|

市場調查報告書

商品編碼

1444142

指紋感應器:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Fingerprint Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

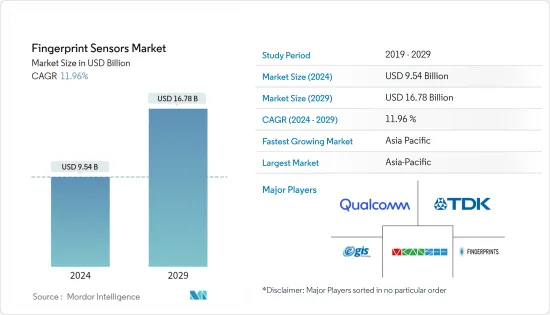

指紋感應器市場規模預計到 2024 年為 95.4 億美元,預計到 2029 年將達到 167.8 億美元,預測期內(2024-2029 年)年複合成長率為 11.96%。

指紋感應器市場在過去幾年中迅速擴大,預計在預測期內將進一步擴大。智慧型手機普及的不斷提高、安全應用數量的增加以及政府採用生物識別的舉措往往是推動全球指紋感測器需求的主要因素。

主要亮點

- 指紋是各種設備和應用領域中使用的典型生物識別之一,這就是指紋感應器的需求不斷增加的原因。此外,生物辨識研究所 2021 年 6 月對全球 360 名受訪者進行的調查顯示,56% 的歐洲受訪者同意有關生物辨識的嚴格法律。

- 配備指紋感應器的智慧型手機的日益普及是指紋感應器成長的顯著促進因素之一。例如,根據Counterpoint的報告,2021年第一季,三星等智慧型手機全球出貨量約7,700萬部,iPhone全球出貨總計為5,700萬部。

- 因此,平板電腦、筆記型電腦、智慧型手機和智慧型穿戴裝置等智慧型裝置的人均數量預計在未來幾年將會增加。這些設備擴大包含指紋感應器。據思科稱,2018年人均網路設備數量為8台,預計2022年將達到每人13.6台。

- 由於高速網路普及影響力不斷擴大,智慧型手機的滲透率正在急劇上升,預計隨著5G的到來,智慧型手機的普及將進一步提高。根據 GSMA 的數據,到 2025 年,北美智慧型手機用戶數量預計將達到 3.28 億。此外,到 2025 年,該地區的行動用戶普及(86%) 和網路普及率 (80%) 可能會提高。此外,根據 GSMA 的數據,預計到 2025 年,歐洲將擁有最高的網路普及(82%) 和智慧型手機普及率 (88%)。

- 臉部辨識系統在各種設備中變得越來越普遍。例如,Apple、Samsung 和 OnePlus 等主要智慧型手機供應商已經內建了這種使用者驗證功能。這種替代技術的日益普及可能會阻礙指紋感測器市場的成長。

- COVID-19 大流行增加了對智慧型手機、筆記型電腦、個人電腦和平板電腦等消費性電器產品的需求。例如,根據 RBC.ru 報導,2020 年 3 月疫情期間俄羅斯筆記型電腦銷量有所成長,增幅達 50%。

指紋感應器市場趨勢

智慧型手機應用程式預計將佔據很大佔有率

- 在研究中考慮的所有其他設備中,智慧型手機是利用指紋感應器進行使用者身份驗證的最大部分。東芝於 2011 年首次將指紋感應器應用於智慧型手機,但 Apple Touch ID 徹底改變了行動裝置中的指紋感應器。

- Apple 的 Touch ID 基於電容技術,準確且易於使用,使用戶身份驗證快速且流暢。在蘋果成功之後,三星和其他大公司也開始使用各種指紋技術進行身份驗證。

- 在技術方面,電容式觸控螢幕感應器正在被高階行動電話中的超音波指紋感應器和其他設備中的光學感應器所取代。放棄電容式感測器是由於將感測器整合到顯示器中的需求不斷增加。

- 另一方面,平板電腦使用電容式感應器,許多小型製造商選擇不在平板電腦上使用指紋感應器以保護邊框。然而,三星、聯想和華碩等公司在其平板電腦中使用電容式感測器。

- 智慧型手機的日益普及預計將在所研究的市場中創造更多機會。例如,《2021 年愛立信行動報告》顯示,新智慧型手機用戶數量超過 55 億。

亞太地區將經歷最高成長

- 中國行動交易的成長,加上政府的舉措,預計將成為該國指紋感測器市場的主要驅動力。中國的移動交易量正在迅速增加,預計這將為所研究的市場創造潛力。

- 根據中國網際網路絡資訊中心(CNNIC)的數據,2020年約有8.525億用戶使用行動付款交易,高於2018年的5.833億。行動付款交易的增加增加了對各種指紋感應器的需求。

- 該公司持續的產品創新主要推動了日本指紋掃描器市場的發展。例如,2021 年 7 月,Fingerprint Cards 與東京公司 MorX 合作,在日本開發並推出生物識別付款卡。該卡具有超低功耗,配備客製化的指紋T型模組,採用標準自動化製造技術整合到支付卡中。在非接觸式付款卡中添加生物識別感測器可以增加卡片支付,同時提高安全性、清潔度和衛生性。

- 日本汽車產業的公司也積極期待將指紋感應器整合到他們的下一代車型中。例如,日產推出了採用指紋生物識別的 Nissan Xmotion 概念車,以增強車輛安全性。

- 在生物識別,付款卡市場強勁,由於生物辨識付款卡需求不斷增加,指紋感應器的需求大幅增加。目前,各種市場供應商正在致力於整合生物識別技術。他們將提供真正顛覆性的服務,從而顯著擴大銀行在國內、各種最終用戶甚至其他地區的客戶群。

指紋感應器產業概況

指紋感應器市場較為分散,高通、Fingerprint Card AB 和 Synaptics 等國際公司透過在各種智慧型手機中部署其解決方案佔據了主要市場佔有率。指紋感應器公司正在開發智慧型手機以外的新市場,甚至進入物聯網領域,將指紋感應器整合到智慧卡中。我們不斷整合不同的技術來改善最終用戶體驗。

- 2022 年 1 月 - Vivo 推出的 IQOO 9 Pro 是首款配備高通 3D Sonic Max超音波指紋辨識器的智慧型手機,並搭載最新的 Snapdragon 8 Gen 1 處理器。 IQOO 9 Pro 上的 Qualcomm 3D Sonic Max 只需輕輕一按即可實現超快速的指紋註冊流程。用戶指紋註冊後,只需 0.2 秒即可解鎖。

- 2021 年 9 月 - IDEMIA 推出 IDEMIA STORM ABIS,這是一個基於 SaaS 的自動生物識別系統 (ABIS),可實現直覺、可存取且經濟實惠的指紋分析、比較和記錄。 IDEMIA STORM ABIS 透過比較、分析和案例管理工具支援本地和國家搜尋,使指紋檢查員能夠在任何地方有效且有效率地完成測試。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 研究假設和市場定義

- 調查範圍

第2章調查方法

- 調查系統

- 二次調查

- 初步調查

- 對資料進行三角測量並產生見解

第3章執行摘要

第4章市場洞察

- 市場概況

- 產業吸引力-波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 競爭程度

- 替代產品的威脅

- 產業價值鏈分析

- 評估 COVID-19 的影響

第5章市場動態

- 市場促進因素

- 智慧型穿戴裝置和智慧型手機擴大使用指紋感應器

- 對安全保障和業務應用程式的需求

- 政府努力在各個領域引入生物辨識技術

- 市場限制因素

- 更多採用臉部和虹膜掃描等替代技術

第6章市場區隔

- 按類型

- 光學

- 電容

- 熱

- 超音波

- 按用途

- 智慧型手機/平板電腦

- 筆記型電腦

- 智慧卡

- 物聯網/其他應用

- 按最終用戶產業

- 軍事/國防

- 消費性電子產品

- BFSI

- 政府

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太地區

- 拉丁美洲

- 中東和非洲

- 北美洲

第7章 競爭形勢

- 公司簡介

- Qualcomm Technologies, Inc.

- TDK Corporation

- Vkansee Technology Inc.

- Egis Technology Inc.

- Fingerprint Cards AB

- Shenzhen Goodix Technology Co. Ltd

- Idex Biometrics ASA

- NEC Corporation

- Next Biometrics Group ASA

- Synaptics Inc.

- Thales Group(Gemalto NV)

- Idemia France SAS

- Crucialtec Co Ltd.

- Sonavation Inc.

第8章投資分析

第9章市場的未來

The Fingerprint Sensors Market size is estimated at USD 9.54 billion in 2024, and is expected to reach USD 16.78 billion by 2029, growing at a CAGR of 11.96% during the forecast period (2024-2029).

The fingerprint sensors market has expanded rapidly over the past few years and is projected to increase even further during the forecast period. Increased adoption of smartphones, increasing security applications, and government initiatives to adopt biometrics tend to be the key factors driving the demand for fingerprint sensors globally.

Key Highlights

- The fingerprint is among the prominent type of biometrics used in various devices and application fields, owing to which the demand for fingerprint sensors is on the rise. Moreover, according to the survey carried out by Biometrics Institute for 360 respondents across the globe in June 2021, 56% of the respondents from Europe agree with strict legislation concerning biometrics.

- The growing penetration of smartphones, which are equipped with fingerprint sensors, is among the prominent driver of the growth of fingerprint sensors. For instance, as reported by counterpoint, In Q1 of 2021, the shipment of smartphones like Samsung accounted for approximately 77 million globally, and loads of iPhones globally accounted for 57 million.

- In line with that, the number of intelligent devices, such as tablets, laptops, smartphones, and smart wearables per person, is expected to increase over the coming years; these devices are increasingly being incorporated with fingerprint sensors. According to Cisco, in 2018, the number of networked devices per person stood at eight and is expected to reach 13.6 per person by 2022.

- The penetration of smartphones is increasing exponentially, owing to the increasing influence of fast internet access, and with the advent of 5G, smartphone penetration is expected to increase even further. According to GSMA, the number of smartphone subscribers in North America is expected to reach 328 million by 2025. Moreover, by 2025, the region may witness an increase in the penetration rates of mobile subscribers (86%) and the internet (80%). Additionally, according to GSMA, by 2025, Europe is estimated to register the highest internet penetration rate (82%) and smartphones (88%).

- Facial recognition systems are increasingly becoming common in various devices. For instance, major smartphone vendors, such as Apple, Samsung, and OnePlus, have already incorporated this user authentication. This increase in the adoption of substitute technology can hamper the growth of the fingerprint sensors market.

- The COVID-19 pandemic has increased the demand for consumer electronics such as smartphones, laptops, PCs, and tablets. For instance, the sale of notebooks grew in Russia amid the pandemic in March 2020 and accounted for a growth of 50%, according to RBC.ru.

Fingerprint Sensors Market Trends

Applications in Smartphones is expected to Hold a Major Share

- The smartphone is the largest segment to utilize fingerprint sensors for user authentication among all the other devices considered in the study. The earliest application of fingerprint sensors in smartphones was in 2011 by Toshiba, but Apple touch ID revolutionized fingerprint sensors in mobile devices.

- Apple's Touch ID, based on capacitive technology, was accurate and easy to use, because of which the authentication of the user became fast and smooth. After Apple's success, Samsung and other major players also started using different fingerprint technologies for authentication.

- Regarding technology, the capacitive touchscreen sensors are being replaced by ultrasonic fingerprint sensors in premium phones and optical sensors in the rest of the devices. The shift from capacitive sensors has been due to the growing demand to integrate sensors in the display.

- On the other hand, Tablets have been using capacitive sensors, and many times to keep the bezels, many small manufacturers have opted not to use fingerprint sensors on their tablets. However, companies like Samsung, Lenovo, and Asus, have been using capacitive sensors in their tablets.

- The increasing penetration of smartphones is expected to create more opportunities in the studied market. For instance, Ericsson Mobility Report 2021 shows more than 5.5 billion new smartphone subscriptions.

Asia Pacific to Witness Highest Growth

- Increasing mobile transactions in China, coupled with the government's initiatives, are expected to be the major drivers for the fingerprint sensors market in the country. China is witnessing a high mobile transactional volume, expected to create the potential for the market studied.

- According to the China Internet Network Information Center (CNNIC), in 2020, around 852.5 million users used mobile payment transactions, which increased from 583.3 million users in 2018. such an increase in mobile payment transactions provides an increasing need for various fingerprint sensors.

- The company's continuous product innovations primarily drive the market for fingerprint scanners in Japan. For instance, in July 2021, Fingerprint Cards collaborated with Tokyo-based company MoriX Co. Ltd to develop and launch biometric payment cards in Japan. Fingerprints' T-Shape module, which boasts ultra-low power consumption and is customized to be integrated into payment cards using standard automated manufacturing techniques, will be featured on the cards. Adding biometric sensors to contactless payment cards improves security, cleanliness, and sanitation while increasing card payment.

- The Japanese companies in the automotive sector are also actively looking forward to integrating fingerprint sensors in their upcoming models. For instance, Nissan introduced its concept car Nissan Xmotion featured fingerprint biometric authentication for enhanced security of the vehicles.

- Fingerprint sensors are witnessing a significant demand in South Korea due to the increasing demand for biometric payment cards, and there is a robust market for payment cards. Various market vendors are currently working to integrate biometric technology. They will have a genuinely disruptive offering that will significantly expand the banking customer base in the country, various end-users, and beyond.

Fingerprint Sensors Industry Overview

The fingerprint sensor market is fragmented, with individual international companies such as Qualcomm, Fingerprint Card AB, and Synaptics occupying a significant market share by deploying their solutions in various smartphones. Fingerprint sensor firms are unlocking new markets beyond smartphones, exploring even the IoT field, and integrating fingerprint sensors into smart cards. They are constantly incorporating different technologies to enhance the end-user experiences.

- January 2022 - The Vivo launched IQOO 9 Pro is the first smartphone to include Qualcomm's 3D Sonic Max ultrasonic fingerprint reader and is powered by the brand-new Snapdragon 8 Gen 1 processor. The IQOO 9 Pro's Qualcomm 3D Sonic Max enables a lightning-fast fingerprint enrollment process with just one tap. Once the user fingerprint is registered, it unlocks the phone in just 0.2 seconds.

- September 2021- IDEMIA launched the SaaS-based Automated Biometric Identification System (ABIS), IDEMIA STORM ABIS, for intuitive, accessible, affordable fingerprint analysis, comparison, and documentation. IDEMIA STORM ABIS supports local and national searches through tools for comparison, analysis, and case management that permits fingerprint examiners to effectively and efficiently complete examinations from anywhere.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Research Framework

- 2.2 Secondary Research

- 2.3 Primary Research

- 2.4 Data Triangulation and Insight Generation

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of New Entrants

- 4.2.4 Degree of Competition

- 4.2.5 Threat of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment Of COVID-19 Impact

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Usage of Fingerprint Sensors for Smart Wearable Devices and Smartphones

- 5.1.2 Need for Secured Security and Business Applications

- 5.1.3 Government Initiatives to Adopt Biometrics in Various Fields

- 5.2 Market Restraints

- 5.2.1 Increase in Adoption of Substitute Technologies, such as Face and Iris Scanning

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Optical

- 6.1.2 Capacitive

- 6.1.3 Thermal

- 6.1.4 Ultrasonic

- 6.2 By Application

- 6.2.1 Smartphones/Tablets

- 6.2.2 Laptops

- 6.2.3 Smartcards

- 6.2.4 IoT and Other Applications

- 6.3 By End-User Industries

- 6.3.1 Military and Defense

- 6.3.2 Consumer Electronics

- 6.3.3 BFSI

- 6.3.4 Government

- 6.3.5 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 South Korea

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle-East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Technologies, Inc.

- 7.1.2 TDK Corporation

- 7.1.3 Vkansee Technology Inc.

- 7.1.4 Egis Technology Inc.

- 7.1.5 Fingerprint Cards AB

- 7.1.6 Shenzhen Goodix Technology Co. Ltd

- 7.1.7 Idex Biometrics ASA

- 7.1.8 NEC Corporation

- 7.1.9 Next Biometrics Group ASA

- 7.1.10 Synaptics Inc.

- 7.1.11 Thales Group (Gemalto NV)

- 7.1.12 Idemia France SAS

- 7.1.13 Crucialtec Co Ltd.

- 7.1.14 Sonavation Inc.

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET

2024-2032 年按類型、技術、應用和地區分類的指紋感測器市場報告

2024-2032 年按類型、技術、應用和地區分類的指紋感測器市場報告 指紋感應器市場:按類型、感測器技術、應用產業分類 - 2024-2030 年全球預測

指紋感應器市場:按類型、感測器技術、應用產業分類 - 2024-2030 年全球預測 全球指紋感應器市場規模、佔有率、趨勢分析報告:按技術、產業和地區分類的展望與預測,2023-2030年

全球指紋感應器市場規模、佔有率、趨勢分析報告:按技術、產業和地區分類的展望與預測,2023-2030年 2024 年指紋感應器全球市場報告

2024 年指紋感應器全球市場報告 指紋感測器市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測

指紋感測器市場:2023-2028年全球行業趨勢、佔有率、規模、成長、機會和預測 指紋感測器的全球市場 (2023-2028年):趨勢、成長機會、競爭分析

指紋感測器的全球市場 (2023-2028年):趨勢、成長機會、競爭分析 指紋感測器的全球市場:市場規模 - 各類型,各技術,各用途,各地區展望,競爭策略,各市場區隔預測(~2032年)

指紋感測器的全球市場:市場規模 - 各類型,各技術,各用途,各地區展望,競爭策略,各市場區隔預測(~2032年) 指紋感測器的全球市場預測(2022年~2027年)

指紋感測器的全球市場預測(2022年~2027年) 全球指紋傳感器市場 (2022-2028):按技術、產品類型、材料、產品、最終用戶和傳感器技術分列的規模、份額、增長分析和預測

全球指紋傳感器市場 (2022-2028):按技術、產品類型、材料、產品、最終用戶和傳感器技術分列的規模、份額、增長分析和預測 全球指紋傳感器市場:規模、細分市場、展望、收入預測2022-2028年、按類型、應用、用戶行業、地區(北美、歐洲、亞太、拉美、中東和非洲)

全球指紋傳感器市場:規模、細分市場、展望、收入預測2022-2028年、按類型、應用、用戶行業、地區(北美、歐洲、亞太、拉美、中東和非洲)