|

市場調查報告書

商品編碼

1444301

熱塑性聚氨酯 (TPU) -市場佔有率分析、行業趨勢和統計、成長預測 (2024-2029)Thermoplastic Polyurethane (TPU) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

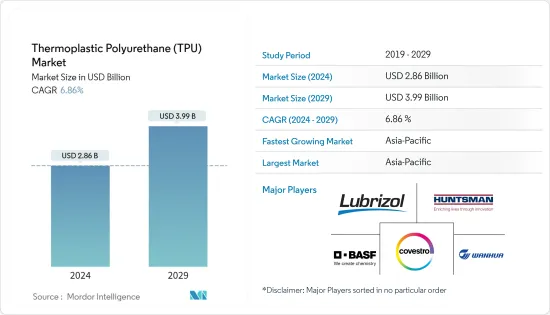

熱塑性聚氨酯市場規模預計到2024年為28.6億美元,預計到2029年將達到39.9億美元,在預測期內(2024-2029年)成長6.86%,年複合成長率為

在COVID-19感染疾病期間,TPU的需求大幅下降,因為它主要用於消費品。不利的宏觀經濟影響了人們的財務狀況,降低了他們的購買力,並對TPU的需求產生了負面影響。供應鏈限制進一步加劇了下滑。然而,一旦限制放鬆,需求將在 2021 年恢復到大流行前的水平。

主要亮點

- 研究市場的主要促進因素是 TPU 在鞋類和服裝行業中的使用不斷增加。

- 相反,原物料價格上漲正在阻礙所研究市場的成長。

- 在預測期內,生物基 TPU 薄膜可能會為接受調查的市場提供成長機會。

- 亞太地區是各種應用領域 TPU 的最大消費國,預計這項需求在預測期內將快速成長。

熱塑性聚氨酯(TPU)市場趨勢

TPU 在鞋類和服裝產業的使用不斷增加

- 由於人口的快速成長和許多經濟體的持續擴張,對皮革的需求正在穩步成長。傳統皮革產業消費量大、污染大。大眾對環境議題的關注給皮革產業帶來了重大挑戰。

- TPU薄膜具有其他塑膠和橡膠所需的性能,使其廣泛應用於鞋類和服裝類領域。

- 隨著科學技術的進步,TPU薄膜及其複合製品的製造技術有了很大的進步,為採用TPU薄膜及其複合製品創造了理想的條件。生產商最近在鞋類和服裝行業推出了許多創新產品。

- 例如,路博潤推出了一款完全由 TPU 製成的原型鞋。這款 100% TPU 原型鞋可以提供改進的「循環」解決方案。鞋類製造商在製造過程中重複利用 TPU廢棄物,促進消費後回收過程。

- 亨斯邁的特殊合成橡膠專業知識創造了一種新型熱塑性聚氨酯 (TPU) 牌號 IROGRAN A 85 P 4394 HR。非常適合為要求性能的服裝類(包括手套和鞋類)提供防水和透氣層。

- 全球大部分鞋類生產集中在亞太地區,佔產量佔有率的85%以上。除亞洲國家和墨西哥外,巴西是世界主要鞋類製造國之一。根據巴西鞋業工業協會(Avicarcados)統計,2022年巴西鞋類產量達8.63億雙。

- 由於鞋類和服裝產量的激增以及技術進步使 TPU 成為鞋類和服裝行業更靈活和首選的材料,預計預測期內對 TPU 薄膜的需求將大幅增加。

亞太地區主導市場

- 亞太地區佔據了最大的區域熱塑性聚氨酯市場。由於汽車需求以及紡織品和鞋類需求的增加,TPU 基黏劑和密封劑預計將在該地區呈現健康的成長速度。

- 中國的製鞋業是世界上最大的,擁有強大的國內銷售和向主要國家出口的網路。與世界其他地區相比,中國對 TPU黏劑的需求預計最為強勁,因為皮鞋在中國製鞋業中佔據最大佔有率。

- 家庭收入水準的提高和農村人口向都市區的遷移預計將繼續推動對中國所研究市場的需求。

- 亞太地區是世界上一些最有價值的汽車製造商的所在地。中國、印度、日本和韓國等新興國家正努力加強製造基礎,建立高效的供應鏈,以提高盈利。

- 根據中國工業協會統計,中國是全球最大的汽車生產基地,預計2022年汽車產量將達到2700萬輛,比去年的2600萬輛成長3.4%。記錄下來了。此外,2022年1-7月,全國汽車產量1,457萬輛,與前一年同期比較成長31.5%。此外,2022年7月,電池驅動的電動車數量比2021年1月至7月增加了117.2%。預計2022年7月國內電動車銷量約61.7萬輛。

- 此外,根據印度汽車工業協會(SIAM)的數據,該國汽車工業在2021-22會計年度(2021年4月至2022年3月)總合生產了2,293萬輛汽車,而2021-22會計年度總合銷售了2293萬輛汽車。相較之下,2020 年 4 月至 2022 年 3 月印度的銷量為 2266 萬台。此外,根據印度經濟監測中心 (CMIE) 的數據,汽車產量從 2022 年 6 月的 169,520 輛增加到 2022 年 7 月的 193,630 輛。這些因素可能會增加所研究市場的需求。

- 印度政府制定的1,205億美元投資目標,發展27個產業叢集,預計將推動該國商業建設。

- 所有這些因素預計將在預測期內推動該地區熱塑性聚氨酯市場的發展。

熱塑性聚氨酯(TPU)產業概況

全球熱塑性聚氨酯市場正在整合,排名前五的公司佔據了研究市場的主要佔有率。該市場的主要企業包括BASF股份公司、科思創股份公司、路博潤公司、亨斯曼國際有限責任公司和萬華化學集團。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 醫療產業應用不斷增加

- 工業應用中的使用增加

- 其他司機

- 抑制因素

- 原物料價格上漲

- 其他限制因素

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔(以金額為準的市場規模)

- 目的

- 擠出成型品

- 射出成型產品

- 黏劑

- 其他用途

- 最終用戶產業

- 建造

- 車

- 鞋類

- 醫療保健

- 電力/電子

- 重工業

- 其他最終用戶產業

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東/非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- Trinseo

- Avient Corporation(Formerly PolyOne Corporation)

- Epaflex Polyurethanes SpA

- BASF SE

- Covestro AG

- Coim Group

- Miracll Chemicals Co. Ltd

- Huafeng Group

- Huntsman International LLC

- Dongsung Corporation

- Sumei Chemical Co. Ltd

- Suzhou New Mstar Technology Ltd

- The Lubrizol Corporation

- Tosoh Corporation

- Wanhua Chemical Group Co. Ltd

- Hexpol AB

第7章市場機會與未來趨勢

- 將重點轉向生物基產品開發

- 增加研發活動

The Thermoplastic Polyurethane Market size is estimated at USD 2.86 billion in 2024, and is expected to reach USD 3.99 billion by 2029, growing at a CAGR of 6.86% during the forecast period (2024-2029).

During the Covid-19 pandemic, the demand for TPU declined heavily as TPU is majorly used in consumer products. The unfavorable macroeconomics affected people's finances and reduced purchasing power, negatively affecting the TPU demand. The supply chain restrictions further compounded the decline. However, as the restrictions eased, the demand returned to pre-pandemic levels in 2021.

Key Highlights

- The major driving factor of the market studied is TPU's increasing usage in the footwear and apparel industries.

- On the flip side, the rising prices of raw materials are hindering the studied market's growth.

- Bio-based TPU films will likely offer growth opportunities for the market studied over the forecast period.

- Asia-Pacific is the largest consumer of TPU for various applications, and this demand is expected to grow rapidly during the forecast period.

Thermoplastic Polyurethane (TPU) Market Trends

Increasing TPU Usage in the Footwear and Apparel Industries

- With the fast rise of the population and the ongoing expansion of many economies, the demand for leather is growing at a healthy rate. The conventional leather sector includes high consumption and causes pollution. The public's attention to environmental concerns poses significant difficulties for the leather business.

- TPU film possesses the essential properties of other plastics and rubbers, making it widely utilized in footwear and clothes.

- The production technology of TPU film and its composite products saw significant growth with the advancement of science and technology, generating ideal conditions for adopting TPU film and its composite products. Producers introduced numerous innovations lately in the footwear and apparel industries.

- For instance, Lubrizol unveiled a prototype shoe made entirely of TPU. This 100% TPU prototype shoe can deliver improved "circularity" solutions. TPU waste can be reused by shoemakers during manufacturing and ease the post-consumer recycling process.

- Huntsman's Specialty Elastomers' expertise led to the creation of IROGRAN A 85 P 4394 HR, a novel thermoplastic polyurethane (TPU) grade. It is ideal for providing a waterproof, breathable layer in demanding performance garments (including gloves and footwear).

- Most of the global footwear production is concentrated in the Asia-Pacific region and occupies a share of over 85% in production volume. Apart from Asian countries, Mexico, brazil is among the major footwear manufacturers in the world. According to the Brazilian Footwear Industries Association (Abicalcados), Brazil's footwear production volume reached 863 million pairs in 2022.

- With a surge in footwear and apparel production and technological advancements making TPU a more flexible and preferable material for the footwear and apparel sectors, the demand for TPU films is expected to grow considerably during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific accounted for the largest regional thermoplastic polyurethane market. Due to the increasing automotive demand and demand for textile and footwear, TPU-based adhesives and sealants are expected to witness a healthy growth rate in the region.

- The Chinese footwear industry is the largest in the world, with a robust network of domestic sales and exports to major countries. As leather footwear accounts for the largest share of the footwear industry in China, the demand for TPU adhesives is estimated to be the strongest in China compared to other parts of the world.

- The rising household income levels and the population migrating from rural to urban areas are expected to continue to drive the demand for the market studied in China.

- The Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea are working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

- According to the China Association of Automobile Manufacturers (CAAM), China includes the largest automotive production base in the world, with a total vehicle production of 27 million units in 2022, registering an increase of 3.4 % compared to 26 million units produced last year. Further, in the first 7 months of 2022, the country produced 14.57 million units of cars, registering a growth rate of 31.5% Year on Year. Furthermore, in July 2022, the number of battery-powered electric vehicles increased by 117.2% compared to January-July in 2021. In July 2022, the country's electric vehicle sales were estimated at around 617,000 units.

- Moreover, in India, during FY 2021-22 (April 2021 to March 2022), according to the Society of Indian Automobile Manufacturers (SIAM), the country's automotive industry produced a total of 22.93 million vehicles compared to 22.66 million units during April 2020 to March 2021. Further, according to the Centre for Monitoring Indian Economy (CMIE), car production increased to 193.63 thousand units in July 2022 from 169.52 thousand units in June 2022. Such factors are likely to increase the demand for the studied market.

- In India, the government's investment target of USD 120.5 billion for developing 27 industrial clusters is expected to boost commercial construction in the country.

- All these factors are expected to boost the region's thermoplastic polyurethane market during the forecast period.

Thermoplastic Polyurethane (TPU) Industry Overview

The global thermoplastic polyurethane market is consolidated, with the top five players accounting for major shares of the market studied. Some major players in the market include BASF SE, Covestro AG, The Lubrizol Corporation, Huntsman International LLC, and Wanhua Chemical Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Applications in the Medical Industry

- 4.1.2 Rising Usage in Industrial Applications

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Rising Prices of Raw Materials

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Application

- 5.1.1 Extruded Products

- 5.1.2 Injection Molded Products

- 5.1.3 Adhesives

- 5.1.4 Other Applications

- 5.2 End-user Industry

- 5.2.1 Construction

- 5.2.2 Automotive

- 5.2.3 Footwear

- 5.2.4 Medical

- 5.2.5 Electrical and Electronics

- 5.2.6 Heavy Engineering

- 5.2.7 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Trinseo

- 6.4.2 Avient Corporation (Formerly PolyOne Corporation)

- 6.4.3 Epaflex Polyurethanes SpA

- 6.4.4 BASF SE

- 6.4.5 Covestro AG

- 6.4.6 Coim Group

- 6.4.7 Miracll Chemicals Co. Ltd

- 6.4.8 Huafeng Group

- 6.4.9 Huntsman International LLC

- 6.4.10 Dongsung Corporation

- 6.4.11 Sumei Chemical Co. Ltd

- 6.4.12 Suzhou New Mstar Technology Ltd

- 6.4.13 The Lubrizol Corporation

- 6.4.14 Tosoh Corporation

- 6.4.15 Wanhua Chemical Group Co. Ltd

- 6.4.16 Hexpol AB

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Shifting Focus Toward the Development of Bio-based Products

- 7.2 Increasing R&D Activities

熱塑性聚氨酯市場:按原料、類型和最終用戶分類 - 全球預測 2024-2030

熱塑性聚氨酯市場:按原料、類型和最終用戶分類 - 全球預測 2024-2030 2030 年熱塑性聚氨酯市場預測:按原料、應用、最終用戶和地區進行的全球分析

2030 年熱塑性聚氨酯市場預測:按原料、應用、最終用戶和地區進行的全球分析 熱塑性聚氨酯 (TPU) 的全球市場:~2030年

熱塑性聚氨酯 (TPU) 的全球市場:~2030年 熱塑性聚氨酯市場報告:2030 年趨勢、預測與競爭分析

熱塑性聚氨酯市場報告:2030 年趨勢、預測與競爭分析 熱塑性聚氨酯(TPU)的全球市場,實際成果與預測(2018年~2029年)

熱塑性聚氨酯(TPU)的全球市場,實際成果與預測(2018年~2029年) 熱塑性聚氨酯(TPU)市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

熱塑性聚氨酯(TPU)市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測 熱塑性聚氨酯(TPU)全球市場概要(2023年)

熱塑性聚氨酯(TPU)全球市場概要(2023年) 熱塑性聚氨酯的全球市場

熱塑性聚氨酯的全球市場 全球熱塑性聚氨酯 (TPU) 市場:按原材料、類型、最終用途行業和地區劃分的未來預測(至 2027 年)

全球熱塑性聚氨酯 (TPU) 市場:按原材料、類型、最終用途行業和地區劃分的未來預測(至 2027 年) 熱塑性聚氨酯(TPU)的全球市場 - 市場規模,市場區隔,展望,收益預測(2022年~2028年):各原料,各類型,各用途,各終端用戶,各地區

熱塑性聚氨酯(TPU)的全球市場 - 市場規模,市場區隔,展望,收益預測(2022年~2028年):各原料,各類型,各用途,各終端用戶,各地區