|

市場調查報告書

商品編碼

1439868

螢石:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Fluorspar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

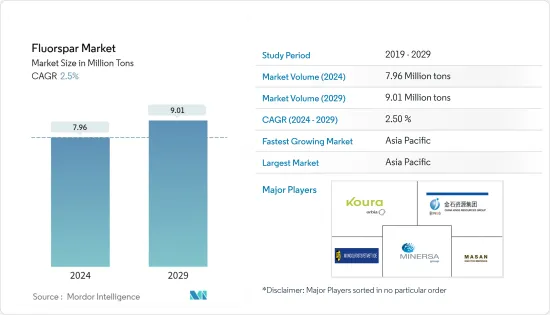

預計2024年螢石市場規模為796萬噸,預計2029年將達到901萬噸,在預測期間(2024-2029年)年複合成長率為2.5%。

COVID-19 大流行的爆發導致了長期關閉和嚴格的社交距離規範。它還導致供應鏈中斷和勞動力短缺,嚴重影響了世界各地的採礦作業。此外,疲軟的鋼鐵需求進一步抑制了這段時期螢石的需求。

主要亮點

- 隨著製造業和服務業逐漸恢復到疫情前的活動水平,化學工業預計將穩步復甦。預計對螢石的需求將受到對從螢石中提取的化學品的需求增加的推動。預計鋼鐵業的復甦和鋼鐵產量的增加將進一步加強這一需求。

- 然而,採礦活動對環境的負面影響導致對螢石等化學品的提取實施嚴格的規定,這可能會阻礙市場的成長。

- 另一方面,全球即將向電動車轉型預計將導致對鋰離子電池以及由螢石製成的含氟聚合物(擴大用於此類電池)的需求預計將增加。

- 隨著化學工業的強勁成長和鋼鐵產量的增加,亞太地區很可能成為全球最大的螢石市場。

螢石市場趨勢

冶金應用成為快速成長的應用

- 螢石主要用於生產鋼、鐵和其他金屬。

- 它可作為助焊劑,去除金屬液中的硫、磷等雜質,改善爐渣的流動性。

- 生產一噸金屬需要使用 20 至 60 磅螢石。

- 螢石可直接用作冶金助焊劑,無需任何選礦過程。它富含螢石,並含有少量必須作為爐渣的一部分提供的其他化合物。

- 它也與石灰一起用於冶煉,以改善煉鋼和罐式冶金過程中的爐渣流動性。鋼鐵生產中螢石消費量由2公斤增加到10公斤,相當於石灰用量的5%~10%。

- 冶金工業是指金屬礦產的探勘、開採、清洗、冶煉和軋延工業。

- 預計對螢石的需求不斷成長將推動全球冶金活動,從而有利於預測期內螢石市場的成長。

- 美國採礦活動的擴張預計將有利於該國的冶金工業。在該國營運的主要礦業公司包括 Newmount Mining Corp.、Peabody Energy Corp.、Arch Resources Inc. 和 Suncoke Energy Inc.。

- 根據世界鋼鐵協會統計,受歐洲及中東地緣政治局勢影響,2022年全球粗鋼產量達18.878億噸,較2021年下降3.8%。然而,鋼鐵需求已恢復並超過 2018 年水平,預計在預測期內將大幅成長,特別是在亞太地區。

- 上述因素表明,冶金應用對螢石的需求在預測期內可能會增加。

亞太地區主導市場

- 預計亞太地區將在預測期內主導螢石市場。中國、日本和印度等開發中國家化學工業對螢石的需求不斷成長,以及鋼鐵和汽車行業應用的擴大,預計將推動該地區螢石的需求。

- 在亞太地區,中國是GDP最大的經濟體。 2020年中國GDP成長2.3%,2021年成長8%,很大程度得益於疫情後消費支出的復甦。根據國際貨幣基金組織的數據,2022年GDP成長已降至3%。

- 根據世界鋼鐵協會的數據,預計2022年中國粗鋼產量為1,017.95噸,而2021年為1,035.24噸。從2021年第三季開始,由於一些製造商在開採螢石時擔心環境問題,本地螢石產量大幅減少。

- 在印度,螢石主要以兩個等級進行消費和交易:酸性等級(acidpar)和亞酸性等級(sub-acid Grade)。冶金和陶瓷牌號包含在弱酸性牌號中,也稱為冶金牌號(Mesper)。與全球產量相比,印度的螢石產量極低。

- 根據國家礦產庫存 (NMI)資料庫,根據 UNFC 方法估計印度的總蘊藏量和資源量為 1,818 萬噸。其中,蘊藏量為29萬噸,其中「已確認」儲量22萬噸,「可能」儲量6萬噸。剩餘資源量1789萬噸。

- 上述因素表明,亞太地區,特別是中國、印度和東南亞國協對螢石的需求在預測期內可能會增加。

螢石產業概況

螢石市場部分整合,只有少數大公司主導市場。一些主要企業(排名不分先後)包括 Mexichem Fluor SA de CV (Koura)、China Kings Resources Group、Mongolrostsvetmet LLC、Minersa Group 和 Masan Resources。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 螢石萃取化學品對螢石的需求不斷增加

- 鋼鐵產量增加拉動需求

- 抑制因素

- 關於螢石化學提取的環境法規

- 其他阻礙因素

- 產業價值鏈分析

- 波特五力分析

- 新進入者的威脅

- 買方議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭程度

- 螢石選礦製程技術簡介

第5章市場區隔

- 年級

- 酸性級

- 陶瓷級

- 冶金級

- 光學級

- 寶石級

- 種類

- 安東尼石

- 藍色約翰

- 氯仿

- 伊特羅斯利特

- 釔螢石

- 其他品種

- 目的

- 冶金

- 陶瓷

- 化學品

- 其他用途

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)**/排名分析

- 主要企業策略

- 公司簡介

- Canada Fluorspar

- China Kings Resources Group Co. Ltd

- Fluorsid(British Fluorspar)

- Kenya Fluorspar

- Koura

- Masan Resources

- MINCHEM IMPEX India Private Limited

- Minersa Group

- Mongolrostsvetmet LLC

- RUSAL

- Sallies Ltd

- Seaforth Mineral & Ore Co.

- Steyuan Mineral Resources Group Ltd

第7章 市場機會及未來趨勢

- Fluspar氟樹脂在鋰電池中的使用增加

The Fluorspar Market size is estimated at 7.96 Million tons in 2024, and is expected to reach 9.01 Million tons by 2029, growing at a CAGR of 2.5% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic resulted in prolonged lockdowns and strict social distancing norms. It also led to supply chain disruptions and a lack of labor, which greatly affected mining operations all over the globe. Additionally, a slump in steel demand further hampered fluorspar demand during this period.

Key Highlights

- With the manufacturing and services sectors slowly resuming pre-pandemic activity levels, the chemical industry is expected to recover steadily. The demand for fluorspar is anticipated to be driven by the growing demand for fluorspar-extracted chemicals. This demand is expected to be further strengthened with the recovery of the steel industry and rising steel production.

- However, the negative impacts of mining activities on the environment have led to stringent regulations being imposed on the extraction of chemicals like fluorspar, which could potentially hinder the market's growth.

- On the flip side, the impending global shift to electric vehicles is expected to create long-term demand for lithium-ion batteries, augmenting demand for fluorspar-made fluoropolymers, which have been increasingly used in these types of batteries.

- With a lot of growth in the chemical industry and more steel being made, the Asia-Pacific region is likely to be the biggest fluorspar market in the world.

Fluorspar Market Trends

Metallurgical Application to be the Fastest Growing Application

- Fluorspar is majorly used in the production of steel, iron, and other metals.

- It serves as a flux that eliminates impurities like sulfur and phosphorous from molten metal and improves the fluidity of slag.

- Between 20 and 60 pounds of fluorspar is used in the production of every ton of metal.

- Fluorspar can be directly used as a metallurgical flux without any beneficiation process. It is rich in fluorite and contains small amounts of other compounds required to be fed as part of slag.

- It is also used as a smelter with lime to improve the fluidity of slag in the steelmaking and metallurgical process of the pot. The consumption of fluorspar in the production of steel increased from 2 to 10 kg or by 5 to 10% of the amount of lime.

- The metallurgical industry refers to the exploration, mining, cleaning, smelting, and rolling of metal minerals.

- The increasing demand for fluorspar is projected to promote metallurgical activities across the world, thereby benefiting the fluorspar market's growth during the forecast period.

- The growing mining activities in the United States are expected to benefit the metallurgical industry in the country. The leading mining companies operating in the country include Newmount Mining Corp., Peabody Energy Corp., Arch Resources Inc, Suncoke Energy Inc., and others.

- According to the World Steel Association, global crude steel production in 2022 reached 1,887.80 million tons, decreased by 3.8% compared to 2021 due to the geopolitical scenarios in Europe and Middle-East. However, the steel demand has recovered and reached above 2018 levels, and it is expected to increase significantly during the forecast period, especially in the Asia-Pacific region.

- The aforementioned factors indicate a strong potential for a rise in demand for fluorspar from metallurgy application during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market for fluorspar during the forecast period. The rising demand for fluorspar from the chemical industry and its growing applications in the steel and automotive industries in developing countries like China, Japan, and India are expected to drive the demand for fluorspar in this region.

- In Asia-Pacific, China is the largest economy in terms of GDP. China's GDP increased by 2.3% in 2020 and by 8% in 2021, owing largely to a rebound in consumer spending following the pandemic. In 2022, the GDP growth reduced to 3%, as per the IMF.

- According to the World Steel Association, crude steel production in China was estimated at 1,017.95 metric tons in 2022, compared to 1,035.24 metric tons in 2021. Starting in the third quarter of 2021, a lot less fluorspar was made locally because several manufacturers were worried about the environment when they mined fluorspar.

- In India, fluorspar is mostly consumed and traded in two grades: acid grade (acidspar) and sub-acid grade. Metallurgical and ceramic grades are included in the sub-acid grade, which is also known as the metallurgical grade (metspar). When compared to global production, India produces extremely little fluorspar.

- According to the National Mineral Inventory's (NMI) database, the country's total fluorspar reserves and resources are estimated at 18.18 million metric tons based on UNFC methodology. Reserves account for 0.29 million metric tons of this total, of which 0.22 million metric tons are in the "proven" category and 0.06 million metric tons are in the "probable" category. There are 17.89 million metric tons of remaining resources.

- The aforementioned factors indicate a strong potential for a rise in demand for fluorspar in the Asia-Pacific region, specially from China, India and ASEAN Countries during the forecast period.

Fluorspar Industry Overview

The fluorspar market is partially consolidated, with only a few major players dominating the market. Some of the major companies (not in any particular order) are Mexichem Fluor SA de CV (Koura), China Kings Resources Group Co. Ltd., Mongolrostsvetmet LLC, Minersa Group, and Masan Resources.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Fluorspar from Fluorspar Extracted Chemicals

- 4.1.2 Increasing Steel Production Driving the Demand

- 4.2 Restraints

- 4.2.1 Environmental Regulation on Extraction of Chemicals from Fluorspar

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot of Fluorspar Beneficiation Process

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Grade

- 5.1.1 Acid Grade

- 5.1.2 Ceramic Grade

- 5.1.3 Metallurgical Grade

- 5.1.4 Optical Grade

- 5.1.5 Lapidary Grade

- 5.2 Variety

- 5.2.1 Antozonite

- 5.2.2 Blue John

- 5.2.3 Chlorophane

- 5.2.4 Yttrocerite

- 5.2.5 Yttrofluorite

- 5.2.6 Other Varieties

- 5.3 Application

- 5.3.1 Metallurgical

- 5.3.2 Ceramics

- 5.3.3 Chemicals

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Canada Fluorspar

- 6.4.2 China Kings Resources Group Co. Ltd

- 6.4.3 Fluorsid (British Fluorspar)

- 6.4.4 Kenya Fluorspar

- 6.4.5 Koura

- 6.4.6 Masan Resources

- 6.4.7 MINCHEM IMPEX India Private Limited

- 6.4.8 Minersa Group

- 6.4.9 Mongolrostsvetmet LLC

- 6.4.10 RUSAL

- 6.4.11 Sallies Ltd

- 6.4.12 Seaforth Mineral & Ore Co.

- 6.4.13 Steyuan Mineral Resources Group Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Use of Fluospar Made Fluoropolymers in Lithium Batteries

全球螢石市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測

全球螢石市場研究報告 - 2024 年至 2032 年產業分析、規模、佔有率、成長、趨勢與預測 螢石市場:依等級、類型、應用分類 - 2024-2030 年全球預測

螢石市場:依等級、類型、應用分類 - 2024-2030 年全球預測 螢石市場:依等級、類型、用途、地區

螢石市場:依等級、類型、用途、地區 螢石的全球市場

螢石的全球市場