|

市場調查報告書

商品編碼

1440130

浮體式液化天然氣發電廠:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Floating LNG Power Plant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

價格

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

簡介目錄

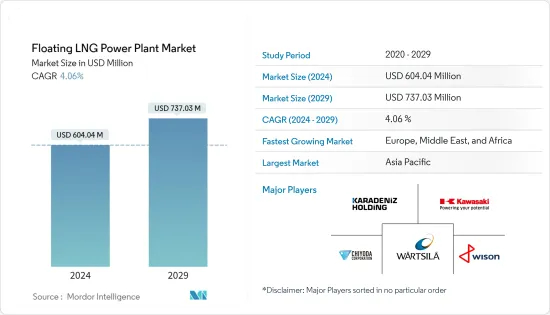

浮體式液化天然氣發電廠市場規模預計到2024年為6.0404億美元,預計到2029年將達到7.3703億美元,在預測期內(2024-2029年)持續成長,複合年成長率為4.06%。

冠狀病毒感染疾病(COVID-19)對 2020 年市場產生了負面影響。現在,市場可能達到大流行前的水平。

主要亮點

- 從長遠來看,人口成長導致的電力需求增加以及新興國家缺乏足夠的電力基礎設施等因素預計將推動浮體式液化天然氣發電廠市場的發展。

- 另一方面,液化天然氣價格的高波動性和不均勻性預計將抑制浮體式液化天然氣電廠市場。

- 儘管如此,由於全球排放標準,預計未來液化天然氣的採用將會增加。液化天然氣是一種相對清潔的燃料,符合排放氣體法規。 IMO 降低船用燃料硫含量的規定將於 2020 年生效,這可能會促使液化天然氣作為船用燃料。西非沿海的石油和天然氣活動也在增加,這也將為 FLNG 發電廠市場創造機會。

- 亞太地區最近佔據了重要的市場佔有率,預計將在預測期內成為最大和最快的市場。

浮體式液化天然氣發電廠的市場趨勢

電力駁船領域預計將主導市場

- 電力駁船是安裝在扁平浮體結構上的發電廠設備。與動力船不同,駁船沒有自航系統從一個地方移動到另一個地方,這降低了駁船的生產成本。

- 這些動力駁船沒有自航式移動系統,由其他小船或船隻移動。駁船推進引擎節省的空間可用於更有效的船內空間。

- 由於發電資本投資低或基礎設施可用性低的國家擴大安裝基於浮體式天然氣的浮動發電廠,電力駁船市場預計在未來幾年將顯著成長。

- 動力駁船具有多項優勢,將推動其在 FLNG 發電領域的採用。這些用於降低運輸成本和大批量運輸,並且有多種尺寸可供選擇。這些駁船即使在低潮時也能航行,產生能量並在漂浮時成功運輸各種類型的貨物。

- 駁船設計用於在特定水域中運行,並且駁船在其整個生命週期中只能在該水域中運行。如果駁船要在其他水域使用,則必須由拖船適當拖曳或協助。

- 2021年12月,惠生海工與MAN Energy Solutions簽署了開發電力解決方案的合作備忘錄。雙方計劃在動力駁船和浮體式液化天然氣發電工程上合作,這將很好地體現雙方在技術和應用方面的優勢。

- 因此,由於上述幾點,電力駁船預計將在預測期內主導浮體式液化天然氣發電廠市場。

預計亞太地區將主導市場

- 在亞太地區,能源供需缺口往往透過煤炭、水力、天然氣、核能和可再生能源技術等資源來緩解。大多數國家已經實現了顯著的電力供應水準。另一方面,再生能源來源已最大程度地克服了電力可靠性問題,這表明浮體式液化天然氣發電廠市場不太可能在該地區發展。

- 然而,東南亞很少國家引進浮動電廠來保障能源供應。據馬來西亞能源局稱,2039年電力需求預計將達到約24GW。為了滿足不斷成長的需求,各國政府正在採取措施擴大能源系統,包括浮體式液化天然氣發電廠來滿足這項需求。

- 2023年,馬來西亞國家石油公司與Kejurtelan Asastela (KAB)簽訂契約,開發和營運一座52MW浮體式液化天然氣發電廠,價值5,220萬美元。浮體式液化天然氣發電廠將位於沙巴。開發工作預計將於 2023 年第二季開始。斯里蘭卡政府也同意與亞洲開發銀行合作,於 2022 年對一座浮體式液化天然氣發電廠進行可行性研究,有助於實現該國能源結構的多元化。

- 此外,2022年,印尼將接受設計用於液化天然氣運作的浮體式發電駁船,這很可能滿足該國的發電需求。 BMPP Nusantara 1 有潛力滿足該國偏遠地區的電力需求,幫助企業和居民最大限度地減少對發電駁船租賃的依賴。

- 因此,由於上述幾點,亞太地區預計將在預測期內主導浮體式液化天然氣發電廠市場。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查範圍

- 市場定義

- 調查先決條件

第 2 章執行摘要

第3章調查方法

第4章市場概況

- 介紹

- 2028 年之前的市場規模與需求預測(十億美元)

- 最新趨勢和發展

- 政府政策法規

- 市場動態

- 促進因素

- 抑制因素

- 供應鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔

- 元件類型

- 燃氣引擎或燃氣渦輪機

- 內燃機

- 蒸氣渦輪和發電機

- 船型

- 動力船

- 動力駁船

- 地區

- 北美洲

- 歐洲

- 亞太地區

- 南美洲

- 中東和非洲

第6章 競爭形勢

- 合併、收購、合作和合資企業

- 主要企業採取的策略

- 公司簡介

- Kawasaki Heavy Industries Ltd

- Wartsila Oyj Abp

- Siemens Energy AG

- Waller Marine Inc.

- Wison Group

- Chiyoda Corporation

- Karadeniz Holding

第7章市場機會與未來趨勢

簡介目錄

Product Code: 70155

The Floating LNG Power Plant Market size is estimated at USD 604.04 million in 2024, and is expected to reach USD 737.03 million by 2029, growing at a CAGR of 4.06% during the forecast period (2024-2029).

COVID-19 negatively impacted the market in 2020. Presently the market is likely to reach pre-pandemic levels.

Key Highlights

- Over the long term, factors such as increasing demand for power due to increasing population and the lack of proper power infrastructures in developing countries are expected to drive the floating LNG power plant market.

- On the other hand, high volatility and uneven LNG prices are expected to restrain the floating LNG power plant market.

- Nevertheless, LNG adoption is expected to increase in the future owing to global emission norms. LNG being a comparatively cleaner fuel fulfills emission regulations. In 2020, IMO's reduced sulfur content in maritime fuel came into force, which is likely to result in the adoption of LNG as a bunker fuel. Offshore West Africa is also seeing increased oil and gas activity that, in turn, will present opportunities in the FLNG power plant market as well.

- Asia-Pacific held a significant market share recently, and it is expected to be the largest and the fastest market during the forecast period.

Floating LNG Power Plant Market Trends

Power Barge Segment Expected to Dominate the Market

- A power barge is a power plant facility installed on flat floating structures. Unlike power ships, a barge doesn't have a self-propelled system for moving from one location to the other, which cuts the cost of production for barges.

- As these power barges do not have any self-propelled moving systems, they are moved by other small boats or ships. The space saved from the propulsion engines in barges is used for more usable space in the vessel.

- The market for power barge is estimated to grow significantly in upcoming years due to the increasing installation of floating LNG-based power plants in countries with lower CAPEX for power generation or by countries having lower infrastructure availability.

- Power barges have several advantages that fuel their adoption across the FLNG power generation segment. These are used to transport bulk with lower transportation costs, and they are available in different sizes. These barges can travel in low-tide water, and they can facilitate successful transportation of any sort of cargo while producing energy and floating.

- The barge is designed to carry out for a specific water body and that barge can only run in that water body throughout its life. If that barge is used in some different water body, then it needs to be properly tugged or assisted by a tugboat.

- In December 2021, Wison Offshore and Marine signed an MoU with MAN Energy Solutions for power solutions development. The two parties will establish cooperation for power barge and floating LNG-to-power projects, which will become a good demonstration of each party's advantage in technology and application.

- Hence, owing to the above points, the power barge segment is expected to dominate the floating LNG power plant market during the forecast period.

Asia-Pacific Expected to Dominate the Market

- In the Asia-Pacific region, the supply-demand energy gap is often mitigated by sources such as coal, hydro, natural gas, nuclear, and renewable energy technologies. A significant rate of electricity access has been achieved in most of the economies. On the other hand, renewable energy sources have eradicated power reliability issues to the maximum extent, which indicates low chances for the development of a floating LNG power plants market in the region.

- However, few countries in Southeast Asia have adopted floating power plants to secure energy supplies. According to Malaysia's energy authority, the electricity demand is expected to reach about 24 GW in 2039. To cater to the growing demand, the government has taken measures to scale up energy systems, such as floating LNG power plants to fulfill the same.

- In 2023, Petronas contracted Kejuruteraan Asastera(KAB) to develop and commission a 52MW floating LNG power plant worth USD 52.2 million. The floating LNG power plant would be located at Sabah. The development work is expected to start in the second quarter of 2023. Also, the Sri Lankan government, in association with Asian Development Bank, agreed to conduct a feasibility study in 2022 on a floating LNG power plant, which could help the country to diversify its energy mix.

- Further, in 2022, Indonesia received a floating power barge designed to run on LNG, which is likely to bridge the power generation requirements in the country. BMPP Nusantara-1 holds the potential to fulfill the electricity demand of far-flung areas of the country, which would help businesses and residents minimize their dependence on rented power generation barges.

- Hence, owing to the above points, Asia-Pacific is expected to dominate the floating LNG power plant market during the forecast period.

Floating LNG Power Plant Industry Overview

The floating LNG power plant market is moderately consolidated. Some of the key players in the market (in no particular order) include Wison Group, Kawasaki Heavy Industries Ltd, Wartsila Oyj Abp, Chiyoda Corp, and Karadeniz Holding.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Component Type

- 5.1.1 Gas Engines or Gas Turbines

- 5.1.2 IC Engines

- 5.1.3 Steam Turbines & Generators

- 5.2 Vessel Type

- 5.2.1 Power Ship

- 5.2.2 Power Barge

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 South America

- 5.3.5 Middle East & Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Collaboration and Joint Ventures

- 6.2 Strategies Adopted by Key Players

- 6.3 Company Profiles

- 6.3.1 Kawasaki Heavy Industries Ltd

- 6.3.2 Wartsila Oyj Abp

- 6.3.3 Siemens Energy AG

- 6.3.4 Waller Marine Inc.

- 6.3.5 Wison Group

- 6.3.6 Chiyoda Corporation

- 6.3.7 Karadeniz Holding