|

市場調查報告書

商品編碼

1445932

農場管理軟體 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Farm Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

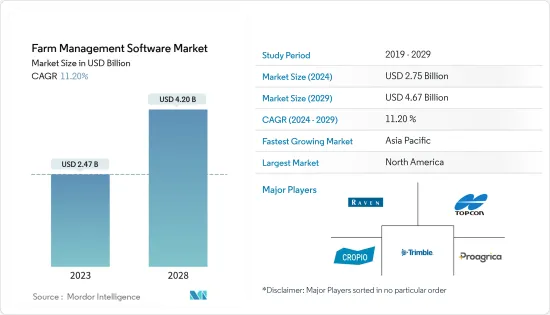

農場管理軟體市場規模預計到2024年為 27.5 億美元,到2029年將達到 46.7 億美元,在預測期內(2024-2029年)CAGR為 11.20%。

主要亮點

- 農場管理軟體的採用逐年增加,農民的需求轉向高生產力和投資回報。用於研究測試的客製化技術系統的開發,包括農民可以輕鬆存取的各種硬體和軟體,加速農場管理軟體市場的成長。

- 農場管理軟體市場的成長在很大程度上也是由農業活動的增加和對決策即時資料的需求不斷增加所推動的。機器學習和人工智慧成為各種農業應用的主流技術,例如精準農業、牲畜監測、養魚和智慧溫室實踐。他們管理硬體設備和個人之間交換的資料,以簡化農場管理流程。

- 此外,各國政府正採取措施鼓勵採用現代農業技術。例如,2021年10月,英國環境、食品和農村事務部(Defra)與英國研究與創新部合作啟動了一項資助計劃,目的是推動農業部門採用創新技術,以提高農民的獲利能力。

- 創新是應對農業部門面臨的挑戰的重要因素。人工智慧和機器學習的滲透簡化了計劃、採購、餵食、收穫、行銷和庫存控制等資料管理活動。新的想法、技術和流程,例如農場管理軟體,將在幫助農民、種植者和企業提高生產力方面發揮關鍵作用,這將導致預測期內研究的市場的成長。

農場管理軟體市場趨勢

農場勞動力短缺和耕地減少

近年來,由於人們對農業的興趣下降,加上農民人口老化,農業勞動力減少。根據聯合國糧農組織2021年統計報告,農林漁業對就業的貢獻從2017年的896,341萬人下降至2020年的873,757萬人。此外,美國、英國等國家的農業產業依賴勞動力方面,其他已開發國家也出現了類似的趨勢。同樣,農業、林業和漁業在經濟中佔據重要地位的亞太地區,勞動力數量也大幅下降,從2017年的 618,147 萬人減少到2020年的 589,103 萬人。

由於技術輔助農業需要技術熟練的勞動力,而技術勞動力卻嚴重短缺,考慮到當前的挑戰,精準農民欽佩並傾向於使用高效的軟體。這種情況是推動市場前進的主要因素之一。耕地減少和全球人口增加是推動市場的主要原因。

此外,根據世界銀行的資料,人均耕地面積從2017年的 0.19 公頃減少到2020年的 0.18 公頃。這促使種植者提高每公頃可用土地的生產力,以滿足日益成長的糧食需求。此外,植保化學品使用中的環境安全等問題日益突出,導致各國政府對植保化學品的使用實施了嚴格的規定。農業領域的所有這些變化推動農場管理軟體的使用,幫助農民提高生產力和投資回報。因此,隨著耕地面積的減少,農業勞動力的短缺預計將推動農民對農場管理軟體的採用率,在預測期內提振整體市場。

北美主導市場

在北美,由於該地區領先的工業自動化行業和人工智慧解決方案的採用,預計未來幾年農場管理軟體將呈指數級成長。與發展中國家相比,已開發國家更大的農場和農民的意識導致現代技術的快速採用。這使得北美地區成為最大的農場管理軟體技術市場。

多年來,美國一直處於將精密技術應用於農業技術的前沿。根據美國農業部(USDA)的報告,2017年美國農場平均面積為441英畝,2021年將增加至445英畝。大型農場更有可能採用智慧農業技術和軟體。隨著美國平均農場規模的擴大和農場勞動力的短缺,大農場主完全有能力使用農業軟體來獲得資料驅動的見解,以最佳化作物產量。

此外,該地區的參與者和政府採取進一步提振市場的措施。例如,2022年,加拿大政府根據農業科學計劃,透過加拿大農業合作夥伴關係向 Mojow Autonomous Solutions Inc. 提供了高達 419,000 美元的資金,投資於農業數位化,以加強加拿大農業部門的永續性。

同樣,加拿大蛋白質工業公司與 Farmers Edge Inc. 和 OPI Systems 合作,投資 2,100 萬美元用於農民資料分析專案,收集與植物和儲存健康管理相關的農場級資料,這些資料可用於開發預測模型可以使用人工智慧(AI)和機器學習來幫助農民提高產量,並做出更好的儲存和行銷決策。預計這將增加種子選擇、設備選擇、灌溉和收穫後管理領域的投資回報。

因此,透過數位技術和人工智慧的融合,農民可以更有效和有效率地管理資源。因此,大型農場、農民的高採用率以及政府措施推動預測期內該地區研究的市場。

農場管理軟體產業概述

農場管理軟體市場高度分散。 Raven Industries, Inc.、Trimble Inc.、Topcon Corporation、Cropio Group(Syngenta)和 Relex Group(Proagrica)是市場上的一些主要參與者。玩家們投資新產品並改進現有產品。他們也參與合作、擴張和收購。

附加優惠:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 研究範圍

第2章 研究方法

第3章 執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 市場限制

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭激烈程度

第5章 市場細分

- 類型

- 本地/基於網路

- 基於雲端

- 軟體即服務(SaaS)

- 平台即服務(PaaS)

- 應用

- 精耕

- 牲畜監測

- 智慧溫室

- 水產養殖

- 其他應用

- 地理

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 西班牙

- 歐洲其他地區

- 亞太

- 印度

- 中國

- 澳洲

- 日本

- 亞太其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 非洲

- 南非

- 非洲其他地區

- 北美洲

第6章 競爭格局

- 最常用的策略

- 市佔率分析

- 公司簡介

- Deere & Company

- Trimble Inc.

- Raven Industries Inc.

- AG Leader Technology

- AGJunction

- AGCO Corporation

- Agrivi

- Topcon Corporation

- Bayer Crop Science(The Climate Corporation)

- Relex Group(Proagrica)

- Cropio Group

- CropIn Technology Solutions Private Limited

第7章 市場機會與未來趨勢

The Farm Management Software Market size is estimated at USD 2.75 billion in 2024, and is expected to reach USD 4.67 billion by 2029, growing at a CAGR of 11.20% during the forecast period (2024-2029).

Key Highlights

- The adoption of farm management software is increasing every year, with farmer needs shifting toward high productivity and return on investments. The development of customized technological systems for research testing, comprising various hardware and software that are easily accessible by the farmers, is accelerating the growth of the farm management software market.

- The growth of the farm management software market is also largely driven by the increasing agricultural activities and increasing need for real-time data for decision-making. Machine learning and Artificial intelligence are becoming the mainstream technologies for various farming applications, such as precision farming, livestock monitoring, fish farming, and smart greenhouse practices. They manage the data exchanged between hardware equipment and individuals to streamline the farm management process.

- Furthermore, governments are taking initiatives to encourage the adoption of modern agricultural technologies. For instance, in October 2021, the UK Department for Environment, Food and Rural Affairs (Defra) and UK Research and Innovation partnered to launch a funding program aimed at driving the adoption of innovative technology in the agricultural sector to improve the profitability of the farmers.

- Innovation is a vital factor in addressing the challenges faced by the agricultural sector. The penetration of artificial intelligence and machine learning has simplified data management activities such as planning, purchasing, feeding, harvesting, marketing, and inventory control. New ideas, technologies, and processes, such as farm management software, will play a key role in helping farmers, growers, and businesses to become more productive, which will result in the growth of the market studied during the forecast period.

Farm Management Software Market Trends

Farm Labor Shortage and Decreasing Arable Land

The agriculture labor force has decreased in recent years due to the decreased interest in farming, combined with the aging farmer population. According to the FAO statistics 2021 report, the agriculture, forestry, and fishing sector's contribution to employment declined from 896,341 thousand people in 2017 to 873,757 thousand people in 2020. Furthermore, the agricultural industry in the US and the UK, among other countries, depend on laborers, and a similar trend is seen across other developed countries as well. On a similar note, Asia-Pacific, where agriculture, forestry, and fishing occupy a significant part of the economy, is witnessing a massive decline in the workforce, nearly a decline of 618,147 thousand people in 2017 to 589,103 thousand people in 2020.

As technologically assisted agriculture needs skilled laborers that are in acute shortage of availability, precision farmers admire and tend to consume software that can be productive, considering the current challenge. This scenario is one of the major factors that drive the market forward. The decreasing arable land and the increasing global population are among the major reasons driving the market.

Further, according to the World Bank, the area of arable land hectares per person decreased from 0.19 hectares in 2017 to 0.18 hectares in 2020. This pushed growers to increase their productivity per hectare of land available to meet the growing demand for food. Additionally, rising issues, such as environmental safety regarding the usage of crop protection chemicals, led the government of various countries to impose strict regulations on the use of crop protection chemicals. All these changes in the agriculture field are boosting the use of farm management software, which helps farmers increase their productivity and the return on investment. As a result, the shortage of farm labor, with the decreasing area of arable land, is expected to drive the rate of adoption of farm management software among farmers, providing a boost to the overall market during the forecast period.

North America Dominates the Market

In North America, farm management software is anticipated to witness exponential growth in the coming years, owing to the leading industrial automation industry and the adoption of artificial intelligence solutions in the region. The larger farms and awareness among the farmers lead to the quick adoption of modern technologies in developed countries compared to developing nations. This makes the North American region the largest farm management software technologies market.

Over the years, the United States has been at the forefront of deploying precision technology to farming techniques. As per a report by the US Department of Agriculture (USDA), the average farm size in the United States was 441 acres in 2017, which increased and reached 445 acres in 2021. As large-holding farms are more likely to adopt smart agriculture technologies and software. With an increase in the average farm size in the United States and the shortage of farm laborers, large-holding farmers are well-positioned to use farming software to gain data-driven insights for optimizing crop yields.

Furthermore, players and governments in the region are taking initiatives that are further boosting the market. For instance, in 2022, the Government of Canada invested in the digitization of farming to strengthen the sustainability of Canada's agriculture sector by granting up to USD 419,000 to Mojow Autonomous Solutions Inc., through the Canadian Agricultural Partnership, under the AgriScience Program.

Likewise, the protein industries Canada has partnered with Farmers Edge Inc. and OPI systems and invested USD 21 million in the project of data analysis farmers and collecting farm-level data related to plant and storage health management, which can be applied to develop predictive models that may use artificial intelligence (AI) and machine learning that can help farmers improve production, as well as make better storage and marketing decisions. This is anticipated to increase return on investments in the areas of seed selection, equipment selection, irrigation, and post-harvest management.

Hence, with the integration of digital technologies and artificial intelligence, farmers can manage resources more effectively and efficiently. Therefore, the large-sized farms, high adoption rate by farmers, and government initiatives are boosting the market studied in the region during the forecast period.

Farm Management Software Industry Overview

The farm management software market is highly fragmented. Raven Industries, Inc., Trimble Inc., Topcon Corporation, Cropio Group (Syngenta), and Relex Group (Proagrica) are some of the major players operating in the market. The players are investing in new products and improvising their existing ones. They are also involved in partnerships, expansions, and acquisitions.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Local/Web-based

- 5.1.2 Cloud-based

- 5.1.2.1 Software as a Service (SaaS)

- 5.1.2.2 Platform as a Service (PaaS)

- 5.2 Application

- 5.2.1 Precision Farming

- 5.2.2 Livestock Monitoring

- 5.2.3 Smart Greenhouse

- 5.2.4 Aquaculture

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 India

- 5.3.3.2 China

- 5.3.3.3 Australia

- 5.3.3.4 Japan

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Rest of Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Deere & Company

- 6.3.2 Trimble Inc.

- 6.3.3 Raven Industries Inc.

- 6.3.4 AG Leader Technology

- 6.3.5 AGJunction

- 6.3.6 AGCO Corporation

- 6.3.7 Agrivi

- 6.3.8 Topcon Corporation

- 6.3.9 Bayer Crop Science (The Climate Corporation)

- 6.3.10 Relex Group (Proagrica)

- 6.3.11 Cropio Group

- 6.3.12 CropIn Technology Solutions Private Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球農場管理軟體市場:按應用、按產品、按農場規模、按農場產量、按地區 - 預測到 2029 年

全球農場管理軟體市場:按應用、按產品、按農場規模、按農場產量、按地區 - 預測到 2029 年 2024 年農場管理軟體全球市場報告

2024 年農場管理軟體全球市場報告 全球農場管理軟體市場 2024-2028

全球農場管理軟體市場 2024-2028 農場管理軟體市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

農場管理軟體市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 歐洲農場管理軟體與資料分析市場分析與預測:2022-2027

歐洲農場管理軟體與資料分析市場分析與預測:2022-2027 農場管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測,按農業類型、農場生產規劃、類型、按應用、地區和競爭細分,2018-2028

農場管理軟體市場-全球產業規模、佔有率、趨勢、機會和預測,按農業類型、農場生產規劃、類型、按應用、地區和競爭細分,2018-2028 農場管理軟體市場規模、佔有率、趨勢分析報告:按農業類型、部署模型、解決方案、地區和細分市場預測,2023-2030 年

農場管理軟體市場規模、佔有率、趨勢分析報告:按農業類型、部署模型、解決方案、地區和細分市場預測,2023-2030 年 農場管理軟體市場、份額、規模、趨勢、產業分析報告:按農業類型、按部署模式、按服務、按地區、細分市場預測,2023-2032 年

農場管理軟體市場、份額、規模、趨勢、產業分析報告:按農業類型、按部署模式、按服務、按地區、細分市場預測,2023-2032 年 農場管理軟體及資料分析市場- 全球及各地區分析:各用途,各產品,各國分析:分析、預測(2022年~2027年)

農場管理軟體及資料分析市場- 全球及各地區分析:各用途,各產品,各國分析:分析、預測(2022年~2027年) 農場管理軟體的全球市場

農場管理軟體的全球市場