|

市場調查報告書

商品編碼

1444455

全球工業潤滑油市場:市場佔有率分析、產業趨勢/統計、成長預測(2024-2029)Industrial Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

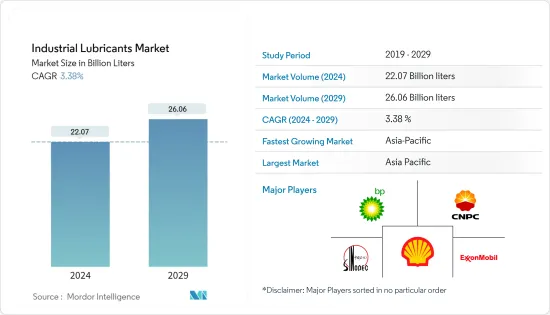

據預測,2024年全球工業潤滑油市場規模將達到220.7億公升,2024-2029年預測期間年複合成長率為3.38%,到2029年將達到260.6億公升。

2020 年的市場受到了 COVID-19 的負面影響。然而,疫情對工業活動中的自動化流程產生了大規模的正面影響。由於大流行而導致的勞動力供應有限、工作場所保持安全距離的需要以及各種個人防護設備的使用正在加速各行業自動化的採用。此外,生產率的提高也增加了機器的運作時間和設備速度,增加了承載能力設備適當潤滑的重要性,增加了所研究市場的需求。

主要亮點

- 短期內,風力發電產業需求的增加預計將推動市場成長。

- 然而,潤滑油對環境的負面影響可能會阻礙所研究市場的成長。

- 然而,生物潤滑劑的日益突出和低黏度潤滑劑的開發可能成為研究市場的成長機會。

- 亞太地區主導全球市場,大部分消費來自中國、印度和印尼等國家。

工業潤滑油市場趨勢

發電業主導市場

- 發電是全球經濟最重要的部門之一,沒有發電,幾乎所有製造業務都可能停止。製造技術的進步使各種新工廠運作,增加了各個最終用戶行業的電力需求。

- 渦輪機在發電能源領域發揮重要作用。渦輪機廣泛用於發電,無論電力源為何,例如風能、太陽能、水力發電或火力發電。在發電過程中,渦輪機釋放大量的熱。一般來說,除了渦輪機外,發電領域使用的主要零件還包括泵浦、軸承、風扇、壓縮機、齒輪和液壓系統。風力發電機受到許多因素的影響,例如濕度、高壓、高負載、振動和溫度。齒輪油和透平油廣泛用於該領域的潤滑目的。

- 許多公司已經意識到,降低機器生命週期內的總擁有成本 (TCO) 是從投資中獲得最大價值的關鍵。然而,潤滑對 TCO 的影響常常被低估。

- 通常,潤滑油成本佔發電公司總營運費用的比例不到 5%。根據一項行業調查,大約 58% 的公司認知到他們選擇的潤滑劑可以節省 5% 或更多的成本,但他們認知到潤滑劑的影響可能高達 6 倍。不到十分之一的公司( 8%) 有

- 在水力發電中,潤滑油用於空氣壓縮機、齒輪、渦輪機、循環油系統、液壓設備、軸承等。消耗的潤滑油包括潤滑脂、一般潤滑油、傳動油、透平油、液壓油等。在核能發電廠中,潤滑油(透平油)主要用於蒸氣渦輪以提高效率。

- 燃煤發電廠的空氣壓縮機、油壓設備、渦輪機、移動設備、軸承、齒輪等都使用潤滑油。煤炭挖土機系統還消耗各種類型的潤滑油,如齒輪油、潤滑脂、變速箱油、液壓油等。燃煤發電廠消耗高溫、耐用的潤滑油。

- 因此,所有這些因素和趨勢預計將在全球經濟從疫情中復甦後推動潤滑油的需求。

亞太地區主導市場

- 由於中國、印度和印尼等國家消費量的增加,亞太地區已成為鋰消費的主要市場。

- 目前,中國已成為最大的潤滑油和潤滑脂消費國。涉及各行業的大規模製造活動以及工業和汽車行業的快速成長使該國成為形勢領先的潤滑油消費國和生產國之一。

- 2021年,中國經濟高層批准了90個固定資產投資計劃,為促進發展做出了貢獻。 2021年,發改委核准投資計劃1,220億美元,主要投向交通、能源、節水、資訊科技等領域。根據最新統計,2021年中國固定資產投資超過54.45兆元(約7.68兆美元),與前一年同期比較增4.9%,較2019年同期成長8%。隨著2021年及以後財政和金融支持的增加,該國有潛力和獎勵擴大有效投資。

- 此外,中國正在重點發展新型基礎設施,在不久的將來,新基礎設施的建設將佔固定資產的大部分。由於支出增加和政府對基礎設施發展的關注,預計未來建設活動將繼續成長。

- 中國工業協會公佈的數據顯示,2021年汽車累計產量2,608.2萬輛,與前一年同期比較增加3.4%。中國汽車工業協會預測,2022年及以後汽車市場可能會持續保持穩定成長。

- 印度是該地區第二大潤滑油消費國,也是僅次於美國和中國的世界第三大潤滑油消費國。該國約佔全球潤滑油市場需求的 7%。雖然工業潤滑油市場本質上是分散的,但印度潤滑脂市場本質上是高度一體化的,排名前五的公司佔據了75%以上的市場佔有率。

- 有利的政府政策,例如將 FAME-II 計劃延長至 2024 年、加強對兩輪車的獎勵以及針對汽車和汽車零部件行業推出生產連結獎勵計畫(PLI) 計劃(價值 2600 億盧比)(約 PLI)盧比的先進化學電池。

- 印尼(世界第四人口大國)由於人口眾多、都市化程度高、中產階級迅速崛起,近年來成為潛在的潤滑油市場之一。近年來,採礦、紡織和基礎設施等產業的工業潤滑油消耗量不斷增加。

- 根據印尼食品和飲料企業家協會 (GAPMMI) 預測,到 2021 年,食品和飲料產業預計將成長 7%。據印尼統計局Badan Pusat Statistik稱,大中型製造業產出為負值。 2021年成長率為8.01%。

- 印尼政府計劃在2024年投資約4,120億美元用於建設計劃,包括興建25個機場和住宅。此類投資是政府加強國家成長目標的一部分。然而,供應鏈中斷預計將在短期內擾亂該行業最初預期的成長途徑。

- 因此,所有上述因素都可能對未來所研究的市場產生重大影響。

工業潤滑油產業概況

全球工業潤滑油市場本質上是分散的。市場主要企業包括荷蘭皇家殼牌公司、埃克森美孚公司、中國石油化學股份有限公司、中國石油天然氣集團公司、英國石油公司(嘉實多)等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 風力發電產業的需求不斷增加

- 其他司機

- 抑制因素

- 潤滑油對環境的負面影響

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 產品類別

- 機油

- 變速箱/液壓油

- 金屬加工液

- 一般工業油

- 齒輪油

- 潤滑脂

- 加工油

- 其他產品類型

- 最終用戶產業

- 發電

- 重型機械

- 食品與飲品

- 冶金/金屬加工

- 化學製造

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 菲律賓

- 印尼

- 馬來西亞

- 泰國

- 越南

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美其他地區

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 土耳其

- 西班牙

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 南美洲其他地區

- 中東

- 沙烏地阿拉伯

- 伊朗

- 伊拉克

- 阿拉伯聯合大公國

- 科威特

- 其他中東地區

- 非洲

- 埃及

- 南非

- 奈及利亞

- 阿爾及利亞

- 摩洛哥

- 其他非洲

- 亞太地區

第6章 競爭形勢

- 合併、收購、合資、合作和協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- Amsoil Inc.

- Bharat Petroleum Corporation Limited

- Blaser Swisslube AG

- BP PLC(Castrol)

- Carl Bechem GmbH

- Chevron Corporation

- China National Petroleum Corporation(PetroChina)

- China Petroleum &Chemical Corporation(SINOPEC Group)

- Eni SpA

- Exxon Mobil Corporation

- FUCHS

- Gazprom Neft PJSC

- Gulf Oil International

- HPCL

- Idemitsu Kosan Co. Ltd

- Indian Oil Corporation Ltd

- ITW(ROCOL)

- ENEOS

- Kluber Lubrication

- Lukoil Lubricants Company

- PT Pertamina

- Petrobras

- Petronas Lubricants International

- Phillips 66 Lubricants

- Repsol

- Royal Dutch Shell PLC

- Tide Water Oil Co.(India)Ltd

- TotalEnergies

- Valvoline Inc.

第7章市場機會與未來趨勢

- 生物潤滑劑日益受到關注

- 低黏度潤滑油的開發

The Industrial Lubricants Market size is estimated at 22.07 Billion liters in 2024, and is expected to reach 26.06 Billion liters by 2029, growing at a CAGR of 3.38% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. However, the pandemic has affected the automation process in industrial activities on a large scale in a positive way. The limited availability of manpower due to the pandemic, the need to keep a safe distance in working places, and the use of various personal protective equipment have accelerated the adoption of automation throughout industries. Moreover, the increase in productivity has also increased the run time of the machinery and the speed of the equipment, which has increased the importance of adequate lubrication on the load-bearing surfaces of the equipment, thus enhancing the demand for the studied market.

Key Highlights

- Over the short term, increasing demand from the wind energy sector is expected to drive the market's growth.

- However, the detrimental effects of lubricants on the environment are likely to hinder the growth of the market studied.

- Nevertheless, the growing prominence of bio-lubricants and the development of low-viscosity lubricants are likely to act as opportunities for the growth of the market studied.

- Asia-Pacific dominates the market across the world, with the most substantial consumption from countries like China, India, and Indonesia.

Industrial Lubricants Market Trends

Power Generation Segment Dominated the Market

- Power generation is one of the most important sectors of the global economy, without which almost all manufacturing operations may cease. Advancements in manufacturing technologies are resulting in the commencement of various new plants, increasing the demand for electricity in various end-user industries.

- Turbines play a key role in the energy sector for generating electricity. Irrespective of the source of electricity, i.e., wind, solar, hydro, thermal, and others, turbines are widely used for power generation. A large amount of heat is emitted from a turbine during the production of electricity. In general, other than turbines, the major components used in the power generation sector include pumps, bearings, fans, compressors, gears, and hydraulic systems. Wind turbines are subjected to many factors, such as humidity, high pressure, high loads, vibrations, and temperature. Gear and turbine oils are widely used in this sector for lubrication purposes.

- Many companies are already aware of the fact that reducing the total cost of ownership (TCO) over the lifetime of machinery is key to extracting the best possible value from the investment. However, the impact of lubrication on the TCO is underestimated too often.

- In general, the cost of lubricants accounts for less than 5% of a power generation company's total operational expenditure. According to an industry survey, about 58% of the companies recognized that lubricant selection could help reduce costs by 5% or more, but fewer than 1 in 10 (8%) companies realized that the impact of lubrication could be up to six times more.

- In hydroelectric power generation, lubricants are used for air compressors, gears, turbines, circulating oil systems, hydraulics, and bearings, among other purposes. The lubricants consumed include greases, general lubricating oils, transmission oils, turbine oils, and hydraulic oils, among others. In nuclear power plants, lubricants (turbine oils) are used mainly for steam turbines for better efficiency.

- In coal-fired power plants, lubricants are used for air compressors, hydraulics, turbines, mobile equipment, bearings, and gears. Coal excavator systems also consume different types of lubricants, including gear oils, greases, transmission oils, and hydraulic oils. Coal-fired power plants consume high-temperature and heavy-duty lubricants.

- Hence, all such factors and trends are expected to drive the demand for lubricants, post the global economic recovery from the pandemic.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific was found to be the major market for the consumption of lithium, owing to increasing consumption from countries such as China, India, and Indonesia.

- China is the largest consumer of lubricants and greases in the current scenario. The vast manufacturing activities pertaining to different sectors and the rapid growth in the industrial and automotive sectors have pushed the country to stand among the major lubricant consumers and producers in the global landscape.

- In 2021, China's top economic planner sanctioned 90 fixed-asset investment projects, helping increase development. In 2021, the National Development and Reform Commission approved USD 122 billion in investment projects, mostly in the transportation, energy, water conservation, and information technology sectors. According to the current statistics, China's fixed-asset investment increased by 4.9% Y-o-Y to over CNY 54.45 trillion (~USD 7.68 trillion) in 2021, up 8% from the same period in 2019. With enhanced fiscal and monetary support beyond 2021, the country has the potential and incentive to expand effective investments.

- In addition, China has been focusing on new infrastructure, with construction being the majority type of fixed assets, in the near future. Such growth in construction activity is expected to be witnessed in the future, owing to increased expenditure and the government's focus on infrastructure growth.

- The China Association of Automobile Manufacturers (CAAM) reported cumulative motor vehicle production levels for 2021, which were 26.082 million units, up by 3.4% Y-o-Y. CAAM predicts the motor vehicle market may continue to record steady growth in 2022 and beyond.

- India is the second-largest lubricant consumer in the region and the third-largest in the world, after the United States and China. The country accounts for about 7% of the demand in the global lubricants market. While the industrial lubricants market is fragmented in nature, the Indian grease market is highly consolidated in nature, with the top five players accounting for more than 75% of the market share.

- Favorable government policies, such as the extension of the FAME-II scheme until 2024, the enhancement of incentives for two-wheelers, the launch of the production-linked incentive (PLI) scheme for the auto and auto component sector (worth INR 26,000 crore (~USD 3.20 billion)), and the PLI for advanced chemistry cell worth INR 18,000 crore (~USD 2.22 trillion), are likely to provide significant support to the sector as it adopts advanced technologies.

- Indonesia (the world's fourth-largest populated country) has been among the potential lubricants markets in recent years on account of its huge population, high urbanization, and rapidly rising middle class. Sectors such as mining, textile, and infrastructure have been driving the consumption of industrial lubricants in the recent past.

- According to the Indonesian Food and Beverage Entrepreneurs Association (GAPMMI), the food and beverage industry is estimated to rise by 7% by 2021. As per Badan Pusat Statistik (Statistics Indonesia), the production output from large and medium manufacturing industries exhibited a negative growth of 8.01% in 2021.

- The Government of Indonesia has been planning to invest about USD 412 billion in building projects, including constructing 25 airports, residential complexes, etc., by 2024. Such investments are part of the government's target to seek to strengthen growth in the country. However, the disruption in the supply chain is expected to hinder the initially expected growth path of the sector in the short term.

- Therefore, all the aforementioned factors are likely to significantly impact the market studied in the future.

Industrial Lubricants Industry Overview

The global industrial lubricants market is fragmented in nature. Some of the key players in the market include Royal Dutch Shell PLC, Exxon Mobil Corporation, China Petroleum & Chemical Corporation, China National Petroleum Corporation, and BP PLC (Castrol), among other companies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from the Wind Energy Sector

- 4.1.2 Other Drivers

- 4.2 Restraints

- 4.2.1 Detrimental Effects of Lubricants on the Environment

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Engine Oil

- 5.1.2 Transmission and Hydraulic Fluid

- 5.1.3 Metalworking Fluid

- 5.1.4 General Industrial Oil

- 5.1.5 Gear Oil

- 5.1.6 Grease

- 5.1.7 Process Oil

- 5.1.8 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Power Generation

- 5.2.2 Heavy Equipment

- 5.2.3 Food and Beverage

- 5.2.4 Metallurgy and Metalworking

- 5.2.5 Chemical Manufacturing

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Phillipines

- 5.3.1.6 Indonesia

- 5.3.1.7 Malaysia

- 5.3.1.8 Thailand

- 5.3.1.9 Vietnam

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 Spain

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Chile

- 5.3.4.5 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Iran

- 5.3.5.3 Iraq

- 5.3.5.4 United Arab Emirates

- 5.3.5.5 Kuwait

- 5.3.5.6 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 Egypt

- 5.3.6.2 South Africa

- 5.3.6.3 Nigeria

- 5.3.6.4 Algeria

- 5.3.6.5 Morocco

- 5.3.6.6 Rest of Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Amsoil Inc.

- 6.4.2 Bharat Petroleum Corporation Limited

- 6.4.3 Blaser Swisslube AG

- 6.4.4 BP PLC (Castrol)

- 6.4.5 Carl Bechem GmbH

- 6.4.6 Chevron Corporation

- 6.4.7 China National Petroleum Corporation (PetroChina)

- 6.4.8 China Petroleum & Chemical Corporation (SINOPEC Group)

- 6.4.9 Eni SpA

- 6.4.10 Exxon Mobil Corporation

- 6.4.11 FUCHS

- 6.4.12 Gazprom Neft PJSC

- 6.4.13 Gulf Oil International

- 6.4.14 HPCL

- 6.4.15 Idemitsu Kosan Co. Ltd

- 6.4.16 Indian Oil Corporation Ltd

- 6.4.17 ITW (ROCOL)

- 6.4.18 ENEOS

- 6.4.19 Kluber Lubrication

- 6.4.20 Lukoil Lubricants Company

- 6.4.21 PT Pertamina

- 6.4.22 Petrobras

- 6.4.23 Petronas Lubricants International

- 6.4.24 Phillips 66 Lubricants

- 6.4.25 Repsol

- 6.4.26 Royal Dutch Shell PLC

- 6.4.27 Tide Water Oil Co. (India) Ltd

- 6.4.28 TotalEnergies

- 6.4.29 Valvoline Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Prominence for Bio-Lubricants

- 7.2 Development of Low Viscosity Lubricants

工業潤滑油市場:按類型、基礎油、產品類型、最終用戶分類 - 全球預測 2024-2030

工業潤滑油市場:按類型、基礎油、產品類型、最終用戶分類 - 全球預測 2024-2030 2024-2032 年按產品類型、基礎油、最終用途產業和地區分類的工業潤滑油市場報告

2024-2032 年按產品類型、基礎油、最終用途產業和地區分類的工業潤滑油市場報告 2023-2027年全球工業潤滑油市場

2023-2027年全球工業潤滑油市場 全球工業潤滑油市場

全球工業潤滑油市場 重型設備潤滑油市場 – 2023 年至 2028 年預測

重型設備潤滑油市場 – 2023 年至 2028 年預測 工業潤滑油市場:按類型、基礎油、按產品類型、按最終用戶 - 2023-2030 年全球預測

工業潤滑油市場:按類型、基礎油、按產品類型、按最終用戶 - 2023-2030 年全球預測 2023-2028年按產品類型、基礎油、最終使用行業和地區分類的工業潤滑油市場

2023-2028年按產品類型、基礎油、最終使用行業和地區分類的工業潤滑油市場 中國的產業用潤滑油市場

中國的產業用潤滑油市場 2023-2030工業潤滑油市場各產品(工藝油、通用工業油、金屬加工油、工業發動機油)、應用、地區、細分市場規模、份額和趨勢分析報告

2023-2030工業潤滑油市場各產品(工藝油、通用工業油、金屬加工油、工業發動機油)、應用、地區、細分市場規模、份額和趨勢分析報告 滑道油的全球市場

滑道油的全球市場