|

市場調查報告書

商品編碼

1444153

矽膠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

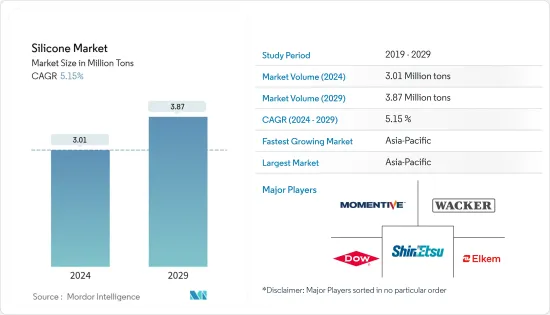

預計2024年矽膠市場規模為301萬噸,預計2029年將達到387萬噸,在預測期間(2024-2029年)年複合成長率為5.15%。

矽膠市場受到 COVID-19 大流行、一系列全國性封鎖、嚴格的社交距離規範以及全球供應鏈網路中斷的阻礙。世界各地許多工廠和產業關閉,影響了矽膠的需求。然而,健康和衛生意識的增強進一步刺激了醫療保健、個人護理和消費品行業的需求,並刺激了對矽膠的需求。

主要亮點

- 從長遠來看,推動矽膠市場成長的主要因素是醫療保健產業的使用量增加、輸配電產業的需求增加以及汽車產業的應用增加。

- 另一方面,地緣政治緊張局勢和政府監管力度加大的影響可能會阻礙市場成長。

- 各種最終用戶對電活性聚合物(EAP)的潛在需求不斷成長,可能為預測期內的矽膠市場帶來機會。

- 預計亞太地區將在其他地區中佔據主導地位,其中中國和印度將推動該地區的成長。

矽膠市場趨勢

增加在工業製程的使用

- 工業消泡劑、工業塗料、液壓油和潤滑劑、RTV(室溫硫化)密封劑、模具和聚合物添加劑代表了矽膠在工業加工領域的主要應用。

- 在石油和天然氣行業,矽膠廣泛用於海上鑽井,其中空間和重量限制需要泡沫和廢棄物管理。矽膠會釋放鑽井泥漿中殘留的氣體。消泡劑可減少能源和化學品的使用,同時提高生產率,因為泡沫的存在會減慢流程並增加維護作業的時間。

- 矽膠也主要用於工業塗料,例如橋樑和隧道中使用的耐腐蝕、耐化學藥品和耐熱塗料。這些還包括用於石油和天然氣(包括煉油廠)、電力和其他行業(包括採礦、廢棄物處理以及紙漿和造紙)的塗層結構。

- 因此,全球石油和天然氣產業的擴張預計將受益於矽膠的需求。各種正在進行的擴張計劃預計將推動成長。例如,國營精製中石油計畫於 2022 年上半年開始運作位於中國南部廣東省揭陽煉油廠的日產 40 萬桶的煉油廠。印度是亞太地區石油和天然氣領域的領先經濟體。天然氣部分。根據印度品牌股權基金會(IBEF)預測,到2045年,印度石油需求預計將達到1,100萬桶。此外,印度天然氣消費量預計將增加250億立方公尺。米。到 2024 年。

- 多年來,世界海上鑽油平臺的數量一直在緩慢成長,同時由於新契約的贏得以及歐洲、非洲和美國生產活動的增加,需求也隨之增加。海洋探勘設備的需求量很大,近年來支撐了包括矽膠消泡劑在內的水處理化學品市場的成長。

- 由於上述所有因素,預計市場在預測期內復甦後將呈現強勁成長。

亞太地區預計將主導市場

- 亞太地區是矽膠的主要消費地區,佔最大佔有率。中國、印度和日本的市場成長是多年來亞太有機矽膠市場成長的主要原因之一。

- 半導體是電子領域的重要組成部分,矽膠用於封裝、塗覆、黏合和保護半導體、PCB、ECU矽膠。根據半導體產業協會的數據,2021年中國半導體銷售額達1,829.3億美元,而2020年為1,504億美元,增加了調查市場的需求。

- 中國擁有14,000多公里的海岸線和多個大型港口,是世界上最大的海洋國家之一。該國是幾個大型造船集團的所在地。中國船舶工業集團公司(CSSC)、中國船舶工業集團公司(CSIC)、中國外運、中遠海運和招商局國際是中國造船業的主要企業。中國造船廠正在建造各種船舶,包括散裝貨船、貨櫃船、油輪、軍艦、客船和豪華船舶,從而創造了對矽膠的需求。

- 此外,中國擁有全球最大的電子產品生產基地。根據ZVEI Dia Elektroindustrie統計,2020年中國電子產業產值約24.3億美元,預計2021年和2022與前一年同期比較%,成為一個龐大的矽膠市場。

- 此外,根據印度品牌股權基金會(IBEF)的數據,到 2025 年,印度對半導體產品的需求預計將達到 4,000 億美元。根據生產連結獎勵計畫(PLI) 計劃,印度預計將獲得 7,600 億印度盧比的半導體產業投資,北方邦政府也致力於成為該國的半導體中心。

- 2020年日本電子產業總產值約9.96兆日元,與前一年同期比較96.6%。然而,到2021年8月電子業產值增至71,930億日元,為2020年前8個月的113.4%,增加了該地區矽膠的消費量。

- 此外,亞太地區是最大的汽車製造地,產量佔全球近60%。根據OICA統計,2021年前9個月汽車總產量為3,267萬輛,較去年同期成長11%。

- 上述因素可能會導致預測期內該地區矽膠市場需求的增加。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 在汽車領域的應用不斷增加

- 增加在醫療保健行業的使用

- 輸配電需求不斷擴大

- 抑制因素

- 政府規章

- 地緣政治影響

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

第5章市場區隔

- 科技

- 合成橡膠

- 體液

- 最終用戶

- 交通設施

- 建築材料

- 電子產品

- 衛生保健

- 工業製程

- 個人護理和消費品

- 其他最終用戶

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、合作與協議

- 市場佔有率(%)分析

- 主要企業採取的策略

- 公司簡介

- BRB International BV(PETRONAS Chemicals Group Berhad)

- CHT Group

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co. Ltd

- Jiangsu Mingzhu Silicone Rubber Material Co. Ltd

- Kaneka Corporation

- Mitsubishi Chemical Holdings Corporation

- Momentive

- Shin-Etsu Chemical Co. Ltd.

- Wacker Chemie AG

- Wynca Group

- Zhejiang Sucon Silicone Co. Ltd.

第7章市場機會與未來趨勢

The Silicone Market size is estimated at 3.01 Million tons in 2024, and is expected to reach 3.87 Million tons by 2029, growing at a CAGR of 5.15% during the forecast period (2024-2029).

The COVID-19 pandemic, the series of nationwide lockdowns, strict social distancing norms, and disruption in the global supply chain network hampered the silicone market. Many factories and industries were shut down globally, affecting the demand for silicone. However, due to increasing awareness of health and hygiene, a further rise in demand from the healthcare, personal care, and consumer products sectors has stimulated the demand for silicone.

Key Highlights

- Over the long term, the major factors driving the silicone market's growth are the increased usage in the healthcare industry, the growing demand from the power transmission and distribution sector, and rising applications in the automotive industry.

- On the flip side, the impact of geopolitical tensions and the rising number of government regulations are likely to hinder the growth of the market.

- Rising potential demand for electroactive polymers (EAP) from various end-users is likely to be an opportunity for the silicone market over the forecast period.

- Asia-Pacific is expected to dominate the market among other regions, with China and India leading the growth in the region.

Silicone Market Trends

Increasing Usage in Industrial Processes

- Industrial anti-foaming agents, industrial coatings, hydraulic fluids and lubricants, RTV (Room-Temperature-Vulcanizing) sealants, molds, and additives for polymers represent the key application of silicones in the industrial processes sector.

- In the oil and gas industry, silicones are widely used in offshore drilling, where managing foam and waste is essential because of space and weight constraints. Silicones enable gas trapped in the drilling mud to get released. Anti-foaming agents reduce the use of energy and chemicals while increasing production rates, as the presence of foam slows down the process and requires time for maintenance operations.

- Silicone also finds its major application in industrial coatings like anti-corrosion, chemical-resistant, and heat-resistant coatings used on bridges and tunnels. They also include coatings on structures used in oil and gas (including refineries), power, and other industries (including mining, waste treatment, and pulp and paper).

- Thus, expanding the global oil and gas industry is anticipated to benefit from the demand for silicone. Various expansion projects underway are expected to drive the growth. For instance, PetroChina, a state-controlled refinery company, is planning to start its 400,000 barrels per day Jieyang refinery in South China's Guangdong province by the first half of 2022. India is a major economy in the Asia-Pacific region in the oil and gas segment. According to India Brand Equity Foundation (IBEF), the oil demand in India is projected to reach 11 million barrels by the year 2045. Furthermore, natural gas consumption in India is expected to grow by 25 billion cu. m. by the year 2024.

- The number of offshore drilling rigs globally has risen at a gradual rate over the years, and this, along with the new contract awards and the increase in production activities from Europe, Africa, and the United States, has led to an increase in the demand for offshore exploration equipment, in turn supporting the growth of the water treatment chemicals including silicone-based anti-foaming agents' market in the recent past.

- Due to all the above factors, the market is expected to witness strong post-recovery growth during the forecast period.

Asia-Pacific Region is Expected to Dominate the Market

- Asia-Pacific is the major consumer of silicone, accounting for the largest share. The growing market in China, India, and Japan has been one of the prominent reasons for the growth of the Asia-Pacific silicone market over the years.

- Semiconductors form a major part of the electronics segment, which involves the usage of silicones as silicone encapsulates, coat, and adhere to and protect semiconductors, PCBs, and ECUs , and others. According to the Semiconductor Industry Association, the semiconductor sales value in China stood at USD 182.93 billion in 2021, compared to USD 150.4 billion in 2020, thereby, increased the demand for studied market.

- With a coastline of over 14,000 km and several large ports, China is one of the world's largest maritime countries. The country has several large shipbuilding conglomerates: China State Shipbuilding Corporation (CSSC), China Shipbuilding Industry Corporation (CSIC), Sinotrans, COSCO shipping, and CMHI are a few major names in the country's shipbuilding industry. The Chinese shipyards build a variety of ships, such as bulk carriers, container ships, oil tankers, naval vessels, passenger vessels, luxury vessels, and others, thereby creating demand for silicone.

- Moreover, China has the world's largest electronics production base. According to ZVEI Dia Elektroindustrie, China's electronics industry was valued at about USD 2,430 million in 2020, and it is forecasted to register 11% and 8% Y-o-Y in 2021 and 2022, thus providing a huge market for silicone.

- Also, acccording to India Brand Equity Foundation (IBEF), India's demand for semiconductor goods will reach USD 400 billion by FY2025. With India estimated to receive INR 76,000 crore as investments in the semiconductor sector under the Production Linked Incentive (PLI) scheme, the Uttar Pradesh government is also aiming to emerge as a semiconductor hub in the country.

- The total production value of the electronics industry in Japan was around JPY 9.96 trillion in 2020, which was 96.6% of the production value compared to the last year. However, the electronics industry production till August 2021 increased to JPY 7.193 trillion, which was 113.4% of the first eight months' value in 2020, thereby increasing the consumption of silicone in the region.

- Furthermore, the Asia-Pacific region is the largest automotive manufacturing hub, registering almost 60% production share of the world. According to OICA, in the first nine months of 2021, the total production of vehicles stood at 32.67 million units, an increase of 11% compared to the same period last year.

- The factors mentioned above may contribute to the increasing demand in the silicone market in the region during the forecast period.

Silicone Industry Overview

The silicone market is consolidated, with most of the share accounted for by key players. Some of the market's major players (not in any particular order) include Wacker Chemie AG, Dow, Shin-Etsu Chemical Co. Ltd, Momentive, and Elkem ASA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Application in Automotive Sector

- 4.1.2 Increasing Usage in Healthcare Industry

- 4.1.3 Growing Demand from Power Transmission and Distribution

- 4.2 Restraints

- 4.2.1 Government Regulation

- 4.2.2 Geopolitical Impact

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Technology

- 5.1.1 Elastomers

- 5.1.2 Fluids

- 5.2 End-user

- 5.2.1 Transportation

- 5.2.2 Construction Materials

- 5.2.3 Electronics

- 5.2.4 Healthcare

- 5.2.5 Industrial Processes

- 5.2.6 Personal Care and Consumer Products

- 5.2.7 Other End-users

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BRB International B.V. (PETRONAS Chemicals Group Berhad)

- 6.4.2 CHT Group

- 6.4.3 Dow

- 6.4.4 DyStar Singapore Pte Ltd

- 6.4.5 Elkem ASA

- 6.4.6 Evonik Industries AG

- 6.4.7 Hoshine Silicon Industry Co. Ltd

- 6.4.8 Jiangsu Mingzhu Silicone Rubber Material Co. Ltd

- 6.4.9 Kaneka Corporation

- 6.4.10 Mitsubishi Chemical Holdings Corporation

- 6.4.11 Momentive

- 6.4.12 Shin-Etsu Chemical Co. Ltd.

- 6.4.13 Wacker Chemie AG

- 6.4.14 Wynca Group

- 6.4.15 Zhejiang Sucon Silicone Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Potential Demand For Electro Active Polymers (EAP)

2024-2032 年重型機械市場中的有機矽依產品類型(彈性體、流體有機矽等)、應用(變壓器、開關設備)和地區分類

2024-2032 年重型機械市場中的有機矽依產品類型(彈性體、流體有機矽等)、應用(變壓器、開關設備)和地區分類 全球有機矽市場 - 2024-2031

全球有機矽市場 - 2024-2031 2030 年汽車矽膠市場預測:按產品、應用和地區分類的全球分析

2030 年汽車矽膠市場預測:按產品、應用和地區分類的全球分析 2024-2032 年按產品類型(彈性體、流體、凝膠、樹脂)、應用(工業流程、建築材料、家庭和個人護理、交通、能源、醫療保健、電子等)和地區分類的有機矽市場報告

2024-2032 年按產品類型(彈性體、流體、凝膠、樹脂)、應用(工業流程、建築材料、家庭和個人護理、交通、能源、醫療保健、電子等)和地區分類的有機矽市場報告 多芯矽膠電纜市場報告:2030 年趨勢、預測與競爭分析

多芯矽膠電纜市場報告:2030 年趨勢、預測與競爭分析 2024 年電氣和電子領域矽膠全球市場報告

2024 年電氣和電子領域矽膠全球市場報告 2024-2028年矽膠全球市場

2024-2028年矽膠全球市場 汽車矽膠市場2024年全球市場報告

汽車矽膠市場2024年全球市場報告 二甲基環矽氧烷市場:按產品類型、等級和應用分類 - 2024-2030 年全球預測

二甲基環矽氧烷市場:按產品類型、等級和應用分類 - 2024-2030 年全球預測 晶片平台即服務市場:按類型、按應用分類 - 2024-2030 年全球預測

晶片平台即服務市場:按類型、按應用分類 - 2024-2030 年全球預測