|

市場調查報告書

商品編碼

1444716

生質乙醇:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Bioethanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

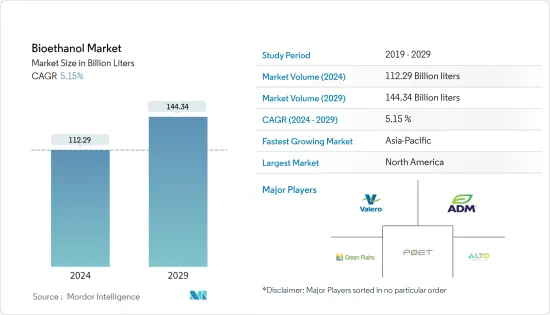

2024年生質乙醇市場規模預估為1,122.9億公升,預估至2029年將達到1,443.4億公升,預測期間(2024-2029年)年複合成長率為5.15%。

由於供應鏈中斷,生質乙醇市場受到了 COVID-19 疾病的負面影響。然而,市場在2021年開始復甦。推動市場的主要因素是美國政府加強並收緊對高乙醇含量汽油銷售的限制。

短期內,越來越多的有利措施、監管機構的指令組合以及對石化燃料使用和生質燃料需求的環境擔憂日益增加將是推動市場成長的因素。

由於電動車需求不斷成長,逐步淘汰燃油汽車以及將重點轉向生物丁醇是阻礙市場成長的因素。

第二代生質乙醇生產的發展以及航空業生質乙醇等生質燃料消費量的增加可能為未來的市場創造機會。

北美主導全球市場,其中美國佔最大的消費量。

生質乙醇市場趨勢

增加在汽車和運輸領域的使用

生質乙醇最廣泛的用途是作為汽車和運輸業的燃料和燃料添加劑。它與傳統汽油一起為道路車輛的汽油引擎提供燃料。我們也可以生產 ETBE(乙基叔丁基醚),這是一種用於多種汽油的辛烷值改良劑。

將生質乙醇與傳統燃料混合可再生。 E10 Energy因含有10%乙醇而得名。生質乙醇是一種低碳燃料,有潛力幫助運輸產業脫碳。

過去30年來,美國一直為使用生質乙醇作為辛烷值改進劑和氣體增量劑的汽油經銷商提供稅收優惠。這導致該領域生質乙醇的使用增加。

美國生質燃料生產商得到了更新立法的推動,其中包括為低碳燃料生產提供資金和大量稅額扣抵。已撥款 5 億美元,透過安裝乙醇和生物柴油混合物的儲存槽和相關設備來改善生質燃料基礎設施。

根據OICA資料,2022年整體汽車產量較2021年成長6%。 2022年全球汽車產量約8,502萬輛。

亞洲大洋洲地區及美洲地區2022年汽車產量分別為5,002萬輛及1,775萬輛,較2020年分別成長近7%及10%。然而,2022年歐洲汽車產量為1621萬輛。比 2021 年產量減少 1%。

此外,美國能源局將於2021年啟動一項研發計劃,致力於生產低成本生質燃料,作為飛機等大型運輸工具的石化燃料替代品,以加強美國實現淨能源目標的承諾。將提供6,470萬美元的資金。 - 到 2050 年實現零排放。

由於各國已宣布計劃增加生質乙醇的消費量可能會激增。

北美地區佔據市場主導地位

北美地區在生質乙醇市場佔有率佔據主導地位。美國是世界上最大的生質乙醇生產國,其次是巴西、中國、印度和加拿大。它也是生質乙醇的最大消費國。

近年來,由於可再生燃料標準(RFS)目標的提高以及國內汽車汽油消費量的增加,生質乙醇產量有所增加,而且現在幾乎全部與10%體積的乙醇混合。

2021年,北美汽車總產量約為13,427,869輛,而2020年為13,374,404輛。

日本 2.63 億輛註冊車輛中約 93% 可能使用 E15。此外,美國大約有 2,200 萬輛靈活燃料汽車 (FFV) 可以使用最高 E85 的乙醇混合物。

加拿大的無污染燃料標準要求液體燃料(汽油、柴油、家用暖氣油)供應商隨著時間的推移逐步降低其生產和銷售在加拿大使用的燃料的碳強度,這也降低了液體燃料的碳強度。到 2030 年,加拿大將使用約 13%(低於 2016 年的水平)。

加拿大政府最近向低碳和零排放燃料基金投資15億美元的措施可能會得到加強,該基金將支持當地生產和採用低碳燃料,如氫和生質燃料。

由於上述所有因素,北美地區對所研究市場的需求預計將會增加。

生質乙醇產業概況

生質乙醇市場有適度分散。市場主要參與者包括(排名不分先後)POET LLC、Valero、ADM、Green Plains Inc.、Alto Elements Inc.等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 積極措施的增加和監管授權的融合

- 由於石化燃料的使用和對生質燃料的需求,環境問題日益嚴重

- 抑制因素

- 由於電動車需求不斷成長,逐步淘汰燃油汽車

- 將焦點轉向生物丁醇

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(市場規模(數量))

- 原料類型

- 甘蔗

- 玉米

- 小麥

- 其他原料類型

- 目的

- 汽車和交通

- 食品和飲料

- 藥品

- 化妝品和個人護理

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- Abengoa

- ADM

- Alto Ingredients Inc.

- Blue Bio Fuels Inc.

- Cenovus Inc.

- Cristalco

- Cropenergies AG

- Ethanol Technologies

- Granbio Investimentos SA

- Green Plains Inc

- Henan Tianguan Group Co. Ltd

- Jilin Fuel Ethanol Co. Ltd

- KWST

- Lantmannen

- Poet LLC

- Raizen

- Sekab

- Suncor Energy Inc.

- Tereos

- Valero

- Verbio Vereinigte Bioenergie AG

第7章市場機會與未來趨勢

- 第二代生質乙醇生產技術開發

- 航空業生質燃料消費量增加

The Bioethanol Market size is estimated at 112.29 Billion liters in 2024, and is expected to reach 144.34 Billion liters by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

The Bioethanol Market was adversely affected by COVID-19 due to disruptions in the supply chain. However, the market rebounded in 2021. The major factors driving the market were the increasing government initiatives and the increased restrictions on marketing gasoline containing a higher percentage of ethanol in the United States.

Over the short term, increasing favorable initiatives, blending mandates by regulatory bodies, and rising environmental concerns about the use of fossil fuels and the need for biofuels are the factors driving the market's growth.

Phasing out of fuel-based vehicles due to rising demand for electric cars and shifting focus to bio-butanol are the factors hindering the market's growth.

Developing second-generation bio-ethanol production and increasing consumption of biofuels like bioethanol in the aviation industry is likely to create opportunities for the market in the future.

North America dominated the global market, with the United States having the most significant consumption.

Bioethanol Market Trends

Increasing Usage in the Automotive and Transportation Sector

The most extensive bioethanol applications are fuel and fuel additives in the automotive and transportation industries. It is used alongside conventional petrol to fuel petrol engines in road vehicles. It can also produce ETBE (ethyl-tertiary-butyl-ether), an octane booster used in many types of petrol.

Blending bioethanol with conventional fuels improves its renewability. E10 energy is so named because it contains 10% ethanol. Bioethanol is a low-carbon fuel that may help to decarbonize the transport industry.

In the United States, tax incentives have been provided to gasoline marketers for using bio-ethanol as an octane enhancer and gas extender over the past three decades. This has driven boosted the usage of bio-ethanol in this sector.

Biofuel producers in the United States received a boost from the latest legislation, which encompasses funding and critical tax credits for producing low-carbon fuels. Funding of USD 500 million was allocated for biofuel infrastructure improvements by installing storage tanks and related equipment for ethanol-biodiesel blends.

In 2022, according to OICA data, the overall production of automobiles increased by 6% compared to 2021. The global automotive production in 2022 was around 85.02 million units.

The Asia-Oceania and Americas regions recorded automotive production of 50.02 million and 17.75 million units in 2022, registering an increase of nearly 7% and 10%, respectively, compared to 2020. However, Europe recorded a production of 16.21 million units in 2022, a decrease of 1% from the production achieved in 2021.

Furthermore, in 2021, the United States Department of Energy announced to provide USD 64.7 million in funds for research and development projects dedicated to producing low-cost biofuels as fossil-fuel replacements for heavy-duty transportation like airplanes to bolster America's commitment to reaching net-zero emissions by 2050.

With various economies announcing their plans to increase bio-ethanol consumption in fuels, the demand for bio-ethanol will likely surge during the forecast period.

North America Region to Dominate the Market

The North American region is dominating the bioethanol market share. The United States is the largest producer of bioethanol globally, followed by Brazil, China, India, and Canada. It is also the largest consumer of bioethanol.

In recent years, bioethanol production increased due to higher renewable fuel standard (RFS) targets and growth in domestic motor gasoline consumption, almost all of which is now blended with 10% ethanol by volume.

In 2021, the overall production of automobiles in North America was around 13,427,869 units compared to 13,374,404 units in 2020.

Around 93% of the country's 263 million registered automobiles may operate on E15. Furthermore, around 22 million flex-fuel vehicles (FFVs) in the United States can run on ethanol blends up to E85.

The Canadian Clean Fuel Standard requires liquid fuel (gasoline, diesel, and home heating oil) suppliers to gradually reduce the carbon intensity of the fuels they produce and sell for use in Canada over time, resulting in a reduction in the carbon intensity of liquid fuels used in Canada of approximately 13% (below 2016 levels) by 2030.

Some initiatives include the Canadian government's recent USD 1.5 billion investment in a Low-carbon and Zero-Emissions Fuels Fund, which may enhance support for local production and adoption of low-carbon fuels like hydrogen and biofuels.

Due to all the factors mentioned above, the demand in the market studied is expected to increase in the North American region.

Bioethanol Industry Overview

The Bioethanol Market is moderately fragmented. Some major players in the market include POET LLC, Valero, ADM, Green Plains Inc., and Alto Ingredients Inc., among others (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Favorable Initiatives and Blending Mandates by Regulatory Bodies

- 4.1.2 Rising Environmental Concerns by the Use of Fossil Fuels and Need for the Bio-fuels

- 4.2 Restraints

- 4.2.1 Phasing out of Fuel-based Vehicles Due to Rising Demand for Electric Vehicles

- 4.2.2 Shifting Focus to Bio-butanol

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Feedstock Type

- 5.1.1 Sugarcane

- 5.1.2 Corn

- 5.1.3 Wheat

- 5.1.4 Other Feedstock Types

- 5.2 Application

- 5.2.1 Automotive and Transportation

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceutical

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Abengoa

- 6.4.2 ADM

- 6.4.3 Alto Ingredients Inc.

- 6.4.4 Blue Bio Fuels Inc.

- 6.4.5 Cenovus Inc.

- 6.4.6 Cristalco

- 6.4.7 Cropenergies AG

- 6.4.8 Ethanol Technologies

- 6.4.9 Granbio Investimentos SA

- 6.4.10 Green Plains Inc

- 6.4.11 Henan Tianguan Group Co. Ltd

- 6.4.12 Jilin Fuel Ethanol Co. Ltd

- 6.4.13 KWST

- 6.4.14 Lantmannen

- 6.4.15 Poet LLC

- 6.4.16 Raizen

- 6.4.17 Sekab

- 6.4.18 Suncor Energy Inc.

- 6.4.19 Tereos

- 6.4.20 Valero

- 6.4.21 Verbio Vereinigte Bioenergie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Second-generation Bio-ethanol Production

- 7.2 Increasing Consumption of Bio-fuels in the Aviation Industry

生物乙醇市場,按原料、按燃料生成、按混合物、按應用和按地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測

生物乙醇市場,按原料、按燃料生成、按混合物、按應用和按地區 - 2024-2032 年行業分析、市場規模、市場佔有率和預測 2024 年生質乙醇酵母全球市場報告

2024 年生質乙醇酵母全球市場報告 2024 年生質乙醇全球市場報告

2024 年生質乙醇全球市場報告 生物丁醇市場報告:2030 年趨勢、預測與競爭分析

生物丁醇市場報告:2030 年趨勢、預測與競爭分析 運輸級生質乙醇市場:依原料、混合物分類 - 2024-2030 年全球預測

運輸級生質乙醇市場:依原料、混合物分類 - 2024-2030 年全球預測 生物丁醇市場:按原料、包裝和應用分類 - 2024-2030 年全球預測

生物丁醇市場:按原料、包裝和應用分類 - 2024-2030 年全球預測 生物乙醇市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

生物乙醇市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 生物丁醇市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

生物丁醇市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 全球生物乙醇酵母市場規模研究與預測,依產品種類(麵包、啤酒)、應用(清潔與消毒、生質燃料、食品、動物飼料等)及區域分析,2023-2030年

全球生物乙醇酵母市場規模研究與預測,依產品種類(麵包、啤酒)、應用(清潔與消毒、生質燃料、食品、動物飼料等)及區域分析,2023-2030年 全球生物乙醇市場按原材料(澱粉基、糖基□□、纖維素基)、燃料混合物和用途行業劃分、按燃料發電量和地區劃分的未來預測(直到2028年)

全球生物乙醇市場按原材料(澱粉基、糖基□□、纖維素基)、燃料混合物和用途行業劃分、按燃料發電量和地區劃分的未來預測(直到2028年)