|

市場調查報告書

商品編碼

1445450

電信 API - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029 年)Telecom API - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

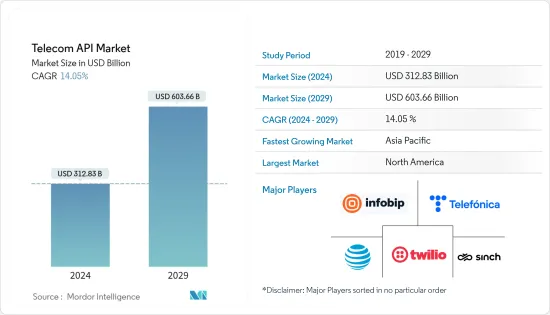

2024年,電信API市場規模預估為3,128.3億美元,預估至2029年將達到6,036.6億美元,在預測期間(2024-2029年)CAGR為14.05%。

主要亮點

- 2022年,北美在電信API市場佔據主導地位,市佔率超過30%,這主要歸功於其早期和廣泛採用API技術。快速的技術創新以及基於雲端的服務在電信領域的日益普及預計將推動電信 API 市場的成長。

- 在過去的幾十年裡,隨著技術的不斷進步和新軟體基礎設施的實施,全球電信業的發展出現了高潮。向數位技術的結構性轉變可能會對電信業的未來產生重大影響。

- 隨著行動服務用戶數量的不斷增加,對基於行動的技術的需求在過去幾年中顯著成長,由於其可擴展性,對電信 API 的需求也隨之增加。簡化的訊息傳遞和語音的整合是可能在預測期內重塑電信產業的主要因素。

- 儘管電信 API 提供了所有好處,但資料安全仍然是一個令人擔憂的問題,其中惡意方的攻擊可能導致他們存取用戶和運行應用程式的裝置的敏感資訊。

- 在新冠肺炎(COVID-19) 全球大流行期間,電信API 供應商一直在透過實施新產品開發、併購和地理擴張等策略來開發能夠應對這種情況的解決方案,以實現更好的可及性。例如,去年 3 月,美國 T-Mobile Venture 投資了電信 API 開發新創公司 signalwire,該公司開發語音、視訊和訊息 API,以推進 API 和 5G 技術等。

電信應用程式介面 (API) 市場趨勢

混合業務部門將持有主要股份

- 旨在連接任何兩個人的通訊目前正在轉向人對機器和機器對機器的連接,以交換各種資料。由於該過程涉及各種類型的資料,因此這種傳輸場景以及不斷增加的主動和被動用戶數量,為一系列通訊協定奠定了基礎。在這個不斷擴大的通訊領域,中間件可以被認為是一組硬體和軟體,用於將不同平台與最終用戶連接起來,最終用戶的數量每天都在增加,可能廣泛用於任何領域。範圍從幾米到幾公里。

- 電信業正從實體網路轉向數位網路。電信業由廣泛的消費者組成,無論他們的設備和位置如何,他們都需要廣泛的服務。為了滿足同樣的需求,電信業者尋求雲端解決方案來提供服務以滿足消費者的需求。

- 對微服務需求的成長可以被視為企業應用程式開發自然演變的標誌。當前的市場狀況正在見證技術趨勢,例如向雲端平台的遷移和向 API 經濟的轉變。基於Web的應用程式可以幫助電信業的服務供應商提高其行動通訊、寬頻服務和開源技術的品質和可靠性,擴大其市場佔有率,並提高其獲利能力。

- 專注於改善客戶體驗,電信業者正在修改其 IT 和網路架構功能中的微服務架構 (MSA),以支援可擴展性和彈性。全球支持性政府法規也鼓勵電信業者透過 API 開放其通訊系統。預計這將促進跨電信業務模式的中間件架構解決方案的成長。

- 行動應用支援環境 (MASE) 是一個分散式系統,可在行動裝置和稱為行動閘道的裝置上運作。後者充當固定和無線網路基礎設施之間的橋樑。它是行動用戶端的代理,通常透過頻寬有限的不可靠無線接取網路進行連結。 MASE 提供對 UMTS 適配層 (UAL) 的訪問,從而允許應用程式和中間件元件統一存取所有可能的底層網路。附加的通用支援層提供分散式系統所需的功能。

- 蜂窩網路技術的發展使用戶能夠體驗更快的資料速度和更低的延遲。它還促使數據密集型服務和應用程式的使用迅速增加。蜂窩網路承載的資料量顯著增加主要是由消費者對視訊和業務的需求以及消費者轉向使用雲端服務所推動的。這一因素預計將推動對提供快速、高容量網路的 5G 連接的需求。此外,隨著未來幾年5G的推出,電信公司預計將渴望專注於邊緣運算解決方案,這將由中介軟體架構供應商提供支援。

北美將佔據主要市場佔有率

- 該地區的主導地位可歸因於最近移動性的增加以及由於 IT 消費化而促使的智慧行動裝置的爆炸式成長,從而幫助電信 API 在該地區成長。

- 此外,隨著對經濟高效且方便用戶使用的基於瀏覽器的通訊解決方案的需求不斷成長,許多知名供應商正在尋求在該地區推出特定於垂直行業的WebRTC和雲端解決方案,預計這將促進市場的成長。

- 該地區包括美國和加拿大。在美國,大量行動網路業者已經在利用電信 API 來支援自動呼叫偵測和騷擾電話管理。其中一些相同的流程和程序將成為物聯網網路身份驗證和授權中介的橋樑。

- 美國因其對5G部署的高投資率而成為5G市場最重要的創新者和投資者之一。該國的電信業佔全球 5G 技術消費的很大一部分。

- 2023年1月,為了創建安全的5G網路切片並增強加拿大的安全和國防,滑鐵盧大學宣布創建「5G and Beyond」行動網路技術合作。該組織已獲得國防部 (DND) 的資助,作為其國防卓越與安全創新 (IDEaS) 計劃的一部分。來自滑鐵盧大學的一群電腦科學家正在領導這個多合作夥伴聯盟。它將花費 150 萬加元(112 萬美元)。

- 在這場危機期間,加拿大的基礎設施電信服務供應商(即建造和營運加拿大電信網路的公司)致力於確保經過多年對網路基礎設施和營運的投資,在面對網路流量增加和變化的情況下,打造出具有極高彈性的網路。隨著使用模式的變化,電信 API 市場正在成長。

電信應用程式介面 (API) 產業概覽

由於 AT&T Inc.、諾基亞公司、Twilio Inc. 和愛立信等主要電信公司的存在,電信 API 市場的競爭非常激烈。由於更高的市場滲透率和強大的創新 API 演算法的部署,尤其是成熟市場參與者的部署,預計競爭的激烈程度在預測期內將顯著增加。

2023 年 8 月,思科宣布有意收購第二工作小組 (WG2),這是一家挪威公司,該公司率先推出了完全 API 可使用且高度可編程的雲端原生行動服務平台。 WG2 的平台專為簡單、創新和高效而構建,採用網路規模的劇本和操作模型,這使其與行動服務平台自然契合。 WG2 的技術和團隊完美地採用了相同的方法:簡化行動網路架構以提供徹底創新的行動服務。借助 WG2 和思科行動服務平台,該公司為應用程式開發合作夥伴、企業客戶和服務供應商合作夥伴推動了服務邊緣部署和 API 優先策略。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業生態系統分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 競爭激烈程度

- 替代產品的威脅

- COVID-19 對產業生態系統的影響

第 5 章:市場動態

- 市場促進因素

- 可擴展性增強,上市時間縮短,營運成本降低

- 中介軟體架構在電信業務模式的擴散

- 市場課題

- API 漏洞不斷增加引發安全性疑慮

第 6 章:電信業的 API 用例

第 7 章:市場區隔

- 依服務類型

- 訊息傳遞API

- IVR/語音儲存與語音控制 API

- 支付介面

- WebRTC(即時連線)API

- 位置和地圖 API

- 訂戶身分管理和 SSO API

- 其他類型的服務

- 依部署類型

- 混合

- 多雲

- 其他部署類型

- 依最終用戶

- 企業開發者

- 內部電信開發商

- 合作夥伴開發者

- 長尾開發者

- 依地理

- 北美洲

- 歐洲

- 亞太地區

- 中國

- 韓國

- 澳洲和紐西蘭

- 印度

- 印尼

- 泰國

- 新加坡

- 馬來西亞

- 亞太地區其他地區

- 拉丁美洲

- 中東和非洲

第 8 章:競爭格局

- 公司簡介

- AT&T Inc.

- Telefonica SA

- Twilio Inc.

- Infobip Ltd

- Sinch (CLX Communication)

- Verizon Communications Inc.

- Orange SA

- Deutsche Telekom AG

- Ribbon Communications

- Huawei Technologies Co. Ltd

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Google LLC (Apigee Corporation)

- Vodafone Group

- Nokia

第 9 章:供應商能力矩陣

第 10 章:主要供應商的關鍵案例研究

第 11 章:投資分析

第 12 章:市場機會與未來趨勢

The Telecom API Market size is estimated at USD 312.83 billion in 2024, and is expected to reach USD 603.66 billion by 2029, growing at a CAGR of 14.05% during the forecast period (2024-2029).

Key Highlights

- North America dominated the Telecom API market in 2022 with a market share of more than 30% which can be attributed mainly to its early and widespread adoption of API technologies. Rapid technological innovations, along with the increasing penetration of cloud-based services across the telecom sector, are expected to drive the growth of the telecom API market.

- Over the past couple of decades, with the ongoing technological advancements and implementation of new software infrastructure, there has been a climacteric rise in the development of the telecommunication sector worldwide. The tectonic shift toward digital technologies will likely substantially impact the telecom sector's future.

- With the increasing number of mobile service subscribers, the demand for mobile-based technologies has grown significantly in past years, increasing the demand for telecom apis due to their scalability. The integration of streamlined messaging and voice is the primary factor that is likely to reshape the telecom industry during the forecast period.

- Despite all the benefits offered by the telecom API, data security remains a concern where-in attacks by malicious parties can lead to them accessing the sensitive information of the users and the devices on which the application is being operated.

- At the time of the COVID-19 pandemic worldwide, telecom API vendors have been developing solutions that can cope with the situation for better accessibility by implementing strategies such as new product developments, mergers & acquisitions, and geographical expansion. For instance, in March last year, U.S.-based T-Mobile Venture invested in telecom API development startup signalwire, which develops voice, video, and messaging apis to advance API and 5G technology, among others.

Telecom Application Programming Interface (API) Market Trends

Hybrid Segment to hold major share

- Communication, which aims to connect any two individuals, is currently shifting toward man-to-machine and machine-to-machine connections for exchanging various sorts of data. Because of the various types of data involved in the process, this transmission scenario, with an ever-increasing number of active and passive users, sets the groundwork for a range of communication protocols. Middleware, in this ever-expanding communication arena, can be thought of as a set of hardware and software that is used to connect different platforms with end-users, who are increasing in number on a daily basis, with a possible widespread use over any region spanning from a few meters to several kilometers.

- The telecommunications sector is significantly transitioning from physical to digital networks. The telecom industry comprises a wide range of consumers that need to be offered a wide spectrum of services, irrespective of their devices and locations. To cater to the same, telecom carriers seek cloud solutions for delivering their services in response to consumer demands.

- This rise in demand for microservices can be considered a sign of the natural evolution of enterprise application development. Technology trends, such as migration to cloud platforms and a shift toward an API economy, are being witnessed in the current market scenario. Web-based applications can help service providers in the telecom industry improve the quality and reliability of their mobile communications, broadband services, and open-source technologies, boost their market share, and improve their profitability.

- Focusing on improving the customer experience, telecommunications players are revising microservices architecture (MSA) in their IT and network architectural capabilities to support extensibility and elasticity. The supportive government regulations worldwide also encourage telecom players to open their communication systems via APIs. This is expected to promote the growth of middleware architecture solutions across telecommunications business models.

- The Mobile Application Support Environment (MASE) is a distributed system that works on both the mobile device and a device known as a mobility gateway. The latter acts as a bridge between fixed and wireless network infrastructures. It is an agent for mobile clients, often linked over unreliable wireless access networks with limited bandwidth. MASE gives access to the UMTS adaption layer (UAL), which allows unified access to all conceivable underlying networks for applications and middleware components. An additional general support layer provides the functionality required for distributed systems.

- The evolution of cellular network technology has allowed users to experience faster data speeds and lower latency. It has also prompted the rapidly increasing use of services and applications that are data-heavy. The significant rise in the volume of data being carried by cellular networks has been primarily driven by consumer demand for video and business and consumer moves to the use of cloud services. This factor is expected to drive the need for a 5G connection that offers fast and high-capacity networks. Moreover, with the introduction of 5G in the coming years, telecom companies are expected to be eager to focus on edge computing solutions, which would be enabled by middleware architecture vendors.

North America to Hold Major Market Share

- The region's dominance can be attributed to the recent increase in mobility and the explosion of smart mobile devices due to the consumerization of IT, thereby helping the Telecom API grow in the region.

- Moreover, with the rising demand for cost-effective and user-friendly browser-based communication solutions, many notable vendors are looking to introduce vertical-specific WebRTC and cloud solutions in the region, which is expected to boost the market's growth.

- The region comprises the United States and Canada. A significant number of mobile network operators are already leveraging telecom APIs to support robocall detection and unwanted call management in the United States. Some of these same processes and procedures will become bridges toward the mediation of LoT network authentication and authorization.

- The US is one of the foremost innovators and investors in the 5G market, owing to its high rate of investment in 5G deployment. The telecom industry in the country accounts for a significant portion of the global consumption of 5G technology.

- In January 2023, to create safe 5G network slicing and enhance Canada's security and defense, the University of Waterloo announced the creation of the "5G and Beyond" mobile network technology collaboration. The organization has received funding from the Department of National Defense (DND) as part of its Innovation for Defense Excellence and Security (IDEaS) program. A group of computer scientists from the University of Waterloo is leading the multi-partner consortium. It will cost CAD 1.5 million (USD 1.12 million).

- During this crisis, Canada's facilities-based telecommunications service providers, the companies that build and operate Canada's telecommunications networks, are focused on ensuring After years of investing in network infrastructure and operations, resulting in incredibly resilient networks in the face of intensified network traffic and altered usage patterns, the telecom API market is growing.

Telecom Application Programming Interface (API) Industry Overview

The intensity of competitive rivalry is high in the telecom API market, owing to the presence of major telecom players such as AT&T Inc., Nokia Corporation, Twilio Inc., and Ericsson. The level of intensity of competitive rivalry is expected to increase significantly over the forecast period, owing to higher market penetration and the deployment of powerful, innovative API algorithms, especially by established market players.

August 2023, Cisco is announcing its intent to acquire Working Group Two (WG2), a Norwegian company that pioneered a cloud-native mobile services platform that's entirely API consumable and highly programmable. Built for simplicity, innovation, and efficiency, WG2's platform uses the web-scale playbook and operating models, which makes it a natural fit with our Mobility Services Platform. WG2's technology and team beautifully align with the same approach: simplifying the Mobile network architecture to deliver a radically innovative mobile service. With WG2 and the Cisco Mobility Services Platform, the company boosts service edge deployment and API first strategy for application development partners, Enterprise customers, and Service Provider partners.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 COVID-19 Impact on the Industry Ecosystem

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growth in Enhanced Scalability and Reduced Time-to-Market along with Decreasing Operational Cost

- 5.1.2 Proliferation of the Middleware Architecture across Telecom's Business Model

- 5.2 Market Challenges

- 5.2.1 Security Concern due to the Increasing API Vulnerabilities

6 API USE CASES IN THE TELECOM INDUSTRY

7 MARKET SEGMENTATION

- 7.1 By Type of Service

- 7.1.1 Messaging API

- 7.1.2 IVR/Voice Store and Voice Control API

- 7.1.3 Payment API

- 7.1.4 WebRTC (Real-Time Connection) API

- 7.1.5 Location and Map API

- 7.1.6 Subscriber Identity Management and SSO API

- 7.1.7 Other Types of Service

- 7.2 By Deployment Type

- 7.2.1 Hybrid

- 7.2.2 Multi-cloud

- 7.2.3 Other Deployment Types

- 7.3 By End-User

- 7.3.1 Enterprise Developer

- 7.3.2 Internal Telecom Developer

- 7.3.3 Partner Developer

- 7.3.4 Long Tail Developer

- 7.4 By Geography

- 7.4.1 North America

- 7.4.2 Europe

- 7.4.3 Asia Pacific

- 7.4.3.1 China

- 7.4.3.2 South Korea

- 7.4.3.3 Australia and New Zeland

- 7.4.3.4 India

- 7.4.3.5 Indonesia

- 7.4.3.6 Thailand

- 7.4.3.7 Singapore

- 7.4.3.8 Malaysia

- 7.4.3.9 Rest of Asia Pacific

- 7.4.4 Latin America

- 7.4.5 Middle East and Africa

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles*

- 8.1.1 AT&T Inc.

- 8.1.2 Telefonica SA

- 8.1.3 Twilio Inc.

- 8.1.4 Infobip Ltd

- 8.1.5 Sinch (CLX Communication)

- 8.1.6 Verizon Communications Inc.

- 8.1.7 Orange SA

- 8.1.8 Deutsche Telekom AG

- 8.1.9 Ribbon Communications

- 8.1.10 Huawei Technologies Co. Ltd

- 8.1.11 Telefonaktiebolaget LM Ericsson

- 8.1.12 Cisco Systems Inc.

- 8.1.13 Google LLC (Apigee Corporation)

- 8.1.14 Vodafone Group

- 8.1.15 Nokia

9 VENDOR CAPABILITY MATRIX

10 KEY CASE STUDIES OF MAJOR VENDORS

11 INVESTMENT ANALYSIS

12 MARKET OPPORTUNITIES AND FUTURE TRENDS

API 整合平台市場:按產品、部署類型、最終用途、組織規模分類 - 2024-2030 年全球預測

API 整合平台市場:按產品、部署類型、最終用途、組織規模分類 - 2024-2030 年全球預測 電信 API 市場:按類型、部署類型、最終用戶分類 - 2024-2030 年全球預測

電信 API 市場:按類型、部署類型、最終用戶分類 - 2024-2030 年全球預測 全球通訊API市場:按API類型、使用者、地區分類 - 到2028年的預測

全球通訊API市場:按API類型、使用者、地區分類 - 到2028年的預測 電信 API 市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

電信 API 市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 全球電信 API 市場

全球電信 API 市場 到2028年的全球電信API市場預測-按服務類型(身份管理API,消息傳遞API,地圖和位置API,語音/語音API,支付API,WebRTC API,其他服務類型),最終用戶,區域另一個分析

到2028年的全球電信API市場預測-按服務類型(身份管理API,消息傳遞API,地圖和位置API,語音/語音API,支付API,WebRTC API,其他服務類型),最終用戶,區域另一個分析 通信API市場規模,份額,趨勢分析報告:按類型(消息傳遞/IVR/支付/位置API),最終用途(企業/合作夥伴開發人員),地區,細分市場預測2023-2030

通信API市場規模,份額,趨勢分析報告:按類型(消息傳遞/IVR/支付/位置API),最終用途(企業/合作夥伴開發人員),地區,細分市場預測2023-2030 全球通信 API 市場:按技術、應用程序、服務類型、利益相關者、用戶類型、部署方法、PaaS 類型分類(2022-2027 年)

全球通信 API 市場:按技術、應用程序、服務類型、利益相關者、用戶類型、部署方法、PaaS 類型分類(2022-2027 年) 電信 API 市場 - 增長、未來展望、競爭分析,2022 年至 2030 年

電信 API 市場 - 增長、未來展望、競爭分析,2022 年至 2030 年 通訊用API的全球市場:預測(2022年~2027年)

通訊用API的全球市場:預測(2022年~2027年)