|

市場調查報告書

商品編碼

1444473

Quartz - 市佔率分析、產業趨勢與統計、成長預測(2024 - 2029)Quartz - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

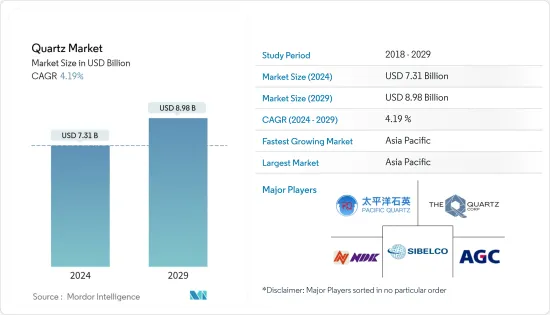

2024年石英市場規模預計為73.1億美元,預計到2029年將達到89.8億美元,在預測期內(2024-2029年)CAGR為4.19%。

COVID-19 大流行導致全球多個行業的供應鏈停止,包括電子和半導體、建築和汽車。因而,這對這些產業對石英的需求產生了不利影響。太陽能的使用量增加,但僅此一項並不能提振市場。 COVID-19 大流行影響了全球建築業,計畫面臨勞動力短缺、供應鏈問題和融資壓力。其影響波及整個產業,從最初的中國危機到世界各地的建築工地。然而,隨著全球大多數國家解除封鎖,大多數產業恢復生產,市場已經復甦。

主要亮點

- 從中期來看,推動市場成長的主要因素是半導體產業對高純度石英的需求,以及不斷成長的太陽能產業。

- 石英開採的生態影響,加上石英磚和石英板的變色,預計將阻礙市場在預測時間內的成長。

- 由於其獨特的性能,石英粉的新興應用可以為市場帶來機會。

- 亞太地區主導全球市場,其中中國的消費量最大。

石英市場趨勢

電子和半導體產業需求不斷成長

- 石英因其高度穩定、高性能的諧振器而在電子行業中使用,進一步用於濾波器和振盪器。石英具有多種適用於電子工業的特性,包括壓電特性,其熔點高於 1700°C,固化溫度為 573°C。

- 電子業對石英的需求不斷增加。這是因為它在手機、平板電腦、筆記型電腦和桌上型電腦等設備中的使用量不斷增加。

- 此外,石英晶體也用作收音機、手錶和壓力表中的振盪器。石英晶體也用於製造各種產品的電子電路中的頻率濾波器、頻率控制器和計時器,例如通訊設備、電腦、電子遊戲機和電視接收器。

- 幾十年來,美國公司在生產為現代技術提供動力的微型半導體晶片方面一直處於世界領先地位。根據半導體產業協會(SIA)統計,美國半導體產業佔全球半導體市場的47%,為全球第一大佔有率。

- 半導體製造商正計劃在該國投資,預計這將有助於市場成長。例如,2021年 3月,英特爾在新墨西哥州工廠投資 35 億美元,用於生產幾乎所有現代設備中使用的微型微晶片,因為這些設備的需求不斷成長。

- 物聯網(IoT)等數位技術和 5G 等最新通訊技術預計將有助於開發創新的消費性電子產品。根據 JEITA 公佈的資料,2022年全球電子產品產量較2020年大幅成長。

- 受此因素影響,電子產業對石英的需求預計將快速成長。

亞太地區將主導市場

- 中國是亞太地區主要國家之一,建築活動豐富。該國的工業和建築業預計將佔GDP的50%左右。

- 根據住房和城鄉建設部的預測,到2025年,中國建築業佔國內生產總值的比重預計將保持在6%。根據上述預測,中國政府公佈了五年計劃2022年1月的計劃重點是使建築業更加永續和品質驅動。

- 由於中美之間的關稅戰,電子產品供應鏈在疫情爆發前就已經處於中斷的陣痛之中。它迫使一些知名電子製造商從中國遷往東南亞,包括GoPro、京瓷和任天堂,將製造業務轉移到越南、卡西歐、大金和理光,並將業務轉移到泰國。

- 為了受益於廣泛的需求場景,中國啟動了「中國製造2025」等戰略舉措,中國政府宣佈到2030年實現產值3050億美元,滿足80%的國內需求。

- 印度的數位視覺是一個巨大的機會,具有巨大的經濟價值。透過實施目前計畫的 30 個數位主題,預計到2022年印度經濟將產生超過 1 兆美元的收入。隨著電子設備製造生態系的增加,印度半導體和電子市場的成長幅度極高。

- 根據韓國科學技術通訊部發布的產業展望,2021年電子元件產值較2020年成長12.5%。該成長的推動因素是資料中心、邊緣運算(IoT)、汽車和 5G 智慧型手機對半導體記憶體的持續需求,以及電視和行動裝置對 OLED 面板需求的飆升。

- 越南的電子工業(EI)是該國成長最快、最重要的產業之一。中美貿易戰和中國製造成本上升使越南電子產業受益匪淺。它佔據了中國電子產業遷移中最重要的佔有率之一。菲律賓的半導體工業和電子工業是該國製造業最重要的貢獻者。而印尼的電子工業主要服務於當地工業,出口很少。

- 預計這些因素將在預測期內增加石英的需求。

石英行業概況

石英市場本質上是分散的。一些重要的參與者包括AGC Inc.、Nihon Dempa Kogyo、Quartz Corporation、Sibelco和Jiangsu Pacific Quartz Co.。

附加優惠:

- Excel 格式的市場估算(ME)表

- 3 個月的分析師支持

目錄

第1章 簡介

- 研究假設

- 研究範圍

第2章 研究方法

第3章 執行摘要

第4章 市場動態

- 促進要素

- 不斷發展的太陽能產業

- 半導體產業對高純度石英的需求

- 限制

- 石英開採的生態影響

- 石英磚和石英板的變色

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章 市場區隔(市場價值規模)

- 類型

- 高純度石英

- 石英石表面和瓷磚

- 熔融石英坩堝

- 石英玻璃

- 石英晶體

- 金屬矽

- 高純度石英

- 最終用戶產業

- 電子和半導體

- 太陽的

- 建築物和建築

- 光纖和電信

- 汽車

- 其他最終用戶產業

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第6章 競爭格局

- 併購、合資、合作與協議

- 市場排名分析

- 領先企業採取的策略

- 公司簡介

- AGC Inc.

- Beijing Kai de Quartz Co. Ltd

- Dow

- Elkem ASA

- Ferroglobe

- Heraeus Holding

- Jiangsu Pacific Quartz Co. Ltd

- Wonic QnC Corporation

- Nihon Dempa Kogyo Co. Ltd

- Nordic Mining ASA

- RUSNANO Group

- Saint-Gobain

- Sibelco

- SUMCO Corporation

- The Quartz Corporation

第7章 市場機會與未來趨勢

- 石英粉因其獨特的性能而出現新興應用

The Quartz Market size is estimated at USD 7.31 billion in 2024, and is expected to reach USD 8.98 billion by 2029, growing at a CAGR of 4.19% during the forecast period (2024-2029).

The COVID-19 pandemic halted the supply chain of several industries worldwide, including electronics and semiconductors, building and construction, and automotive. It, in turn, adversely affected the demand for quartz in these industries. Solar power usage increased, but this alone could not lift the market back. The COVID-19 pandemic impacted the global construction industry, with projects facing labor shortages, supply chain issues, and financing pressures. The effects rippled across the sector, from the initial crisis in China to construction sites worldwide. However, as the lockdowns were lifted in most countries worldwide, the market has recovered due to production resumed in most industries.

Key Highlights

- Over the mid-term, the primary factor driving the market's growth is the demand for high-purity quartz in the semiconductor industry, coupled with the growing solar industry.

- The ecological impact of quartz mining, coupled with discoloration in quartz tiles and slabs, is anticipated to hinder the market's growth during the forecast timeframe.

- Due to its unique properties, emerging applications of quartz powder can act as an opportunity for the market.

- Asia-Pacific dominated the global market, with the most significant consumption in China.

Quartz Market Trends

Rising Demand from the Electronics and Semiconductor Industry

- Quartz is used within the electronics industry for its highly stable, high-performance resonators for further use in filters and oscillators. Quartz possesses various properties for the electronics industry, including piezoelectric properties, as its melting point is above 1700º C and its curing temperature is 573º C.

- There is an increasing demand for quartz from the electronics industry. It is because of its growing usage in devices, such as mobile phones, tablets, laptops, and desktops.

- Additionally, quartz crystal is used as an oscillator in radios, watches, and pressure gauges. Quartz crystal is also used to make frequency filters, frequency controls, and timers in electronic circuits for various products, such as communication equipment, computers, electronic games, and television receivers.

- For decades, companies in the United States have led the world to produce tiny semiconductor chips that power modern technologies. According to Semiconductor Industry Association (SIA), the semiconductor industry in the United States accounts for 47% of the global semiconductor market, which is the largest share in the world.

- The semiconductor manufacturers are planning to invest in the country, which is anticipated to contribute to market growth. For instance, in March 2021, Intel invested USD 3.5 billion in its New Mexico plant to manufacture tiny microchips used in nearly all modern devices, as their demand is increasing.

- Digital technologies such as the internet of things (IoT) and the latest communication technologies, such as 5G, are expected to aid in developing innovative consumer electronic products. As per data published by JEITA, global electronics production increased significantly in 2022 compared to 2020.

- Owing to such factors, the demand for quartz is expected to witness rapid growth in the electronics industry.

Asia-Pacific Region to Dominate the Market

- China is one of the major countries in the Asia-Pacific region, with ample construction activities. The country's industrial and construction sectors are expected to account for approximately 50% of the GDP.

- As per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025. Keeping in view the given forecasts, the Chinese government unveiled a five-year plan in January 2022 focused on making the construction sector more sustainable and quality-driven.

- The electronics supply chain was already in the throes of disruption before the outbreak due to the tariff war between the US and China. It forced the relocation of some high-profile electronics manufacturers from China to Southeast Asia, including GoPro, Kyocera, and Nintendo, moving manufacturing to Vietnam, Casio, Daikin, and Ricoh, and shifting operations to Thailand.

- To benefit from the extensive demand scenario, China embarked on strategic initiatives like the "Made in China 2025" plan, under which the Chinese government announced its goal to reach an output of USD 305 billion by 2030 and meet 80% of its domestic demand.

- The digital vision in India is a vast opportunity and includes significant economic value. The Indian economy is expected to generate revenue of more than USD 1 trillion by 2022 by implementing the 30 digital themes that are currently planned. With the increase in electronic device manufacturing ecosystems, the growth scope of the semiconductors and electronics market in India is extremely high.

- According to the industrial outlook released by South Korea's Ministry of Science and ICT, electronic component production in value grew by 12.5% in 2021 compared to 2020 values. This growth is driven by the continuous demand for semiconductor memory for data centers, edge computing (IoT), automobiles, and 5G smartphones, as well as soaring demand for OLED panels for TV and mobile devices.

- Vietnam's electronics industry (EI) is one of the country's fastest-growing and most important industries. The US-China trade war and rising manufacturing costs in China have hugely benefited the Vietnam electronics industry. It captured one of China's most significant shares of electronic industry migration. The Philippines' semiconductor industry, coupled with the electronics industry, is the most critical contributor to the manufacturing sector within the country. While the electronics industry in Indonesia primarily serves the local industry with very little export.

- Such factors are expected to increase the demand for quartz during the forecast period.

Quartz Industry Overview

The quartz market is fragmented in nature. Some significant players include AGC Inc., Nihon Dempa Kogyo Co. Ltd, Quartz Corporation, Sibelco, and Jiangsu Pacific Quartz Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Solar Industry

- 4.1.2 Demand for High-purity Quartz in the Semiconductor Industry

- 4.2 Restraints

- 4.2.1 Ecological Impact of Quartz Mining

- 4.2.2 Discoloration in Quartz Tiles and Slabs

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 High-purity Quartz

- 5.1.1.1 Quartz Surface and Tile

- 5.1.1.2 Fused Quartz Crucible

- 5.1.1.3 Quartz Glass

- 5.1.2 Quartz Crystal

- 5.1.3 Silicon Metal

- 5.1.1 High-purity Quartz

- 5.2 End-user Industry

- 5.2.1 Electronics and Semiconductor

- 5.2.2 Solar

- 5.2.3 Buildings and Construction

- 5.2.4 Optical fiber and Telecommunication

- 5.2.5 Automotive

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East & Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East & Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AGC Inc.

- 6.4.2 Beijing Kai de Quartz Co. Ltd

- 6.4.3 Dow

- 6.4.4 Elkem ASA

- 6.4.5 Ferroglobe

- 6.4.6 Heraeus Holding

- 6.4.7 Jiangsu Pacific Quartz Co. Ltd

- 6.4.8 Wonic QnC Corporation

- 6.4.9 Nihon Dempa Kogyo Co. Ltd

- 6.4.10 Nordic Mining ASA

- 6.4.11 RUSNANO Group

- 6.4.12 Saint-Gobain

- 6.4.13 Sibelco

- 6.4.14 SUMCO Corporation

- 6.4.15 The Quartz Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Emerging Applications of Quartz Powder due to its Unique Properties

2024-2032 年按產品、最終用戶和地區分類的石英市場報告

2024-2032 年按產品、最終用戶和地區分類的石英市場報告 2024 年石英世界市場報告

2024 年石英世界市場報告 到 2030 年石英整流器市場預測:按類型、蒸餾類型、材料、應用、最終用戶和地區進行全球分析

到 2030 年石英整流器市場預測:按類型、蒸餾類型、材料、應用、最終用戶和地區進行全球分析 全球石英設備零件市場分析(2023-2024年)

全球石英設備零件市場分析(2023-2024年) UVC 照明用高純度石英砂市場(應用:空氣處理、表面消毒、水消毒等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測

UVC 照明用高純度石英砂市場(應用:空氣處理、表面消毒、水消毒等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢和預測 半導體合成石英錠的全球市場的考察,預測(~2029年)

半導體合成石英錠的全球市場的考察,預測(~2029年) 光學石英市場報告:2030 年趨勢、預測與競爭分析

光學石英市場報告:2030 年趨勢、預測與競爭分析 透明石英管全球市場2023-2027

透明石英管全球市場2023-2027 石英坩堝的全球市場:實際成果與預測(2018年~2029年)

石英坩堝的全球市場:實際成果與預測(2018年~2029年) 2023-2030 年全球石英市場規模研究與預測(按類型、最終用戶行業和區域分析)

2023-2030 年全球石英市場規模研究與預測(按類型、最終用戶行業和區域分析)