|

市場調查報告書

商品編碼

1444721

自動物料搬運 (AMH) - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029 年)Automated Material Handling (AMH) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

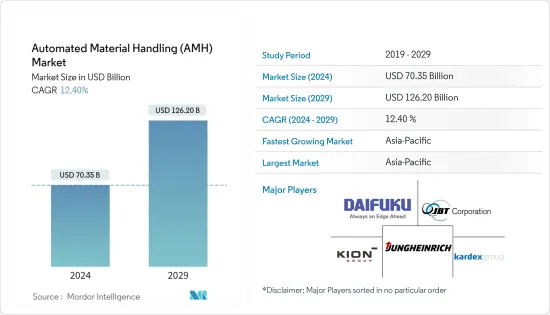

自動化物料搬運市場規模預計到 2024 年為 703.5 億美元,預計到 2029 年將達到 1,262 億美元,在預測期內(2024-2029 年)CAGR為 12.40%。

技術進步不斷進步,勞動力成本和安全問題不斷上升,製造和倉儲營運公司的效率和生產力不斷提高,全球製造業顯著復甦,工業自動化需求不斷成長,製造單位和倉儲設施對機器人的需求不斷成長,新興市場只是推動自動化物料搬運市場成長的幾個關鍵因素。此外,在整個預測期內,全球自動化物料搬運市場將受益於供應鏈營運數位化的不斷擴大。這種擴張將透過增加訂單客製化和個人化來補充。

主要亮點

- 自動物料搬運 (AMH) 系統有助於有效地將物料轉移到製造區域、倉庫、零售店、機場、配送和物流中心的不同地點。這些系統有助於將材料從一個地方轉移到同一車間、製造端對面的部門或兩個獨立建築物之間的另一個地方。 AMH 系統使用製造執行系統 (MES) 提供的路線或路徑。這些車輛使用光學字元辨識(OCR)、條碼、RFID、超寬頻室內追蹤和近場通訊來定位材料的位置來進行材料辨識。

- 在過去的 70 年裡,物料搬運經歷了各種變革,改變了產業的面貌。物料搬運機器和機器人已經取代了個別工人。由於這種轉變,許多行業都得到了成長,特別是汽車產業,成長了10倍。

- 加拿大開發的工業 4.0 創新和下一代製造能力正在改變各種產業和氣候條件下產品和組件的設計、交付和維護方式。機器人、自動化和積層製造(3D 列印)等技術在加拿大各行業有著廣泛的應用,例如電子商務、汽車、農業和製藥。加拿大創新者正在為國內和競爭激烈的全球市場生產各種技術複雜、增值的產品,分享改進的實踐,並為塑造先進自動化技術的未來的合作奠定基礎。

- 儘管第一種形式的 AGV 已於 1953 年使用,但由於多種緩解因素(成本是阻礙成長的重要因素),AGV 基本上無法在所有生產/倉儲公司中廣泛採用。典型導引車的平均價格預計在 60,000-100,000 美元左右。同時,配備導航設備、感測器、安全設備和通訊組件的整合系統可能要昂貴得多。高初始價格和維護問題繼續對所研究的市場產生不利影響。各大公司齊心協力控制總成本,同時確保創新和研發活動不受影響。

- COVID-19 大流行使各行業採用自動化的情況變得更加複雜。它帶來了社交距離和非接觸式操作的獨特課題,改變了標準作業程序。組織被迫限制勞動力並應對不斷成長的需求。自 2020 年以來,COVID-19 疫情已感染美國數名工人,促使第一線公司實施新的安全流程。雖然病毒的傳播已經嚴重到需要關閉食品生產設施等,但透過採取新的衛生措施,許多其他企業已經能夠繼續運作。

自動物料搬運 (AMH) 市場趨勢

工業 4.0 投資顯著推動市場成長

- 該市場是由各國採用工業 4.0 和物聯網技術所帶來的發展所推動的。透過使用機器人技術,工業 4.0 正在徹底改變物料搬運的方式。在倉庫和配送設施中,機器人技術變得越來越普遍。除了揀選和包裝訂單、裝卸卡車,甚至清潔倉庫地板外,他們還可以從事這些活動。機器人技術可以提高工作場所的準確性和生產力。機器人還可以透過減少必要的體力工作量來幫助公司節省金錢。

- 例如,由於倉庫很大,員工必須步行相當長的距離才能找到 SKU 並將訂單交付到包裝和運輸區域。每年,一個倉庫平均浪費 6.9 週的時間在不必要的行走和其他活動上,相當於 2.65 億小時的工作時間,成本達 43 億美元。在選擇過程的每個階段,協作機器人也最大限度地減少了功能區域之間長時間行走的需要。物料搬運設備訂單的增加將顯著推動所研究的市場。

- 此外,機器人、自動化和積層製造(3D列印)等技術在加拿大電子商務、汽車、農業和製藥等行業有著廣泛的應用。加拿大創新者正在為國內和競爭激烈的全球市場生產各種技術複雜、增值的產品,分享改進的實踐,並為塑造先進自動化技術的未來的合作奠定基礎。

- 此外,德國也專注於 2030 年工業 4.0 願景的三個策略行動領域:自主性、互通性和永續性。在這個 2030 年願景中,工業 4.0 平台的利害關係人提出了塑造數位生態系統的整體方法。目標是根據社會市場經濟的要求,創建未來資料經濟的框架,強調開放的生態系統、多樣性,並根據具體情況和德國工業基礎的既定優勢,支持所有市場利益相關者之間的競爭。自動化市場。

- 此外,政府對收購計劃的大力支持使中國能夠邁向工業4.0。例如,中國工業機器人製造商新鬆與中國科學院有聯繫,而中國科學院又與政府有進一步的聯繫。該國各公司採用工業控制系統是一個顯著的趨勢。先進的系統使工廠的生產變得容易。這也顯示公司正逐漸從依賴體力勞動轉向基於先進技術的系統,以實現設施的自動化。

- 影響所研究市場的一個重要趨勢是對智慧製造實踐的關注。 IBEF的資料顯示,印度政府制定了雄心勃勃的目標,即到2025年將製造業產出佔國內生產毛額(GDP)的比重從16%提高到25%。智慧先進製造和快速轉型中心 (SAMARTH) Udyog Bharat 4.0 計畫旨在提高印度製造業對工業 4.0 的認知,並使利益相關者能夠應對與自動化物料搬運相關的課題。

亞太地區預計將成為成長最快的市場

- 中國一直是亞太地區 AMH 市場成長的重要貢獻者。製造業、汽車和電子商務等行業對 AMH 產品的需求不斷成長,推動了市場的成長。中國人口眾多,奉行產業政策。以購買力平價計算,中國在本十年內成為全球最大經濟體、全球最大出口國和貿易國。該國目前正從製造業和建築業主導型經濟轉向消費主導型經濟。

- 根據中國國家統計局的數據,2022年中國消費品市場零售總額約為439,733億元人民幣。中國網路購物者數量從2006年的不到3,400萬人迅速成長到2022年的8.45億人以上,使中國的電子商務成為可能。商貿事業蓬勃發展。因此,隨著電子商務的發展,對物料搬運設備的需求在預測的幾年中可能會增加。

- 日本是一個以製造業為主的國家。其製造業對名目GDP的貢獻接近20%,而其他已開發國家則接近10%。據國際貨幣基金組織稱,由於資訊通訊技術的普及,該國製造業的工業生產率顯著高於服務業。汽車和電子產業是全國生產力最高的製造業。

- 政府基礎設施投資和行業投資的增加以及「印度製造」計劃預計將推動 AMH 系統的需求。印度政府的目標是到2022年將製造業佔國內生產毛額(GDP)的比重從2018年的17%提高到25%。因此,製造商預計將採用工業4.0和其他數位技術來實現這一目標。

- 韓國迎來了第四次工業革命。在韓國,智慧工廠將是最重要的領域之一。 2022年,韓國計劃興建3萬座智慧工廠。韓國政府制定了一項支持計劃,幫助老企業成為碳中和智慧工廠。那些希望將韓國工廠改造為智慧工廠的企業,如果達到中二級水平,將獲得韓國政府36萬美元的財政援助。此外,達到中一級還將獎勵 18 萬美元。這些智慧工廠將是完全整合的自動化系統,將用於製造業。自動化解決方案也將遵循物料搬運和儲存解決方案的自動化,這將推動所研究的市場。

自動物料搬運 (AMH) 產業概述

自動物料搬運 (AMH) 市場本質上競爭非常激烈。產品發布、高額研發費用、合作和收購等是市場主要參與者為維持激烈競爭而採取的主要成長策略。

2022 年 8 月,英特諾在中國成立 20 週年之際在蘇州開設了一家新工廠。在中國物料搬運市場取得二十年的成功之後,英特諾現已為亞太地區和中國的未來機會做好了充分準備,位於中國蘇州的新工廠全面投入營運,有效地將產能加倍。

2022年2月,凱傲集團啟動歐洲研究計畫IMOCO。該項目的目標是促進智慧卡車在倉庫或工廠中自動導航。 IMOCO 代表“智慧運動控制”,致力於在快速移動的內部物流環境中安全使用移動機器人系統。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察

- 市場概況

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 競爭激烈程度

- 替代產品的威脅

- COVID-19 對市場的影響

第 5 章:市場動態

- 市場促進因素

- 漸進的技術進步有助於市場成長

- 工業 4.0 投資推動自動化和物料搬運需求

- 電子商務產業快速發展

- 市場課題

- 初始設備成本高

- 缺乏熟練勞動力

第 6 章:市場區隔

- 依產品類型

- 硬體

- 軟體

- 服務

- 依設備類型

- 移動機器人

- 自動導引車(AGV)

- 自主移動機器人(AMR)

- 自動儲存和檢索系統

- 固定通道

- 輪播

- 垂直升降模組

- 自動輸送機

- 腰帶

- 滾筒

- 托盤

- 高架

- 碼高機

- 傳統的

- 機器人

- 分類系統

- 移動機器人

- 依最終用戶

- 飛機場

- 汽車

- 食品和飲料

- 零售/倉儲/配送中心/物流中心

- 一般製造

- 藥品

- 郵政和包裹

- 其他最終用戶

- 依地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太

- 中國

- 日本

- 印度

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 北美洲

第 7 章:競爭格局

- 公司簡介

- Daifuku Co. Ltd

- Kardex Group

- KION Group AG

- JBT Corporation

- Jungheinrich AG

- TGW Logistics Group GmbH

- SSI Schaefer AG

- KNAPP AG

- Mecalux SA

- System Logistics SpA

- Viastore Systems GmbH

- BEUMER Group GmbH & Co. KG

- Interroll Holding AG

- WITRON Logistik

- Siemens AG

- KUKA AG

- Honeywell Intelligrated Inc. (Honeywell International Inc.)

- Murata Machinery Ltd

- Toyota Industries Corporation

- Visionnav Robotics

- Dearborn Mid-West Company

第 8 章:投資分析

第 9 章:市場的未來

The Automated Material Handling Market size is estimated at USD 70.35 billion in 2024, and is expected to reach USD 126.20 billion by 2029, growing at a CAGR of 12.40% during the forecast period (2024-2029).

The rising technological advancements, rising labor costs and safety concerns, rising efficiency and productivity of manufacturing and warehouse operating companies, a significant recovery in global manufacturing, growing demand for automation in industries, rising demand for robots in manufacturing units and warehousing facilities, and rising emerging markets are just a few of the key factors driving the growth of the automated material handling market. Additionally, throughout the projection period, the global automated material handling market would benefit from the expanding digitization of supply chain operations. This expansion will be complemented by increasing order customization and personalization.

Key Highlights

- Automated material handling (AMH) systems help efficiently transfer materials to different places in the manufacturing area, warehouse, retail shops, airports, distribution, and logistics centers. These systems help transfer materials from one place to another within the same bay, department opposite manufacturing ends, or between two separate buildings. An AMH system uses a route or path provided by the Manufacturing Execution System (MES). Material identification is made by these vehicles using optical character recognition (OCR), barcode, RFID, ultra-wideband indoor tracking, and near-field communication for locating the position of materials.

- Over the last 70 years, material handling has undergone various transformations that have changed the industry's outlook. Material-handling machines and robots have replaced individual workers. Owing to this transformation, many industries have grown, especially the automotive industry, which has experienced a 10-fold growth.

- Industry 4.0 innovations and next-generation manufacturing capabilities developed in Canada are changing the way products and components are designed, delivered, and maintained across various industries and climate conditions. Robotics, automation, and technologies like additive manufacturing (3D printing) have a wide range of applications in Canadian industries, such as e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are producing a comprehensive range of technologically complex, increased-value products for domestic and competitive global markets, sharing enhanced practices and laying the groundwork for collaborations that shape the future of advanced automation technologies.

- Although the first form of AGV was used in 1953, AGVs have been mostly unable to gain widespread adoption across all the production/warehousing firms due to several mitigating factors (cost being a significant factor impeding growth). The average price of a typical guided vehicle is expected to be around USD 60,000-100,000. At the same time, an integrated system equipped with navigation aids, sensors, safety equipment, and communication components could be much more expensive. The high initial prices and maintenance issues continue to have an adverse impact on the market studied. Major companies have concerted efforts to keep the total costs in check while ensuring that innovation and R&D activities remain unaffected.

- The COVID-19 pandemic complicated the situation of automation adoption in various sectors. It has changed the standard operating procedure by bringing in unique challenges of social distancing and contactless operation. Organizations were forced to limit their workforce and deal with the increasing demand. The COVID-19 outbreak has infected several workers in the United States since 2020, leading companies on the front lines to implement new safety processes. While the spread of the virus has been severe enough to warrant shutdowns, for instance, food production facilities, multiple other businesses have been able to continue operations with the addition of new health measures.

Automated Material Handling (AMH) Market Trends

Industry 4.0 Investments Significantly Drive the Market Growth

- The market is driven by the developments occurring due to countries adopting Industry 4.0 and IOT technologies. Through the use of robotics, industry 4.0 is revolutionizing how material handling is done. In warehouses and distribution facilities, robotics is becoming more and more prevalent. In addition to picking and packaging orders, loading and unloading trucks, and even cleaning the warehouse floor, they can also be employed for these activities. Workplace accuracy and productivity can both be enhanced by robotics. Robots can also enable company save money by lowering the quantity of necessary manual work.

- For instance, as warehouses are huge, associates must walk considerable distances to locate SKUs and deliver orders to the packing and shipping regions. Every year, an average warehouse wastes 6.9 weeks on unnecessary walking and other movements, equating to 265 million hours of work at the cost of USD 4.3 billion. During each stage of the selection process, collaborative robots also minimize the need for extended walks between functional areas. The rise in material handling equipment orders will significantly drive the studied market.

- Moreover, robotics, automation, and technologies like additive manufacturing (3D printing) have a wide range of applications in Canadian industries such as e-commerce, automotive, agriculture, and pharmaceuticals. Canadian innovators are producing a comprehensive range of technologically complex, increased-value products for domestic and competitive global markets, sharing enhanced practices and laying the groundwork for collaborations that shape the future of advanced automation technologies.

- Moreover, Germany is also focused on the 2030 vision for Industry 4.0 in three strategic fields of action: Autonomy, Interoperability, and Sustainability. In this 2030 vision, the stakeholders of the platform Industry 4.0 presents a holistic approach to shaping the digital ecosystem. The goal is to create a framework for a future data economy that is by the demands of a social market economy, emphasizing open ecosystems, diversity, and supporting competition between all market stakeholders based on the specific situation and established strengths of the German industry base for the automation market.

- Furthermore, the government's strong support in the acquisition program has enabled China to move toward Industry 4.0. For instance, Siasun, a China-based industrial robot maker, has affiliations with the Chinese Academy of Sciences, which is further linked to the government. The country's adoption of industrial control systems by various companies is a notable trend. The advanced systems allow ease of production in factories. This also points to the gradual shift of companies from depending on manual labor to advanced technology-based systems that will enable the facility's automation.

- A significant trend impacting the market studied is the focus on smart manufacturing practices. According to the data from IBEF, the Government of India set an ambitious target of increasing manufacturing output contribution to 25% of the Gross Domestic Product (GDP) by 2025 from 16%. The Smart Advanced Manufacturing and Rapid Transformation Hub (SAMARTH) Udyog Bharat 4.0 initiative aim to enhance awareness about Industry 4.0 within the Indian manufacturing industry and enable stakeholders to address challenges related to automation material handling.

Asia-Pacific is Expected to be the Fastest Growing Market

- China has been a prominent contributor to the growth of the AMH market in the Asia-Pacific region. The increasing demand for AMH products across industries, such as manufacturing, automotive, and e-commerce, boosts the market's growth. China has a vast population and pursues an industrial policy. Measured on the PPP basis, the country became the global largest economy and the global largest exporter and trader during the current decade. The country is currently transitioning from a manufacturing and construction-led economy to a consumer-led economy.

- According to China's National Bureau of Statistics, total retail sales in China's consumer products market were around CNY 43,973.3 billion in 2022. The number of Chinese online buyers has risen rapidly from under 34 million in 2006 to over 845 million in 2022, enabling China's e-commerce business to proliferate. Hence, with growing e-commerce, the demand for material-handling equipment will likely rise in the forecasted years.

- Japan is predominantly a manufacturing nation. Its manufacturing industry contributes close to 20% to the nominal GDP, whereas it is close to 10% for other developed countries. According to the IMF, the country's manufacturing sector has achieved significant industrial productivity gains over the services sector, owing to the increased adoption of ICT. The automotive and electronics sectors are the most productive manufacturing sectors in the country.

- An increase in infrastructure investment by the government and investments from industries coupled with the 'Make in India' initiative is expected to drive AMH systems' demand. The Government of India aims to increase the manufacturing sector's share of the gross domestic product (GDP) to 25% by 2022, from 17% in 2018. Thus, manufacturers are expected to incorporate Industry 4.0 and other digital technologies to achieve this target.

- South Korea adopted the 4th Industrial Revolution. In Korea, smart factories will be one of the most important fields. By 2022, South Korea plans to construct 30,000 smart factories. The government of South Korea established a support program to help old companies become carbon-neutral smart factories. Those wishing to transform their factories in Korea into smart factories will receive USD 360,000 in financial assistance from the Korean government if they reach medium two levels. In addition, USD 180,000 will be awarded for reaching medium one levels. These Smart Factories will be fully integrated, automated systems that will be employed in manufacturing. The automated solutions will also follow automation for material handling and storage solutions, which will boost the studied market.

Automated Material Handling (AMH) Industry Overview

The automated material handling (AMH) market is highly competitive in nature. Product launches, high expenses on research and development, partnerships and acquisitions, etc., are the prime growth strategies adopted by the key players in the market to sustain the intense competition.

In August 2022, Interroll opened a new plant in Suzhou during its 20th anniversary year in China. After two decades of success in the Chinese material-handling market, Interroll has now fully prepared for future opportunities in the Asia-Pacific and China by putting a new plant in Suzhou, China, into full operation, effectively doubling production capacities.

In February 2022, KION Group launched the European research project IMOCO. The project could aim to facilitate intelligent trucks to navigate autonomously in a warehouse or factory. IMOCO, which stands for 'intelligent motion control,' is devoted to the safe usage of mobile robotic systems in fast-moving intralogistics environments.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitute Products

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Incremental Technological Advancements aiding Market Growth

- 5.1.2 Industry 4.0 Investments driving the Demand for Automation and Material Handling

- 5.1.3 Rapid Growth of E-commerce Sector

- 5.2 Market Challenges

- 5.2.1 High Initial Equipment Cost

- 5.2.2 Unavailability for Skilled Workforce

6 MARKET SEGMENTATION

- 6.1 By Product Type

- 6.1.1 Hardware

- 6.1.2 Software

- 6.1.3 Services

- 6.2 By Equipment Type

- 6.2.1 Mobile Robots

- 6.2.1.1 Automated Guided Vehicle (AGV)

- 6.2.1.2 Autonomous Mobile Robot (AMR)

- 6.2.2 Automated Storage and Retrieval System

- 6.2.2.1 Fixed Aisle

- 6.2.2.2 Carousel

- 6.2.2.3 Vertical Lift Module

- 6.2.3 Automated Conveyor

- 6.2.3.1 Belt

- 6.2.3.2 Roller

- 6.2.3.3 Pallet

- 6.2.3.4 Overhead

- 6.2.4 Palletizer

- 6.2.4.1 Conventional

- 6.2.4.2 Robotic

- 6.2.5 Sortation System

- 6.2.1 Mobile Robots

- 6.3 By End User

- 6.3.1 Airport

- 6.3.2 Automotive

- 6.3.3 Food And Beverages

- 6.3.4 Retail/Warehousing/Distribution Centers/Logistic Centers

- 6.3.5 General Manufacturing

- 6.3.6 Pharmaceuticals

- 6.3.7 Post and Parcel

- 6.3.8 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Spain

- 6.4.2.6 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Rest of Latin America

- 6.4.5 Middle-East and Africa

- 6.4.5.1 United Arab Emirates

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Daifuku Co. Ltd

- 7.1.2 Kardex Group

- 7.1.3 KION Group AG

- 7.1.4 JBT Corporation

- 7.1.5 Jungheinrich AG

- 7.1.6 TGW Logistics Group GmbH

- 7.1.7 SSI Schaefer AG

- 7.1.8 KNAPP AG

- 7.1.9 Mecalux SA

- 7.1.10 System Logistics SpA

- 7.1.11 Viastore Systems GmbH

- 7.1.12 BEUMER Group GmbH & Co. KG

- 7.1.13 Interroll Holding AG

- 7.1.14 WITRON Logistik

- 7.1.15 Siemens AG

- 7.1.16 KUKA AG

- 7.1.17 Honeywell Intelligrated Inc. (Honeywell International Inc.)

- 7.1.18 Murata Machinery Ltd

- 7.1.19 Toyota Industries Corporation

- 7.1.20 Visionnav Robotics

- 7.1.21 Dearborn Mid-West Company

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

自動物料輸送設備市場:按產品、應用和最終用戶分類 - 全球預測 2024-2030

自動物料輸送設備市場:按產品、應用和最終用戶分類 - 全球預測 2024-2030 2024年自動物料輸送設備全球市場報告

2024年自動物料輸送設備全球市場報告 全球物料搬運設備輪胎市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球物料搬運設備輪胎市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 物料搬運設備輪胎市場規模-按輪胎(氣動、實心)、設備(堆高機、輸送機、工業車)、銷售通路(售後市場、 OEM)、最終用戶(倉儲、建築、製造、零售和電子商務)和預測,2024-2032

物料搬運設備輪胎市場規模-按輪胎(氣動、實心)、設備(堆高機、輸送機、工業車)、銷售通路(售後市場、 OEM)、最終用戶(倉儲、建築、製造、零售和電子商務)和預測,2024-2032 自動化物料輸送市場:按組件、操作、設備類型和應用分類 - 2024-2030 年全球預測

自動化物料輸送市場:按組件、操作、設備類型和應用分類 - 2024-2030 年全球預測 全球自動化物料搬運設備市場(2016-2030):按產品類型、系統類型、最終用戶產業和地區劃分的機會和預測

全球自動化物料搬運設備市場(2016-2030):按產品類型、系統類型、最終用戶產業和地區劃分的機會和預測 自動化物料搬運設備市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

自動化物料搬運設備市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 到 2030 年靈活交通系統的市場預測:按類型、應用和地區分類的全球分析

到 2030 年靈活交通系統的市場預測:按類型、應用和地區分類的全球分析 自動化物料搬運設備的全球市場

自動化物料搬運設備的全球市場 自動物料搬運全球市場 2023-2027

自動物料搬運全球市場 2023-2027