|

市場調查報告書

商品編碼

1440079

駕駛模擬器:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Driving Simulator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

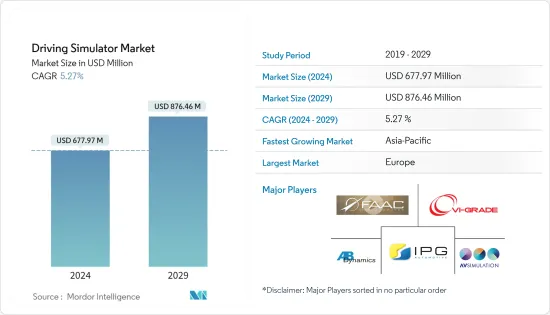

駕駛模擬器市場規模預計2024年為6.7797億美元,預計到2029年將達到8.7646億美元,在預測期內(2024-2029年)成長5.27%,年複合成長率成長。

由於COVID-19感染疾病的爆發以及隨後的封鎖(隨後出現了所有限制),駕駛模擬器市場出現了下滑。與其他產業一樣,疫情也對駕駛模擬器市場產生了負面影響。市場佔有率較大的主要國家受到疫情的負面影響,導致駕駛模擬器安裝量下降。然而,隨著經濟逐漸恢復正常,市場正在加快步伐,預計在預測期內將出現正成長。

汽車技術日益進步,對安全功能的需求也不斷增加。大多數事故是由於人為錯誤或駕駛技術不佳造成的。為了避免這種情況,駕駛模擬器是人為創建即時環境並虛擬提高駕駛員技能的完美方式。該系統可幫助駕駛員以受控的方式管理情況。因此,駕駛模擬器的效率更高,安全性也顯著提高。

駕駛模擬器和分析技術擴大應用於鐵路、航空、海事、國防和汽車領域,以幫助在虛擬環境中測試和分析產品設計。特別是在汽車領域,大多數國家都頒布了新的立法來提高車輛安全性,輕型和中型車輛對先進安全功能的需求不斷增加。此外,日益嚴格的安全和環境法規迫使製造商和當局投資用於培訓目的的創新設計的駕駛模擬器。這大大降低了新車先進功能的研發成本。

模擬器是新車開發和測試的關鍵方面之一。模擬器結果可幫助工程師在建造原型並在賽道上測試車輛時運行虛擬模擬,從而做出關鍵決策。

此外,汽車零件的電動、半自動駕駛和自動駕駛汽車的出現,以及科技公司在汽車產業影響力的不斷增強,也正在推動駕駛模擬器市場的成長要素。汽車產業正向自動駕駛汽車邁進。

大多數汽車製造商都在研究自動駕駛汽車技術,如果沒有模擬器,這是不可能實現的,未來,新的參與者可能會進入自動駕駛汽車領域,這有助於預測期內市場的成長。可能會得到升遷。在過去五年裡,主要汽車製造商、科技巨頭和專業新興企業已在自動駕駛汽車 (AV) 技術開發上投資超過 500 億美元,其中 70% 的資金來自汽車產業以外。同時,公共當局認知到自動駕駛汽車可能帶來顯著的經濟和社會效益。

駕駛模擬器市場趨勢

自動駕駛汽車成為市場成長引擎

自動駕駛汽車製造商在將自動駕駛汽車引入公共道路時正在努力解決安全問題。這些相關人員認為,自動駕駛汽車將比人類駕駛員安全得多。該標準需要大幅增加現有的測試設備。

然而,近年來,雖然自動駕駛汽車的真實道路測試規模不斷擴大,但由於自動駕駛汽車需要大量的資料收集和處理,市場企業對自動駕駛汽車的安全性提出了擔憂。你參加駕駛汽車模擬器測試。資料在物聯網連接的車輛之間共用,並無線傳輸到雲端系統以進行檢查和改進自動化。

幾大市場參與者正在大力投資開發自動駕駛汽車的測試模擬系統和軟體,以便讓具有相當高安全等級的自動駕駛汽車上路。例如,

在最新的 CommunicAsia 2022展覽會上,開發自動駕駛汽車模擬技術的韓國公司 MORAI 展示了「真正的自動駕駛汽車駕駛模擬器」MORAI SIM Drive。 MORAI 為自動駕駛車輛和自動系統開發模擬工具和解決方案。

MORAI SIM Drive是自動駕駛汽車的真實駕駛模擬器,為自動駕駛汽車提供檢驗和模擬環境、感測器資料以及忠實再現真實事物的車輛模型。 MORAI SIM Drive 可自動建立虛擬環境,並透過高清地圖和高效能 3D 圖形引擎 (Unity) 提供準確的網路表示。

自動駕駛汽車需要收集和處理大量資料,因此汽車製造商正在大力投資自動駕駛汽車技術並建立合作關係,以開發最好的自動駕駛汽車。整個資料在物聯網連接的車輛之間共用,並無線上傳到雲端系統,在雲端系統中進行分析並用於提高自動化程度。

- 2021 年 12 月,本田研發公司在試運行最新的先進 Delta S3 DIL 模擬器後,延長了與 Ansible Motion 的長期合作關係。具有更大操作空間和更大動態範圍的多功能模擬器將能夠在櫻花工程工廠高效開發未來的公路和賽車及其相關技術。

- 2021年3月,Volvo集團與NVIDIA簽署協議,共同開發自動駕駛商用車和機械的決策系統。利用 NVIDIA 的端到端人工智慧平台進行訓練、模擬和汽車運算,最終的系統預計將能夠安全地處理公共道路和高速公路上的全自動駕駛。事實確實如此。

- 2021年1月,通用汽車宣布與微軟建立長期策略合作關係,以加速自動駕駛汽車的商業化。兩家公司預計將結合其卓越的軟體和硬體工程、雲端運算能力、製造技術和合作夥伴生態系統來改變交通運輸。

OEM很快就會專注於自動駕駛,而電動車的後續成長預計將增加對用於測試和研究的駕駛模擬器的需求,特別是活躍於市場的原始OEM。

歐洲可望引領市場

主導的歐洲是世界上技術最先進的市場之一。配備碰撞偵測、車道偏離警告和主動車距控制巡航系統等 ADAS(高級駕駛員輔助系統)的 2 級和 3 級自動駕駛汽車正在該地區迅速成長。

從駕駛員教練學院到賽道,駕駛模擬器擴大被用作駕駛員和賽車手培訓教育的戰略工具。此外,還將部署駕駛模擬器來評估乘坐舒適性和操控性、NVH(噪音、振動、聲振粗糙度)、人機介面和硬體在環,以加快整個車輛開發過程的創新速度。我很期待到它。減少實體原型的數量、開發時間和成本。

隨著公共產業合作夥伴的各種投資和購買,德國駕駛模擬器市場正在蓬勃發展。例如,

- 2022 年 4 月,模擬和駕駛模擬器開發商 VI-grade 宣布其 DiM250 動態模擬器的增強版已被長期客戶本田採用。本田新收購的DiM是本田集團內第二款VI級動態模擬器,該公司的研發中心位於德國奧芬巴赫,自2018年以來一直使用DiM250模擬器版本進行車輛開發和測試。

- 2022 年 2 月,博世將透過收購 Atratech 來擴大其自動駕駛專業知識,並有可能加強其市場地位,該公司為自動駕駛和模擬開發高解析度地圖。

一些公共事業平台和公司了解駕駛模擬器的先進準備,並積極投資研究和技術,以設計先進且可靠的刺激解決方案。例如:

- 2022年5月,法國泰雷茲完成了瑞士RUAG模擬與訓練公司(RUAG S&T)的收購。 RUAG 模擬與培訓 (RUAG S&T) 的全部 500 名員工已全部轉移到泰雷茲,該公司擁有約 900 名員工。泰雷茲目前是歐洲領先的軍事模擬和培訓開發和供應公司之一,Uniwest 為其用戶提供服務。 RUAG S&T 去年的銷售額約為 9,000 萬歐元(9,450 萬美元)。

泰雷茲聲稱,此次合併將擴大企業發展,同時保留在直升機和軍用飛機解決方案方面的專業知識。此次收購也將使我們能夠擴大在阿拉伯聯合大公國和澳洲的業務,同時加強我們在法國、瑞士、英國的本地業務。

考慮到德國駕駛模擬器的持續開發和購買,預計其需求在預測期內將呈現高成長率。

駕駛模擬器產業概況

駕駛模擬器市場由多個活躍參與者主導,包括老牌大公司和新興企業。市場主要參與者包括 Cruden BV、AutoSim AS、AVSimulation、Ansible Motion 等。公共產業合作夥伴和OEM正在大力投資開發用於車輛測試和道路動態的先進駕駛模擬器技術。玩家為此結成策略聯盟。例如:

- 2022 年 9 月,AB Dynamics PLC 收購了 Ansible Motion Limited,該公司是全球汽車市場先進模擬器的領先供應商。此次收購已宣布總金額為 3,120 萬英鎊,初始對價為 1,920 萬英鎊,在滿足某些業績標準的情況下支付 1,200 萬英鎊。

- 2022年6月,香港研究機構微美全像宣布,正與全像科學研發中心密切合作,促進車輛驅動系統對虛擬實境技術的持續需求。

- 2022 年 5 月,Ansible Motion 宣布了量產 Delta 系列 S3 駕駛員在環 (DIL) 模擬器的所有規格。它旨在檢驗實現新的電動趨勢、自動駕駛、駕駛輔助、HMI 和車輛動力學所需的技術。

- 2021 年 7 月,英國Dynisma Ltd 宣布發布新型高級駕駛模擬器。這些 Dynisma 運動產生器 (DMG) 專為汽車製造商和供應商開發和測試先進車輛而設計。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章 簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 市場促進因素

- 市場限制因素

- 產業吸引力-波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔(以金額為準的市場規模)

- 按車型

- 小客車

- 商用車

- 按使用類型

- 訓練

- 測試和研究

- 依模擬器類型

- 緊湊型模擬器

- 成熟的模擬器

- 海拔模擬器

- 按地區

- 北美洲

- 美國

- 加拿大

- 北美其他地區

- 歐洲

- 德國

- 英國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 世界其他地區

- 巴西

- 阿拉伯聯合大公國

- 其他國家

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- AutoSim AS

- AVSimulation

- VI-grade GmbH

- Ansible Motion Ltd

- Cruden BV

- Tecknotrove Simulator System Pvt. Ltd

- IPG Automotive GmbH

- AB Dynamics PLC

- Virage Simulation

- XPI Simulation

- FAAC Incorporated

第7章市場機會與未來趨勢

The Driving Simulator Market size is estimated at USD 677.97 million in 2024, and is expected to reach USD 876.46 million by 2029, growing at a CAGR of 5.27% during the forecast period (2024-2029).

Due to the COVID-19 pandemic outbreak and the subsequent lockdowns (with all the restrictions followed), the driver simulator market witnessed a decline. Like any other industry, the pandemic showed a negative impact on the driving simulator market as well. Major countries with a large market share are negatively impacted by the pandemic, reducing the installation of driving simulators. However, as the economies slowly returned to a state of normalcy, the market is picking up pace and is expected to grow positively during the forecast period.

As technologies in automobiles are improving day by day, there is also a significant need for safety features in them. Most accidents happen due to human errors, lack of driving skills, etc. To avoid such situations, driving simulators are the best way to enhance driver skills virtually, where a real-time environment is created artificially. This system helps the driver in managing the situation in a controlled manner. Thus, a driving simulator is more efficient and improves safety to a great extent.

The adoption of driving simulators and analysis technology has experienced an increase in the railways, aviation, marine, defense, and automotive sectors, as it helps in testing and analyzing the designs of products in a virtual environment. Especially in the automobile sector, there is a consistent increase in the demand for advanced safety features in compact and mid-sized automobiles, as most countries are bringing in new laws to improve vehicular safety. Moreover, increasing stringency of safety and environmental regulations has compelled manufacturers and authorities to invest in driving simulators with innovative designs for training. This drastically decreases the research and development cost of the advanced features in a new vehicle.

Simulators are one of the crucial aspects of the development and testing of new vehicles. The simulator's result helps engineers make important decisions by running virtual simulations while building the prototype and testing the vehicle on the track.

Additionally, the electrification of automotive components, the advent of semi-autonomous and autonomous vehicles, and the increasing influence of technology companies in the automotive industry are growth factors for the driving simulator market. The automotive industry is heading toward autonomous vehicles.

Most vehicle manufacturers are working on autonomous vehicle technology, which is not possible without simulators, and in the future, new players are likely to enter the field of autonomous vehicles, which may drive market growth in the forecast period. Major automaker companies, technology giants, and specialist start-ups have invested more than USD 50 billion over the past five years to develop autonomous vehicle (AV) technology, with 70% of the money coming from other than the automotive industry. At the same time, public authorities see that AVs offer substantial potential economic and social benefits.

Driving Simulator Market Trends

Autonomous Vehicle Acts as a Growth Engine for the Market

Autonomous vehicle makers are working hard to address the issue of autonomous vehicle safety when they are deployed on public roads. These players believe that autonomous vehicles will be far safer drivers than human drivers. This standard necessitates a large increase in existing testing installations.

However, while testing of driverless vehicles on actual roads has expanded in recent years, safety worries about autonomous vehicles are prompting market firms to engage in simulator testing for autonomous vehicles, as autonomous vehicles require a massive amount of data collection and processing. The data is shared among IoT-connected automobiles and wirelessly transferred to a cloud system to be examined and utilized to improve automation.

Several key market companies are substantially investing in the development of testing simulation systems and software for autonomous cars for these vehicles to be released on the road with considerably higher safety ratings. For instance,

At the most recent CommunicAsia 2022 trade show, MORAI, a Korean company that creates simulation technology for autonomous vehicles, demonstrated its MORAI SIM Drive, a "true-to-life autonomous vehicle driving simulator.' As an autonomous vehicle and autonomous system, MORAI develops simulation tools and solutions.

The realistic driving simulator for autonomous vehicles, MORAI SIM Drive, can verify autonomous vehicles and offer simulation environments, sensor data, and vehicle models that are exact replicas of the real thing. MORAI SIM Drive automates building virtual environment and offers accurate network representation with HD map and a high-performance 3D graphic engine (Unity).

Vehicle manufacturers are investing heavily in autonomous car technology and entering partnerships to develop the best autonomous vehicle, as autonomous vehicles require enormous data collecting and processing. The entire data is shared between IoT-connected cars and uploaded wirelessly to a cloud system to be analyzed and used to improve automation.

- In December 2021, Honda R&D Co. extended its long-term relationship with Ansible Motion after commissioning the latest advanced Delta S3 DIL simulator. With its larger motion space and increased dynamic range, the versatile simulator would enable the efficient development of future road and race vehicles and their associated technologies at its Sakura engineering facility.

- In March 2021, Volvo Group signed an agreement with NVIDIA to jointly develop the decision-making system of autonomous commercial vehicles and machines. Utilizing NVIDIA's end-to-end artificial intelligence platform for training, simulation, and in-vehicle computing, the resulting system is expected to be designed to handle fully autonomous driving on public roads and highways safely.

- In January 2021, General Motors announced they had entered a long-term strategic relationship with Microsoft to accelerate the commercialization of self-driving vehicles. The companies are expected to bring together their software and hardware engineering excellence, cloud computing capabilities, manufacturing know-how, and partner ecosystem to transform transportation.

With OEM's focus on automated driving soon and subsequent growth of electric vehicles is anticipated to drive the demand for driving simulators, especially for testing and research by the OEMs operating in the market.

Europe is Expected to Lead the Market

Europe is led by Germany, one of the global most technologically superior markets. There is rapid growth for Level 2 and Level 3 autonomous cars in this region, equipped with advanced driver assistance systems like collision detection, lane departure warning, and adaptive cruise control.

From driver instructor academies to the race track, driving simulators are increasingly used as strategic tools in training education for drivers and racers. Moreover, the driving simulator will be deployed to assess ride and handling, NVH (Noise, Vibration, and Harshness), human-machine interface, and hardware in the loop in the hope of accelerating the rate of innovation in the overall vehicle development process while reducing the number of physical prototypes, and development time and costs.

The German driving simulator market is booming due to various investments and purchases ensured by utility partners. For instance,

- In April 2022, Simulation and driving simulator developer VI-grade announced that an extended version of its DiM250 Dynamic simulator had been adopted by long-standing customer Honda. Honda's newly acquired DiM is the second VI-grade Dynamic simulator within the Honda Group, with the company's R&D site in Offenbach, Germany, relying on a version of the DiM250 simulator for vehicle development and testing since 2018.

- In February 2022, Bosch could expand its expertise in automated driving and strengthen its market position by acquiring Atlatec, a developer of high-definition maps for autonomous driving and simulation.

Several utility platforms and companies understand the deep readiness of driving simulators and thus actively invest in research and technologies to come up with advanced and reliable stimulation solutions. For instance:

- In May 2022, Thales, based in France, completed its acquisition of Switzerland's RUAG Simulation and Training (RUAG S&T). All 500 RUAG Simulation and Training (RUAG S&T) employees have transferred to Thales, which employs approximately 900 people. Thales is now one of Europe's leading companies in the development and supply of simulation and training for the military, as brought to users by Uniwest. RUAG S&T made around EUR90 million (US$94.5 million) in sales last year.

Thales claims that the consolidation will expand its footprint in the land market while maintaining its expertise in helicopters and military aircraft solutions. This acquisition also allows it to strengthen its local footprint in France, Switzerland, Germany, and the United Kingdom, while expanding its presence in the United Arab Emirates and Australia.

Considering these ongoing developments and purchases for driving simulators in Germany, demand for the same is expected to witness a high growth rate during the forecast period.

Driving Simulator Industry Overview

The driving simulator market is dominated by several active players' presence, which includes major existing companies and new startups. Some of the major players in the market are Cruden BV, AutoSim AS, AVSimulation, and Ansible Motion. utility partners and OEMs are heavily investing in developing advanced driving simulator technology for their vehicle testing and its on-road dynamics. Players are carrying strategic alliances for the same. For instance:

- In September 2022, AB Dynamics PLC acquired Ansible Motion Limited, a leading provider of advanced simulators to the global automotive market. The acquisition was announced for a total fee of Pound 31.2 Million, which comprises a Pound 19.2 Million initial consideration and a Pound 12 Million payment subject to meeting certain performance criteria.

- In June 2022, WIMI Hologram Academy, which is a research institute in Hong Kong, announced that it is deeply working in close partnership with Holographic Science Innovation Center in order to felicitate the ongoing demand for virtual reality technology in vehicle driving systems.

- In May 2022, Ansible Motion unveiled all the specifications for the production Delta series S3 Driver-in-the-Loop (DIL) simulator, which is intended to validate the technologies required to enable the emerging electrification trends, autonomy, driver assistance, as well as HMI and vehicle dynamics.

- In July 2021, Dynisma Ltd of the United Kingdom announced the release of its new advanced driving simulators. These Dynisma Motion Generators (DMGs) were specifically designed for automotive manufacturers and suppliers for advanced vehicle development and testing.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD Million)

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Commercial Vehicle

- 5.2 By Application Type

- 5.2.1 Training

- 5.2.2 Testing and Research

- 5.3 By Simulator Type

- 5.3.1 Compact Simulator

- 5.3.2 Full-scale Simulator

- 5.3.3 Advanced Simulator

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 Brazil

- 5.4.4.2 United Arab Emirates

- 5.4.4.3 Other Countries

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 AutoSim AS

- 6.2.2 AVSimulation

- 6.2.3 VI-grade GmbH

- 6.2.4 Ansible Motion Ltd

- 6.2.5 Cruden BV

- 6.2.6 Tecknotrove Simulator System Pvt. Ltd

- 6.2.7 IPG Automotive GmbH

- 6.2.8 AB Dynamics PLC

- 6.2.9 Virage Simulation

- 6.2.10 XPI Simulation

- 6.2.11 FAAC Incorporated

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

駕駛模擬器市場:按車輛類型、模擬器類型、應用分類 - 2024-2030 年全球預測

駕駛模擬器市場:按車輛類型、模擬器類型、應用分類 - 2024-2030 年全球預測 全球駕駛模擬器市場規模研究與預測(按車輛類型按應用類型按模擬器類型和區域分析,2023-2030 年)

全球駕駛模擬器市場規模研究與預測(按車輛類型按應用類型按模擬器類型和區域分析,2023-2030 年) 全球賽車模擬器市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測

全球賽車模擬器市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢和預測 全球賽車模擬器市場:按類型、應用、產品細分、車輛類型、銷售管道、組件和地區 - 預測(截至 2030 年)

全球賽車模擬器市場:按類型、應用、產品細分、車輛類型、銷售管道、組件和地區 - 預測(截至 2030 年) 2030 年軍用車輛駕駛模擬器市場預測:按類型、應用和地區分類的全球分析

2030 年軍用車輛駕駛模擬器市場預測:按類型、應用和地區分類的全球分析 2023-2027 年全球車禍衝擊模擬器市場

2023-2027 年全球車禍衝擊模擬器市場 駕駛模擬器市場:按應用、車輛類型、模擬器類型:2023-2032年全球機會分析與產業預測

駕駛模擬器市場:按應用、車輛類型、模擬器類型:2023-2032年全球機會分析與產業預測 駕駛模擬器市場:按車輛類型、模擬器類型、用途- 2023-2030 年全球預測

駕駛模擬器市場:按車輛類型、模擬器類型、用途- 2023-2030 年全球預測 駕駛模擬器全球市場研究報告——2023-2030 年行業分析、規模、份額、增長、趨勢和預測

駕駛模擬器全球市場研究報告——2023-2030 年行業分析、規模、份額、增長、趨勢和預測 汽車用駕駛模擬器的全球市場

汽車用駕駛模擬器的全球市場