西

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他國家

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Koito Manufacturing Co. Ltd

- Stanley Electric Co. Ltd

- Valeo Group

- Magneti Marelli SpA

- HELLA KGaA Hueck & Co.

- Tungsram

- Hyundai Mobis

- Lumax Industries

- Osram

- Philips

- Zizala Lichtsysteme

第7章 市場機會及未來趨勢

The Automotive Lighting Market size is estimated at USD 35.03 billion in 2024, and is expected to reach USD 48.11 billion by 2029, growing at a CAGR of 6.55% during the forecast period (2024-2029).

Global sales of cars and SUVs fell to just under 77 million units in 2020, down from a peak of almost 94.35 million units in 2017. The sector is projected to experience a downward trend on the back of a slowing global economy and the advent of the coronavirus pandemic in all key economies.

Vehicle manufacturers are showing great interest in integrating LED lights in vehicles, as these lights consume less power and have a longer life when compared to halogen and HID lights. Furthermore, LED lights offer durability and strength, have high-quality light-emitting diodes, and are superior to all other forms of lighting technology.

The automotive manufacturers are developing new lighting technologies and are focusing on the major lighting components, such as headlights. They are entering into partnerships to be ahead in the competition within the market. Headlights are a major factor in providing a safe environment for driving at night. For instance, Volkswagen partnered with Hella to develop IQ.LIGHT LED headlamps. The new luxury-class Touareg SUV uses the IQ.LIGHT-LED Matrix Headlamps and 256 LEDs.

Automotive Lighting Market Trends

Growing Demand for Cabin Comfort and Luxury Features

The automotive industry is in the midst of a technological revolution characterized by the convergence of new technology with traditional car manufacturing. With the increasing trend of electric vehicles, automotive lighting manufacturers are developing new lighting technologies to replace the old traditional lights. Electric vehicle manufacturers are launching new vehicle models with the best cabin interiors. For instance, in September 2020, Lucid Motors launched Lucid Air, a luxurious electric sedan that offers a full-size luxury-class interior, which is based on Lucid's exclusive Space Concept philosophy.

Upcoming interior lighting developments will be mainly driven by safety, communication, comfort, and styling demands. Light projections, smart LEDs, micro-LEDs, smart functional surfaces, laser-based lighting, guiding materials for 3D light patterns on-demand, and area backlighting with hidden-until-lit effects are some of the new lighting technologies.

Cabin lights are gaining popularity. They mainly include reading lights and dashboard lights. Interior lights include various applications in the form of reading lamps, ambient interior lighting systems, and roof modules with optimized light guide technology. Additionally, the adaptive lighting system is seeing a positive growth rate, although their demands remain much smaller than LED lights.

Asia-Pacific is Leading the Automotive Lighting Market

Geographically, the automotive lighting market is led by the Asia-Pacific region, followed by the European and North American regions. Some of the major factors driving the growth of the markets in these regions are -

- An increase in the demand for and the sales of luxury cars.

- An increase in the production of vehicles.

- An increase in the sales of and demand for commercial vehicles, owing to the growing logistics industry (primarily due to the propelling e-commerce sector in the region) and the construction industry.

- A rise in the sales of low-cost vehicles, due to an increase in the disposable incomes of middle-class consumers.

- An increase in the number of accidents, especially during the night.

Europe has been recognized as a major region, focusing on both passengers and pedestrian safety and implementing safety standards for vehicles. The regional automotive manufacturers and the automotive component suppliers have been continually investing in the R&D of safety technologies. With rapid technological advancements in the automotive industry, the European region is expected to play a major role in the global automotive lighting market. The region is home to numerous major manufacturers, such as Hella KGaA Hueck & Co., Philips, OSRAM Licht AG, Valeo, Zizala, Robert Bosch, and ZKW.

Automotive Lighting Industry Overview

The automotive lighting market is fairly consolidated with key players such as Koito Manufacturing, Valeo Group, Magneti Marelli, Stanley Electric, Hella, Lumax Industries, Zizila Lichtsysteme, Osram, and Tungsram. Companies are entering into joint ventures and are expanding their global presence. For instance,

- Valeo announced the acquisition of 10.5% of the stake in Aledia, a technology startup company dedicated to the development of cutting-edge LED technology for general and automotive lighting.

- Koito Automotive inaugurated the Hubei Koito Automotive Lamp Co. Ltd plant in China.

- ZKW started the production of the world's first laser-beam headlamps for the BMW i8.

- In 2017, Osram India launched a new automotive lighting solution called Rallye, which is compatible with two-wheelers, four-wheelers, and other commercial vehicles. The product is being manufactured in Osram's manufacturing plants in Germany and China.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Challenges

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Commercial Vehicles

- 5.2 By Application Type

- 5.2.1 Interior Lighting

- 5.2.1.1 Ambient Lighting

- 5.2.1.2 Footwell Lights

- 5.2.1.3 Roof Lights

- 5.2.1.4 Boot Lights

- 5.2.2 Exterior Lighting

- 5.2.2.1 Headlamps

- 5.2.2.2 Fog Lamps

- 5.2.2.3 Taillights

- 5.2.2.4 Daytime Running Lights (DRLs)

- 5.2.2.5 Puddle Lamps

- 5.2.2.6 High Mounted Stop Lamp

- 5.2.1 Interior Lighting

- 5.3 By Technology

- 5.3.1 Halogen

- 5.3.2 Xenon

- 5.3.3 LED

- 5.3.4 Other Technologies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 United Arab Emirates

- 5.4.4.4 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Koito Manufacturing Co. Ltd

- 6.2.2 Stanley Electric Co. Ltd

- 6.2.3 Valeo Group

- 6.2.4 Magneti Marelli SpA

- 6.2.5 HELLA KGaA Hueck & Co.

- 6.2.6 Tungsram

- 6.2.7 Hyundai Mobis

- 6.2.8 Lumax Industries

- 6.2.9 Osram

- 6.2.10 Philips

- 6.2.11 Zizala Lichtsysteme

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球汽車照明市場規模、佔有率、成長分析,依技術(鹵素和 LED)、依應用(外部照明和內部照明)- 2024-2031 年行業預測

全球汽車照明市場規模、佔有率、成長分析,依技術(鹵素和 LED)、依應用(外部照明和內部照明)- 2024-2031 年行業預測 汽車智慧照明:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)

汽車智慧照明:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029) 全球內燃機汽車和電動車照明市場:按技術、類型、位置、應用、車輛類型、地區分類 - 預測至 2030 年

全球內燃機汽車和電動車照明市場:按技術、類型、位置、應用、車輛類型、地區分類 - 預測至 2030 年 下一代汽車照明市場:按產品類型、技術類型、車輛類型、配銷通路- 2024-2030 年全球預測

下一代汽車照明市場:按產品類型、技術類型、車輛類型、配銷通路- 2024-2030 年全球預測 2024年汽車輔助燈全球市場報告

2024年汽車輔助燈全球市場報告 2023-2030年全球汽車輔助燈市場規模研究與預測(按類型、技術、產品類型、銷售通路、車型和區域分析)

2023-2030年全球汽車輔助燈市場規模研究與預測(按類型、技術、產品類型、銷售通路、車型和區域分析) 全球汽車照明市場規模、佔有率和行業趨勢分析報告:2023-2030年按位置、車型、技術、銷售管道和地區分類的展望和預測

全球汽車照明市場規模、佔有率和行業趨勢分析報告:2023-2030年按位置、車型、技術、銷售管道和地區分類的展望和預測 亞太地區下一代汽車照明市場分析與預測:2022-2031

亞太地區下一代汽車照明市場分析與預測:2022-2031 2024 年汽車照明全球市場報告

2024 年汽車照明全球市場報告 2024 年汽車發光二極體(LED) 燈泡全球市場報告

2024 年汽車發光二極體(LED) 燈泡全球市場報告