|

市場調查報告書

商品編碼

1444843

粉末冶金:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Powder Metallurgy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

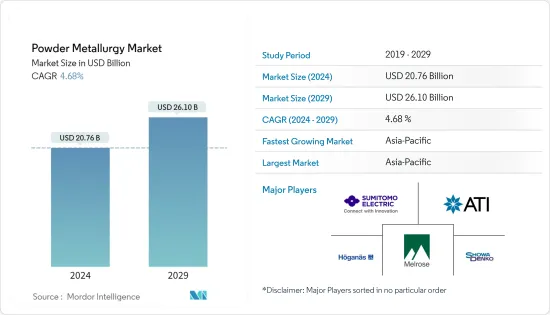

粉末冶金市場規模預計到2024年為207.6億美元,預計到2029年將達到261億美元,在預測期內(2024-2029年)年複合成長率為4.68%。

2020年,COVID-19對市場產生了負面影響。然而,目前估計市場已達到大流行前的水平,並預計將繼續穩定成長。

主要亮點

- 粉末冶金擴大被汽車OEM使用,這是推動市場的關鍵因素之一。

- 另一方面,原料和工具成本的上漲可能會減緩市場成長。

- 未來幾年,粉末冶金技術在醫療領域的廣泛使用預計也將帶來市場機會。

- 亞太地區引領粉末冶金市場,預計未來幾年將呈現最高成長率。

粉末冶金市場趨勢

汽車應用主導市場

- 粉末金屬零件的孔隙率得到良好控制,並且可以自我潤滑,從而能夠過濾氣體和液體。這使得粉末冶金成為製造具有複雜彎曲、凹陷和突出的零件的絕佳方法。

- 能夠靈活開發多種成分的機械零件,例如金屬與非金屬、金屬與金屬的組合,使得製造具有高尺寸精度的汽車零件成為可能,同時最大限度地減少廢料和材料浪費。確保一致的性能和尺寸。

- 軸承和齒輪是採用粉末冶金工藝製造的最常見的汽車零件。這項製程也應用於汽車的許多零件,包括底盤、轉向、排氣、變速箱、避震器零件、引擎、電池、座椅、空氣濾清器和煞車盤。

- 汽車零件由多種金屬製成,包括黑色金屬(鐵、鋼、合金鋼、不銹鋼)和有色金屬(銅、青銅、鋁合金、鈦合金)。粉末冶金著重於淨形狀改善、熱處理和特殊表面處理以提高精度。

- 歐洲汽車工業協會(ACEA)的報告顯示,2022年前三季全球小客車產量約5,000萬輛,較2021年同季成長近9%。

- 中國汽車工業協會也表示,2021年12月至2022年12月,國產新能源汽車保有量成長96.9%。因此,電動車市場的擴張預計將在預測期內增加市場需求。

- 由於這些因素,汽車領域對粉末冶金的需求不斷增加。

亞太地區主導市場

- 亞太地區是最重要的粉末冶金市場之一,也是製造商的首選目的地,因為其經濟不斷成長,人們有更多的錢可以花。

- 近年來,中國、印度和日本等國家的經濟成長趨勢增加了對粉末冶金產品和應用的需求。

- 根據中國工業協會(CAAM)統計,中國擁有全球最大的汽車生產基地。 2022年,中國汽車產量預計將達到2,700萬輛,比2017年的2,600萬輛成長3.4%。

- 此外,2022年1-7月,全國汽車產量1,457萬輛,與前一年同期比較成長31.5%。

- 印度汽車工業商協會(SIAM)也表示,2020-21年(2020年4月-2020年3月)印度汽車工業產量為22,655,609輛,而2021-22年(2021-22年)產量為22,655,609輛。 ( 2022年4月至3月),數量將達22,933,230台。

- 此外,該地區的航太業也在顯著成長。例如,波音公司《2022-2041年商業展望》預計,2041年,中國將新增交付8,485架,市場服務價值達5,450億美元,推動市場成長。

- 因此,由於上述因素,亞太地區很可能在預測期內主導市場。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 汽車原始OEM對粉末冶金的興趣日益濃厚

- 增加電氣和電磁應用的實施

- 抑制因素

- 原料和工具成本增加

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 產品類別

- 鐵

- 有色金屬

- 目的

- 車

- 工業機械

- 電氣和電子

- 航太

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- ATI

- Catalus Corporation

- fine-sinter Co., Ltd.

- HC Starck Tungsten GmbH

- Showa Denko Materials Co., Ltd.

- Hoganas AB

- Horizon Technology

- Melrose Industries PLC

- Miba AG

- Perry Tool &Research, Inc.

- Phoenix Sintered Metals, LLC

- Precision Sintered Parts

- Sandvik AB

- Sumitomo Electric Industries, Ltd.

第7章市場機會與未來趨勢

- P/M 技術在醫療領域的使用增加

The Powder Metallurgy Market size is estimated at USD 20.76 billion in 2024, and is expected to reach USD 26.10 billion by 2029, growing at a CAGR of 4.68% during the forecast period (2024-2029).

In 2020, COVID-19 negatively impacted the market. However, the market has now been estimated to have reached pre-pandemic levels and is expected to grow steadily in the future.

Key Highlights

- Powder metallurgy is being used more and more by automotive OEMs, which is one of the main things driving the market.

- On the other hand, rising costs of raw materials and tools are likely to slow the market's growth.

- In the coming years, market opportunities are also expected to come from the growing use of P/M techniques in the medical field.

- The Asia-Pacific region led the market for powder metallurgy, and it is expected to have the highest growth rate over the next few years.

Powder Metallurgy Market Trends

Automotive Applications to Dominate the Market

- Powder metal parts have great control over how porous they are and can lubricate themselves, which lets them filter gases and liquids.Because of this, powder metallurgy is a very good way to make parts that have complicated bends, depressions, and projections.

- This flexibility to develop mechanical parts with diverse compositions, such as metal-nonmetal and metal-metal combinations, enables the production of automotive parts with high dimensional accuracy and ensures consistent properties and dimensions with very little scrap and material waste.

- Bearings and gears are the most common vehicle parts made through the powder metallurgy process. The process is also used for a large number of parts in a vehicle, including the chassis, steering, exhaust, transmission, shock absorber parts, engine, battery, seats, air cleaners, brake discs, etc.

- Auto parts are made from a wide range of metals, such as ferrous (iron, steel, alloy steel, and stainless steel) and non-ferrous (copper, bronze, aluminum alloys, and titanium alloys).The focus of powder metallurgy is to improve the net shape, utilize heat treatment, provide special surface treatment, and improve precision.

- In the first three quarters of 2022, around 50 million passenger cars were manufactured worldwide, up nearly 9% compared to the same quarter in 2021, as per the report of the European Automobile Manufacturers' Association (ACEA).

- Also, the China Association of Automobile Manufacturing says that the number of New Energy Vehicles made in the country rose by 96.9% from December 2021 to December 2022.Thus, the expanding electric vehicle market is expected to increase market demand during the forecast period.

- Due to such factors, the demand for powder metallurgy in the automotive sector is increasing.

Asia-Pacific to Dominate the Market

- Asia-Pacific has become one of the most important powder metallurgy markets and a top destination for manufacturers because its economy is growing and people have more money to spend.

- The positive economic growth trends in countries such as China, India, and Japan have boosted the demand for powder metallurgy products and applications in recent years.

- China has the largest automotive production base in the world, according to the China Association of Automobile Manufacturers (CAAM). In 2022, 27 million vehicles were expected to be made in China, which is 3.4% more than the 26 million vehicles made in 2017.

- Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% year over year.

- Also, the Society of Indian Automobile Manufacturers (SIAM) said that India's automotive industry will make 22,933,230 vehicles in FY 2021-22 (April 2021-March 2022), compared to 22,655,609 units in FY 2020-21 (April 2020-March 2020).

- Furthermore, the aerospace industry is also growing significantly in the region. For instance, the Boeing Commercial Outlook 2022-2041 predicts that by 2041, 8,485 new deliveries with a market service value of USD 545 billion will take place in China.thus boosting market growth.

- Hence, due to the aforementioned factors, Asia-Pacific is likely to dominate the market during the forecast period.

Powder Metallurgy Industry Overview

The powder metallurgy market is consolidated in nature. Some of the major players in the market include Melrose Industries PLC, Sumitomo Electric Industries, Ltd., Hoganas AB, ATI, and Showa Denko Materials Co., Ltd., among others (in no particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Preference for Powder Metallurgy by Automotive OEMs

- 4.1.2 Growing Implementation in Electrical and Electromagnetic Applications

- 4.2 Restraints

- 4.2.1 Increasing Raw Material and Tooling Costs

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Product Type

- 5.1.1 Ferrous

- 5.1.2 Non-ferrous

- 5.2 Application

- 5.2.1 Automotive

- 5.2.2 Industrial Machinery

- 5.2.3 Electrical and Electronics

- 5.2.4 Aerospace

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 ATI

- 6.4.2 Catalus Corporation

- 6.4.3 fine-sinter Co., Ltd.

- 6.4.4 H.C. Starck Tungsten GmbH

- 6.4.5 Showa Denko Materials Co., Ltd.

- 6.4.6 Hoganas AB

- 6.4.7 Horizon Technology

- 6.4.8 Melrose Industries PLC

- 6.4.9 Miba AG

- 6.4.10 Perry Tool & Research, Inc.

- 6.4.11 Phoenix Sintered Metals, LLC

- 6.4.12 Precision Sintered Parts

- 6.4.13 Sandvik AB

- 6.4.14 Sumitomo Electric Industries, Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Usage of P/M Techniques in Medical Sector

2024 年粉末冶金世界市場報告

2024 年粉末冶金世界市場報告 2024年粉末冶金零件全球市場報告

2024年粉末冶金零件全球市場報告 粉末冶金零件市場報告:2030 年趨勢、預測與競爭分析

粉末冶金零件市場報告:2030 年趨勢、預測與競爭分析 粉末冶金壓機的全球市場:2023年

粉末冶金壓機的全球市場:2023年 粉末冶金市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

粉末冶金市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測 粉末冶金市場:按材料、工藝、用途和最終用途分類 - COVID-19、俄羅斯-烏克蘭衝突和高累積的累積影響 - 2023-2030 年全球預測

粉末冶金市場:按材料、工藝、用途和最終用途分類 - COVID-19、俄羅斯-烏克蘭衝突和高累積的累積影響 - 2023-2030 年全球預測 2023-2030年全球粉末冶金市場規模研究與預測,按產品類型(黑色金屬和有色金屬)、應用(汽車、工業機械、電氣和電子、航太和其他應用)和區域分析

2023-2030年全球粉末冶金市場規模研究與預測,按產品類型(黑色金屬和有色金屬)、應用(汽車、工業機械、電氣和電子、航太和其他應用)和區域分析 金屬粉末射出成型 (MIM) 的全球市場:考察與預測 (到2029年)

金屬粉末射出成型 (MIM) 的全球市場:考察與預測 (到2029年) 粉末冶金市場規模、份額、趨勢分析報告、材料(鈦、鋼)、工藝(MIM、PMHIP)、按應用、用途、2023-2030年地區和細分市場預測

粉末冶金市場規模、份額、趨勢分析報告、材料(鈦、鋼)、工藝(MIM、PMHIP)、按應用、用途、2023-2030年地區和細分市場預測 粉末冶金、粉末注射成型 (PIM)、增材製造 (AM) 和相關市場 - 全球市場、最終用戶、應用:分析和預測 (2021-2027)

粉末冶金、粉末注射成型 (PIM)、增材製造 (AM) 和相關市場 - 全球市場、最終用戶、應用:分析和預測 (2021-2027)