|

市場調查報告書

商品編碼

1445880

離散半導體 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029 年)Discrete Semiconductor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

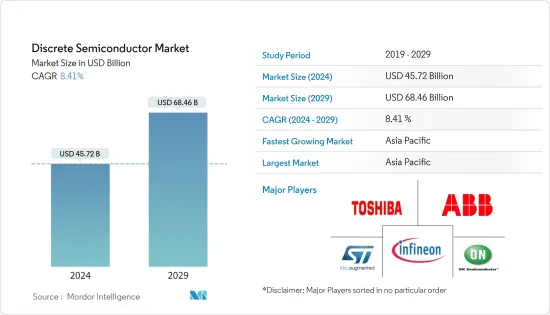

離散半導體市場規模預計到2024年為457.2億美元,預計到2029年將達到684.6億美元,在預測期內(2024-2029年)CAGR為8.41%。

離散半導體市場是由電子和小型化領域對電源管理日益成長的需求所推動的。封裝尺寸的減小與功耗成反比。例如,恩智浦半導體透過保持相同的功率性能,將其電晶體系列的封裝尺寸縮小了 55%。此外,Diodes 公司也推出了採用 DFN2020 封裝的 40V 額定值 DMTH4008LFDFWQ 和 60V 額定值 DMTH6016LFDFWQ 汽車級 MOSFET。

主要亮點

- 此外,汽車零件的安全、資訊娛樂、導航和燃油效率等特性,以及工業零件的安全、自動化、固態照明、運輸和能源管理等特性預計將推動所研究的市場。例如,絕緣柵雙極電晶體(IGBT)是電動車電力電子系統中不可或缺的組件。由於全球電動車銷量的增加,預計 IGBT 的需求將會很大。 IEA報告顯示,2021年全球電動車銷量達660萬輛。電動車佔全球汽車銷量的9%。

- 這些電動車的商業化正在興起。沃爾沃的目標是到 2025 年其銷量的 50% 由純電動車構成。寶馬也放棄了 i5 計劃,現在將重點放在 X3 和 4 系列 GT 等其他系列車型的電氣化上。後者將直接與特斯拉的Model 3和Model y競爭。

- 此外,各公司正在電源模組領域開發新的解決方案,以擴大其影響力並增加市場佔有率。例如,2021 年 12 月,為各種電子應用領域的客戶提供服務的著名半導體公司意法半導體宣布推出第三代 STPOWER 碳化矽 (SiC) MOSFET1,推動了最先進的用於電動車(EV) 動力系統和其他以功率密度、能源效率和可靠性為關鍵目標標準的應用的功率元件。

- 相較之下,COVID-19 疫情對全球和各國經濟產生了巨大影響。許多最終用戶產業都受到了影響,包括離散半導體。電子元件製造的很大一部分包括在工廠車間進行的工作,人們在工廠車間密切接觸,協作提高生產力。目前,市場上的企業正在快速評估市場需求、供應鏈和勞動力三個面向的影響。產品的需求正在 ASICS、記憶體、感測器等方面發生變化,而消費者行為則快速變化且未來波動較大。此外,許多公司也推遲了硬體升級和其他長期遷移項目。例如,印度、日本、波蘭、以色列等許多國家5G計畫的推出都被推遲,這為5G商用服務的推出帶來了不確定性。

- 隨著病毒在世界各地傳播,全球供應鏈受到干擾,隔離期限仍存在不確定性。世界各地許多製造工廠被關閉以遏制這種致命病毒。例如,由於馬來西亞、中國、馬來西亞和菲律賓等國家的政府強制要求,安森美半導體的大部分製造設施被關閉,這影響了其向客戶供應產品的能力,並造成了供需缺口。

離散半導體市場趨勢

汽車領域預計將推動市場成長

- 汽車應用推動了對離散元件的大部分需求,尤其是功率電晶體和整流器。傳統汽車自 20 世紀 50 年代以來一直使用 12V 電池系統,但在當前情況下,它們無法處理下一代汽車更重的電子負載,因此需要提高電源效率。

- 自動駕駛和全電動汽車需要更高性能的微控制器和微處理器,以及更有效率、高功率的 MOSFET,用於電源管理和電池監控系統。

- 離散半導體在電動車中已廣泛應用。空間限制和高效率要求要求設備能夠承載高功率並以更高的頻率進行開關。它們可以以非常低的損耗和非常高的頻率產生高電流,從而為電動車應用創造了對這些設備的巨大需求。

- 此外,隨著電動車市場的加速發展,許多汽車製造商現在都採用 800V 驅動系統來提高效率、實現更快的充電並擴大此類車輛的續航里程,同時減輕重量和成本。 SiCMOSFET 等寬頻隙元件正在幫助汽車製造商為電動車動力系統和其他此類因素非常重要的應用開發最先進的功率元件。

- 2022年12月,義法半導體推出了新型碳化矽(SiC)高功率模組,旨在提高電動車的性能和續航里程。現代汽車已選擇五款基於 SiC MOSFET 的新型功率模組,用於Kia EV6 和多款車型共享的 E-GMP 電動車平台。

- 2022年8月,瑞薩電子公司宣布開發新一代Si-IGBT。透過此次發布,該公司瞄準了下一代電動車逆變器,AE5 代 IGBT 預計將於 2023 年上半年開始在瑞薩位於 Naka 的工廠的 200 毫米和 300 毫米晶圓生產線上進行量產。日本。

- 電動車市場競爭激烈,新廠商正在課題創新極限。例如,保時捷為其 Taycan 配備了 800 V 系統,而許多當代電動車則使用 400 V 電池。這促使傳統汽車零件製造商為汽車產業開發離散半導體產品線。

美洲預計將佔據主要市場佔有率

- 該地區消費電子產業的激增是推動市場成長的主要因素之一。例如,根據美國消費者科技協會(CTA)的預測,2023年美國科技零售收入預計將達到4,850億美元,雖然較2021年創紀錄的5,120億美元略有下降,但仍將維持在2023年之前的水平以上。 - 根據組織的規定,流行病級別。

- 此外,物聯網 (IoT) 等新興技術在半導體產業掀起了新一輪創新浪潮。該地區每年都有越來越多的電子設備(從筆記型電腦到恆溫器)相互連接,使它們與其用戶之間能夠進行更複雜的通訊和協調。例如,根據 CTA 的數據,到 2021 年,23% 的美國家庭擁有智慧或連網健康監測設備,19% 擁有連網運動或健身設備(比前一年增加 7 個百分點)。不斷擴大的物聯網市場預計將對該地區對離散半導體的需求產生正面影響。

- 根據汽車研究中心的數據,美國汽車產業是經濟成長的重要組成部分,歷來對國內生產毛額 (GDP) 的貢獻率為 3 - 3.5%。該產業也佔該地區半導體元件總需求的很大一部分。

- 汽車產業向電氣化的轉型也刺激了對複雜半導體元件的需求。例如,根據 IEA 年度《2023 年全球電動車展望》,美國是第三大電動車市場,銷量強勁成長 55%。

- 此外,根據阿貢國家實驗室的數據,2023會計年度美國混合動力汽車銷量為97,972輛,比2022年4月的銷量成長36.4%。本月豐田佔混合動力汽車總銷量的44.3%。

- 加拿大不斷成長的再生能源產業預計也將支持市場成長。根據加拿大再生能源協會(CanREA) 的數據,加拿大的風能和太陽能產業在2022 年將大幅成長。該組織表示,太陽能成長尤其迅速,2022 年新增裝置容量佔加拿大總裝置容量的四分之一以上獨自的。

離散半導體產業概況

全球離散半導體市場高度分散,有許多半導體製造商提供產品。這些公司不斷投資於產品和技術,以促進永續的環境成長並防止環境危害。這些公司也收購了其他專門經營這些產品的公司,以提高市場佔有率。市場的一些最新發展是:

- 2023年1月,日本著名汽車零件製造商日立Astemo有限公司宣布,其電動車逆變器將採用羅姆半導體全新第四代SiCMOSFET和閘極驅動器IC。 ROHM 最新的第四代 SiCMOSFET 提供業界最低的導通電阻,並改善了短路耐受時間,與 IGBT 相比,可將電動車的續航里程增加 6%。

- 2023 年 1 月,瑞薩電子公司宣布推出一款新型閘極驅動器 IC,旨在驅動電動車 (EV) 逆變器中的 IGBT 和 SiC MOSFET 等高壓功率元件。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- 產業價值鏈/供應鏈分析

- 評估 COVID-19 對市場的影響

- 市場促進因素

- 汽車和電子領域對高能源效率設備的需求不斷成長

- 綠色能源發電需求拉動市場

- 市場限制

- 積體電路需求不斷成長

第 5 章:市場區隔

- 建築類型

- 場效管

- MOSFET - 依材料分類

- 矽MOSFET

- 碳化矽MOSFET

- MOSFET - 由最終用戶提供

- 消費性電子產品

- 醫療的

- 汽車

- 運算與儲存

- 工業的

- 網路與電信

- 其他最終用戶

- IGBT - 概述和市場預測

- 汽車

- 能源(生產和分配)

- 運輸

- 工業的

- 商業的

- 雙極電晶體

- 閘流管

- 整流器

- 其他類型(結型閘極場效電晶體 (JFET)、GaN HEMT、雙向可控矽、變容二極體、TVS 二極體和齊納二極體)

- 場效管

- 最終用戶垂直領域

- 汽車

- 消費性電子產品

- 溝通

- 工業的

- 其他最終用戶垂直領域

- 地理

- 美洲

- 歐洲

- 亞太地區(中國、日本、台灣)

- 世界其他地區

第 6 章:競爭格局

- 公司簡介

- ABB Ltd

- On Semiconductor Corporation (Fairchild Semiconductor)

- Infineon Technologies AG

- STMicroelectronics NV

- Toshiba Electronic Devices & Storage Corporation

- NXP Semiconductors NV (To be Acquired by Qualcomm)

- Diodes Incorporated

- Nexperia BV

- D3 Semiconductor LLC

- Eaton Corporation PLC

- Hitachi Ltd

- Mitsubishi Electric Corp.

- Fuji Electric Corp.

- Taiwan Semiconductor Manufacturing Company Ltd

- Vishay Intertechnology Inc.

- Renesas Electronics Corporation

- ROHM Co. Ltd

- Microsemi Corporation (Microchip Technology)

- Qorvo Inc.

- Cree Inc.

- General Electric Company

- Littelfuse Inc

- United Silicon Carbide Inc.

第 7 章:投資分析

第 8 章:市場機會與未來趨勢

The Discrete Semiconductor Market size is estimated at USD 45.72 billion in 2024, and is expected to reach USD 68.46 billion by 2029, growing at a CAGR of 8.41% during the forecast period (2024-2029).

The discrete semiconductor market is driven by the increasing need to manage power across electronics and miniaturization. The reduction in package size is inversely proportional to power dissipation. For instance, NXP semiconductors achieved a 55% reduction in packaging size for their transistors range by retaining the same power performance. Additionally, Diodes Incorporated launched 40V-rated DMTH4008LFDFWQ and 60V-rated DMTH6016LFDFWQ automotive-compliant MOSFETs packaged in DFN2020.

Key Highlights

- Moreover, characteristics like safety, infotainment, navigation, and fuel efficiency in the automotive components, and security, automation, solid-state lighting, transportation, and energy management in industrial components are expected to fuel the market studied. For instance, an insulated gate bipolar transistor (IGBT) is an integral component in the EV power electronics system. IGBTs are expected to witness significant demand due to increasing sales of EVs globally. As per the IEA report, sales of electric cars globally reached 6.6 million in 2021. Electric cars accounted for 9% of global car sales.

- Commercialization of these electric vehicles is on the rise. Volvo is aiming for 50% of its sales to be made up of fully electric cars by 2025. BMW has also dropped its i5 plans and will now focus on electrification of other series models like the X3 and 4 Series GT. The latter will directly compete with Tesla's Model 3 and Model y.

- Furthermore, companies are developing new solutions in the power module segment to expand their presence and increase market share. For instance, In December 2021, STMicroelectronics, a prominent semiconductor company serving customers across the spectrum of electronics applications, has announced the release of its third generation of STPOWER silicon-carbide (SiC) MOSFETs1, advancing the state-of-the-art in power devices for electric-vehicle (EV) powertrains and other applications where power density, energy efficiency, and reliability are key target criteria.

- In contrast, the COVID-19 outbreak has had an enormous impact on the global and national economies. Many end-user industries have been affected, including discrete semiconductors. A large part of the manufacturing of electronic components includes work on the factory floor, where people are in close contact as they collaborate to boost productivity. Currently, companies in the market are quickly evaluating the impacts on three fronts: market demand, supply chain, and workforce. Demand for the product is shifting across ASICS, memory, sensors, etc., while consumer behavior changes rapidly and with future volatility. Also, many companies have delayed their hardware upgrades and other long-term migration projects. For instance, the rollout of the 5G plan has been delayed in many countries, such as India, Japan, Poland, and Israel, which, in turn, caused uncertainty for the launch of commercial 5G services.

- The global supply chains are disrupted as the virus spreads across the world, as still there is uncertainty over quarantine durations. Many manufacturing factories were shut down across the world to contain the deadly virus. For instance, most of the manufacturing facilities of On Semiconductors were shut down due to government mandates in countries like Malaysia, China, Malaysia, and the Philippines, which impacted its ability to supply products to its clients and created a gap in demand and supply.

Discrete Semiconductor Market Trends

The Automotive Segment is Expected to Drive the Market's Growth

- Automotive applications are driving a majority of the demand for discretes, especially for power transistors and rectifiers. Conventional cars have been using 12-V battery systems since the 1950s, but in the current scenario, they cannot handle the heavier electronic loads of next-generation vehicles, thus creating the need for power-efficiency.

- Autonomous driving and fully electric vehicles are demanding higher-performance microcontrollers and microprocessors, with more efficient, high-power MOSFETS, for power management and battery monitoring systems.

- Discrete semiconductors find widespread use in electric vehicles. Space limitations and high-efficiency requirements demand a device that can carry high power and switch at higher frequencies. They can have high currents with very low losses and at a very high frequency, creating significant demand for these devices for EV applications.

- Moreover, with the acceleration of the EV market, many car makers are now embracing 800-V drive systems to increase efficiency, achieve faster charging, and expand the range of such vehicles, all while reducing weight and cost. Wide-bandgap devices, such as SiCMOSFETs, are helping automakers advance state-of-the-art power devices for EV powertrains and other applications where such factors are important.

- In December 2022, STMicroelectronics launched new silicon-carbide (SiC) high-power modules designed to increase electric vehicles' performance and driving range. Five new SiC MOSFET-based power modules have been selected by Hyundai for use in the E-GMP electric vehicle platform shared by the KIA EV6 and multiple models.

- In August 2022, Renesas Electronics Corporation announced the development of a new generation of Si-IGBTs. Through this launch, the company imed at next-generation EV inverters, AE5-generation IGBTs were expected to be mass-produced starting in the first half of 2023 on Renesas' 200- and 300-mm wafer lines at the company's factory in Naka, Japan.

- The EVs market is highly competitive, and new manufacturers are pushing the envelope for innovation. For instance, Porsche equipped its Taycan with an 800 V system, while many contemporary electric cars operate with 400 V batteries. This led traditional automotive component manufacturers to develop their discrete semiconductor lineup for the automotive sector.

The Americas is Expected to Hold a Major Market Share

- The proliferating consumer electronics industry in the region is one of the primary factors driving the growth of the market. For instance, according to the Consumer Technology Association (CTA), U.S. technology retail revenues are expected to reach USD 485 billion in 2023. Though it is slightly down from the record-breaking USD 512 billion in 2021, the revenues will still remain above pre-pandemic levels, as per the organization.

- Further, emerging technologies like the Internet of Things (IoT) have created a new wave of innovation in the semiconductor industry. An increasing number of electronic devices, ranging from laptops to thermostats, are becoming connected each year in the region, allowing for more sophisticated communication and coordination between them and their users. For instance, as per the CTA, 23% of U.S. homes had smart or connected health monitoring devices in 2021, and 19% had connected sports or fitness equipment (up seven points from the previous year). The expanding IoT market is expected to positively influence the region's demand for discrete semiconductors.

- The automotive sector in the United States is a crucial component of economic growth and has historically contributed 3 - 3.5% to the overall Gross Domestic Product (GDP), as per the Center for Automotive Research. The industry also contributes to a significant portion of the region's total demand for semiconductor components.

- The automotive industry's transformation toward electrification is also fueling the demand for sophisticated semiconductor components. For instance, as per IEA's annual Global Electric Vehicle Outlook 2023, the United States is the third largest electric vehicle market, with strong sales growth of 55%.

- Moreover, according to Argonne National Laboratory, in FY2023, 97,972 HEVs were sold in the United States, up 36.4% from the sales in April 2022. Toyota accounted for a 44.3% share of total HEV sales this month.

- The growing renewable energy sector in Canada is also expected to support market growth. According to the Canadian Renewable Energy Association (CanREA), Canada's wind and solar energy sectors grew significantly in 2022. As per the organization, solar is growing particularly quickly, with more than one-quarter of all the installed capacity in Canada being added in 2022 alone.

Discrete Semiconductor Industry Overview

The global discrete semiconductor market is highly fragmented, with numerous semiconductor manufacturers providing the product. The companies are continuously investing in product and technology to promote sustainable environmental growth and prevent environmental hazards. The companies are also acquiring other companies that specifically deal with these products to boost the market's share. Some of the recent developments in the market are:

- In January 2023, Hitachi Astemo, Ltd., a renowned Japanese manufacturer of automotive components, announced that its electric vehicle inverters would use ROHM Semiconductor's new fourth-generation SiCMOSFETs and gate driver ICs. The newest fourth-generation SiCMOSFETs from ROHM offer the lowest ON-resistance in the industry and improved short-circuit withstand time, allowing for an increase in the cruising range of electric vehicles by 6% when compared to IGBTs.

- In January 2023, Renesas Electronics Corporation announced the introduction of a new gate driver IC designed to drive high-voltage power devices such as IGBTs and SiC MOSFETs for electric vehicle (EV) inverters.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain / Supply Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Market

- 4.5 Market Drivers

- 4.5.1 Rising Demand for High-energy and Power-efficient Devices in the Automotive and Electronics Segment

- 4.5.2 Demand for Green Energy Power Generation Drives the Market

- 4.6 Market Restraints

- 4.6.1 Rising Demand for Integrated Circuits

5 MARKET SEGMENTATION

- 5.1 Construction Type

- 5.1.1 MOSFET

- 5.1.1.1 MOSFET - BY MATERIAL

- 5.1.1.1.1 Si MOSFET

- 5.1.1.1.2 SiC MOSFET

- 5.1.1.2 MOSFET - BY END USER

- 5.1.1.2.1 Consumer Electronics

- 5.1.1.2.2 Medical

- 5.1.1.2.3 Automotive

- 5.1.1.2.4 Computing and Storage

- 5.1.1.2.5 Industrial

- 5.1.1.2.6 Network and Telecom

- 5.1.1.2.7 Other End Users

- 5.1.2 IGBT - Overview and Market Estimates

- 5.1.2.1 Automotive

- 5.1.2.2 Energy (Production and Distribution)

- 5.1.2.3 Transportation

- 5.1.2.4 Industrial

- 5.1.2.5 Commercial

- 5.1.2.6 Bipolar Transistor

- 5.1.2.7 Thyristor

- 5.1.2.8 Rectifier

- 5.1.2.9 Other Types (Junction Gate Field Effect Transistor (JFET), GaN HEMT, Triacs, Varactor Diodes, TVS Diodes, and Zener Diodes)

- 5.1.1 MOSFET

- 5.2 End-user Vertical

- 5.2.1 Automotive

- 5.2.2 Consumer Electronics

- 5.2.3 Communication

- 5.2.4 Industrial

- 5.2.5 Other End-user Verticals

- 5.3 Geography

- 5.3.1 Americas

- 5.3.2 Europe

- 5.3.3 Asia-Pacific (China, Japan, Taiwan)

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 ABB Ltd

- 6.1.2 On Semiconductor Corporation (Fairchild Semiconductor)

- 6.1.3 Infineon Technologies AG

- 6.1.4 STMicroelectronics NV

- 6.1.5 Toshiba Electronic Devices & Storage Corporation

- 6.1.6 NXP Semiconductors NV (To be Acquired by Qualcomm)

- 6.1.7 Diodes Incorporated

- 6.1.8 Nexperia BV

- 6.1.9 D3 Semiconductor LLC

- 6.1.10 Eaton Corporation PLC

- 6.1.11 Hitachi Ltd

- 6.1.12 Mitsubishi Electric Corp.

- 6.1.13 Fuji Electric Corp.

- 6.1.14 Taiwan Semiconductor Manufacturing Company Ltd

- 6.1.15 Vishay Intertechnology Inc.

- 6.1.16 Renesas Electronics Corporation

- 6.1.17 ROHM Co. Ltd

- 6.1.18 Microsemi Corporation (Microchip Technology)

- 6.1.19 Qorvo Inc.

- 6.1.20 Cree Inc.

- 6.1.21 General Electric Company

- 6.1.22 Littelfuse Inc

- 6.1.23 United Silicon Carbide Inc.

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

離散半導體市場:按類型、最終用戶分類 - 2024-2030 年全球預測

離散半導體市場:按類型、最終用戶分類 - 2024-2030 年全球預測 2024 年分立半導體世界市場報告

2024 年分立半導體世界市場報告 分離半導體市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

分離半導體市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 晶閘管分立半導體市場報告:2030 年趨勢、預測與競爭分析

晶閘管分立半導體市場報告:2030 年趨勢、預測與競爭分析 2023-2030 年全球分立半導體市場規模研究與預測、按類型(二極體、電晶體、晶閘管、模組)、按應用(網路與通訊、汽車、消費電子、工業及其他)和地區分析

2023-2030 年全球分立半導體市場規模研究與預測、按類型(二極體、電晶體、晶閘管、模組)、按應用(網路與通訊、汽車、消費電子、工業及其他)和地區分析 半導體分離式的全球市場 (2023-2028年):趨勢、成長機會、競爭分析

半導體分離式的全球市場 (2023-2028年):趨勢、成長機會、競爭分析 離散半導體的全球市場

離散半導體的全球市場 離散半導體的全球市場預測(2022年~2027年)

離散半導體的全球市場預測(2022年~2027年) 離散半導體的全球市場 - 市場規模,市場區隔,展望,收益預測:各類型,各零件,各用途,各地區(2022年~2028年)

離散半導體的全球市場 - 市場規模,市場區隔,展望,收益預測:各類型,各零件,各用途,各地區(2022年~2028年) 離散半導體的全球市場預測:各類型,各零件,各終端用戶,各地區的分析(到2028年)

離散半導體的全球市場預測:各類型,各零件,各終端用戶,各地區的分析(到2028年)