|

市場調查報告書

商品編碼

1444737

資料中心電源 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Data Center Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

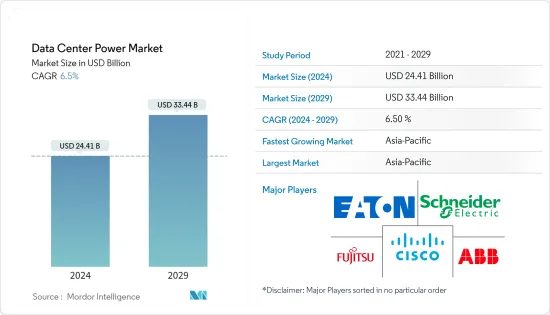

資料中心電力市場規模估計到2024年為 244.1 億美元,預計到2029年將達到 334.4 億美元,在預測期內(2024-2029年)CAGR為 6.5%。

大型資料中心的日益普及推動市場發展。根據位置減少大型資料中心的數量可以使公司享受某些當地優勢,例如低能源價格、有利的氣候或替代能源的可用性。虛擬化大幅提高了硬體利用率,並使公司能夠減少耗電伺服器和儲存設備的數量。

主要亮點

- 雲端運算的日益普及也有助於市場成長,導致大規模超大規模雲端資料中心的興起。例如,2022年10月,Cisco推出了新的共享解決方案,幫助企業、網路規模公司和超大規模公司提供更豐富的雲端應用程式和服務,同時平衡他們對增加頻寬的需求,同時消耗更少的空間和電力。

- 此外,綠地和棕地設施的增加以及模組化資料中心的部署預計將推動對電力系統的需求。邊緣運算的出現和二級資料中心市場不斷擴大的設施推動了對模組化、高效電力基礎設施解決方案的需求。電力成本上升、碳排放以及超大規模營運商整合再生能源的舉措預計將改變市場。設施營運商採用創新、高效的電力基礎設施來減少碳排放和營運成本。

- 全球許多資料中心實施 2N 冗餘 UPS 系統,以應對設施的各種饋電設計和頻繁故障。成本、可靠性、效率和可維護性等因素影響 UPS 系統和發電機在全球市場的採用。

- 智慧機架PDU 解決方案目的是協助在具有大量機架的複雜設施中保持平穩運行。資料中心託管供應商尋找需要更少維護和更少空間且正常運行時間達到99.99%的現代基礎設施解決方案。這些多樣化的需求預計將刺激供應商提供創新的電源解決方案。 PDU 是資料中心電源市場中規模最大、最成熟的產品類別,預計在預測期內將出現更為溫和的成長水準。

- 然而,較高的投資限制了市場的成長,因為主要投資領域是佈線、電力設施和資料中心基礎設施管理(DCIM)解決方案,這些解決方案在初始投資期間需要很高的成本。

資料中心電力市場趨勢

資訊科技領域預計將佔據主要市場佔有率

- IT 產業需要本地私有資料儲存和超大規模資料中心來進行營運,具體取決於組織的規模。此外,由於 SaaS 供應商的成長,雲端儲存的採用率逐年增加,使雲端儲存供應商能夠擴展其容量。因此,不斷增加的資料負載需要更多的電力。這就產生了對 IT 應用中高效能電源解決方案的需求。根據 Vertiv 最近發布的資料中心調查,98%的參與者投票支持到2025年 IT 利用率達到20%以上。這表明 IT 公司重點為資料中心部署高效電源,提高資料中心利用率。

- AWS、微軟和Google等雲端儲存供應商擴展其儲存功能,以在雲端提供更有效率的工作流程。這些公司對超大規模交易進行投資。例如,去年六月,亞馬遜網路服務公司(AWS)宣佈在以色列開設資料中心。該公司的目標是讓該地區更多的開發商、新創公司、企業、政府、教育和非營利組織能夠運行他們的應用程式並從該國的資料中心為最終用戶提供服務。

- 此外,去年11月,AWS 宣布計劃於2023年底或2024年初在加拿大阿爾伯塔省開設基礎設施區域。新的AWS 加拿大西部(卡加利)區域將在啟動時由三個可用區(AZ)組成,並加入位於蒙特婁的現有 AWS 加拿大(中部)區域,該區域也包含三個可用區。新的AWS加拿大西部(卡加利)區域將使更多的開發人員、新創公司、企業、教育、政府和非營利組織能夠從加拿大的資料中心運行他們的應用程式並為最終用戶提供服務。

- 此外,其他公司也在計劃在各個地區擴建資料中心。例如,去年6月,澳洲房地產公司Stockland宣布計劃在雪梨建造新的資料中心。該資料中心的最終價值為 1.81 億美元。此外,還將包括6,300平方公尺的資料大廳、3,215平方公尺的辦公空間以及超過13,000平方公尺的機電服務。預計資料中心產業的此類發展將推動預測期內資料中心電力市場的成長。 SpaceDC、Keppel資料中心和Princeton Digital Group等一些新進業者也採取行動投資超大規模設施和資料中心。

- 儘管該行業迅速採用雲,但對本地和混合資料中心的依賴仍然很大。這些公司嘗試擴大自己的資料儲存容量,預計這需要為資料中心提供高效的電源解決方案。此外,IT產業敏捷和DevOps營運框架的趨勢日益增加對更有效率的資料儲存解決方案的需求。

預計亞太地區市場將出現高速成長

- 根據Cloudscene統計,中國目前擁有447個資料中心和112家服務供應商。大量資料中心的存在推動該國資料中心電力系統的需求。此外,越來越多的新資料中心開發和現有資料中心的升級也預計將推動市場的成長。

- 去年4月,蘋果正式宣佈在中國貴州啟用新資料中心。蘋果公司與雲上貴州大資料產業共同建造了這個資料中心。該國此類新資料中心的發展預計將增加對資料中心電源解決方案的需求。由於大多數資料中心由污染性煤炭提供動力,受影響國家的政府轉向清潔和再生能源。中國的再生能源裝置容量最大,其中太陽能發電量超過 174 吉瓦,風電發電量超過 184 吉瓦。此外,資料中心開發投資的激增預計將推動對資料中心電源解決方案的需求。

- 此外,日本政府還宣布計劃為新的零碳排放資料中心的建築成本提供 50%的補貼,並升級現有設施,作為一項耗資 73 億美元的新行業創新和減少碳排放計劃的一部分。

- 根據 DataSpan 的一項研究,在高達 55%的資料中心中,能源消耗用於運行冷卻和通風系統。因此,為了減少碳排放和資料中心的能源使用量(主要是維持伺服器適合的溫度),日本計劃在較冷的地區建造更多設施。去年 11月,AirTrunk 在日本開設了第一個資料中心,以支持該國越來越多的公司轉向雲端運算。該公司已在印西建設了一個 300 兆瓦的資料中心園區,並將開始營運 60 兆瓦的階段。

- Colt 去年也推出了第三個 Inzai資料中心,這是一個 27 MW 的設施,毗鄰其現有的兩座 Inzai 大樓。因而,預計將為該國資料中心電源解決方案市場創造利潤豐厚的機會。

- 日本對綠色電力有著巨大的推動力,預計將會出現大量目的是改善監管框架以在市場上購買綠色電力的活動。市場供應商尋求與日本綠色能源的第三方供應商合作。 Google、微軟和 Digital Realty 等公司尋找其他公司透過購電協議為再生能源提供資金,以建造太陽能和風電場。

資料中心電力產業概況

資料中心電力市場高度分散,存在多家供應商。參與者採取多種策略,例如併購(M&A)、合作、夥伴關係等。政府機構以及私人資料中心建設採取各種舉措,這造成激烈的競爭。主要參與者有Schneider Electric SE、富士通、Cisco Technology Inc.等。市場的最新發展有:

2022年 10月,數位基礎設施企業 Equinix, Inc. 宣布了一項耗資 7,400 萬美元在雅加達市中心建設國際商業交換(IBX)資料中心的計畫。 Equinix 的發展將使印尼公司以及在印尼開展業務的跨國公司能夠利用其值得信賴的平台來連接和整合推動其企業發展的基礎設施。

2022年 1月,Eaton的 Tripp Lite 推出了用於在工廠和倉庫等要求苛刻的工業環境中連接和控制網路設備的實用選項。新型託管和精簡託管工業十億位元乙太網路交換器具有 IP30 級堅固金屬外殼,可承受工廠車間常見的振動、衝擊以及低溫和高溫。這些開關還提供靜電放電(ESD)保護,靜電放電可能會干擾正常操作。隨附的導軌夾可安裝至標準 35 毫米 DIN 導軌。

附加優惠:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 研究範圍

第2章 研究方法

第3章 執行摘要

第4章 市場動態

- 市場概況

- 市場促進因素

- 大型資料中心和雲端運算的採用不斷增加

- 增加需求以降低營運成本

- 市場限制

- 安裝和維護成本高

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買家的議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭激烈程度

- 評估 COVID-19 對市場的影響

第5章 技術概覽

第6章 市場細分

- 依類型

- 解決方案

- 配電單元

- UPS

- 母線槽

- 其他解決方案

- 服務

- 諮詢

- 系統整合

- 專業服務

- 解決方案

- 依最終用戶應用

- 資訊科技

- 製造業

- BFSI

- 政府

- 電信

- 其他最終用戶應用程式

- 按資料中心規模

- 中小型

- 大型

- 按地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太

- 中國

- 日本

- 澳洲

- 新加坡

- 印度

- 亞太其他地區

- 世界其他地區

- 北美洲

第7章 競爭格局

- 公司簡介

- Schneider Electric SE

- Fujitsu Ltd

- Cisco Technology Inc.

- ABB Ltd

- Eaton Corporation

- Tripp Lite

- Rittal GmbH & Co. KG

- Schleifenbauer

- Vertiv Co.

- Legrand SA

- Black Box Corporation

第8章 投資分析

第9章 市場機會與未來趨勢

The Data Center Power Market size is estimated at USD 24.41 billion in 2024, and is expected to reach USD 33.44 billion by 2029, growing at a CAGR of 6.5% during the forecast period (2024-2029).

The rising adoption of mega data centers is driving the market. Implementing fewer mega data centers depending on their locations can allow a company to enjoy the advantages of certain local benefits, such as low energy prices, a favorable climate, or the availability of alternative energy sources. Virtualization dramatically improves hardware utilization and enables firms to reduce the number of power-consuming servers and storage devices.

Key Highlights

- The rising adoption of cloud computing is also aiding market growth, leading to the rise of vast, hyperscale cloud data centers. For instance, in October 2022, Cisco introduced new shared solutions for assisting businesses, webscale firms, and hyperscale firms in delivering richer cloud applications and services while balancing their need for increased bandwidth while consuming less space and power.

- Further, the increase in greenfield and brownfield facilities, along with the modular data center deployment, is anticipated to drive the demand for power systems. The emergence of edge computing and expanding facilities in the secondary data center market drive the need for modular and efficient power infrastructure solutions. The market is expected to be transformed by rising electricity costs, carbon emissions, and hyperscale operators' initiatives to integrate renewable energy sources.The facility operators are adopting innovative and efficient power infrastructure to reduce carbon emissions and OPEX costs.

- Many data centers around the world are implementing 2N redundant UPS systems to deal with the facility's various feed designs and frequent failure.Factors such as cost, reliability, efficiency, and maintainability impact the adoption of UPS systems and generators in the global market.

- The intelligent rack PDU solutions are made to help keep things running smoothly in complex facilities with a lot of racks.Datacenter colocation providers are looking for modern infrastructure solutions that require less maintenance and less space, with 99.99% uptime. These diverse demands are expected to spur vendors to offer innovative power solutions. PDU is the biggest and most established product category in the data center power market, which is expected to register a much more moderate growth level during the forecast period.

- However, higher investment is restraining market growth as the primary investment areas are cabling, power facilities, and data center infrastructure management (DCIM) solutions, which require high costs during the initial investment.

Data Center Power Market Trends

The Information Technology Segment is Expected to Hold a Major Market Share

- The IT industry requires on-premise private data storage and hyper-scale data centres for its operations, depending on the size of the organization. Additionally, the adoption of cloud storage has increased over the years due to growth among SaaS providers, enabling cloud storage providers to expand their capacities. Hence, the increasing data load requires more power. This creates a requirement for efficient power solutions in IT applications. According to the Data Center Survey recently published by Vertiv, 98% of the participants voted for IT utilization to be above 20% by 2025. This indicates that IT companies are focusing on deploying an efficient power source for their data centres and increasing their utilization rate.

- Cloud storage providers, like AWS, Microsoft, and Google, are expanding their storage capabilities to offer more efficient workflows in the cloud. These companies are making investments in hyperscale deals. For instance, in June last year, Amazon Web Services Inc. (AWS) announced the opening of data centers in Israel. The company aims to enable more developers, startups, enterprises, the government, education, and non-profits in the region to run their applications and serve end-users from data centers in the country.

- Also, in November last year, AWS announced plans to open an infrastructure region in Alberta, Canada, in late 2023 or early 2024. The new AWS Canada West (Calgary) Region will consist of three availability zones (AZs) at launch and join the existing AWS Canada (Central) Region in Montreal, which also consists of three availability zones. The new AWS Canada West (Calgary) Region will enable even more developers, startups, enterprises, education, government, and non-profits to run their applications and serve end-users from data centers in Canada.

- Furthermore, other companies are planning data center expansion in various regions.For instance, in June last year, Stockland, an Australian real-estate firm, announced plans to build a new data center in Sydney. The data center is to have an end value of USD 181 million. Moreover, it will include 6,300 sq m of data halls, 3,215 sq m of office space, and more than 13,000 sq m of electrical and mechanical services. Such developments in the data center industry are anticipated to propel the growth of the data center power market during the forecast period. Some new entrants, like SpaceDC, Keppel Data Centers, and Princeton Digital Group, are also making moves to invest in hyperscale facilities and data center investments.

- Although the industry is rapidly adopting the cloud, the dependency on on-premise and hybrid data centers is still significant. These companies are trying to expand their own data storage capacities, which is expected to demand an efficient power solution for data centers. Moreover, the trend of the IT industry's agile and DevOps operational frameworks is increasing the need for more efficient data storage solutions.

The Asia Pacific Region is Expected to Witness a High Market Growth

- According to Cloudscene, China currently has 447 data centres and 112 service providers. The presence of a large number of data centres is driving the demand for data centre power systems in the country. Furthermore, the increasing number of new data centre developments and the upgrading of existing data centres are also expected to drive the market's growth.

- In April of last year, Apple officially announced the opening of a new data centre in Guizhou, China. Apple and Guizhou-Cloud Big Data Industry Co., Ltd. jointly built this data centre. Such new data centre developments in the country are expected to increase demand for data centre power solutions. As most of the data centres are powered by polluting coal, the governments of the affected countries are shifting toward clean and renewable energy sources. China has installed the most significant amount of renewable energy, with solar power reaching over 174 GW and wind power over 184 GW. Furthermore, the surge in investment in data centre development is expected to fuel the demand for data centre power solutions.

- Further, the Japanese government has announced its plan to subsidize 50% of the building costs for new zero-carbon-emissions data centers and upgrade existing facilities as part of a new USD 7.3 billion initiative to innovate the industry and reduce carbon emissions.

- According to a study by DataSpan, in up to 55% of data centers, energy consumption is used to run cooling and ventilation systems. Thus, to reduce carbon emissions and the amount of energy used by data centers, mainly required to maintain server-suited temperatures, Japan is planning to build more facilities in its colder regions. In November last year, AirTrunk opened its first data center in Japan to support the growing number of companies in the country shifting to the cloud. The company has built a 300MW data center campus in Inzai and is set to begin operations with a 60MW phase.

- Colt also launched its third Inzai data center last year, a 27 MW facility next to its existing two Inzai buildings. In turn, it is expected to create lucrative opportunities for the country's data center power solution market.

- Japan has a tremendous impetus for green power, and a lot of activity toward an improved regulatory framework to buy green power on the market is expected to be witnessed. Market vendors seek to work with third-party providers on green energy in Japan. Players like Google, Microsoft, and Digital Realty are looking for other companies to fund renewable power through power purchase agreements to build solar and wind farms.

Data Center Power Industry Overview

The Data Center Power market is highly fragmented, with multiple vendors present.Players are adopting several strategies, such as mergers and acquisitions (M&A), collaborations, partnerships, etc. Various initiatives are being undertaken by governmental bodies as well as private data center construction, which is creating intense competition. Key players are Schneider Electric SE, Fujitsu Ltd., Cisco Technology Inc., etc. Recent developments in the market are:

In October 2022, Equinix, Inc., a digital infrastructure business, unveiled a plan for a USD 74 million International Business Exchange (IBX) data center in the heart of Jakarta. Equinix's growth will allow Indonesian companies, as well as multinationals with a presence in Indonesia, to utilize their trusted platform to connect together and integrate the foundational infrastructure that will drive their enterprises.

In January 2022, Tripp Lite by Eaton introduced practical options for connecting and controlling network equipment in demanding industrial environments, such as factories and warehouses. The new managed and lite-managed industrial Gigabit Ethernet switches have an IP30-rated ruggedized metal case that can withstand vibration, shock, and the low and high temperatures often found on the factory floor. The switches also offer protection from electrostatic discharge (ESD), which can interfere with normal operation. A rail clip is included to allow mounting to standard 35 mm DIN rail.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mega Data Centers and Cloud Computing

- 4.2.2 Increasing Demand to Reduce Operational Costs

- 4.3 Market Restraints

- 4.3.1 High Cost of Installation and Maintenance

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Assessment of the Impact of COVID-19 on the Market

5 TECHNOLOGY SNAPSHOT

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Solutions

- 6.1.1.1 Power Distribution Unit

- 6.1.1.2 UPS

- 6.1.1.3 Busway

- 6.1.1.4 Other Solutions

- 6.1.2 Services

- 6.1.2.1 Consulting

- 6.1.2.2 System Integration

- 6.1.2.3 Professional Service

- 6.1.1 Solutions

- 6.2 By End-user Application

- 6.2.1 Information Technology

- 6.2.2 Manufacturing

- 6.2.3 BFSI

- 6.2.4 Government

- 6.2.5 Telecom

- 6.2.6 Other End-user Applications

- 6.3 By Data Center Size

- 6.3.1 Small and Medium

- 6.3.2 Large

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 Australia

- 6.4.3.4 Singapore

- 6.4.3.5 India

- 6.4.3.6 Rest of Asia-Pacific

- 6.4.4 Rest of the World

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Schneider Electric SE

- 7.1.2 Fujitsu Ltd

- 7.1.3 Cisco Technology Inc.

- 7.1.4 ABB Ltd

- 7.1.5 Eaton Corporation

- 7.1.6 Tripp Lite

- 7.1.7 Rittal GmbH & Co. KG

- 7.1.8 Schleifenbauer

- 7.1.9 Vertiv Co.

- 7.1.10 Legrand SA

- 7.1.11 Black Box Corporation

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024 年資料中心電源管理全球市場報告

2024 年資料中心電源管理全球市場報告 2024 年全球資料中心電力市場報告

2024 年全球資料中心電力市場報告 資料中心電力市場 - 2024 年至 2029 年預測

資料中心電力市場 - 2024 年至 2029 年預測 資料中心的AC-DC電源的全球市場:實際成果與預測(2019年~2030年)

資料中心的AC-DC電源的全球市場:實際成果與預測(2019年~2030年) 資料中心電力市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按解決方案、組件、最終用戶產業(IT 和電信,BFSI)、地區和競爭細分

資料中心電力市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按解決方案、組件、最終用戶產業(IT 和電信,BFSI)、地區和競爭細分 資料中心電力市場 - 按組件(解決方案、服務)、最終用途(託管、BFSI、能源、政府、醫療保健、製造、IT 和電信),預測 2023 - 2032 年

資料中心電力市場 - 按組件(解決方案、服務)、最終用途(託管、BFSI、能源、政府、醫療保健、製造、IT 和電信),預測 2023 - 2032 年 電源管理解決方案市場 - 2023-2031年全球行業分析、規模、佔有率、成長、趨勢和預測

電源管理解決方案市場 - 2023-2031年全球行業分析、規模、佔有率、成長、趨勢和預測 資料中心電力市場:按產品、解決方案、服務和最終用戶 - 2023-2030 年全球預測

資料中心電力市場:按產品、解決方案、服務和最終用戶 - 2023-2030 年全球預測 數據中心電源市場規模、份額和趨勢分析報告,按產品(UPS、PDU、母線槽)、最終用途(IT/電信、BFSI、零售、政府)、地區(亞太地區、北美)和細分市場預測, 2023-2030

數據中心電源市場規模、份額和趨勢分析報告,按產品(UPS、PDU、母線槽)、最終用途(IT/電信、BFSI、零售、政府)、地區(亞太地區、北美)和細分市場預測, 2023-2030 數據中心電源市場:按組件,按最終用戶,按數據中心規模,按部署類型,按行業(BFSI,IT/電信,媒體/娛樂,醫療保健,其他),按地區-規模,份額,前景,機會分析,2022-2030

數據中心電源市場:按組件,按最終用戶,按數據中心規模,按部署類型,按行業(BFSI,IT/電信,媒體/娛樂,醫療保健,其他),按地區-規模,份額,前景,機會分析,2022-2030