|

市場調查報告書

商品編碼

1445653

塑膠射出成型:市場佔有率分析、產業趨勢與統計、成長預測 (2024:2029)Plastics Injection Molding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

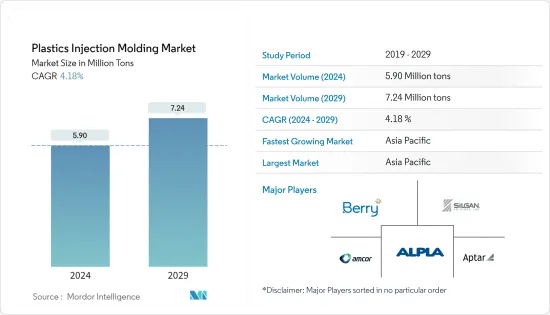

2024年塑膠射出成型市場規模預計為590萬噸,預計到2029年將達到724萬噸,在預測期內(2024-2029年)年複合成長率為4.18%。

儘管在 COVID-19 大流行期間射出成型需求下降,但受訪的市場已穩步復甦並達到疫情前的活動水平。

主要亮點

- 推動市場射出成型需求的主要因素是其在汽車應用中的使用不斷增加以及包裝行業的需求不斷增加。此外,由於對消費品和電子產品的需求增加,預計這種需求將進一步加強。

- 然而,進入射出成型市場的高昂初始成本以及 3D 列印等替代技術和新興技術的普及預計將阻礙市場成長。

- 另一方面,輕型和電動車的製造以及醫療保健領域新應用的轉變可能為塑膠射出成型市場的成長提供利潤豐厚的機會。

- 亞太地區主導全球塑膠射出成型市場,最大的消費來自中國、印度和日本等國家。

塑膠射出成型市場趨勢

主導市場的包裝領域

- 塑膠射出成型提供了許多解決方案,從散裝包裝到薄壁容器和瓶子的模具。這些解決方案廣泛用於各個最終用戶行業的包裝目的。

- 塑膠成型不僅提供了多功能的包裝解決方案,而且還減少了塑膠消費量,並已被證明是經濟和環境原因的理想選擇。

- 世界各地的包裝產業正在迅速發展和擴張。根據包裝加工技術研究所(PMMI)發布的報告,2021年全球包裝產業總產值達422億美元。

- 這一成長主要是由人口成長、永續性問題日益突出、開發中國家可支配收入增加、新興國家零售業成長以及對智慧包裝解決方案需求的增加所推動的。

- 例如,日本是全球最大、成長最快的電子商務市場之一,位居全球第三。預計到2023年,該國將產生約2,322億美元的收入,預計2023年至2028年年均成長率為11.23%。國內電子商務領域的成長預計將增加對包裝解決方案的需求。

- 同樣,美國是零售業的領導者。全球十大零售商中有五家位於美國。根據美國軟包裝協會統計,軟包裝是美國第二大包裝類別,約佔20%的市場。

- 此外,由於該國包裝食品和飲料的消費主義不斷上升,以及 COVID-19感染疾病後外帶外賣的增加,到 2025 年,食品和飲料行業的收益可能會達到 250 億美元。截至2021年,該產業價值約為210億美元,其中食品包裝佔所有軟包裝應用的50%以上。

- 因此,由於上述因素,包裝領域對塑膠射出成型的需求預計將快速成長。

亞太地區主導市場

- 由於中國、印度、日本和韓國等新興經濟體的影響,預計亞太地區將在預測期內主導全球射出成型市場。

- 中國是亞太地區主要經濟體之一。該國的包裝產業預計在未來幾年將出現強勁成長,到 2025 年年複合成長率將達到 6.8% 左右。包裝產業的成長預計將增加該國對塑膠射出成型的需求。

- 同樣,中國汽車產業面臨許多障礙,包括COVID-19感染疾病頻繁復發、半導體晶片短缺以及擾亂供應鏈的地緣政治緊張局勢。

- 根據中國工業協會統計,中國生產汽車2702.1萬輛,銷售汽車2686.4萬輛,與前一年同期比較成長3.4%和2.1%。汽車產業擴大採用塑膠射出成型可能會在預測期內推動所研究市場的需求。

- 此外,國內住宅建築業的成長預計將增加對塑膠射出成型的需求。在 2022-23 年聯邦預算中,印度政府為「PM Aawas 住宅 」計畫撥款 4,800 億印度盧比(64.4 億美元),該計畫旨在建造 800 萬套經濟適用住宅。我們重申了實施承諾。 2022-23 年瞄準都市區貧困階級。

- 亞太地區的電子產業近年來穩步成長,其中中國、印度和日本在市場競爭中處於領先地位。電子情報技術產業協會(JEITA)發布的報告顯示,2021年國內電子產業總產值與前一年同期比較增加近10%。

- 因此,上述因素顯示亞太地區將在預測期內主導全球射出成型市場。

塑膠射出成型產業概況

塑膠射出成型市場分散,主要企業佔據較小的市場佔有率。該市場的主要企業包括 Berry Global Inc.、AptarGroup, Inc.、Silgan Holdings Inc.、Amcor PLC 和 ALPLA。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 包裝產業需求不斷成長

- 消費品和電子產品需求強勁

- 增加在汽車應用的使用

- 抑制因素

- 高進入成本和替代技術的存在

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(市場規模(數量))

- 原料類型

- 聚丙烯

- 丙烯腈丁二烯苯乙烯 (ABS)

- 聚苯乙烯

- 聚乙烯

- 聚氯乙烯(PVC)

- 聚碳酸酯

- 聚醯胺

- 其他原料

- 應用

- 包裝

- 建築與建造

- 消費品

- 電子產品

- 汽車和交通

- 衛生保健

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場排名分析

- 主要企業採取的策略

- 公司簡介

- ALPLA

- Amcor PLC

- AptarGroup Inc.(CSP Technologies)

- BERICAP

- Berry Global Inc.

- EVCO Plastics

- HTI Plastics

- IAC Group

- Magna International

- Quantum Plastics

- Silgan Holdings Inc.

- The Rodon Group

第7章市場機會與未來趨勢

- 輕型汽車和電動車的介紹

- 醫療保健領域的新應用

The Plastics Injection Molding Market size is estimated at 5.90 Million tons in 2024, and is expected to reach 7.24 Million tons by 2029, growing at a CAGR of 4.18% during the forecast period (2024-2029).

Although there was a dip in demand for injection molding during the COVID-19 pandemic, the studied market steadily recovered and reached pre-pandemic activity levels.

Key Highlights

- The major factors driving the demand for injection molding in the market are the increasing usage in automotive applications and the growing demand from the packaging industry. Additionally, increased consumer goods and electronics demand is anticipated to strengthen this demand further.

- However, the high initial costs associated with entering the injection molding market and the strong prevalence of alternative and emerging technologies like 3D printing are expected to hinder the market growth.

- On the flip side, the shift towards manufacturing lightweight and electrified vehicles and the emerging applications in the healthcare sector could open up lucrative opportunities for the growth of the plastics injection molding market.

- The Asia-Pacific region dominated the plastics injection molding market worldwide, with the largest consumption from countries such as China, India, and Japan.

Plastics Injection Molding Market Trends

Packaging Segment to Dominate the Market

- Plastic injection molding offers many solutions, from high-volume packaging to thin-wall containers and bottle molds. These solutions are extensively used in packaging purposes across various end-user industries.

- Besides providing versatile packaging solutions, plastic molding reduces plastic consumption, proving an ideal choice for economical and ecological reasons.

- The packaging industry across the globe is evolving and expanding at a rapid pace. According to a report published by the Association for Packaging and Processing Technologies (PMMI), the total value of the global packaging industry reached USD 42.2 billion in 2021.

- The growth was majorly led by the increasing population, growing sustainability concerns, rising disposable income in developing nations, growing retail sector in emerging economies, and increasing demand for smart packaging solutions.

- For instance, Japan stands in the 3rd position globally as one of the largest and fastest-growing e-commerce markets. The country is anticipated to generate revenue of around USD 232.20 billion by 2023 and is expected to grow at an average annual growth rate of 11.23% between 2023-28. The growing e-commerce sector in the nation is anticipated to strengthen the demand for packaging solutions.

- Similarly, the United States is the foremost company in the retail industry. Out of the top 10 largest retail companies in the world, five of them are based out of the United States. According to the Flexible Packaging Association of the United States, flexible packaging is the second-largest packaging segment in the country, with around 20% share in the market.

- Additionally, with the growing consumerism for packaged food and beverages in the country and the rise in restaurant takeaways in the aftermath of the COVID-19 pandemic, the revenue from the food and beverage industry could reach USD 25 billion by 2025. As of 2021, the industry is valued at around USD 21 billion, with food packaging accounting for over 50% of the total flexible packaging applications.

- Thus, owing to the factors above, the demand for plastic injection molding is anticipated to rise sharply in the packaging segment.

Asia-Pacific Region to Dominate the Market

- Due to emerging economies like China, India, Japan, and South Korea, the Asia-Pacific region is expected to dominate the global plastics injection molding market during the forecast period.

- China is one of the leading economies in the Asia-Pacific region. The packaging industry in the country is anticipated to register strong growth figures in the coming years, registering a CAGR of around 6.8% by 2025. The growth of the packaging industry is anticipated to augment the nation's demand for plastic injection molding.

- Similarly, China's automotive industry experienced growth in 2022, despite facing many obstacles, including the reoccurrence of frequent COVID-19 outbreaks, semiconductor chip shortages, and geopolitical tensions resulting in supply chain disruptions.

- According to China's Association of Automobile Manufacturers, the country recorded production and sales figures of 27.021 million and 26.864 million, respectively, an increase of 3.4% and 2.1% compared to the previous year. The growing adoption of plastic injection molding in the automotive industry could drive demand for the studied market during the forecast period.

- Additionally, demand for plastic injection molding is anticipated to be strengthened by the growing residential construction sector in the country. The Indian government, in its Union Budget 2022-23, allocated INR 48,000 crores (USD 6.44 billion) for its 'PM Aawas Yojana' scheme, reiterating its commitment to implementing 'Housing for All' which aims to build 80,00,000 affordable housing units for the urban and rural poor in FY 2022-23.

- The Asia-Pacific's electronic sector witnessed steady growth in the last several years, with China, India, and Japan leading the market race. According to the report published by the Japan Electronics and Information Technology Industries Association (JEITA), in 2021, the total production value of the electronics industry in Japan showcased a rise of nearly 10% from the previous year.

- Thus, the factors mentioned above indicate the Asia-Pacific region is set to dominate the global plastics injection molding market., during the forecast period.

Plastics Injection Molding Industry Overview

The plastics injection molding market is fragmented, with the top players accounting for a marginal market share. Some of the key companies in the market include Berry Global Inc, AptarGroup, Inc., Silgan Holdings Inc., Amcor PLC, and ALPLA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Packaging Industry

- 4.1.2 Favorable Demand from Consumer Goods and Electronics

- 4.1.3 Increasing Usage in Automotive Applications

- 4.2 Restraints

- 4.2.1 High Entry Cost and Presence of Alternative Technologies

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Raw Material Type

- 5.1.1 Polypropylene

- 5.1.2 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.3 Polystyrene

- 5.1.4 Polyethylene

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Polycarbonate

- 5.1.7 Polyamide

- 5.1.8 Other Raw Materials

- 5.2 Applications

- 5.2.1 Packaging

- 5.2.2 Building and Construction

- 5.2.3 Consumer Goods

- 5.2.4 Electronics

- 5.2.5 Automotive and Transportation

- 5.2.6 Healthcare

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ALPLA

- 6.4.2 Amcor PLC

- 6.4.3 AptarGroup Inc. (CSP Technologies)

- 6.4.4 BERICAP

- 6.4.5 Berry Global Inc.

- 6.4.6 EVCO Plastics

- 6.4.7 HTI Plastics

- 6.4.8 IAC Group

- 6.4.9 Magna International

- 6.4.10 Quantum Plastics

- 6.4.11 Silgan Holdings Inc.

- 6.4.12 The Rodon Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Adoption of Lightweight Vehicles and Electric Vehicles

- 7.2 Emerging Applications in the Healthcare Sector

全球聚合物微注射成型市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球聚合物微注射成型市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 橡膠成型機的全球市場:實際成果·預測 (2019~2030年)

橡膠成型機的全球市場:實際成果·預測 (2019~2030年) 2024 年工業模俱全球市場報告

2024 年工業模俱全球市場報告 到 2030 年冷鐓和冷沖模具市場預測:按類型、材料、最終用戶和地區分類的全球分析

到 2030 年冷鐓和冷沖模具市場預測:按類型、材料、最終用戶和地區分類的全球分析 工業模具市場:按材料、類型和最終用戶分類 - 全球預測 2023-2030

工業模具市場:按材料、類型和最終用戶分類 - 全球預測 2023-2030 全球滾塑產品市場 - 2023-2030

全球滾塑產品市場 - 2023-2030 全球工業模具市場

全球工業模具市場 全球橡膠成型市場

全球橡膠成型市場 全球滾塑市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測

全球滾塑市場研究報告 - 2023 年至 2030 年的行業分析、規模、佔有率、成長、趨勢和預測 塑膠射出成型市場:按原料和用途分類 - 2023 年至 2030 年全球預測

塑膠射出成型市場:按原料和用途分類 - 2023 年至 2030 年全球預測