|

市場調查報告書

商品編碼

1444358

地震服務 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Seismic Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

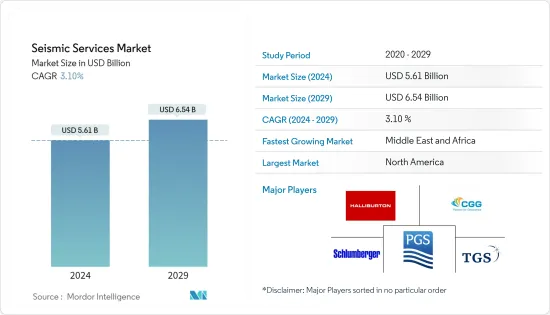

地震服務市場規模預計到 2024 年為 56.1 億美元,預計到 2029 年將達到 65.4 億美元,在預測期內(2024-2029 年)CAGR為 3.10%。

主要亮點

- 從中期來看,西非和墨西哥灣等近海地區探勘增加等因素,加上原油價格走強,使上游活動在經濟上可行,可能會推動市場。

- 另一方面,許多國家正在轉向再生能源並結束對原油的依賴,這可能會限制預測期內的市場成長。

- 然而,陸上和淺水油田已經成熟,這些地區幾乎沒有新油田發現的空間。因此,深水和超深水儲量的開發預計將為未來地震服務市場創造重大機會。

地震服務市場趨勢

海上石油和天然氣產業的需求不斷成長

- 海上部分佔據地震服務市場的最大佔有率。由於多種有利條件,包括可重複且一致的震源、震源和接收器良好的耦合條件以及水作為介質的均勻特性等,海上地震資料的品質通常比陸上地震資料高得多。

- 根據貝克休斯的數據,2022年世界平均鑽機總數為1,824個,高於2022年世界平均鑽機數量1,747個。隨著鑽機數量的增加,探勘活動將會增加,進而預計將推動地震探勘活動。世界的服務需求。

- 2022 年 1 月,殼牌公司宣佈在奈米比亞發現一口大型海上油氣井。對探勘鑽探的早期分析估計,新發現的油井可能含有 2.5 至 3 億桶石油和天然氣。這項發現之後,商業石油生產所需的油藏開發工作可能會推動市場。

- 此外,挪威石油管理局估計,大陸架上剩餘資源的 47% 左右必須被發現。英國大陸棚 (UKCS) 約有 350 個未開發的發現,蘊藏著 32 億桶石油當量 (bboe)。

- 因此,增加深水和超深水儲量的探勘和生產(E&P)活動以及石油和天然氣巨頭加大力度開發未發現的資源預計將推動海上地震服務市場的發展。

中東和非洲可能會顯著成長

- 海上地震勘測是繪製石油和天然氣礦藏圖的最便宜的方法。這種方法可以定位地下結構並記錄折射和反射資料。由於調查需要多個來源,因此聘請了多個工作小組來收集資料。

- 中東和非洲的海上探勘不斷增加,例如西非近海地區擁有廣泛的未開發資源,為石油和天然氣探勘公司創造了機會。因此,該地區的探勘可能會推動地震服務市場。

- 2022年1月,殼牌公司在奈米比亞近海Graff-1井獲得重大油氣發現,可能引發奈米比亞投資熱潮。鑽探結果顯示,一層至少 60 公尺深的碳氫化合物,估計蘊藏著 2.5 億至 3 億桶石油和天然氣當量。該油田開發完成後預計將於 2026 年投入生產,其中地震勘測預計將推動市場發展。

- 此外,2022 年 1 月,澳洲地球科學公司 Searcher 開始在南非西海岸進行地震勘測,以進行涵蓋多個石油許可區塊的多客戶勘測專案。許可證面積約297,087平方米,許可證規定可以進行2D和3D推測地震探勘計畫。這可能有助於該地區市場的成長。

- 因此,新石油和天然氣的發現以及地震測試的批准等上述因素預計將在預測期內推動中東和非洲地區的地震服務市場。

地震服務業概況

地震服務市場高度集中。一些主要公司包括(排名不分先後)Schlumberger NV、CGG SA、PGS ASA、TGS ASA 和 Halliburton Company 等。

2022 年 8 月,斯倫貝謝和微軟簽署了一項多年期協議,旨在匯集聯合專業知識,為能源產業建立開放、可擴展的雲端原生資料產品。下一階段將利用OSDU資料平台的開放性和敏捷性,開發第一個雲端原生地震處理解決方案-DELFI地震處理。透過利用 OSDU 資料平台,合作夥伴為開發創新應用程式和工作流程以滿足當前的地震需求提供了經濟高效的基礎。第三方開發人員將建構和增強地震處理解決方案,供其內部使用或提供給市場。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究範圍

- 市場定義

- 研究假設

第 2 章:執行摘要

第 3 章:研究方法

第 4 章:市場概覽

- 介紹

- 到 2028 年市場規模與需求預測(十億美元)

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進要素

- 增加近海地區的探勘

- 原油價格走強,使上游活動在經濟上可行

- 限制

- 轉向再生能源

- 促進要素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者的議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭激烈程度

第 5 章:市場區隔

- 服務

- 數據採集

- 數據處理和解釋

- 部署地點

- 陸上

- 離岸

- 地理

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 亞太

- 中國

- 印度

- 澳洲

- 亞太其他地區

- 歐洲

- 德國

- 俄羅斯

- 英國

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 伊朗

- 伊拉克

- 中東和非洲其他地區

- 北美洲

第 6 章:競爭格局

- 併購、合資、合作與協議

- 領先企業採取的策略

- 公司簡介

- Halliburton Company

- Briscoe Group Limited

- CGG SA

- Fugro NV

- ION Geophysical Corporation

- PGS ASA

- Polarcus Ltd

- SAExploration Holdings Inc.

- Schlumberger NV

- SeaBird Exploration PLC

- Shearwater GeoServices Holding AS

- TGS ASA

- Magseis Fairfield ASA (WGP Group Ltd)

- China Oilfield Services Limited

第 7 章:市場機會與未來趨勢

- 深水和超深水儲量的可用性

The Seismic Services Market size is estimated at USD 5.61 billion in 2024, and is expected to reach USD 6.54 billion by 2029, growing at a CAGR of 3.10% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, factors such as increasing exploration in the offshore areas such as in West Africa and the Gulf of Mexico, coupled with the strengthening of crude oil prices, making the upstream activities economically feasible, are likely to drive the market.

- On the other hand, a lot of countries are shifting to renewable energy sources and ending their reliance on crude oil, which may restrain the market growth during the forecast period.

- Nevertheless, land-based and shallow-water oil fields have reached their maturity, and there is little scope for any new field discovery in these areas. Therefore, the development of deepwater and ultra-deepwater water reserves is expected to create significant opportunities for the seismic services market in the future.

Seismic Services Market Trends

Increasing Demand from the Offshore Oil and Gas Industry

- The offshore segment accounts for the largest share of the seismic services market. Offshore seismic data usually has much higher quality than onshore due to several favorable conditions, including repeatable and consistent sources, good conditions for coupling at sources and receivers, and the uniform property of water as the medium.

- According to Baker Hughes, the total world average rig count was 1,824 in 2022, more significant than the world average of 1,747 in 2022. With the increasing number of rigs, exploration activities will grow, which, in turn, is expected to drive the seismic services demand in the world.

- In January 2022, Shell PLC announced the discovery of a substantial offshore oil and gas well in Namibia. Early analysis of the exploratory drilling estimates that the newly discovered well could contain 250 to 300 million barrels of oil and gas. After this discovery, the reservoir development work necessary for commercial petroleum production will likely drive the market.

- Furthermore, the Norwegian Petroleum Directorate has estimated that around 47% of all the remaining resources on the shelf must be discovered. Around 350 undeveloped discoveries in the United Kingdom Continental Shelf (UKCS) contain 3.2 billion barrels of oil equivalent (bboe).

- Therefore, increasing exploration and production (E&P) activities in the deepwater and ultra-deepwater reserves and increasing efforts by the oil and gas majors to tap into the undiscovered resources are expected to drive the offshore seismic services market.

Middle-East and Africa is Likely to Experience Significant Growth

- The Offshore Seismic Survey is the least expensive method of mapping oil and gas deposits. This approach locates subsurface structures and records data on refraction and reflection. Because the survey requires more than one source, several WGs are employed to collect data.

- Middle-East and Africa is witnessing increasing offshore exploration in regions such as offshore West Africa, which has widespread untapped resources, creating opportunities for the oil and gas exploration companies. Thus, explorations in this region are likely to drive the seismic services market.

- In January 2022, Shell PLC made a significant oil and gas discovery in the Graff-1 well in offshore Namibia, which can spark a wave of investment in Namibia. The drilling results have shown one layer of at least 60 meters deep of hydrocarbons, holding an estimated 250 to 300 million barrels of oil and gas equivalent. The field expects to go into production by 2026 after its development, including seismic surveys, which are expected to drive the market.

- Furthermore, in January 2022, the Australian geoscience company Searcher started its seismic survey off the West Coast of South Africa for a multi-client survey program that covers a number of petroleum license blocks. The permit area is approximately 297,087 m2, and the permit provides for the undertaking of a two-dimensional and three-dimensional speculative seismic survey program. This is likely to aid the growth of the market in the region.

- Therefore, the above-mentioned factors, such as new oil and gas discoveries and approvals for seismic testing, are expected to drive the seismic services market in the Middle-East and Africa region over the forecast period.

Seismic Services Industry Overview

The seismic services market is highly concentrated. Some of the major companies include (not in a particular order ) Schlumberger NV, CGG SA, PGS ASA, TGS ASA, and Halliburton Company, among others.

In August 2022, Schlumberger and Microsoft have signed a multi-year agreement to pool joint expertise and build open and extensible cloud-native data products for the energy industry. The next phase will use the openness and agility of the OSDU Data Platform to develop the first cloud-native seismic processing solution - DELFI Seismic Processing. By leveraging the OSDU Data Platform, the partners are providing a cost-effective foundation for developing innovative applications and workflows to address current seismic needs. Third-party developers will build and augment seismic processing solutions, either for their internal use or to offer to the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Exploration in Offshore Areas

- 4.5.1.2 The Strengthening of Crude Oil Prices, Making the Upstream Activities Economically Feasible

- 4.5.2 Restraints

- 4.5.2.1 Shifting to Renewable Energy Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Service

- 5.1.1 Data Acquisition

- 5.1.2 Data Processing and Interpretation

- 5.2 Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States of America

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Asia-Pacific

- 5.3.2.1 China

- 5.3.2.2 India

- 5.3.2.3 Australia

- 5.3.2.4 Rest of Asia-Pacific

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 Russia

- 5.3.3.3 United Kingdom

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of the South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Iran

- 5.3.5.4 Iraq

- 5.3.5.5 Rest of the Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Halliburton Company

- 6.3.2 Briscoe Group Limited

- 6.3.3 CGG SA

- 6.3.4 Fugro NV

- 6.3.5 ION Geophysical Corporation

- 6.3.6 PGS ASA

- 6.3.7 Polarcus Ltd

- 6.3.8 SAExploration Holdings Inc.

- 6.3.9 Schlumberger NV

- 6.3.10 SeaBird Exploration PLC

- 6.3.11 Shearwater GeoServices Holding AS

- 6.3.12 TGS ASA

- 6.3.13 Magseis Fairfield ASA (WGP Group Ltd)

- 6.3.14 China Oilfield Services Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Availability of Deepwater and Ultra-Deepwater Water Reserves

海底地震勘探設備與資料收集市場:2024-2034

海底地震勘探設備與資料收集市場:2024-2034 陸域地震勘探設備與資料採集市場:2024-2034

陸域地震勘探設備與資料採集市場:2024-2034 地震服務市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

地震服務市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 地震服務市場規模 - 按調查類型(陸地、海洋)、最終用戶(石油和天然氣、採礦)、區域展望、成長潛力、價格趨勢、競爭格局和預測,2023 - 2032 年

地震服務市場規模 - 按調查類型(陸地、海洋)、最終用戶(石油和天然氣、採礦)、區域展望、成長潛力、價格趨勢、競爭格局和預測,2023 - 2032 年 2023-2027年全球地震探勘服務市場

2023-2027年全球地震探勘服務市場 全球地震服務市場規模研究和預測,按類型(數據採集、提供的服務、技術)、按部署地點(陸上、海上)、按應用(石油和天然氣、建築、採礦、其他)和區域分析,2023年- 2030年

全球地震服務市場規模研究和預測,按類型(數據採集、提供的服務、技術)、按部署地點(陸上、海上)、按應用(石油和天然氣、建築、採礦、其他)和區域分析,2023年- 2030年 陸上地震觀測設備及取得的全球市場

陸上地震觀測設備及取得的全球市場 地震探勘服務的全球市場 - 產業規模,佔有率,趨勢,機會,預測(2017年~2027年):各類服務,各技術,部署地點,各用途,各地區

地震探勘服務的全球市場 - 產業規模,佔有率,趨勢,機會,預測(2017年~2027年):各類服務,各技術,部署地點,各用途,各地區