|

市場調查報告書

商品編碼

1444300

工業氣體 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Industrial Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

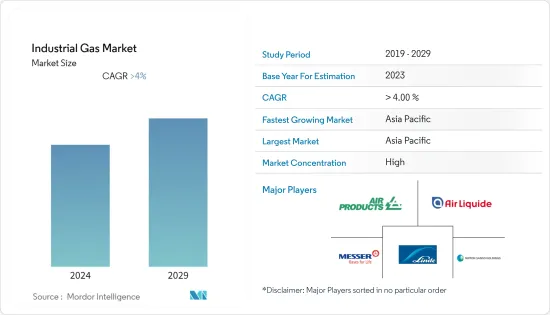

2024年工業氣體市場規模預估為16.7億噸,預估至2029年將達20.7億噸,在預測期間(2024-2029年)CAGR為4.35%。

COVID-19 對 2020 年市場產生了負面影響。二氧化碳用於生產碳酸軟性飲料和蘇打水,由於大流行情況而受到影響。然而,疫情期間醫療產業對復甦和吸入治療用氧氣的需求增加,刺激了市場的成長。

主要亮點

- 短期內,對替代能源的需求不斷成長以及醫療保健行業不斷成長的需求預計將推動工業氣體市場的成長。

- 環境法規和安全問題預計將推動市場的成長。

- 亞太和非洲的工業成長可能會在未來幾年創造市場機會。

- 預計亞太地區將主導市場,並可能在預測期內實現最高的CAGR。

工業氣體市場趨勢

醫療和製藥業的需求不斷成長

- 工業氣體,例如氧氣、氮氣、二氧化碳、氫氣、甲烷和丙烷,是化學生產鏈中各個製程步驟所需的反應劑的重要分子。

- 工業氣體為惰化、反應器冷卻和 pH 控制提供解決方案。石化產品是從石油和天然氣的精煉和加工中獲得的物質。它們需要惰性氣氛來運輸和儲存,而惰性氣氛由氮氣提供。

- 在煉油廠中,氧氣用於富集催化裂解再生器的空氣進料,從而提高裝置的產能。它用於硫磺回收裝置以實現類似的優點。氧氣也用於再生催化劑。

- 大量二氧化碳被用作化學程序工業的原料,特別是用於甲醇和尿素的生產。

- 氫氣主要用於煉油和化學製造。氫氣用作生產兩種工業化學品氨和甲醇的原料。在煉油廠中,它用於各種加氫脫硫 (HDS) 和加氫裂解程序。

- 甲烷在化學工業中用作製造甲醇、合成氨、乙炔和二氯甲烷等的原料。此外,丙烷用於生產乙烯和丙烯。

- 由於消費的增加、出口需求的增加以及政府措施的支持,預計世界各地的化學工業將出現成長。

- 亞太地區已發展成為全球化學加工中心。中國、印度、日本等國的化學工業發展迅速。迄今為止,亞洲佔據全球化學品市場最大佔有率。自2012年以來,連續佔據全球化學品市場一半以上的佔有率。

- 2022 年,亞洲化學品產量整體成長 4.2%。然而,各國的情況差異很大。印度產量顯著增加(+4.6%)。相較之下,日本、韓國和台灣的產量分別下降了3.0%、7.4%和12.9%。

- 在歐盟(EU),由於天然氣價格大幅上漲,化學品產量大幅下降5.8%。在德國,隨著天然氣密集型基礎化學品的生產停止,這一數字下降了約 12%。英國的化學品產量也大幅下降。

- 相較之下,2022年美國化學品產量增加了2.3%。然而,2021年天氣相關產量損失的潛在影響發揮了主要作用。同時,2022 年南美洲產量成長 2.6%,略低於上年(+3.6%)。

- 因此,預計上述因素將影響化學工業對工業氣體的需求。

亞太地區將主導工業氣體市場

- 亞太地區是最大的工業氣體市場。中國佔該地區消費的主要部分。然而,印度預計將成為該地區成長最快的國家。

- 中國航空航太業在經歷前幾年的大幅下滑後,預計將於 2022 年恢復盈利。中國民用航空局(CAAC)預計,航空業國內運輸量將恢復至疫情前水準的 85% 左右。

- 工業氣體也應用於交通運輸,包括使用加壓氮氣、用於安全氣囊的高壓氬氣以及用於精確安全焊接的二氧化碳和氮氣來製造輪胎。根據IATA(國際航空運輸協會)的報告,印度預計在2030年底成為世界第三大航空市場。

- 根據住房和城鄉建設部的預測,到 2025 年,中國建築業佔國內生產總值的比重預計將保持在 6%。考慮到這一預測,中國政府於 2025 年公佈了一項五年計劃。2022年1 月,使建築業更加永續和品質驅動。

- 2023 年 3 月,主要工業氣體生產商液化空氣集團宣布投資約 6,000 萬歐元(約 6,564 萬美元)改造集團在中國天津工業盆地營運的兩台空氣分離裝置 (ASU)。本公告是在與博化集團子公司天津博化永利化工(「YLC」)續簽長期工業氣體供應合約的背景下發布的。

- 印度是亞太地區第二大鋼鐵生產國,產量每年快速成長。

- 根據印度政府 2022 年 12 月的報告,印度的鋼鐵產量達到每年約 1.2 億噸的歷史水平,成為世界第二大鋼鐵生產國。該國每年的鋼鐵產量約佔全球的 4.8%。

- 根據世界鋼鐵協會的資料,2022 年印度粗鋼產量增加約 5.80%,達到 1.244 億噸,而 2021 年為 118.2 噸。根據世界鋼鐵協會的資料,2023 年 1 月至 2 月期間,印度生產了約 10.9 噸鋼材,較 2022 年同期下降約 0.2%。

- 各產業對鋼鐵的需求不斷成長,加上政府推動製造業發展的舉措,預計將增加機械天然氣生產裝置的使用,以滿足現代天然氣的大量先決條件。

- 因此,預計上述因素將在未來幾年推動該地區的市場成長。

工業氣體產業概況

工業氣體市場本質上是整合的。該市場的一些主要參與者(排名不分先後)包括液化空氣集團、梅塞爾Group Limited、日本酸素控股公司、林德集團和空氣產品公司。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 促進要素

- 對替代能源的需求不斷成長

- 對冷凍和儲存食品的需求不斷增加

- 醫療保健產業的需求不斷增加

- 限制

- 環境法規和安全問題

- 其他限制

- 價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭程度

第 5 章:市場區隔(依數量分類的市場規模)

- 產品類別

- 氮

- 氧

- 二氧化碳

- 氫

- 氦

- 氬氣

- 氨

- 甲烷

- 丙烷

- 丁烷

- 其他產品類型

- 最終用戶產業

- 化學加工和精煉

- 電子產品

- 食品與飲品

- 油和氣

- 金屬製造和加工

- 醫療與製藥

- 汽車和交通

- 能源與電力

- 其他最終用戶產業

- 地理

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 東協國家

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 歐洲其他地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第 6 章:競爭格局

- 併購、合資、合作與協議

- 市佔率(%)**/排名分析

- 領先企業採取的策略

- 公司簡介

- Air Liquide

- Air Products and Chemicals Inc.

- Asia Technical Gas Co Pte Ltd.

- BASF SE

- Bhuruka Gases Limited

- Ellenbarrie industrial Gases

- Gruppo SIAD

- Iwatani Corporation

- Linde PLC

- Messer Group GmbH

- Nippon Sanso Holdings Corporation

- PT Samator Indo Gas TBK

- Sapio Group

- SOL SPA

- Yingde Gases Group

第 7 章:市場機會與未來趨勢

- 未來幾年對低碳氣體的需求不斷成長

The Industrial Gas Market size is estimated at 1.67 Billion tons in 2024, and is expected to reach 2.07 Billion tons by 2029, growing at a CAGR of 4.35% during the forecast period (2024-2029).

COVID-19 negatively impacted the market in 2020. Carbon dioxide is used to produce carbonated soft drinks and soda water, which was affected owing to the pandemic scenario. However, the medical industry's demand for oxygen for resuscitation and inhalation therapy increased during the pandemic, stimulating the market's growth.

Key Highlights

- Over the short term, the growing need for alternate energy sources and increasing demand from the healthcare sector are expected to drive the growth of the industrial gas market.

- Environmental regulations and safety issues are projected for the market's growth.

- Industrial growth in Asia-Pacific and Africa will likely create market opportunities in the coming years.

- The Asia-Pacific region is expected to dominate the market and will likely witness the highest CAGR during the forecast period.

Industrial Gases Market Trends

Increasing Demand from the Medical and Pharmaceutical Sector

- Industrial gases, such as oxygen, nitrogen, carbon dioxide, hydrogen, methane, and propane, are essential molecules required as reaction agents for various process steps in the chemical production chain.

- Industrial gases provide solutions for inerting, reactor cooling, and pH control. Petrochemicals are substances obtained from the refining and processing of petroleum and natural gases. They require inert atmospheres for transportation and storage, which is provided by nitrogen.

- In refineries, oxygen is used to enrich the air feed to catalytic cracking regenerators, increasing the units' capacity. It is used in sulfur recovery units to achieve similar benefits. Oxygen is also used to regenerate catalysts.

- Large quantities of carbon dioxide are used as a raw material in the chemical process industry, especially for methanol and urea production.

- Hydrogen is mostly used in oil refining and chemical manufacturing. Hydrogen is used as a feedstock in the production of two industrial chemicals, ammonia and methanol. In refineries, it is used in various hydro-desulfurization (HDS) and hydrocracking procedures.

- Methane is used as a raw material in the chemical industry to make methanol, synthetic ammonia, acetylene, and methylene chloride, among others. Further, propane is used in the production of ethylene and propylene.

- The chemical industry across the world is projected to witness growth, owing to the increasing consumption, increasing export demand, and enabling government initiatives.

- Asia-Pacific has grown to be the hub for chemical processing globally. The chemical industry in countries such as China, India, and Japan has been growing rapidly. The largest proportion of the global chemicals market is held by Asia by far. Since 2012, it has continuously accounted for more than half of the global chemicals market.

- Chemical production in Asia overall increased by 4.2% in 2022. However, this varies greatly from country to country. India saw a significant increase in production (+4.6%). In contrast, production in Japan, South Korea, and Taiwan fell by 3.0%, 7.4%, and 12.9%, respectively.

- In the European Union (EU), chemical production fell sharply by 5.8% due to a sharp rise in natural gas prices. In Germany, this fell by around 12% as the production of gas-intensive basic chemicals ceased. The United Kingdom also experienced a significant decline in chemical production.

- In contrast, US chemical production increased by 2.3% in 2022. However, the underlying impact of weather-related production losses in 2021 played a major role. Meanwhile, production in South America grew at 2.6% in 2022, slightly slower than the previous year (+3.6%).

- Thus, the abovementioned factors are expected to influence the demand for industrial gases used in the chemical industry.

Asia-Pacific to Dominate the Industrial Gas Market

- Asia-Pacific is the largest market for industrial gases. China accounted for a major chunk of the consumption in the region. However, India is expected to witness the fastest growth in the region.

- China's aerospace industry is projected to return to profitability in 2022 after facing a significant decline in the previous years. The Civil Aviation Administration of China (CAAC) estimated the aviation sector to recover domestic traffic to around 85% of pre-pandemic levels.

- Industrial gases also find their application in transportation, including tire manufacturing using pressurized nitrogen, high-pressure argon for airbags, and carbon dioxide and nitrogen for precise and secure welding. According to the IATA (International Air Transport Association) report, India is poised to become the third-largest aviation market in the world by the end of 2030.

- As per the forecast given by the Ministry of Housing and Urban-Rural Development, China's construction sector is expected to maintain a 6% share of the country's GDP going into 2025. Considering the given forecasts, the Chinese government unveiled a five-year plan in January 2022 to make the construction sector more sustainable and quality-driven.

- In March of 2023, Air Liquide, a major industrial gas player, announced investing around EUR 60 million (~USD 65.64 million) to revamp two Air Separation Units (ASUs), which the Group operates in the Tianjin industrial basin in China. This announcement comes within the context of the renewal of a long-term industrial gases supply contract with Tianjin Bohua YongliChemical Industry Co., Ltd ('YLC'), a subsidiary of the BohuaGroup.

- India is the Asia-Pacific's second-largest iron and steel producer, and production is increasing rapidly yearly.

- Steel production in India reached a historic level of around 120 million tons per annum, making it the world's second-largest steel producer, as per the Indian government report in December 2022. The country accounts for around 4.8% of global steel production annually.

- The crude steel production in India rose by around 5.80% to 124.4 million tons (MT) in 2022, compared to 118.2 MT in 2021, according to World Steel Association data. India produced around 10.9 MT of steel between January-February 2023, down by around 0.2% compared to the same period in 2022, as per the World Steel Association data.

- Growing demand for iron and steel from various industries and the upcoming steel ventures, coupled with government initiatives to boost the manufacturing sector, is expected to boost the usage of mechanical gas creation units to address the mass prerequisites for modern gases.

- Therefore, the abovementioned factors are expected to drive market growth in th region in the coming years.

Industrial Gases Industry Overview

The industrial gas market is consolidated in nature. Some of the market's major players (not in any particular order) include Air Liquide, Messer Group GmbH, Nippon Sanso Holdings Corporation, Linde PLC, and Air Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Need for Alternate Energy Sources

- 4.1.2 Increasing Demand For Frozen and Stored Food

- 4.1.3 Increasing Demand from the Healthcare Sector

- 4.2 Restraints

- 4.2.1 Environmental Regulations and Safety Issues

- 4.2.2 Other Restraints

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size by Volume)

- 5.1 Product Type

- 5.1.1 Nitrogen

- 5.1.2 Oxygen

- 5.1.3 Carbon dioxide

- 5.1.4 Hydrogen

- 5.1.5 Helium

- 5.1.6 Argon

- 5.1.7 Ammonia

- 5.1.8 Methane

- 5.1.9 Propane

- 5.1.10 Butane

- 5.1.11 Other Product Types

- 5.2 End-user Industry

- 5.2.1 Chemical Processing and Refining

- 5.2.2 Electronics

- 5.2.3 Food and Beverage

- 5.2.4 Oil and Gas

- 5.2.5 Metal Manufacturing and Fabrication

- 5.2.6 Medical and Pharmaceutical

- 5.2.7 Automotive and Transportation

- 5.2.8 Energy and Power

- 5.2.9 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 NORDIC Countries

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Liquide

- 6.4.2 Air Products and Chemicals Inc.

- 6.4.3 Asia Technical Gas Co Pte Ltd.

- 6.4.4 BASF SE

- 6.4.5 Bhuruka Gases Limited

- 6.4.6 Ellenbarrie industrial Gases

- 6.4.7 Gruppo SIAD

- 6.4.8 Iwatani Corporation

- 6.4.9 Linde PLC

- 6.4.10 Messer Group GmbH

- 6.4.11 Nippon Sanso Holdings Corporation

- 6.4.12 PT Samator Indo Gas TBK

- 6.4.13 Sapio Group

- 6.4.14 SOL SPA

- 6.4.15 Yingde Gases Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Demand for Low-Carbon Gases in the Coming Years

2024-2028 年全球工業氣體市場

2024-2028 年全球工業氣體市場 中國的工業用氣體市場

中國的工業用氣體市場 工業氣體市場報告按類型(氮氣、氧氣、二氧化碳、氬氣、氫氣等)、應用(製造、冶金、能源、化學、醫療保健等)、供應模式(包裝、散裝、現場)、和地區 2024-2032

工業氣體市場報告按類型(氮氣、氧氣、二氧化碳、氬氣、氫氣等)、應用(製造、冶金、能源、化學、醫療保健等)、供應模式(包裝、散裝、現場)、和地區 2024-2032 工業氣體填充玻璃產業 2024 年全球市場報告

工業氣體填充玻璃產業 2024 年全球市場報告 2024 年工業氣體世界市場報告

2024 年工業氣體世界市場報告 全球工業氣體市場:按類型(氧氣、氮氣、氫氣、二氧化碳、乙炔、惰性氣體)、最終用途行業(化學品、電子、食品和飲料、醫療保健、製造、冶金、精製)、按地區分類- 預測(~2028)

全球工業氣體市場:按類型(氧氣、氮氣、氫氣、二氧化碳、乙炔、惰性氣體)、最終用途行業(化學品、電子、食品和飲料、醫療保健、製造、冶金、精製)、按地區分類- 預測(~2028) 塑膠和橡膠產業工業氣體的全球市場(2024 年)

塑膠和橡膠產業工業氣體的全球市場(2024 年) 工業氣體 - 金屬和金屬加工世界市場報告 2024年

工業氣體 - 金屬和金屬加工世界市場報告 2024年 美國工業氣體市場規模、佔有率和趨勢分析報告:按產品、應用和細分市場預測,2024-2030 年

美國工業氣體市場規模、佔有率和趨勢分析報告:按產品、應用和細分市場預測,2024-2030 年 塑膠和橡膠行業的工業氣體市場:按氣體類型、應用、分銷/運輸和最終用途 - 2023-2030 年全球預測

塑膠和橡膠行業的工業氣體市場:按氣體類型、應用、分銷/運輸和最終用途 - 2023-2030 年全球預測