|

市場調查報告書

商品編碼

1441610

液化天然氣燃料庫:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)LNG Bunkering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

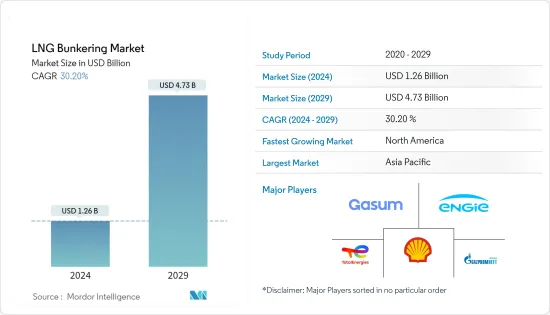

液化天然氣燃料庫市場規模預計到 2024 年為 12.6 億美元,預計到 2029 年將達到 47.3 億美元,預測期內(2024-2029 年)年複合成長率為 30.20%。

在COVID-19感染疾病期間,由於臨時進出口禁令,市場低迷。然而,由於航運對液化天然氣作為船用燃料的需求不斷增加,市場從 2021 年下半年的收益下降中恢復過來。在市場成長方面,限制傳統燃料硫含量的標準和提高效率正在推動對液化天然氣燃料庫基礎設施的需求。各地船舶逐漸開始採用液化天然氣作為推進燃料。此外,減少傳統燃料中的硫含量可能成本高且不經濟。

主要亮點

- 在預測期內,油輪船隊可能會顯著成長。

- 與傳統船用燃料相比,液化天然氣作為船用燃料具有巨大的優勢,從延長合規期到減少溫室氣體排放。隨著IMO法規的實施,船舶將改用硫含量較低的燃料,使液化天然氣成為理想的選擇,並為燃料庫市場帶來機會。

- 大部分需求來自美國和加拿大,其中北美預計將主導市場。

液化天然氣(LNG)燃料庫市場趨勢

油輪船隊顯著成長

- 油輪船隊包括小型油輪、中型油輪、中程1號(MR1)、中程2號(MR2)、大型油輪1號(LR1)、大型油輪2號(LR2)、超大型原油裝運船隻( VLCC)和超大型油輪. 包括油輪。大型原油裝運船隻(ULCC) 的油輪容量各不相同。

- 油輪船隊用於儲存或運輸大量氣體/液體。它們用於儲存和運輸石油、天然氣、化學品和其他產品,如植物油、淡水、酒和糖蜜。

- 2020年,國際海事組織對全球燃油硫含量實施新的0.5%上限,低於先前的3.5%,以限制海上活動產生的溫室氣體排放。液化天然氣作為船用燃料比其他類型的船用燃料具有顯著優勢,包括減少高達 80% 的氮氧化物排放並消除硫氧化物顆粒物,而最新的引擎技術可最大程度減少 23% 的溫室氣體排放。運作具競爭力的設計的液化天然氣船舶將確保比傳統設計更長期的合規性。這些因素導致擴大採用液化天然氣作為船用燃料,並增加油輪運輸液化天然氣。

- 截至年終,液化天然氣船隊總數為642艘,總作業量為9,340萬立方公尺。 2020年,製造商又交付了47艘船舶,並訂購了40艘新油輪。到2020年,訂單量將達到147台、2,270萬立方公尺。

- 因此,對燃料中硫含量的監管預計將使液化天然氣成為未來幾年海上活動的首選燃料,從而導致油輪運輸液化天然氣船用燃料的增加。

北美市場佔據主導地位

- 在預測期內,北美地區可能會主導液化天然氣燃料庫市場,其中大部分需求來自美國和加拿大。

- 推動液化天然氣燃料庫市場的主要因素是航運業對液化天然氣減少碳排放的需求不斷增加。此外,液化天然氣是一種更好的替代燃料,各國政府正在推動液化天然氣適應工作。

- 2020年,國際海事組織實施了降低船用燃料硫含量的措施,以遏制海上活動產生的溫室氣體排放。由於這一因素,IMO後的液化天然氣很可能成為船用燃料的經濟替代品,美國液化天然氣燃料庫市場預計在未來幾年將成長。

- 2022年1月,美國造船公司芬坎蒂尼灣造船公司開始建造美國最大的液化天然氣燃料庫駁船。該LNG燃料庫駁船由一艘長126.8公尺的船舶組成,可容納12,000立方公尺的LNG。計劃預計完工日期為2023年。

- 此外,2021年9月,穩定解決方案與德克薩斯州伊莎貝爾港物流海上碼頭和路易斯安那州卡梅倫教區港口碼頭區簽署了一份合作備忘錄(MoU),以開發船舶液化天然氣加註服務。

- 同樣,2021年4月,惠生海工訂單Pilot LNG位於加拿大加爾維斯頓液化天然氣加註港計劃的前端工程開發(FEED)契約,計劃於2024年開始營運。

- 加拿大政府致力於大幅減少溫室氣體排放,且該國擁有豐富的天然氣供應。燃燒天然氣產生的溫室氣體排放較少,使液化天然氣成為加拿大航運業的絕佳替代船用燃料。

- 儘管液化天然氣船舶的初始安裝成本較高,但營運成本低於運行帶有洗滌器的舊船舶。因此,北美地區可能在預測期內主導整個液化天然氣燃料庫市場。

液化天然氣(LNG)燃料庫產業概述

液化燃料庫市場適度整合。主要企業包括殼牌公司、Gazprom Neft PJSC、TotalEnergies SE、Gasum Oy 和 Engie SA。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查範圍

- 市場定義

- 調查先決條件

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2027年之前的市場規模與需求預測(百萬美元)

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 最終用戶

- 油輪船隊

- 貨櫃船隊

- 散貨和雜貨船隊

- 渡輪和 OSV

- 其他最終用戶

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 南美洲

第6章 競爭形勢

- 併購、合資、合作與協議

- 主要企業採取的策略

- 公司簡介

- Shell PLC

- ENN Energy Holdings Ltd

- Korea Gas Corporation

- Harvey Gulf International Marine LLC

- Gasum Oy

- Engie SA

- Gazprom Neft PJSC

- TotalEnergies SE

- Naturgy Energy Group SA

第7章市場機會與未來趨勢

The LNG Bunkering Market size is estimated at USD 1.26 billion in 2024, and is expected to reach USD 4.73 billion by 2029, growing at a CAGR of 30.20% during the forecast period (2024-2029).

During the COVID-19 pandemic, the market experienced a decline due to temporary bans on export and import. However, the market recovered from the declining revenues in the second half of 2021, owing to the rising demand for LNG as bunker fuel from maritime transport. In terms of market growth, the norms to restrict the sulfur content in conventional fuels and the increased efficiency are driving the demand for LNG bunkering infrastructure. The ships across various regions are slowly starting to adopt LNG as a fuel for propulsion. Moreover, reducing the sulfur content from conventional fuel requires high costs, which is likely to hamper its economic viability.

Key Highlights

- The tanker fleet segment is likely to witness significant growth during the forecast period.

- LNG as a bunker fuel presents immense benefits over conventional bunker fuel, ranging from increased length of compliance to reduced GHG emissions. With the IMO regulations in place, maritime vessels will be switching to less sulfur content fuel, making LNG an ideal choice and leading to opportunities in the bunkering market.

- North America is expected to dominate the market, with most of the demand coming from the United States and Canada.

Liquefied Natural Gas (LNG) Bunkering Market Trends

Tanker Fleet to Witness Significant Growth

- Tanker fleets include small tanker, intermediate tanker, medium-range 1 (MR1), medium-range 2 (MR2), large range 1 (LR1), large range 2 (LR2), very large crude carrier (VLCC), and ultra-large crude carrier (ULCC), which differ based on tanker capacity.

- Tanker fleets are used to store or transport gases/liquids in bulk amounts. These are used to store and carry oil, gas, chemicals, and other products, like vegetable oil, freshwater, wine, molasses, etc.

- In 2020, the International Maritime Organization enforced a new 0.5% global sulfur cap on fuel content, lowering from the earlier 3.5% to limit the greenhouse gas emissions from the marine activities. LNG as a bunker fuel presents significant advantages over other kinds of bunker fuels, such as reducing NOx emissions by up to 80% and eliminating SOx particulate matter, leading to a reduction in GHG emissions by up to 23% with modern engine technology. Vessels that run on LNG on a competitive design ensure longer compliance than conventional designs. These factors have led to increasing adoption of LNG as a bunker fuel and increasing transport of LNG through tankers.

- At the end of 2020, the total LNG tanker fleet consisted of 642 vessels with a total operational capacity of 93.4 million cubic meters. In 2020, 47 more vessels were delivered by the manufacturers and 40 new orders for tankers. The order book consisted of 147 units of 22.7 million cubic meters by 2020.

- Thus, with the regulations related to sulfur content in the fuel, LNG is projected to become a reliant fuel for maritime activity in the coming years, leading to the increased transportation of LNG bunker fuel through tankers.

North America to Dominate the Market

- The North American region is likely to dominate the LNG bunkering market during the forecast period, with most demand coming from the United States and Canada.

- The key factor driving the LNG bunkering market is the increased LNG demand to reduce the carbon footprint in the shipping industry. Furthermore, LNG is a better alternative fuel, and the governments have been taking initiatives for LNG adaptation.

- In 2020, the International Maritime Organization implemented the reduced sulfur content in bunker fuels to contain the GHG emission from maritime activity. Due to this factor, the US LNG bunkering market is expected to witness growth in the coming years, as LNG is likely to be an economical alternative for marine fuel after IMO's regulation.

- In January 2022, the US shipbuilder Fincantieri Bay Shipbuilding commenced the construction of the largest LNG bunkering barge in the United States. The LNG bunkering barge will consist of a 126.8 m vessel, which will have the capacity for 12,000 m3 of LNG. The expected completion date of the project is 2023.

- Furthermore, in September 2021, Stabilis Solutions Inc. signed a memorandum of understanding (MoU) with Port Isabel Logistical Offshore Terminal in Texas and Louisiana's Cameron Parish Port, Harbor & Terminal District to develop LNG refueling services for ships.

- Similarly, in April 2021, Wison Offshore & Marine (Wison) was awarded the Front-End Engineering Development (FEED) contract for Pilot LNG's Galveston LNG Bunker Port project in Canada, with operations slated to begin in 2024.

- The Canadian government made commitments to significantly reduce greenhouse gas emissions, and the country has an abundant supply of natural gas. Natural gas on combustion produces less greenhouse gas emissions, making LNG a better alternative marine fuel for the Canadian shipping industry.

- Although the initial installation cost of LNG-based vessels is high, the operational cost is lower compared to running old ships with installed scrubbers. Therefore, the North American region is likely to dominate the overall LNG bunkering market during the forecast period.

Liquefied Natural Gas (LNG) Bunkering Industry Overview

The LNG bunkering market is moderately consolidated. The major companies include Shell PLC, Gazprom Neft PJSC, TotalEnergies SE, Gasum Oy, and Engie SA.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD million, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End User

- 5.1.1 Tanker Fleet

- 5.1.2 Container Fleet

- 5.1.3 Bulk and General Cargo Fleet

- 5.1.4 Ferries and OSV

- 5.1.5 Other End Users

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Shell PLC

- 6.3.2 ENN Energy Holdings Ltd

- 6.3.3 Korea Gas Corporation

- 6.3.4 Harvey Gulf International Marine LLC

- 6.3.5 Gasum Oy

- 6.3.6 Engie SA

- 6.3.7 Gazprom Neft PJSC

- 6.3.8 TotalEnergies SE

- 6.3.9 Naturgy Energy Group SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

液化天然氣加註市場報告,依產品類型(船對船、卡車對船、港口對船、攜帶式儲槽)、應用(貨運船隊、貨櫃船隊、油輪船隊、渡輪、內陸船舶等)、和地區2024-2032

液化天然氣加註市場報告,依產品類型(船對船、卡車對船、港口對船、攜帶式儲槽)、應用(貨運船隊、貨櫃船隊、油輪船隊、渡輪、內陸船舶等)、和地區2024-2032 2024 年液化天然氣燃料庫世界市場報告

2024 年液化天然氣燃料庫世界市場報告 全球液化天然氣加註市場 2024-2031

全球液化天然氣加註市場 2024-2031 液化天然氣加註市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按應用、最終用途、地區和競爭細分

液化天然氣加註市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會和預測,按應用、最終用途、地區和競爭細分 LNG燃料庫的全球市場,預測(~2030年)

LNG燃料庫的全球市場,預測(~2030年) 液化天然氣加註市場:按產品(港口到船、攜帶式罐體、船到船)、最終用戶(散貨和雜貨船隊、貨櫃船隊、客船)-2023-2030 年全球預測

液化天然氣加註市場:按產品(港口到船、攜帶式罐體、船到船)、最終用戶(散貨和雜貨船隊、貨櫃船隊、客船)-2023-2030 年全球預測 LNG 加註市場:2023-2028 年全球行業趨勢、份額、規模、增長、機遇和預測

LNG 加註市場:2023-2028 年全球行業趨勢、份額、規模、增長、機遇和預測 LNG燃料庫的全球市場

LNG燃料庫的全球市場 LNG 加註全球市場規模、份額和增長分析(按產品類型、應用)- 2022-2028 年行業預測

LNG 加註全球市場規模、份額和增長分析(按產品類型、應用)- 2022-2028 年行業預測 LNG 加註市場:按產品類型、船舶類型、地區 - 規模、份額、展望、機會分析,2022-2030 年

LNG 加註市場:按產品類型、船舶類型、地區 - 規模、份額、展望、機會分析,2022-2030 年