|

市場調查報告書

商品編碼

1441571

Facade - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Facade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

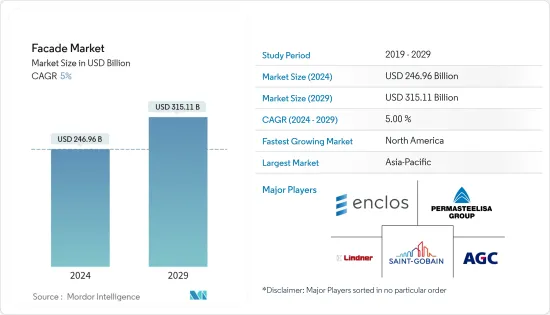

2024年,外牆市場規模預計為2,469.6億美元,預計到2029年將達到3,151.1億美元,在預測期內(2024-2029年)CAGR為5%。

COVID-19 嚴重打擊了全球建築業,導致工程延誤、勞動力短缺,一些地方還因疫情限制而停工。

後來,限制放鬆後,建築業緩慢復甦。目前,一些地區的商業和住宅項目正在顯著成長,進一步推動了幕牆製造業的發展。

此外,立面裝置在世界各地越來越受歡迎,這主要是由於人們對能源效率和外部美化方面的日益關注。此外,太陽能帷幕牆安裝正在實現利潤豐厚的成長,為了滿足對太陽能帷幕牆不斷成長的需求,大多數製造商都專注於開發新型和先進的太陽能帷幕牆。例如,2022年3月,加拿大太陽能技術製造商Mitrex推出了Solar Brick,它看起來像磚牆,但嵌入了太陽能模組。這些模組重量輕、耐用,並且可以儲存能量,足以為建築物供電。

此外,全球不斷增加的商業和住宅項目推動了立面的採用。例如,2022 年,在歐洲,博杜安國王基金會計劃資助超過 50 萬歐元(534,175 美元),支持 11 個公共空間綠化項目,在比利時各地的公共建築外觀上創建垂直花園。此外,還提交了超過28個項目用於醫院、市政廳、圖書館、文化中心、體育設施、游泳池、博物館、劇院、圖書館和社區中心的外牆綠化,其中近11個項目被選中。因此,全球幕牆市場正在經歷利潤豐厚的成長。

帷幕牆市場趨勢

亞太地區正見證顯著成長

亞太地區正在經歷大量的建設項目,該地區廣泛關注外牆美化和能源效率因素,這些因素正在推動該國的外牆安裝。此外,印度、日本、中國等發展中國家的快速城市化推動了該地區帷幕牆安裝的需求。例如,2022年9月,中國揭開了世界上最扭曲的塔樓的面紗,也被稱為「光之舞」摩天大樓。這座 180 公尺高的塔樓被外牆包圍。

此外,立面裝置在該地區越來越受歡迎,這主要是由於商業和住宅房地產開發的不斷增加。例如,2022年12月,中國恆大集團計劃恢復631個預售未交付專案的開工,以滿足其物業交付費用。此外,該房地產開發商在2022年1月至11月期間交付了超過256,000套單位,預計到2023年底將交付近30萬套單位。

同時,該地區的立面綠化正在顯著成長。此外,印度和日本正積極採用立面綠化技術來實現其永續發展目標。此外,為了在氣候變遷和建築緻密化導致氣溫升高的情況下創造生活品質,立面綠化在城市地區發揮著至關重要的作用。而且,綠色辦公理念也推動了立面綠化技術的發展。根據業界專家預測,2022年,日本東京的綠色辦公室存量是亞太地區12個地區中最多的。此外,東京還擁有近900萬平方公尺的環保認證辦公空間。

商業部門正在推動外牆安裝

大多數國家都致力於開發節能的商業建築和辦公空間。在未來幾年,預計老化辦公大樓翻修支出的增加將增加對立面安裝的需求。近年來,商業建築對美觀的需求日益成長,推動了幕牆市場的擴張。

此外,儘管經濟衰退,商業和工業仍實現了顯著成長。此外,過去 18 個月美國建築業的表現優於加拿大和墨西哥。與此同時,北美和歐洲地區正在經歷大量商業項目。例如,2022年第二季度,美國基斯通貿易中心開工建設,第八辦公大樓開工,在華盛頓州貝爾維尤建設佔地50,167平方公尺、25層的辦公大樓。等,這些項目將促進幕牆安裝。

此外,歐洲地區的商業部門正在見證大量投資,促使新項目的建設,進一步推動了帷幕牆安裝市場。然而,2022 年第一季度,跨國房地產交易有所增加。此外,由歐洲、中東和非洲組成的EMEA地區跨境交易量最大,達364億美元。因此,全球不斷成長的商業領域將為帷幕牆製造商創造巨大的機會。

帷幕牆產業概況

全球帷幕牆市場高度分散且競爭激烈,大公司佔據了重要的市場佔有率。此外,一些關鍵參與者還參與合作、創新、業務擴張、獎勵、合資企業和其他策略,以改善其產品足跡並保持市場競爭力。此外,市場上的一些主要參與者包括 Saint-Gobain SA、Enclos Corp.、Permasteelisa Sp 等。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究成果

- 研究假設

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場洞察與動態

- 當前市場概況

- 市場動態

- 市場促進因素

- 全球高層建築和摩天大樓數量的不斷增加為帷幕牆系統創造了一個強勁的市場

- 建築業主和開發商更加重視其結構的整體性能

- 市場限制

- 高品質的外牆材料和設計可能成本高昂,使得某些項目難以滿足預算限制

- 外牆必須符合建築規範和安全法規,這些法規和安全法規可能因地點而異

- 市場機會

- 裝修和改造項目

- 波特五力分析

- 供應商的議價能力

- 買家/消費者的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭激烈程度

- 市場促進因素

- 市場消費者行為變化洞察

- 市場中政府監管的見解

- 市場技術進步的見解

- COVID-19 對市場的影響

第 5 章:市場區隔

- 依類型

- 通風

- 不通風

- 其他類型

- 依材質

- 玻璃

- 金屬

- 塑膠和纖維

- 石頭

- 其他材料

- 依最終用戶

- 商業的

- 住宅

- 其他最終用戶

- 依地理

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 英國

- 法國

- 德國

- 歐洲其他地區

- 亞太

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 拉丁美洲

- 巴西

- 阿根廷

- 拉丁美洲其他地區

- 北美洲

第 6 章:競爭格局

- 公司簡介

- Saint-Gobain SA

- Enclos Corp.

- Kawneer

- Permasteelisa SpA

- Aluplex

- AFS International

- Kingspan Group

- Lindner Group

- Norsk Hydro ASA

- AGC Glass Europe*

第 7 章:外牆市場的未來

第 8 章:附錄

The Facade Market size is estimated at USD 246.96 billion in 2024, and is expected to reach USD 315.11 billion by 2029, growing at a CAGR of 5% during the forecast period (2024-2029).

COVID-19 hard hit on the construction sector across the globe, resulting in project delays, labor shortages, and halts in some places due to the pandemic restrictions.

Later, after easing the restrictions, the construction sector experienced a slow recovery. Currently, some of the regions are witnessing significant growth in commercial and residential projects, further driving the facade manufacturing sector.

Moreover, facade installations are gaining traction across the world, majorly driven by increasing concern towards energy efficiency and external beautification aspects. In addition, solar facade installations are exercising lucrative growth, and to meet the increasing demand for solar facades most manufacturers are focusing on developing new and advanced solar facades. For instance, in March 2022, a Canadian solar technology manufacturer, Mitrex, launched the Solar Brick, which looks like a brick wall but has embedded solar modules. These modules are lightweight and durable and can store energy, which is enough to power the building.

Furthermore, increasing commercial and residential projects across the globe fuel the facade's adoption. For instance, in 2022, in Europe, the King Baudouin Foundation planned to fund more than EUR 500,000 (USD 534,175) to support 11 projects to green the public space by creating vertical gardens on the facades of public buildings throughout Belgium. In addition, more than 28 projects were submitted for greening the outer walls of hospitals, town halls, libraries, cultural centers, sports facilities, swimming pools, museums, theatres, libraries, and community centers, out of which nearly 11 projects were selected. Thus, the facade market is witnessing lucrative growth across the globe.

Facade Market Trends

Asia-Pacific is Witnessing Significant Growth

Asia-Pacific is experiencing a significant number of construction projects, and the region is widely focusing on external wall beautification and energy efficiency factors, these factors are driving the installation of the facades in the country. In addition, rapid urbanization in developing countries such as India, Japan, China, etc. driving the demand for facade installations in the region. For instance, in September 2022, China unveiled the world's most twisted towers, also known as the Dance of Light skyscraper. This 180-meter tall tower was enveloped with facades.

Moreover, facade installations are gaining traction in the region, majorly due to increasing commercial and residential property development. For instance, in December 2022, China Evergrande Group planned to resume its work on 631 pre-sold and undelivered projects to meet its property delivery charger. In addition, the property developer delivered more than 256,000 units between January to November of 2022, and they expect to deliver nearly 300,000 units by the end of 2023.

Meanwhile, facade greening is witnessing significant growth in the region. In addition, India and Japan are actively adopting facade greening techniques to reach their sustainability targets. In addition, to create a quality of life against rising temperatures due to climate change and building densification, facade greening plays a vital role in urban areas. Moreover, the green office concept also promotes the facade greening technology. In 2022, as per industry experts, Tokyo, Japan, had the largest inventory of green offices among the 12 Asia-Pacific areas. Also, Tokyo owns nearly 9 million square meters of environmentally certified office spaces.

Commercial Sector is Driving the Facades Installation

Most countries are focusing on developing commercial buildings and office spaces that are energy efficient. In the upcoming years, it is anticipated that increased spending on the renovation of aging office buildings will increase demand for facade installations. A growing need for aesthetic appearance in commercial buildings has emerged in recent years, which has fuelled the expansion of the facade market.

Moreover, commercial and industrial witnessed significant growth despite the recession. In addition, the United States construction sector has outperformed Canada and Mexico over the past 18 months. Meanwhile, North America and Europe regions are experiencing a significant number of commercial projects. For instance, in Q2 2022, construction of the Keystone Trade Center was started in the United States, and the Eight Office Tower was started, which involves the construction of 50,167 square meters and a 25-story office tower in Bellevue, Washington. etc., these projects will boost the facade installations.

Furthermore, the commercial sector in the European region is witnessing a positive number of investments, resulting in the construction of new projects, further driving the facade installation market. However, in Q1 2022, cross-border real estate transactions increased. In addition, the EMEA region, consisting of Europe, the Middle East, and Africa, received the largest volume of cross-border transactions, amounting to USD 36.4 billion. Thus, the growing commercial sector across the globe will create a huge opportunity for facade manufacturers.

Facade Industry Overview

The global facade market is highly fragmented and competitive, with large companies claiming significant market share. Moreover, several key players engage in collaborations, innovations, business expansion, awards, joint ventures, and other strategies to improve their product footprint and remain competitive in the market. Furthermore, some of the major players in the market include Saint-Gobain S.A, Enclos Corp., Permasteelisa S.p., etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Market Overview

- 4.2 Market Dynamics

- 4.2.1 Market Drivers

- 4.2.1.1 The growing number of high-rise buildings and skyscrapers globally has created a robust market for facade systems

- 4.2.1.2 Building owners and developers are placing greater emphasis on the overall performance of their structures

- 4.2.2 Market Restraints

- 4.2.2.1 High-quality facade materials and designs can be costly, making it challenging for some projects to meet budget constraint

- 4.2.2.2 Facades must comply with building codes and safety regulations, which can vary based on location

- 4.2.3 Market Opportunities

- 4.2.3.1 Renovation and Retrofitting Projects

- 4.2.4 Porter's Five Forces Analysis

- 4.2.4.1 Bargaining Power of Suppliers

- 4.2.4.2 Bargaining Power of Buyers/Consumers

- 4.2.4.3 Threat of New Entrants

- 4.2.4.4 Threat of Substitute Products

- 4.2.4.5 Intensity of Competitive Rivalry

- 4.2.1 Market Drivers

- 4.3 Insights on Changes in Consumer Behavior in the Market

- 4.4 Insights on Government Regulations in the Market

- 4.5 Insights on Technological Advancements in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Ventilated

- 5.1.2 Non-Ventilated

- 5.1.3 Other Types

- 5.2 By Material

- 5.2.1 Glass

- 5.2.2 Metal

- 5.2.3 Plastic and Fibres

- 5.2.4 Stones

- 5.2.5 Other Materials

- 5.3 By End-User

- 5.3.1 Commercial

- 5.3.2 Residential

- 5.3.3 Other End-Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 United Arab Emirates

- 5.4.4.2 Saudi Arabia

- 5.4.4.3 South Africa

- 5.4.4.4 Rest of Middle East & Africa

- 5.4.5 Latin America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of Latin America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Overview (Market Concentration and Major Players)

- 6.2 Company Profiles

- 6.2.1 Saint-Gobain S.A

- 6.2.2 Enclos Corp.

- 6.2.3 Kawneer

- 6.2.4 Permasteelisa S.p.A

- 6.2.5 Aluplex

- 6.2.6 AFS International

- 6.2.7 Kingspan Group

- 6.2.8 Lindner Group

- 6.2.9 Norsk Hydro ASA

- 6.2.10 AGC Glass Europe*

7 FUTURE OF THE FACADE MARKET

8 APPENDIX

2024 年建築幕牆系統世界市場報告

2024 年建築幕牆系統世界市場報告 2024 年建築幕牆全球市場報告

2024 年建築幕牆全球市場報告 帷幕牆系統市場:依產品類型、依材料、依最終用途、按技術、按地區

帷幕牆系統市場:依產品類型、依材料、依最終用途、按技術、按地區 帷幕牆市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按產品、帷幕牆類型、建築類型、地區、競爭細分

帷幕牆市場 - 2018-2028 年全球產業規模、佔有率、趨勢、機會與預測,按產品、帷幕牆類型、建築類型、地區、競爭細分 全球外牆系統市場

全球外牆系統市場 全球幕牆系統市場 - 2023-2030

全球幕牆系統市場 - 2023-2030 帷幕牆系統市場:按產品類型(覆層、幕牆、外部隔熱和飾面系統)、材料類型(陶瓷、混凝土、玻璃)、最終用途- 2023-2030 年全球預測

帷幕牆系統市場:按產品類型(覆層、幕牆、外部隔熱和飾面系統)、材料類型(陶瓷、混凝土、玻璃)、最終用途- 2023-2030 年全球預測 建築幕牆的全球市場 2023-2027

建築幕牆的全球市場 2023-2027 全球幕牆系統市場:按類型(EIFS,覆層,壁板,幕牆),最終用戶(住宅,非住宅),地區(北美,歐洲,南美,亞太,中東和非洲)預測(2027)

全球幕牆系統市場:按類型(EIFS,覆層,壁板,幕牆),最終用戶(住宅,非住宅),地區(北美,歐洲,南美,亞太,中東和非洲)預測(2027) 立面錨固系統市場按類型(立面錨固,砌體錨固)應用(砌體,混凝土,幕牆)用戶(住宅,非住宅):2021-2031年全球機會分析和行業預測

立面錨固系統市場按類型(立面錨固,砌體錨固)應用(砌體,混凝土,幕牆)用戶(住宅,非住宅):2021-2031年全球機會分析和行業預測