|

市場調查報告書

商品編碼

1445823

紙吸管 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Paper Straw - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

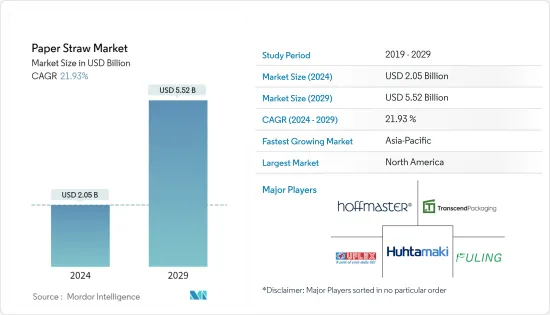

紙吸管市場規模預計到2024年為20.5億美元,預計到2029年將達到55.2億美元,在預測期內(2024-2029年)CAGR為21.93%。

各個最終用戶產業對紙草紙的需求不斷成長,預計將推動市場擴張。

主要亮點

- 對環保產品不斷成長的需求是推動市場成長的關鍵因素。政府採取了各種減少塑膠使用的舉措,並制定了嚴格的法律限制在器俱生產中使用傳統塑膠材料。通常,紙材質具有適應性強、多變、輕質、堅固且可回收等特性。它們可以製成各種顏色、形狀和尺寸,以滿足客戶的需求。快速成長的全球食品和飲料產業是另一個成長誘導因素。

- 然而,紙吸管的高成本和低價替代品的可用性可能會阻礙市場的成長。據 PacknWood 稱,紙吸管的成本約為 0.025 美元,明顯高於塑膠吸管的 0.005 美元。

- COVID-19 大流行對紙吸管產業產生了複雜的影響。市面上紙吸管的供需受到食品服務機構和餐廳關閉以及供應鏈管理中斷的影響。然而,網路訂餐趨勢的上升以及醫院攝取液體藥物對紙吸管的需求不斷成長正在推動紙吸管的銷售。

紙吸管市場趨勢

餐飲服務業推動市場

- 許多咖啡館和餐廳更注重路邊取貨或外帶。一些商店減少了店內容量,並建立了創造性的送貨選項,以確保封鎖期間的食品配送。食品和飲料行業預計將大幅增加紙吸管的需求。這主要是因為衛生產品的需求不斷成長,這使得紙張成為可行的包裝材料。

- 據StatsCan稱,預計2022年上半年加拿大的餐飲服務和飲酒場所將呈現成長趨勢。2022年1月的銷售額為33.2億美元,2022年7月增至57.9億美元。成長趨勢意味著食品飲料銷售量的上升,直接拉動了上述時期全國餐飲場所對紙吸管的需求。

- 值得注意的是,預計到 2023 年 12 月,加拿大將禁止銷售一次性塑膠(某些例外情況除外)。對於秸稈市場的參與者來說,食品服務業將繼續是他們的主要收入來源。近年來,各國紛紛禁止餐廳發放塑膠吸管。因此,多家公司正在選擇其他替代材料來製作餐具和吸管。

- 例如,加拿大麥當勞在 2021 年 10 月表示,將在 2021 年 12 月之前淘汰塑膠餐具、攪拌棒和吸管。這一逐步淘汰發生在加拿大 1,400 多個地點,同時加拿大政府正在採取行動禁止一次性塑膠,法規將於2021 年底敲定。截至2021 年11 月,木製餐具和攪拌棒以及紙吸管已在餐廳推出。截至2021 年11 月,麥當勞的目標是使用100% 回收、可再生或可重複使用的材料到2025 年,所有客戶的包裝中都會採用這種材料。

- 快餐店、全方位服務餐廳、咖啡和小吃店等最終用戶的健康成長需要方便的包裝,預計將推動生產更高包裝形式的需求。食物鏈持續成長的趨勢正在相應地增加市場需求。據麥當勞稱,2022年,該公司在全球經營和特許經營了40,275家門店,比2021年的40,031家門店有所增加。在過去17年裡,該公司的餐廳數量逐年成長。

亞太地區成長最快

- 推動原生紙包裝市場成長的因素是其輕量特性,使產品能夠有效率地運輸。目前,針對不同品牌的客製化包裝符合原紙包裝市場客戶的關鍵利益。然而,原料成本的快速上漲正在限制原紙包裝市場。

- 推動紙包裝市場成長的主要原因是人們越來越意識到採用永續和環保包裝材料的好處。一些國家強力的紙張回收措施正在為市場成長創造機會。來自軟塑膠包裝的競爭日益激烈是影響該地區紙包裝市場的最重要的限制。

- 印度計劃從2022年7月起禁止製造、進口、儲存、分銷、銷售和使用包括吸管在內的各種一次性塑膠製品。在此背景下,塑膠吸管禁令將限制深受印度大眾歡迎的小包裝軟性飲料的銷售。但該禁令還包括塑膠吸管,這是小包裝中的重要配件,因此軟性飲料公司預計會受到影響。此類禁令推動了該國紙吸管市場的發展。

- 快餐連鎖店專注於在該地區創新新的解決方案。例如,2022 年 10 月,日本麥當勞在所有門市都採用了紙吸管和木製餐具,這家快餐連鎖店預計每年將減少 900 噸塑膠垃圾。由於全國約 2,900 個地點的塑膠吸管和叉子供應耗盡,該連鎖店將停止提供塑膠吸管和叉子。日本四月頒布了一項減少一次性塑膠的法律後,麥當勞做出了這項改變,擴大了餐飲業在快速、低成本禮貌和永續發展之間平衡的努力。

- 此外,2022年6月,無菌包裝產品和解決方案的產業領導者之一Lamipak宣佈為印度市場推出U型紙吸管解決方案。 Lamipak 打算為受塑膠吸管禁令影響的飲料公司提供快速可靠的解決方案。該公司在中國擁有一條U型紙吸管生產線,併計劃在2023年第三季之前擴大在印尼的產能。全面投產後,兩張紙吸管生產線的總產能將達到每月2億根紙吸管,計劃到2023 年每月增加1 億。

- 塑膠廢棄物是一個重大且持久的環境問題,促使政府和企業重新考慮其方法並實施綠色舉措,例如回收和使用替代的可生物分解材料。雀巢(泰國)迎接課題,使MILO 泰國成為第一個推出首款軟性紙吸管的UHT 品牌,並在2022 年亞洲快速消費品獎中贏得年度綠色計劃獎- 泰國。所有這些舉措均由在該地區營運的公司實施將在預測期內增加該地區紙吸管的市場成長。

紙吸管行業概況

紙吸管市場相當分散。主要公司包括 UFlex Limited、Hoffmaster Group Inc.、Fuling Global Inc.、Canada Brown Eco Products Ltd 和 Huhtamaki OYJ。兩家公司不斷創新並建立策略合作夥伴關係,以維持其市場佔有率。

2022年4月,Ulfex推出了U型紙吸管,目標是第一個月生產1億根吸管,隨後幾個月生產2億根。 Ulfex 還打算每年生產 24 億根吸管。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭激烈程度

- 產業價值鏈分析

- COVID-19 對市場影響的評估

第 5 章:市場動態

- 市場促進因素

- 消費者對環保吸管的需求不斷增加

- 亞太地區需求不斷成長

- 市場限制

- 紙吸管的高成本和替代品的可用性

第 6 章:市場區隔

- 材料種類

- 維珍紙

- 再生紙

- 依應用

- 餐飲服務

- 家庭

- 機構

- 其他應用

- 依地理

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第 7 章:競爭格局

- 公司簡介

- UFlex Limited

- Hoffmaster Group Inc.

- Transcend Packaging Ltd.

- Huhtamaki OYJ

- Fuling Global Inc.

- Soton Daily Necessities Co. Ltd.

- Tetra Pak International SA

- Canada Brown Eco Products Ltd.

- Karat by Lollicup

- IPI SRL

第 8 章:投資分析

第 9 章:市場機會與未來展望

The Paper Straw Market size is estimated at USD 2.05 billion in 2024, and is expected to reach USD 5.52 billion by 2029, growing at a CAGR of 21.93% during the forecast period (2024-2029).

The increasing demand for paper straw papers across various end-user industries is anticipated to fuel market expansion.

Key Highlights

- The growing demand for environment-friendly products is the key factor driving the market's growth. There are various government initiatives to reduce plastic use and stringent laws that restrict using conventional plastic materials in the production of utensils. Typically, paper materials are adaptable, changeable, light, strong, and recyclable. They can be made in a wide range of colors, forms, and sizes to satisfy the client's needs. The rapidly growing global food and beverage industry is acting as another growth-inducing factor.

- However, the high cost associated with paper straws and the availability of the low price substitute can hinder the market's growth. According to PacknWood, paper straws cost about USD 0.025, which is significantly higher than USD 0.005 for plastic straws.

- The COVID-19 pandemic has had a complex effect on the paper straw industry. The supply and demand of paper straws in the market were affected by the closure of food service establishments and restaurants and a disruption in supply chain management. However, the rising trend in online food ordering and the growing demand for paper straws in hospitals for the intake of liquid medications are driving paper straw sales.

Paper Straw Market Trends

Foodservice sector to Drive the Market

- Numerous cafes and restaurants have focused more on curbside pickup or carryout only. Some stores reduced their in-store capacity and established inventive delivery options to ensure food delivery during the lockdowns. The food and beverage industry is anticipated to increase paper straw demand significantly. This is mainly because of the growing need for hygiene products, which has made paper a viable packaging material.

- According to StatsCan, there was expected to be a growing trend in food service and drinking places in Canada during the first half of 2022. The sale value in January 2022 amounted to USD 3.32 billion, which rose to USD 5.79 billion in July 2022. This growing trend signifies the upward movement in food and beverage sales, which directly pushes the demand for paper straws in the food and drinking places in the period above across the country.

- Notably, single-use plastics are expected to be banned from sale in Canada by December 2023 (barring certain exceptions). For players in the straw market, the food service sector would continue to be their primary source of income. In recent years, various countries have banned restaurants from giving out plastic straws. Due to this, multiple companies are choosing other alternative materials for their cutlery and straws.

- For instance, in October 2021, McDonald's Canada stated it would eliminate plastic cutlery, stir sticks, and straws by December 2021. The phase-out occurred at more than 1,400 Canadian locations and comes as the government of Canada moves to ban single-use plastics, with regulations finalized by the end of 2021. As of November 2021, wooden cutlery and stir sticks were already being rolled out in restaurants, along with paper straws, as of November 2021. McDonald's aims to use 100% recycled, renewable, or reusable materials in all its customers' packaging by 2025.

- The healthy growth of end-users, such as quick-service restaurants, full-service restaurants, and coffee and snack outlets, requiring convenient packaging is expected to drive the need to produce higher packaging formats. The trend of consistent growth of food chains is proportionately increasing the demand for the market. According to McDonald's, in 2022, it operated and franchised 40,275 locations globally, an increase over the 40,031 stores it used in 2021. During the past 17 years, the company has seen growth in restaurants year over year.

Asia-Pacific to Witness Fastest Growth

- The factor driving the growth of the virgin paper packaging market is its lightweight property, which allows the product to be efficiently transported. Customized packaging for different brands is currently in the critical interest of customers in the virgin paper packaging market. However, the rapidly increasing cost of the raw material is restraining the virgin paper packaging market.

- The primary reason driving the growth of the paper packaging market is the growing awareness of the benefits of adopting sustainable and environmentally friendly packaging materials. Strong paper recycling initiatives in several countries are creating opportunities for market growth. Increasing competition from flexible plastic packaging is the most significant constraint impacting the paper packaging market across the region.

- From July 2022, India planned to ban the manufacturing, importing, storing, distributing, selling, and using of various single-use plastic products, including straws. Against this backdrop, the ban on plastic straws will limit the sale of small packs of soft drinks that are popular with the Indian public. But the prohibition extends to plastic straws, an essential accessory in small packages, so soft drink companies were expected to be impacted. Such bans drive the market for paper straws in the country.

- Fast-food chains are focused on innovating new solutions in the region. For instance, in October 2022, McDonald's Japan adopted paper straws and wooden utensils at all locations, which the fast-food chain anticipated would eliminate 900 metric tons of plastic waste annually. The chain will stop offering plastic straws and forks as supplies run out at roughly 2,900 locations nationwide. The change by McDonald's, which comes after Japan enacted a law in April to reduce single-use plastics, widens the restaurant industry's efforts to balance fast, low-cost courtesy, and sustainability.

- Furthermore, in June 2022, Lamipak, one of the industry leaders in aseptic packaging products and solutions, announced the launch of U-shape paper straw solutions for the Indian market. Lamipak intends to deliver beverage companies impacted by the plastic straw ban a swift and reliable solution. The company has a production line for U-shaped paper straws in China and plans to expand production capacity in Indonesia by the third quarter of 2023. When fully launched, both paper straw lines will have a combined capacity of 200 million paper straws per month, with an additional 100 million per month planned for 2023.

- Plastic waste is a significant and persistent environmental problem, prompting governments and businesses to rethink their approaches and implement green initiatives such as recycling and using alternative biodegradable materials. Nestle (Thailand) meets the challenge by making MILO Thailand the first UHT brand to introduce the first flexible paper straws and winning the Green Initiative of the Year-Thailand award at the FMCG Asia Awards 2022. All such initiatives by the companies operating in the region will increase the market growth for paper straws across the region over the forecast period.

Paper Straw Industry Overview

The market for paper straw is quite fragmented. UFlex Limited, Hoffmaster Group Inc., Fuling Global Inc., Canada Brown Eco Products Ltd, and Huhtamaki OYJ are among the major companies. The corporations continue to innovate and form strategic partnerships to maintain their market share.

In April 2022, Ulfex introduced its U-Shape Paper Straw, aimed to produce 100 million straws in the first month and 200 million in the following months. Ulfex also intended to create 2.4 billion straws every year.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of COVID-19 Impact on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Consumer Demand for Eco-Friendly Straws

- 5.1.2 Growing Demand from Asia-Pacific Region

- 5.2 Market Restraints

- 5.2.1 High Cost of Paper Straws and Availability of Substitutes

6 MARKET SEGMENTATION

- 6.1 Material Type

- 6.1.1 Virgin Paper

- 6.1.2 Recycled Paper

- 6.2 By Application

- 6.2.1 Foodservice

- 6.2.2 Households

- 6.2.3 Institutions

- 6.2.4 Other Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles*

- 7.1.1 UFlex Limited

- 7.1.2 Hoffmaster Group Inc.

- 7.1.3 Transcend Packaging Ltd.

- 7.1.4 Huhtamaki OYJ

- 7.1.5 Fuling Global Inc.

- 7.1.6 Soton Daily Necessities Co. Ltd.

- 7.1.7 Tetra Pak International SA

- 7.1.8 Canada Brown Eco Products Ltd.

- 7.1.9 Karat by Lollicup

- 7.1.10 IPI SRL

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

紙吸管市場、份額、尺寸、趨勢、行業分析報告:材料、產品類型、吸管長度、直徑、銷售管道、最終用途、地區、細分市場、預測,2024-2032

紙吸管市場、份額、尺寸、趨勢、行業分析報告:材料、產品類型、吸管長度、直徑、銷售管道、最終用途、地區、細分市場、預測,2024-2032 2024年紙吸管全球市場報告

2024年紙吸管全球市場報告 紙吸管市場規模、佔有率和趨勢分析報告:按材料、按產品類型、按吸管長度、按直徑、按銷售管道、按最終用途、按地區和按細分市場預測,2023-2023年

紙吸管市場規模、佔有率和趨勢分析報告:按材料、按產品類型、按吸管長度、按直徑、按銷售管道、按最終用途、按地區和按細分市場預測,2023-2023年 紙吸管市場 - 按類型(軟性、非軟性)、按材料類型(原生紙、再生紙)、按產品(印刷、非印刷)、按最終用途行業(食品服務、家庭)和預測,2023 年 - 2032

紙吸管市場 - 按類型(軟性、非軟性)、按材料類型(原生紙、再生紙)、按產品(印刷、非印刷)、按最終用途行業(食品服務、家庭)和預測,2023 年 - 2032 全球紙吸管市場規模研究與預測,按材料(原生紙、再生紙)、應用(餐飲服務、家庭、機構)和區域分析,2023-2030

全球紙吸管市場規模研究與預測,按材料(原生紙、再生紙)、應用(餐飲服務、家庭、機構)和區域分析,2023-2030 紙吸管的全球市場規模、佔有率和行業趨勢分析報告:按類型(非軟性、軟性)、最終用途、材料類型(原生紙、再生紙)、產品類型、長度和前景地區. 預測, 2023-2030

紙吸管的全球市場規模、佔有率和行業趨勢分析報告:按類型(非軟性、軟性)、最終用途、材料類型(原生紙、再生紙)、產品類型、長度和前景地區. 預測, 2023-2030 全球紙吸管市場:按類型(柔性,非柔性),材料類型(原生紙,再生紙),產品類型(印刷,未印刷),吸管長度,吸管直徑,用途(食品,服務,家庭),地區到2028

全球紙吸管市場:按類型(柔性,非柔性),材料類型(原生紙,再生紙),產品類型(印刷,未印刷),吸管長度,吸管直徑,用途(食品,服務,家庭),地區到2028 紙吸管市場:按材料(牛皮紙、再生紙)、按產品(非印刷、印刷)、按長度、按分銷管道、按最終用戶 - 2023-2030 年全球預測

紙吸管市場:按材料(牛皮紙、再生紙)、按產品(非印刷、印刷)、按長度、按分銷管道、按最終用戶 - 2023-2030 年全球預測 紙吸管的全球市場

紙吸管的全球市場 全球紙吸管市場-2022-2029

全球紙吸管市場-2022-2029