|

市場調查報告書

商品編碼

1440532

二次元素肥料:全球市場佔有率分析、產業趨勢與統計、成長預測(2024-2030)Global Secondary Macronutrients Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2030) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

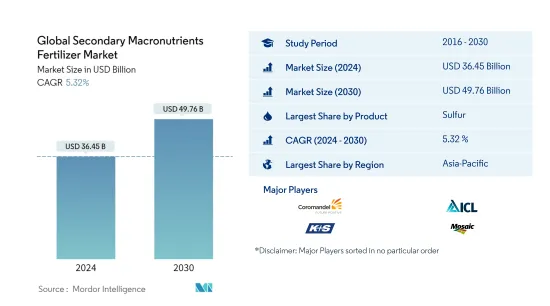

在預測期間(2024-2030年),全球二次元素肥料市場規模預計到2024年為364.5億美元,到2030年將達到497.6億美元,複合年成長率為5.32%。

主要亮點

- 依類型分類成長最快的部分 - 硫磺:由於土壤健康狀況下降、土壤 pH 值不平衡以及蔥屬和十字花科作物的作物方法,土壤中硫磺的可用性受到限制。

- 依作物類型分類的最大區隔市場 -田間作物:田間作物在世界各地廣泛種植,並且是世界許多地區的主食。在大多數農業國家,它們在單位面積中所佔的佔有率最大。

- 以施用方式分類的最大部分 - 土壤:土壤施用是一種無需設備的便捷施肥方法。這種施用方法有助於改善植物健康和土壤肥力。

- 最大的國家 - 印度:印度土壤中 41% 的土壤缺乏硫,鈣和鎂的缺乏也變得越來越嚴重。這些肥料的施用量正在增加,以最大限度地提高生產力。

中量元素肥料市場趨勢

硫磺是最大的產品部分。

- 2021年,硫磺佔全球中量元素肥料市場的50.6%。 2021年南美硫磺市場價值約12.7億美元。在該市場中,特種硫肥的市場佔有率高達約62.7%,而常規硫肥約佔37.2%。特種硫肥的使用比其他中量元素肥料更為普遍。到預測期末,特種硫肥市場預計將達到 22.6 億美元。

- 2021年鎂佔全球中量元素肥料市場的42.8%。田間作物佔比最大,為 92.3%,其次是草坪作物、觀賞作物和園藝作物,佔 7.4% 和 0.3%。消耗化肥最多的作物是小麥和玉米,合計佔全國土地面積的40.0%。

- 鈣佔全球中量元素肥料市場總額的 6.1%,2021 年約 4.697 億美元。亞太地區在鈣肥市場佔據主導地位,約佔全球鈣肥市場價值的35.2%,創下歷史紀錄。 2021 年為 1.924 億美元。亞太地區在鈣肥市場的主導地位主要是由於土壤酸化,這意味著鈣和鎂等鹼性陽離子會流失,並被鐵等酸性元素所取代。和鋁複合材料。

- 由於種植面積的減少增加了對更高生產力的需求,預計在作物期內對大量大量營養素肥料的需求將會增加。

亞太地區是最大的地區。

- 施用中量元素肥料對作物產量有正面作用。當今產量作物系統的需求增加了對鈣、鎂和硫的需求,這些對植物生產力至關重要。

- 亞太地區在全球大量營養素肥料市場中佔據主導地位,2021年佔市場價值的33.3%。在亞太地區,硫磺佔最大的市場佔有率,佔 47.5%,其次是鎂,佔 45.7%。 %,鈣佔二次元市場總量的6.7%。其中,印度佔據市場主導地位,2021年佔39.7%的佔有率。

- 2021年,歐洲在全球次微營養素肥料市場中佔據第二大佔有率(25.0%)。硫磺在中量元素肥料市場中佔據最大佔有率,2021年約佔總量的61.9%。俄羅斯在歐洲市場佔據主導地位,2021年佔17.7%的市場佔有率。

- 2021年,南美洲中量元素肥料市場約佔全球中量元素肥料市場的17.8%。巴西在中量元素肥料市場佔據主導地位,約佔全部區域市場價值的67.6%,達9.478億美元。這主要得益於全國範圍內的大面積種植。 2021年,巴西約佔該地區農業總面積的61.8%。

- 次要元素對於平衡植物營養至關重要。每種營養素在決定植物代謝方面都有特定的作用。預計這種情況將在預測期內推動市場。

中量元素肥料產業概況

全球二次元素肥料市場適度整合,前五名企業佔54.07%。該市場的主要企業包括 Coromandel International、Israel Chemicals Ltd.、K+S AKTIENGESELLSCHAFT、The Mosaic Company 和 Yara International(依字母順序排列)。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章執行摘要和主要發現

第2章 提供報告

第3章簡介

- 研究假設和市場定義

- 調查範圍

- 調查方法

第4章 產業主要趨勢

- 主要作物種植面積

- 平均養分施用量

- 法律規範

- 價值鍊和通路分析

第5章市場區隔

- 類型

- 直的

- 二次元

- 鈣

- 鎂

- 硫

- 直的

- 如何使用

- 施肥

- 葉子

- 土壤

- 作物類型

- 田裡的作物

- 園藝作物

- 草坪和裝飾

- 地區

- 亞太地區

- 澳洲

- 孟加拉

- 中國

- 印度

- 印尼

- 日本

- 巴基斯坦

- 菲律賓

- 泰國

- 越南

- 其他亞太地區

- 歐洲

- 法國

- 德國

- 義大利

- 荷蘭

- 俄羅斯

- 西班牙

- 烏克蘭

- 英國

- 其他歐洲國家

- 中東和非洲

- 奈及利亞

- 沙烏地阿拉伯

- 南非

- 土耳其

- 其他中東和非洲

- 北美洲

- 加拿大

- 墨西哥

- 美國

- 北美其他地區

- 南美洲

- 阿根廷

- 巴西

- 南美洲其他地區

- 亞太地區

第6章 競爭形勢

- 重大策略舉措

- 市場佔有率分析

- 公司形勢

- 公司簡介

- Compo Expert

- Coromandel International

- Deepak Fertilisers and Petrochemicals

- Haifa Group

- Israel Chemicals Ltd.

- K+S AKTIENGESELLSCHAFT

- Koch Industries

- The Mosaic Company

- Yara International

第7章 CEO 面臨的關鍵策略問題

第8章附錄

- 世界概況

- 概述

- 波特的五力框架

- 全球價值鏈分析

- 市場動態(DRO)

- 來源和參考文獻

- 表格和圖形列表

- 重要見解

- 資料包

- 詞彙表

The Global Secondary Macronutrients Fertilizer Market size is estimated at USD 36.45 billion in 2024, and is expected to reach USD 49.76 billion by 2030, growing at a CAGR of 5.32% during the forecast period (2024-2030).

Key Highlights

- Fastest growing segment by Type - Sulfur : Depleting soil health, imbalances in the soil pH, and intensive cultivating methods of crops from allium and cruciferous groups limit the availability of sulfur in the soil.

- Largest Segment by Crop Type - Field Crops : Field crops are widely cultivated worldwide and are a staple food in many parts of the world. They account for a maximum share by area in most agricultural countries.

- Largest Segment by Application Mode - Soil : Soil application is a convenient way of applying fertilizers without any equipment. This method of application helps in improving both plant health and soil fertility.

- Largest segment by Country - India : Indian soils are deficient in S by 41%, and Ca and Mg deficiencies are also becoming prominent. The application of these fertilizers is increasing to maximize productivity.

Secondary Macronutrients Fertilizer Market Trends

Sulfur is the largest segment by Product.

- In 2021, sulfur accounted for 50.6% of the global secondary macronutrient fertilizer market. In 2021, the value of the South American sulfur market was about USD 1.27 billion. In this market, specialty sulfur fertilizer accounted for a maximum market share of approximately 62.7%, and conventional sulfur fertilizer accounted for about 37.2%. The adoption of specialty sulfur fertilizer is more than other secondary macronutrients. The specialty sulfur fertilizer market is anticipated to reach USD 2.26 billion by the end of the forecast period.

- Magnesium accounted for 42.8% of the global secondary macronutrient fertilizer market in 2021. Field crops accounted for a maximum share of 92.3%, followed by turf and ornamental crops and horticulture crops, holding shares of 7.4% and 0.3%, respectively. The largest fertilizer-consuming crops are wheat and corn, accounting for a total of 40.0% of the land area.

- Calcium recorded 6.1% of the total value of the global secondary macronutrient fertilizer market, accounting for about USD 469.7 million in 2021. The Asia-Pacific region dominated the calcium fertilizer market and accounted for about 35.2% of the global calcium fertilizer market's value, registering USD 192.4 million in 2021. The dominance of the Asia-Pacific region in the calcium fertilizer market is mainly due to the acidification of soils, which means the loss of base cations, such as calcium and magnesium, and replacement with acidic elements, like iron and aluminum complexes.

- The demand for secondary macronutrient fertilizer is anticipated to grow during the forecast period, as the need for higher productivity is increasing due to the decline in the area under the cultivation of crops.

Asia-Pacific is the largest segment by Region.

- Fertilizing with secondary macronutrients has a positive effect on crop yields. The need for calcium, magnesium, and sulfur has increased due to the demands from today's high-yielding crop systems, and they are essential for plant productivity.

- The Asia-Pacific region dominates the global secondary macronutrient fertilizer market, having accounted for 33.3% of the market value in 2021. In the Asia-Pacific region, sulfur accounts for the maximum market share of 47.5%, followed by magnesium, accounting for 45.7%, and calcium, accounting for 6.7% of the total secondary macronutrient market. Among all the countries, India dominated the market, accounting for a share of 39.7% in 2021.

- In 2021, Europe accounted for the second-largest share (25.0%) of the global secondary micronutrient fertilizer market. Sulfur occupies the largest share in the secondary macronutrient fertilizer market, having accounted for about 61.9% of the total value in 2021. Russia dominated the European market, accounting for 17.7% of the market share in 2021.

- The South American secondary macronutrient fertilizer market accounted for about 17.8% of the value of the global secondary macronutrient fertilizer market in 2021. Brazil dominated the secondary macronutrient fertilizer market and accounted for about 67.6% of the total regional market value, amounting to USD 947.8 million in 2021. This was mainly due to the large cultivational area across the country. Brazil accounted for about 61.8% of the total agricultural area in the region in 2021.

- Secondary macronutrients are essential for balanced plant nutrition. Each nutrient has a specific role in determining the metabolism of plants. This situation is expected to drive the market during the forecast period.

Secondary Macronutrients Fertilizer Industry Overview

The Global Secondary Macronutrients Fertilizer Market is moderately consolidated, with the top five companies occupying 54.07%. The major players in this market are Coromandel International, Israel Chemicals Ltd., K+S AKTIENGESELLSCHAFT, The Mosaic Company and Yara International (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.2 Average Nutrient Application Rates

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Straight

- 5.1.1.1 Secondary Macronutrients

- 5.1.1.1.1 Calcium

- 5.1.1.1.2 Magnesium

- 5.1.1.1.3 Sulfur

- 5.1.1 Straight

- 5.2 Application Mode

- 5.2.1 Fertigation

- 5.2.2 Foliar

- 5.2.3 Soil

- 5.3 Crop Type

- 5.3.1 Field Crops

- 5.3.2 Horticultural Crops

- 5.3.3 Turf & Ornamental

- 5.4 Region

- 5.4.1 Asia-Pacific

- 5.4.1.1 Australia

- 5.4.1.2 Bangladesh

- 5.4.1.3 China

- 5.4.1.4 India

- 5.4.1.5 Indonesia

- 5.4.1.6 Japan

- 5.4.1.7 Pakistan

- 5.4.1.8 Philippines

- 5.4.1.9 Thailand

- 5.4.1.10 Vietnam

- 5.4.1.11 Rest Of Asia-Pacific

- 5.4.2 Europe

- 5.4.2.1 France

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Netherlands

- 5.4.2.5 Russia

- 5.4.2.6 Spain

- 5.4.2.7 Ukraine

- 5.4.2.8 United Kingdom

- 5.4.2.9 Rest Of Europe

- 5.4.3 Middle East & Africa

- 5.4.3.1 Nigeria

- 5.4.3.2 Saudi Arabia

- 5.4.3.3 South Africa

- 5.4.3.4 Turkey

- 5.4.3.5 Rest Of Middle East & Africa

- 5.4.4 North America

- 5.4.4.1 Canada

- 5.4.4.2 Mexico

- 5.4.4.3 United States

- 5.4.4.4 Rest Of North America

- 5.4.5 South America

- 5.4.5.1 Argentina

- 5.4.5.2 Brazil

- 5.4.5.3 Rest Of South America

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Compo Expert

- 6.4.2 Coromandel International

- 6.4.3 Deepak Fertilisers and Petrochemicals

- 6.4.4 Haifa Group

- 6.4.5 Israel Chemicals Ltd.

- 6.4.6 K+S AKTIENGESELLSCHAFT

- 6.4.7 Koch Industries

- 6.4.8 The Mosaic Company

- 6.4.9 Yara International

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

藻類肥料市場:型態、藻類類型和應用分類 - 2024-2030 年全球預測

藻類肥料市場:型態、藻類類型和應用分類 - 2024-2030 年全球預測 複合肥料市場:型態、營養成分、應用分類 - 2024-2030 年全球預測

複合肥料市場:型態、營養成分、應用分類 - 2024-2030 年全球預測 昆蟲肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F

昆蟲肥料市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F 草肥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F

草肥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按類型、形式、應用、地區和競爭細分,2019-2029F 全球有機礦物肥料市場 - 2024-2031

全球有機礦物肥料市場 - 2024-2031 全球矽肥市場 - 2024-2031

全球矽肥市場 - 2024-2031 硼肥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按來源、應用、地區和競爭細分,2019-2029F

硼肥市場 - 全球產業規模、佔有率、趨勢、機會和預測,按來源、應用、地區和競爭細分,2019-2029F 固氮螺菌肥料市場 - 2023-2030

固氮螺菌肥料市場 - 2023-2030 海藻肥市場 - 2023-2030

海藻肥市場 - 2023-2030 到 2030 年生物炭肥料市場預測 - 按產品類型、技術、應用和地理位置進行的全球分析

到 2030 年生物炭肥料市場預測 - 按產品類型、技術、應用和地理位置進行的全球分析