|

市場調查報告書

商品編碼

1445401

MEMS 壓力感測器:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)MEMS Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

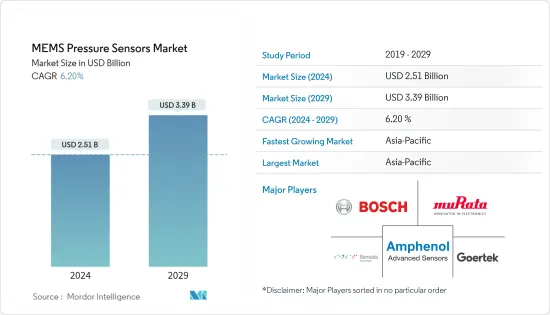

MEMS壓力感測器市場規模預計到2024年為25.1億美元,預計到2029年將達到33.9億美元,在預測期內(2024-2029年)成長6.20%。年複合成長率為

全部區域的工業自動化和小型消費性設備(例如穿戴式裝置和物聯網連接設備)的需求是推動 MEMS 壓力感測器市場的關鍵因素。

主要亮點

- MEMS感測器由於其精度和可靠性等優勢,以及小型電子設備的製造範圍,在過去幾年受到了極大的關注,在各個領域越來越受歡迎。全部區域的工業自動化和小型消費性設備(例如穿戴式裝置和物聯網連接設備)的需求是推動 MEMS 壓力感測器市場的關鍵因素。

- 此外,汽車產業目前正在經歷一場以提高安全性、舒適性和娛樂性為重點的技術轉型,為 MEMS 壓力感測器提供了充足的機會。自動駕駛汽車、無人機和 AR/VR 設備等新興感測器密集型應用進一步增加了對 MEMS 壓力感測器的需求。

- 此外,MEMS 技術可實現小型化、經濟高效且可靠的感測器,其中一些感測器可承受高溫和惡劣環境,從而擴大了半導體裝置的範圍。 MEMS 裝置的多樣性及其製造所涉及的不同技術導致了從設計到測試的複雜但永續的供應鏈。

- 介面在基於感測器的系統設計中引起最嚴重的問題。連接到感測器介面的多個障礙物使設計和製造變得複雜。雖然允許零件在不同的實現之間分離和重複使用是非常有價值的,但它足以使設計和製造變得困難。事實上,在 Fierce Electronics 最近一項關於感測器設計的調查中,超過三分之一的受訪者表示,將感測器涵蓋他們的計劃是最困難的問題。預計這將對市場成長構成挑戰。

- 此外,2020年和2021年,COVID-19大流行襲擊了MEMS壓力感測器市場,導致MEMS壓力感測器略有下降。然而,所研究的市場在 COVID-19感染疾病後可能會成長。放鬆管制導致消費者主要在配備 MEMS 壓力感測器的物聯網設備上做出支出決定。

MEMS壓力感測器市場趨勢

市場驅動的自動化與工業 4.0 的出現

- 支援智慧工業的MEMS的主要特點是精度、可靠性和壽命。在工業4.0中,MEMS感測器可應用於需要振動、溫度、壓力、聲音和聲學分析的早期故障檢測和預測維修系統系統,從而促進其在自動化和工業4.0應用中的使用。

- 隨著工業4.0和物聯網(IoT)的引入為製造業帶來重大變革,企業擴大利用技術透過自動化來補充和增強人力,減少流程故障造成的工傷。採用靈活和創造性的策略來推進我們的業務。由於互聯設備和感測器的普及以及 M2M通訊的加速,製造業產生的資料點數量不斷增加。

- 此外,各行業也擴大採用自動化,也大大增加了人們對工業機器人的興趣。國際機器人聯合會(IFR)預計,2020年全球工業機器人出貨達到約38.4萬台,較2019年略有成長。預計未來幾年工業機器人出貨將快速成長,甚至可能超過2018年的高峰。全球約有 422,000 台工業機器人出貨。預計2024年全球工業機器人出貨將達51.8萬台。

- 工業機器人擴大應用於各個行業。儘管高度自動化的電子機械產業仍然是機電機械最大的市場之一,但電氣和電子產業在 2020 年引入了最多的工業機器人。工業機器人的增加也將增加全球對 MEMS 壓力感測器的需求。

- 此外,據思科稱,到 2022 年,支援物聯網應用的機器對機器 (M2M) 連接預計將佔全球 285 億台連網裝置的一半以上。世界各地的製造商也意識到,下一代機器人和自動化技術是在生產力、品質、安全和成本指標方面升級製造業的革命性機會。此外,機器人自動化支出的與前一年同期比較主要擴大了研究市場的範圍。

亞太地區維持主要市場佔有率

- 亞太地區被稱為製造地,並且正在快速成長。汽車產業需要更多的安全法規。由於智慧型手機、智慧型裝置和電器產品中 MEMS 壓力感測器的普及,消費性電子產業預計將主導區域 MEMS 壓力感測器市場。

- 此外,亞太地區的汽車工業是世界上最大的汽車工業之一,在過去的幾十年中從一個由政府控制的小型產業發展成為由大型跨國公司控制的產業。韓國是起亞汽車、現代汽車、雷諾等大公司的所在地,預計汽車需求將穩定成長。汽車產業的成長預計將增加該地區對 MEMS 壓力感測器的需求。

- MEMS 壓力感測器廣泛應用於汽車產業,目前汽車產業正在經歷技術轉型,其主要目標是提高安全性、舒適性和娛樂性。這些感測器(如 MEMS)由於尺寸小而在汽車行業中需求量很大,這是普及的主要驅動力。

- 由於汽車產業在壓力感測器市場中佔據很大一部分,因此該地區在未來幾年將帶來巨大的機會。 MEMS壓力感測器的採用預計也將受到聯網汽車概念的不斷擴大和中國有關車輛安全的法規的影響。

- 未來幾年,技術的不斷發展、物聯網的大規模採用以及與產品相關的政府法規預計都將促進壓力感測器市場的成長。然而,由於監管障礙較高,壓力感測器市場可能面臨額外的挑戰。

MEMS壓力感測器產業概況

MEMS 壓力感測器市場由許多能夠進行後向整合和向前整合的大型供應商組成,展現出巨大的產生收入能力。市場相對整合,供應商正在增加研發支出,以獲得相對於其他公司的技術力和競爭優勢。市場上的供應商競爭的是技術和質量,而不是價格。市場上競爭公司之間的敵對激烈程度相當高,預計未來幾年將進一步加劇。

- 2022 年 7 月 - Bosch Sensor Tech 宣布其 Edge Impulse 機器學習平台現在支援 Arduino NiclaSense ME 微控制器上的感測器。根據該公司的公告,首款 Arduino Pro 產品是與 Bosch Sensortec 合作創建的,Bosch Sensortec 的感測器利用 BMP390 壓力感測器提供多種高精度資料收集和分析方法。

- 2022 年 2 月 -電子機械系統 (MEMS) 製造商意法半導體發布第三代 MEMS 感測器。新感測器將進一步顯著提高消費性行動裝置、智慧工業、醫療保健和零售業的性能和功能。經銷商很快就能購買採用 2.8mm x 2.8mm x 1.95mm 7 接腳 LGA 封裝的 LPS28DFW 壓力感知器和採用 2.0mm x 2.0mm x 0.73mm 10 接腳 LGA 封裝的 LPS22DF 壓力感知器。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵意強度

- 產業價值鏈分析

- 技術簡介

- 評估 COVID-19感染疾病對市場的影響

- 聚對二甲苯在 MEMS 壓力感測器中的使用概述

第5章市場動態

- 市場促進因素

- 自動化和工業 4.0 的出現

- 對感測器密集型應用的需求不斷成長

- 市場限制因素

- 多個介面的複雜性

第6章市場區隔

- 按用途

- 醫療保健

- 車

- 產業

- 航太和國防

- 家用電器

- 按類型

- 矽壓敏電阻

- 矽電容

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

第7章 競爭形勢

- 公司簡介

- Bosch Sensortec GmbH

- Murata Manufacturing Co. Ltd

- Amphenol Advanced Sensors(Amphenol Corporation)

- Sensata Technologies Inc.

- Goertek INC.

- STMicroelectronics NV

- Omron Corporation

- Alps Alpine Co. Ltd

- Infineon Technologies AG

- TE Connectivity Ltd

- NXP Semiconductors NV(Freescale)

- InvenSense Inc.(TDK Corporation)

- ROHM Co. Ltd

- Honeywell International Inc.

- Melexis

- Vendor Ranking for the Top 5 Vendors Across the End-user Verticals

- 2021年排名前15的供應商市場佔有率

第8章投資分析

第9章市場的未來

The MEMS Pressure Sensors Market size is estimated at USD 2.51 billion in 2024, and is expected to reach USD 3.39 billion by 2029, growing at a CAGR of 6.20% during the forecast period (2024-2029).

Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT-connected devices, are among the significant factors driving the MEMS pressure sensors market.

Key Highlights

- MEMS sensors are gaining popularity across sectors, due to their advantages, such as accuracy and reliability, in addition to the scope for making smaller electronic devices, which have gained significant traction in the past few years. Industrial automation and demand for miniaturized consumer devices across regions, such as wearables and IoT-connected devices, are among the crucial factors driving the MEMS pressure sensors market.

- Also, The automotive industry, which is presently undergoing a technology transition with a significant focus on increasing safety, comfort, and entertainment, provides ample opportunities for MEMS pressure sensors. Emerging sensor-rich applications, such as autonomous vehicles, drones, and AR/VR equipment, further accelerate the need for MEMS pressure sensors.

- In addition, MEMS technologies have enabled miniaturized, cost-effective, and reliable sensors, some of which can withstand high temperatures and harsh environments, expanding the scope of semiconductor devices. Such diversity in MEMS devices and the different technologies involved in their manufacture have led to a complex but sustainable supply chain, from design to testing.

- The interfaces are a source of some of the most severe issues in the design of sensor-based systems. The multiple obstacles connected with sensor interfaces are enough to make design and manufacture complicated. While invaluable for decoupling parts and allowing reuse across different implementations, they are enough to make design and manufacturing difficult. Indeed, more than a third of respondents in a recent Fierce Electronics study on sensor design said that incorporating sensors into a plan is their most demanding issue. This is expected to challenge the market's growth.

- Moreover, the COVID-19 pandemic hurt the MEMS pressure sensors market in 2020 and 2021, which resulted in a slight drop in the MEMS pressure sensors. However, the market studied is likely to grow after the COVID-19 pandemic; the ease of restrictions attracted consumers to make spending decisions on IoT-enabled devices, which mostly come with MEMS pressure sensors.

MEMS Pressure Sensors Market Trends

Emergence of Automation and Industry 4.0 to Drive the Market

- MEMS's key features to support the smart industry are accuracy, reliability, and longevity. For Industry 4.0, MEMS sensors can be applied in early-failure-detection and predictive-maintenance systems where vibration, temperature, pressure, sound, and acoustics analyses are needed, thus, driving its usage in automation and Industry 4.0 applications.

- Massive changes in the manufacturing industry brought by Industry 4.0 and the adoption of IoT demand that businesses adopt flexible and creative strategies to advance production with technologies that complement and augment human labor with automation and lower industrial accidents brought on by process failure. There has been an increase in the number of data points generated in the manufacturing sector as a result of the widespread adoption of connected devices and sensors and the facilitation of M2M communication.

- In addition, the increased adoption of automation across a variety of industries has significantly increased interest in industrial robotics. The International Federation of Robotics (IFR) estimates that industrial robot shipments worldwide reached about 384,000 in 2020, only slightly up from 2019. Industrial robot shipments are anticipated to rise sharply in the years to come, possibly even exceeding the peak year of 2018, when about 422,000 industrial robots were shipped globally. Global shipments of industrial robots are predicted to reach 518,000 units in 2024.

- Industrial robots can be used in a growing number of industries for a variety of tasks. The electrical and electronic industries installed the most industrial robots in 2020, despite the highly automated auto industry continuing to be one of the largest markets for electro-mechanical machines. Such a rise in industrial robots would also boost the demand for MEMS pressure sensors globally.

- Additionally, According to Cisco, by 2022, machine-to-machine (M2M) connections that support IoT applications are expected to account for over half of the world's 28.5 billion connected devices. Manufacturers worldwide also understand that the next generation of robotics and automation technologies is a revolutionary opportunity to upgrade manufacturing in terms of productivity, quality, safety, and cost metrics. Also, increased year-on-year robotic automation expenditure mainly expands the scope of the studied market.

Asia Pacific to Hold Major Market Share

- Asia-Pacific is a well-known manufacturing hub and rapidly growing. There is a need for more safety regulations in the automotive industry. Due to the widespread use of MEMS pressure sensors in smartphones, smart devices, and home electronics, the consumer electronics segment is predicted to dominate the regional MEMS pressure sensor market.

- Additionally, Asia pacific automotive industry is among the largest worldwide, growing from a small government-controlled sector to one controlled by large multinational enterprises over the past few decades. South Korea is home to major players like Kia, Hyundai, and Renault, and it is expected to witness steady growth in the demand for automobiles. Such growth in automobiles will increase demand for MEMS pressure sensors in the region.

- MEMS pressure sensors have a variety of applications in the automotive industry, which is currently undergoing a technological transformation with the primary goal of enhancing safety, comfort, and entertainment. These sensors, like MEMS, are in high demand in the automotive industry due to their small size, which is a key driver of their widespread adoption.

- Since the automotive sector accounts for a sizable portion of the pressure sensor market, the region presents an excellent opportunity over the coming years. The adoption of MEMS pressure sensors is also anticipated to be influenced by the expanding idea of connected cars and Chinese regulations regarding automotive safety.

- In the upcoming years, expanding technological development, IoT adoption on a large scale, pro-product government regulations, and more will all contribute to the growth of the pressure sensors market. However, the market for pressure sensors may face additional challenges due to high regulatory barriers.

MEMS Pressure Sensors Industry Overview

The MEMS pressure sensor market comprises many large-scale vendors capable of both backward and forward integration and commands significant revenue generation capabilities. The market is relatively consolidated, and vendors are increasingly spending on R&D to gain technological capabilities and a competitive edge over other companies. The vendors in the market are competing on technology and quality but not on price. The intensity of competitive rivalry in the market is moderately high and is expected to increase over the coming years.

- July 2022 - Bosch Sensortec announced that Edge Impulse's machine-learning platform supports its sensors on the Arduino NiclaSense ME microcontroller. According to the company's announcement, the first Arduino Pro product was created in association with Bosch Sensortec, in which sensors offered by Bosch Sensortec offer numerous high-accuracy data collection and analysis methods by utilizing the pressure sensor BMP390.

- February 2022 - STMicroelectronics manufacturer of micro-electro-mechanical systems (MEMS), is releasing its third generation of MEMS sensors. The new sensors offer the next jump in performance and features for consumer mobile devices, intelligent industries, healthcare, and retail. Distributors will soon be able to purchase the LPS28DFW pressure sensor in a 2.8mm x 2.8mm x 1.95mm 7-lead LGA and the LPS22DF pressure sensor in a 2.0mm x 2.0mm x 0.73mm 10-lead LGA package.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.5 Assessment of Impact of COVID-19 on the Market

- 4.6 Overview of the Use of Parylene in the MEMS Pressure Sensors

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Emergence of Automation and Industry 4.0

- 5.1.2 Increasing Demand for Sensor-rich Applications

- 5.2 Market Restraints

- 5.2.1 Complexity Regarding Multiple Interface

6 MARKET SEGMENTATION

- 6.1 By Application

- 6.1.1 Medical

- 6.1.2 Automotive

- 6.1.3 Industrial

- 6.1.4 Aerospace and Defense

- 6.1.5 Consumer Electronics

- 6.2 By Type

- 6.2.1 Silicon Piezoresistive

- 6.2.2 Silicon Capacitive

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Bosch Sensortec GmbH

- 7.1.2 Murata Manufacturing Co. Ltd

- 7.1.3 Amphenol Advanced Sensors (Amphenol Corporation)

- 7.1.4 Sensata Technologies Inc.

- 7.1.5 Goertek INC.

- 7.1.6 STMicroelectronics NV

- 7.1.7 Omron Corporation

- 7.1.8 Alps Alpine Co. Ltd

- 7.1.9 Infineon Technologies AG

- 7.1.10 TE Connectivity Ltd

- 7.1.11 NXP Semiconductors NV (Freescale)

- 7.1.12 InvenSense Inc. (TDK Corporation)

- 7.1.13 ROHM Co. Ltd

- 7.1.14 Honeywell International Inc.

- 7.1.15 Melexis

- 7.2 Vendor Ranking for the Top 5 Vendors Across the End-user Verticals

- 7.3 Vendor Market Share for the Top 15 Vendors in 2021

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

MEMS 感測器 - 市場佔有率分析、行業趨勢與統計、成長預測(2024 - 2029 年)

MEMS 感測器 - 市場佔有率分析、行業趨勢與統計、成長預測(2024 - 2029 年) MEMS 感測器市場 - 2018-2028 年按類型、最終用戶產業、地區、競爭分類的全球產業規模、佔有率、趨勢、機會和預測

MEMS 感測器市場 - 2018-2028 年按類型、最終用戶產業、地區、競爭分類的全球產業規模、佔有率、趨勢、機會和預測 MEMS感測器的全球市場 - 預測(~2032年)

MEMS感測器的全球市場 - 預測(~2032年) MEMS 麥克風傳感器的全球市場 - 市場規模、份額、增長分析:按應用、類型、方向性 - 行業預測 (2023-2030)

MEMS 麥克風傳感器的全球市場 - 市場規模、份額、增長分析:按應用、類型、方向性 - 行業預測 (2023-2030) MEMS 組合傳感器全球市場規模研究與預測:按類型、最終用戶和地區分析,2022-2029 年

MEMS 組合傳感器全球市場規模研究與預測:按類型、最終用戶和地區分析,2022-2029 年 MEMS及感測器的全球市場 - 產業趨勢和至2029年的預測

MEMS及感測器的全球市場 - 產業趨勢和至2029年的預測 北美的MEMS及感測器市場 - 產業趨勢和至2029年的預測

北美的MEMS及感測器市場 - 產業趨勢和至2029年的預測