|

市場調查報告書

商品編碼

1443998

金屬罐 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Metal Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

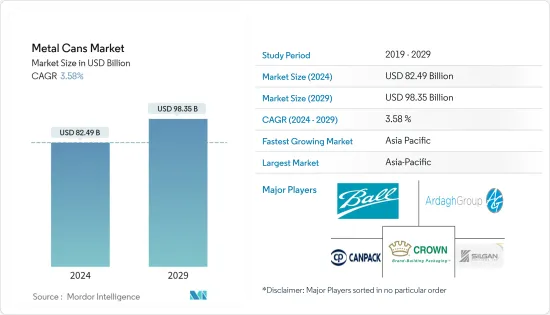

金屬罐市場規模預計到2024年為824.9億美元,預計到2029年將達到983.5億美元,在預測期內(2024-2029年)CAGR為3.58%。

該產品因其獨特的特點而受到關注,如耐運輸、密封蓋、粗暴搬運和易於回收。

主要亮點

- 金屬罐的高可回收性是市場的重要驅動力之一。鋁罐幾乎可以提供防潮保護。這些罐子不生鏽、耐腐蝕,並且是任何包裝中保存期限最長的罐子之一。它還具有許多優點,例如剛性、穩定性和高阻隔性。

- 由於歐洲地區啤酒和碳酸飲料等酒精和非酒精飲料的消費量不斷增加,對金屬罐的需求量很大。根據Barth-Haas Group的數據,2021年德國是歐洲最大的啤酒生產國。德國的啤酒產品產量超過8,500萬公升,是英國產量的兩倍多。俄羅斯產量為 8,200 萬公升,位居歐洲第二。

- 鋁罐短缺繼續影響食品和飲料行業,因為與餐廳相比,家庭消費和雜貨的飲料需求增加。許多知名市場參與者已宣布投資建立新的製造基礎設施,以滿足增加的訂單並解決鋁罐短缺。例如,2021年9月,鮑爾公司宣布計劃在美國內華達州新建一座美國鋁製飲料包裝工廠。該多線工廠計劃於 2022 年底開始生產。該公司計劃在未來幾年內對該工廠投資約 2.9 億美元。即使進行了調整並提高了製造能力,波爾公司預計,到 2023 年,需求仍將繼續超過供應。

- 消費者對在包裝中應用非致癌材料的意識的提高以及對輕質包裝的需求增加正在為金屬罐市場帶來高成長前景。然而,由於聚乙烯和聚對苯二甲酸乙二醇酯 (PET) 等聚合物包裝材料的替代可能性,金屬罐的使用具有課題性。

- 為了因應COVID-19大流行對需求的影響,歐洲鋼鐵製造商迅速減少供應,第一季產量較去年同期下降10%。此外,有色金屬產業是食品包裝等重要價值鏈的重要供應商。由於關鍵價值鏈需求大幅減少、供應中斷和運輸困難,COVID-19 正在對歐洲有色金屬產業造成重大且日益嚴重的經濟影響。

金屬罐市場趨勢

罐頭食品消費推動市場成長

- 全球生活方式的變化促使消費者選擇易於烹飪的食物。年輕人口和個體消費者消費更多的罐頭食品。這些使用者時間較少,預算有限,因此會選擇成本較低、便利性較高的產品。

- 許多罐頭食品的普通消費者選擇該產品是因為其方便且成本較低。罐頭食品食用較方便,烹調所需的能量和時間較少。大多數罐頭食品的準備時間比一般餐點少 40%。

- 此外,大流行後市場對植物性食品的需求顯著增加。由於英國是越南植物性產品的主要市場,越南素食食品出口商正在探索充足的機會。例如,2022年8月,在英國最大的越南商品進口國倫敦的支持下,位於同塔省的Binh Loan素食工廠向英國出口了2噸罐頭素食食品。

- 現代便利商店和超市在全國範圍內的擴張已經加速,這可能會增加所研究市場的成長。例如,2022年7月,零售巨頭WinCommerce計劃在年底前在越南開設數百家新超市和便利商店,以滿足簡便食品日益成長的需求,並加速擴大其市場佔有率在國內。

- 此外,2021 年 10 月,北美食品和家居用品鋼罐製造商 Ball Metalpack 在其密爾瓦基製造工廠新增了一條兩片式食品罐生產線。這條新鮮、高速兩片式食品罐生產線將支援每年數百萬個食品罐的生產,並使 Ball Metalpack 能夠滿足食品和營養行業客戶不斷成長的需求。這是密爾瓦基工廠的第二條高速兩件式生產線,使其能夠擁有更快的投產時間和更低的總成本結構。 Ball Metalpack 在其北美八家工廠擁有四種高速兩片罐。

- 此外,根據 StatCan 的數據,過去十年中新鮮和加工水果和蔬菜的供應量有所下降。因此,人們正在轉向罐頭食品。

- 第三大生活支出是食品。罐頭食品通常比新鮮或冷凍食品便宜,成本大約是冷凍食品的一半,是冷凍新鮮食品的五分之一。此外,加拿大人口的成長速度超過了這些成長速度,導致人均罐頭食品的供應量較低。例如,根據 StatCan 的數據,加拿大人均可消費的烘焙豆和罐裝豆量已從 2013 年的 1.13 公斤下降到 2021 年的 0.92 公斤。

北美將在市場中佔據重要佔有率

- 由於對不同健康飲料、碳酸軟性飲料、保健飲料和三氯蔗糖果汁的需求不斷成長,預計北美將在整個預測期內對金屬罐的需求產生積極影響。此外,一些重要的參與者透過廣泛的促銷活動和新的研究影響著業務的發展。

- 食品和零售業是影響美國產品需求的主要因素。該國的雜貨店和超市比以往任何時候都多,該國食品和零售業的擴張主要是由於小型住宅數量的增加。因此,它推動了對較小包裝單位的需求。

- 由於美國的生活方式,對金屬罐的需求更大。人們選擇即食且可以快速製作的有益健康的食物,因為他們的日程繁忙,幾乎沒有時間做飯。透過提供簡單的包裝和即用食品,罐頭食品實現了這一目標。由於金屬罐可以長時間保持食物新鮮和高品質,因此將推動市場成長。

- 此外,該地區的參與者正在關注垂直和水平整合。例如,2021年11月,Ardagh集團子公司Ardagh Metal Packaging (AMP)收購了加拿大數位印刷罐供應商Hart Print。 Hart Print 成立於 2018 年,總部位於魁北克,為飲料市場客戶提供靈活的數位印刷解決方案。 Hart Print 聲稱是北美市場第一家提供數位印刷罐的公司。

金屬罐產業概況

由於全球和本地行業參與者的存在,金屬罐市場適度分散。該市場的供應商根據產品組合、差異化和定價參與。市場主要參與者有 SKS Bottle & Packaging, Inc.、Silgan Containers LLC、Ball Corporation 等。

2022 年3 月,德國馬口鐵製造商ThyssenKrupp Rasselstein 與瑞士公司Hoffmann Neopac 和Ricola 合作,推出了世界上第一個由減少二氧化碳排放的藍薄荷鋼製成的食品罐,後者將銷售罐裝草藥滴劑。

2022 年 1 月,Ardagh Metal Packaging Europe 推出了 HIGHEND,這是其客製化系列的新成員,為客戶提供提升品牌的創意機會。該技術可以在整個外殼表面上進行 CMYK 顏色的高品質裝飾,這意味著品牌可以以最大的視覺衝擊力突出、客製化和區分他們的罐子。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場動態

- 市場概況

- 市場促進因素

- 由於能源使用量較少,包裝的可回收性高

- 酒精和非酒精飲料的消費量增加

- 市場限制

- 替代包裝解決方案如聚對聚對苯二甲酸乙二酯的存在

- 產業價值鏈分析

- 產業吸引力-波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- COVID-19 對市場的影響

第 5 章:市場區隔

- 依材料類型

- 鋁

- 鋼

- 依罐頭類型

- 食物

- 飲料

- 化妝品和個人護理

- 藥品

- 畫

- 其他最終用戶產業

- 地理

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太

- 中國

- 印度

- 日本

- 亞太其他地區

- 澳洲

- 拉丁美洲

- 中東和非洲

- 北美洲

第 6 章:競爭情報

- 公司簡介

- Ball Corporation

- Ardagh Group

- Mauser Packaging Solutions

- Silgan Containers LLC

- Crown Holdings Inc.

- DS Containers Inc.

- CCL Container Inc.

- Toyo Seikan Group Holdings Ltd

- Pacific Can China Holdings Limited

- Universal Can Corporation

- CPMC HOLDINGS Limited (COFCO Group)

- Showa Denko KK

- Independent Can Company

- Hindustan Tin Works Ltd

- Saudi Arabian Packaging Industry WLL (SAPIN)

第 7 章:投資分析

第 8 章:市場機會與未來趨勢

The Metal Cans Market size is estimated at USD 82.49 billion in 2024, and is expected to reach USD 98.35 billion by 2029, growing at a CAGR of 3.58% during the forecast period (2024-2029).

The product is gaining prominence because of its distinct features, like transportation resistance, hermetically sealed cover, rough handling, and easy recyclability.

Key Highlights

- The high recyclability of metal cans is one of the significant drivers of the market. Aluminum cans deliver nearly protection against moisture. The cans do not rust and are resistant to corrosion, as well as provide one of the most extended shelf lives considering any packaging. It also offers many benefits, such as rigidity, stability, and high barrier properties.

- Due to the increasing consumption of alcoholic and non-alcoholic beverages, such as beer and carbonated drinks, in the European region, there is significant demand for metal cans. According to Barth-Haas Group, Germany was Europe's top beer producer in 2021. The beer products in Germany were over 85 million hl which was more than twice as much as produced in the UK. With 82 million hl, Russian output was the second-largest in Europe.

- The aluminum can shortage continues to affect the food and beverage industry, as the beverage demand for home consumption and grocery increased compared to restaurants. Many prominent market players have announced investments to set up new manufacturing infrastructures to fulfill the increased order and tackle the shortage of aluminum cans. For instance, in September 2021, Ball Corporation announced plans to build a new US aluminum beverage packaging plant in Nevada, US. This multi-line plant has been scheduled to begin production in late 2022. The company plans to invest around USD 290 million in this facility over the next few years. Even with the adjustments and increased manufacturing capacity, Ball Corporation anticipated that the demand would continue to outstrip supply well into 2023.

- The rise in consumer awareness concerning the application of non-carcinogenic materials in packaging and increased demand for lightweight packing is generating high growth prospects for the metal cans market. However, metal cans are challenging to use due to the replacement possibility of polymer-based packaging materials, including polyethylene and polyethylene terephthalate (PET).

- In response to the COVID-19 pandemic's impact on demand, European steelmakers have swiftly reduced supply, with first-quarter production falling 10% yearly. Also, the non-ferrous metals industry is a crucial supplier of essential value chains, including food packaging. COVID-19 is causing significant and growing economic impacts on the European non-ferrous metals sector, driven by substantial demand reduction in key-value chains, supply disruptions, and transport difficulties.

Metal Cans Market Trends

Canned Food Consumption to Drive the Market Growth

- The changing lifestyles at a global level are resulting in consumers opting for easy-to-cook food. The younger population and individually living consumers are consuming more canned food. These users have less time and are budget restrained, thus, opting for products with lower costs and higher convenience.

- Many regular consumers of canned foods choose the products due to the convenience offered and lower cost of the products. Canned foods are more convenient to consume and require less energy and time to cook. Most canned foods take 40% less time to prepare than regular meals.

- Also, the demand for plant-based foods has significantly increased in the market post-pandemic. Vietnam's vegetarian food exporters are exploring ample opportunities as the UK is the primary market for Vietnam for its plant-based products. For instance, in August 2022, Dong Thap Province-based Binh Loan vegetarian food factory exported two tonnes of canned vegetarian food to the UK with the support of London, the biggest importer of Vietnamese goods in the UK.

- The expansion of modern convenience stores and supermarkets across the country has geared up, which will likely add growth to the market studied. For instance, in July 2022, WinCommerce, a retail giant, plans to open hundreds of new supermarkets and convenience stores in Vietnam by the end of the year to cater to the increased demand for convenience food products and to accelerate the expansion of its market share in the country.

- Also, in October 2021, Ball Metalpack, a North American manufacturer of steel cans for food and household products, added a new two-piece food cans production line at its Milwaukee manufacturing plant. The fresh, high-speed two-piece food can production line will support the production of millions of food cans per year and allow Ball Metalpack to meet growing demand from customers in the food and nutrition industries. It is the second high-speed two-piece production line at the Milwaukee plant, enabling it to have a quicker ramp-up time and a lower total cost structure. Ball Metalpack has four high-speed two-piece cans across its eight North American plants.

- Additionally, according to StatCan, there has been a decline in fresh and processed fruit and vegetable availability over the past ten years. Therefore people are shifting to canned food.

- The third-largest living expenditure is food. Canned food is frequently less expensive than fresh or frozen food, costing approximately half as much as frozen and a fifth as much as frozen fresh. Also, the population of Canada's growth outpaced these increases, yielding lower per capita availability of canned food. For instance, according to StatCan, the baked and canned beans volume available for consumption per person in Canada has declined from 1.13 kg in 2013 to 0.92 kg in 2021.

North America to Hold a Significant Share in the Market

- North America is anticipated to positively influence the demand for metal cans throughout the forecast period due to the growing demand for different healthy beverages, carbonated soft drinks, health drinks, and sucralose juices. Additionally, several significant players impact the business's development through extensive promotional efforts and new research.

- The food and retail industries are the primary factors influencing the demand for products in the United States. The country has more grocery shops and superstores than ever before, and the expansion of the country's food and retail industries is primarily due to the rise in the number of smaller homes. Consequently, it is driving demand for smaller packing units.

- Because of the way of life in the United States, there is a greater need for metal cans. People choose wholesome food that is ready to eat and can make it quickly since they have hectic schedules that leave them with little time for cooking. By offering easy packaging and foods that are ready to use, canned food accomplishes this goal. Because they can keep food fresh and high-quality for an extended period, metal cans will boost the market growth.

- Additionally, players in the region are focusing on vertical and horizontal integration. For instance, in November 2021, Ardagh Metal Packaging (AMP), a subsidiary of Ardagh Group, acquired Canada-based digital printed cans provider Hart Print. Hart Print was established in 2018 and is based in Quebec, offering flexible digital printing solutions to customers serving the beverage market. Hart Print claims to be the first company to provide digitally printed cans in the North-American market.

Metal Cans Industry Overview

The metal cans market is moderately fragmented, owing to the presence of various global and local industry players. Vendors in this market participate based on product portfolio, differentiation, and pricing. Key players in the market are SKS Bottle & Packaging, Inc., Silgan Containers LLC, Ball Corporation, etc.

In March 2022, the German tinplate manufacturer ThyssenKrupp Rasselstein had the world's first food can made of CO2-reduced blue mint Steel, in collaboration with the Swiss companies Hoffmann Neopac and Ricola, the latter of which will sell its herbal drops in the cans.

In January 2022, Ardagh Metal Packaging Europe launched HIGHEND, a new addition to its customization range, which offers customers brand-enhancing creative opportunities. The technology allows high-quality decoration in CMYK colors on the entire shell surface, meaning brands can highlight, customize and differentiate their cans with maximum visual impact.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Recyclability of the Packaging Due to Less Usage of Energy

- 4.2.2 Increasing Consumption of both Alcoholic and Non-Alcoholic Beverages

- 4.3 Market Restraints

- 4.3.1 Presence of Alternate Packaging Solutions as Polyethylene Terephthalate

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Material Type

- 5.1.1 Aluminum

- 5.1.2 Steel

- 5.2 By Can Type

- 5.2.1 Food

- 5.2.2 Beverage

- 5.2.3 Cosmetics and Personal Care

- 5.2.4 Pharmaceuticals

- 5.2.5 Paint

- 5.2.6 Other End user Industry

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Spain

- 5.3.2.5 Italy

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Rest of Asia-Pacific

- 5.3.3.5 Australia

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE INTELLIGENCE

- 6.1 Company Profiles

- 6.1.1 Ball Corporation

- 6.1.2 Ardagh Group

- 6.1.3 Mauser Packaging Solutions

- 6.1.4 Silgan Containers LLC

- 6.1.5 Crown Holdings Inc.

- 6.1.6 DS Containers Inc.

- 6.1.7 CCL Container Inc.

- 6.1.8 Toyo Seikan Group Holdings Ltd

- 6.1.9 Pacific Can China Holdings Limited

- 6.1.10 Universal Can Corporation

- 6.1.11 CPMC HOLDINGS Limited (COFCO Group)

- 6.1.12 Showa Denko KK

- 6.1.13 Independent Can Company

- 6.1.14 Hindustan Tin Works Ltd

- 6.1.15 Saudi Arabian Packaging Industry WLL (SAPIN)

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

2024-2032 年按材料類型(鋁、鋼、錫)、製造(兩片金屬罐、三片金屬罐)、罐類型(食品、飲料、氣霧劑等)和地區分類的金屬罐市場報告

2024-2032 年按材料類型(鋁、鋼、錫)、製造(兩片金屬罐、三片金屬罐)、罐類型(食品、飲料、氣霧劑等)和地區分類的金屬罐市場報告 2024年全球食品和飲料金屬罐市場報告

2024年全球食品和飲料金屬罐市場報告 2023-2030年全球食品和飲料金屬罐市場規模研究與預測(按材料、類型、內壓程度、應用和區域分析)

2023-2030年全球食品和飲料金屬罐市場規模研究與預測(按材料、類型、內壓程度、應用和區域分析)![金屬罐市場[產品:食品(水果、蔬菜、湯等)、飲料(碳酸飲料、酒精飲料、新飲料、蔬果汁)等]-全球產業分析、規模、佔有率、成長、趨勢,2023-2031 年預測](/sample/img/cover/42/1402832.png) 金屬罐市場[產品:食品(水果、蔬菜、湯等)、飲料(碳酸飲料、酒精飲料、新飲料、蔬果汁)等]-全球產業分析、規模、佔有率、成長、趨勢,2023-2031 年預測

金屬罐市場[產品:食品(水果、蔬菜、湯等)、飲料(碳酸飲料、酒精飲料、新飲料、蔬果汁)等]-全球產業分析、規模、佔有率、成長、趨勢,2023-2031 年預測 金屬罐、桶、桶和提桶市場:按材料、最終用戶和應用分類 - 2023-2030 年全球預測

金屬罐、桶、桶和提桶市場:按材料、最終用戶和應用分類 - 2023-2030 年全球預測 非食品和非飲料金屬罐市場報告:到 2030 年的趨勢、預測和競爭分析

非食品和非飲料金屬罐市場報告:到 2030 年的趨勢、預測和競爭分析 食品和飲料金屬罐的全球市場

食品和飲料金屬罐的全球市場 食品和飲料金屬罐市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029

食品和飲料金屬罐市場-全球市場規模、佔有率、趨勢分析、機遇和預測報告,2019-2029 食品飲料用金屬罐全球市場:按材料(鋁,鋼罐)按類型(兩片,三片罐)按內壓程度(加壓,真空罐)按應用(食品飲料罐)飲料)以及按地區劃分未來預測(直到2028)

食品飲料用金屬罐全球市場:按材料(鋁,鋼罐)按類型(兩片,三片罐)按內壓程度(加壓,真空罐)按應用(食品飲料罐)飲料)以及按地區劃分未來預測(直到2028) 金屬罐和玻璃瓶市場:按配銷通路、最終用戶、用途分類 - 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測

金屬罐和玻璃瓶市場:按配銷通路、最終用戶、用途分類 - 俄羅斯-烏克蘭衝突、高通貨膨脹的累積影響 - 2023-2030 年全球預測