|

市場調查報告書

商品編碼

1440533

緩釋肥料:市場佔有率分析、產業趨勢與統計、成長預測(2024-2030)Controlled Release Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

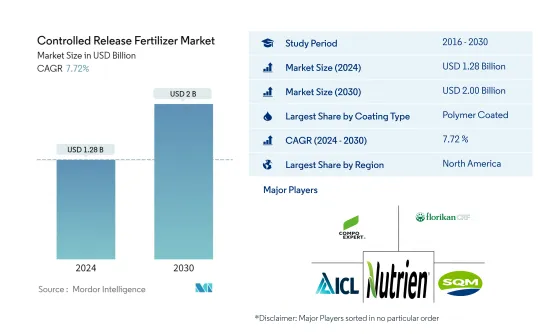

2024年緩釋肥料市場規模估計為12.8億美元,預計到2030年將達到20億美元,在預測期間(2024-2030年)以7.72%的複合年增長率增長。

主要亮點

- 聚合物塗料是最大的塗料類型。聚合物包膜肥料釋放養分的時間更長,減少了肥料在土壤中的淋失,也減少了施用量。

- 田間作物是最大的作物類型:田間作物在世界各地廣泛種植,是世界許多地區的主食。在大多數農業國家,依地區分類,它們所佔佔有率最大。

- 美國是最大的國家:營養物質的高效釋放,減少了營養物質的浸出和揮發,這是推動該國塗層CRF市場的主要因素。

緩釋肥料的市場趨勢

聚合物塗料是最大的塗料類型

- 緩效性肥料 (CRF) 約佔全球肥料市場總量的 2.3%,2021 年價值約 38 億美元。田間作物主導市場,2021 年約佔市場價值的 50.4%。全世界都有廣闊的栽培面積。

- 在CRF中,聚合物包膜肥料佔據市場主導地位,約佔市場價值的62.6%,2021年價值約23.8億美元。聚合物包膜CRF是一種先進的CRF,其中肥料顆粒被聚合物包覆。養分損失非常低,因為養分會慢慢流失。

- 北美地區在全球緩釋肥料市場中佔據主導地位,約佔市場價值的 61.7%,由於技術進步以及該地區田間作物的主導地位和擔憂,預計 2021 年將實現成長硝酸鹽污染造成的損失約為23.7億美元。在農業技術的適應方面。到預測期結束時,該地區的市場價值預計將成長約 2.2%,達到 24.2 億美元。

- 全球緩控釋肥市場量穩定成長。市場價格的波動是由於化肥價格的波動所造成的。緩效性肥料的價格主要取決於製造商用於包膜肥料的技術。

- 由於其高效率、低養分損失和低環境污染,全球緩效肥料市場預計在預測期內將成長。農民意識和可用性的提高也將推動市場的發展。

北美是最大的地區

- 北美主導全球緩釋肥料市場。在該地區,美國是最大的緩效肥料市場,2021年佔市場佔有率63.0%。

- 歐洲在全球緩釋肥料市場中佔據第二大市場佔有率。歐洲緩釋肥市場在該地區各國均表現出顯著且穩定的成長,其中烏克蘭佔2021年市佔率最大,為9.09%,其次是西班牙。

- 亞太地區是全球第三大緩釋肥料市場。中國在亞太地區緩釋肥料市場佔據主導地位,2021年約佔11.2%的市場佔有率。聚合物包膜肥料在緩釋肥料市場中的佔有率最高,其次是聚合物硫包膜肥料。 2017年聚合物包膜肥料領域的價值為2.029億美元,預計到預測期結束時將達到3.72億美元。

- 控釋尿素是世界上最常用的 CRF型態。氮流失是稻農面臨的主要問題之一,水稻氮利用效率往往不足。這是由於氮透過揮發、淋濾和反硝化作用大量損失所造成的。提高氮效率的一種方法是使用控制釋放尿素。控制釋放尿素在減少氮素損失、促進植物生長、提高氮濃度方面通常比顆粒尿素肥料表現更好。

- 緩釋肥料效率的提高將在預測期內推動市場發展。

緩控釋肥產業概況

緩控釋肥市場整合度較高,前5家企業佔67.34%。市場的主要企業包括(依字母順序排列)Compo Expert GMbh、Florikan、ICL Specialty Fertilizers、Nutrien Ltd.、Sociedad Química y Minera de Chile SA。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章執行摘要和主要發現

第2章 提供報告

第3章簡介

- 研究假設和市場定義

- 調查範圍

- 調查方法

第4章 產業主要趨勢

- 主要作物種植面積

- 平均養分施用量

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 塗層類型

- 聚合物塗層

- 聚合物硫塗層

- 其他

- 作物類型

- 田裡的作物

- 園藝作物

- 草坪和裝飾

- 地區

- 亞太地區

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

- 中東和非洲

- 奈及利亞

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 亞太地區

第6章 競爭形勢

- 重大策略舉措

- 市場佔有率分析

- 公司形勢

- 公司簡介

- Compo Expert GMbh

- Ekompany International BV(DeltaChem)

- Florikan

- Haifa Group Ltd

- ICL Speciality Fertilizers

- Kingenta Ecological Engineering Group Co., Ltd.

- Mivena BV

- Nutrien Ltd.

- Sociedad Quimica y Minera de Chile SA

第7章 CEO 面臨的關鍵策略問題

第8章附錄

- 世界概況

- 概述

- 波特的五力框架

- 全球價值鏈分析

- 市場動態(DRO)

- 來源和參考文獻

- 表格和圖形列表

- 重要見解

- 資料包

- 詞彙表

簡介目錄

Product Code: 92585

The Controlled Release Fertilizer Market size is estimated at USD 1.28 billion in 2024, and is expected to reach USD 2 billion by 2030, growing at a CAGR of 7.72% during the forecast period (2024-2030).

Key Highlights

- Polymer Coated is the Largest Coating Type: The polymer coated fertilizers release the nutrients for longer duration and decrease the leaching losses of fertilizers in the soil and also reduce the application rate.

- Field Crops is the Largest Crop Type: Field crops are widely cultivated across the world & are staple food in many parts of the world. They account for maximum share by area in most of the Agricultural countries.

- United States is the Largest Country: The efficient nutrient release led to decreased leaching, and volatilization of the nutrients which are the major factors driving the coated CRF market in the country.

Controlled Release Fertilizers Market Trends

Polymer Coated is the largest Coating Type

- Controlled-release fertilizers (CRFs) account for about 2.3% of the total global fertilizer market value, valued at about USD 3.8 billion in 2021. Field crops dominated the market and accounted for about 50.4% of the market value in 2021, majorly due to their large cultivation area around the world.

- Among CRFs, polymer-coated fertilizers dominated the market and accounted for about 62.6% of the market value, valued at about USD 2.38 billion in 2021. Polymer-coated CRF is an advanced type of CRF where the fertilizer granule is coated with polymers to allow the nutrients to escape from it gradually, leading to very less loss of nutrients.

- The North American region dominated the global controlled-release fertilizer market and accounted for about 61.7% of the market value, valued at about USD 2.37 billion in 2021 due to the dominance of field crops in the region and concern over nitrate pollution in addition to advancement in the adaption of agricultural technologies. The region's market value is anticipated to increase by about 2.2% and reach USD 2.42 billion by the end of the forecast period.

- There is a steady increase in the global controlled-release fertilizer market in terms of volume. The fluctuations in the market value are due to fluctuations in fertilizer prices. The prices of controlled-release fertilizers mainly depend on the technology used by the manufacturers for coating the fertilizers.

- The global controlled-release fertilizer market is projected to grow during the forecast period owing to their higher efficiency and fewer nutrient losses leading to less environmental pollution. Increased awareness among the farmers and increased availability will also drive the market.

North America is the largest Region

- North America dominates the global controlled-release fertilizer market. In the region, the United States is the largest market for controlled-release fertilizers accounting for 63.0% of the market in 2021.

- Europe occupied the second largest market share in the global controlled-release fertilizer market. The controlled-release fertilizer market in Europe is observed to have notably stable growth across all countries in the region, with Ukraine occupying the largest share of 9.09 % in the market, followed by Spain for the year 2021.

- The Asia-Pacific region is the third largest market for controlled-release fertilizers in the world. China dominates the APAC controlled-release fertilizers market by accounting for about 11.2% of the market share in 2021. Polymer-coated fertilizers recorded the highest share in the controlled-release fertilizers market, followed by polymer sulfur-coated fertilizers. Polymer coated fertilizers segment was valued at USD 202.9 million in 2017 and is anticipated to reach USD 372.0 million by the end of the forecast period.

- Control-release urea is the most commonly used form of CRF in the world. Nitrogen loss is one of the main problems faced by rice farmers, and the efficiency of nitrogen utilization in rice is often inadequate. This is due to the large loss of nitrogen due to volatilization, leaching, and denitrification. One way to improve nitrogen efficiency is to use control-release urea. Controlled-release urea generally outperformed granular urea fertilizers in reducing nitrogen loss, stimulating plant growth, and increasing nitrogen concentration.

- The increased efficiency of controlled-release fertilizers will drive the market during the forecast period.

Controlled Release Fertilizers Industry Overview

The Controlled Release Fertilizer Market is fairly consolidated, with the top five companies occupying 67.34%. The major players in this market are Compo Expert GMbh, Florikan, ICL Speciality Fertilizers, Nutrien Ltd. and Sociedad Quimica y Minera de Chile SA (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.2 Average Nutrient Application Rates

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 Australia

- 5.3.1.2 Bangladesh

- 5.3.1.3 China

- 5.3.1.4 India

- 5.3.1.5 Indonesia

- 5.3.1.6 Japan

- 5.3.1.7 Pakistan

- 5.3.1.8 Philippines

- 5.3.1.9 Thailand

- 5.3.1.10 Vietnam

- 5.3.1.11 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 France

- 5.3.2.2 Germany

- 5.3.2.3 Italy

- 5.3.2.4 Netherlands

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 Ukraine

- 5.3.2.8 United Kingdom

- 5.3.2.9 Rest of Europe

- 5.3.3 Middle East & Africa

- 5.3.3.1 Nigeria

- 5.3.3.2 Saudi Arabia

- 5.3.3.3 South Africa

- 5.3.3.4 Turkey

- 5.3.3.5 Rest of Middle East & Africa

- 5.3.4 North America

- 5.3.4.1 Canada

- 5.3.4.2 Mexico

- 5.3.4.3 United States

- 5.3.4.4 Rest of North America

- 5.3.5 South America

- 5.3.5.1 Argentina

- 5.3.5.2 Brazil

- 5.3.5.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Compo Expert GMbh

- 6.4.2 Ekompany International BV (DeltaChem)

- 6.4.3 Florikan

- 6.4.4 Haifa Group Ltd

- 6.4.5 ICL Speciality Fertilizers

- 6.4.6 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.7 Mivena BV

- 6.4.8 Nutrien Ltd.

- 6.4.9 Sociedad Quimica y Minera de Chile SA

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

02-2729-4219

+886-2-2729-4219

控制釋放肥料市場:按類型、作物、方法和最終用途分類 - 2024-2030 年全球預測

控制釋放肥料市場:按類型、作物、方法和最終用途分類 - 2024-2030 年全球預測 2024 年緩釋肥料全球市場報告

2024 年緩釋肥料全球市場報告 聚合物塗層 NPK:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年)

聚合物塗層 NPK:市場佔有率分析、行業趨勢和統計、成長預測(2024-2029 年) 2030 年控制釋放肥料市場預測:按類型、應用、最終用戶和地區分類的全球分析

2030 年控制釋放肥料市場預測:按類型、應用、最終用戶和地區分類的全球分析 控釋肥料市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

控釋肥料市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 控釋肥料的全球市場:按類型(緩釋性、塗層/封裝、氮穩定劑)、按最終用途(農業、非農業)、按型態形式(葉面噴布、施肥、土壤)、按地區2028年

控釋肥料的全球市場:按類型(緩釋性、塗層/封裝、氮穩定劑)、按最終用途(農業、非農業)、按型態形式(葉面噴布、施肥、土壤)、按地區2028年 2023-2030 年硝化抑製劑和尿□抑製劑的全球市場

2023-2030 年硝化抑製劑和尿□抑製劑的全球市場 2023-2030 年全球控釋肥市場

2023-2030 年全球控釋肥市場 到 2028 年控釋肥料的市場預測——按類型、應用、最終用戶和地區進行的全球分析

到 2028 年控釋肥料的市場預測——按類型、應用、最終用戶和地區進行的全球分析 控釋型肥料的全球市場

控釋型肥料的全球市場

▼