|

市場調查報告書

商品編碼

1439800

重晶石:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Barite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

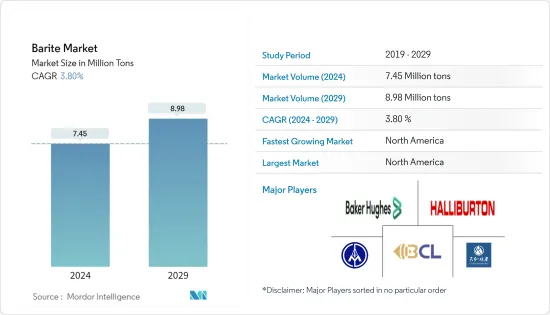

預計2024年重晶石市場規模為745萬噸,預計2029年將達到898萬噸,在預測期間(2024-2029年)年複合成長率為3.80%。

2020 年,市場受到新型冠狀病毒肺炎 (COVID-19) 的負面影響。然而,由於石油和天然氣、化學品和橡膠等各個最終用戶產業的消費增加,2021年至2022年市場顯著復甦。

主要亮點

- 從長遠來看,推動重晶石市場的主要因素是石油和天然氣鑽探活動需求的增加以及全球塑膠產業中重晶石使用量的增加。

- 然而,天青石和鐵礦石等類似替代品的供應限制了重晶石市場的成長。

- 重晶石在塗料和醫療行業的快速採用及其在石油和天然氣行業的作用可能會為市場帶來新的成長機會。

由於石油和天然氣行業的發展,重晶石在其中發揮非常重要的作用,預計北美將成為重晶石的最大市場。

重晶石市場趨勢

石油和天然氣產業的高需求

- 重晶石作為石油和天然氣鑽井作業中鑽井泥漿的稱重劑,需求量很大。它可以防止鑽井過程中石油和天然氣的爆炸性釋放,並具有高比重、化學和物理惰性、低溶解度和磁性中性等獨特的物理和化學性能。

- 世界上大部分需求來自石油工業。鑑於石油產品在運輸和工業最終用途領域的重要性,全球對重晶石的需求將持續下去,直到石油產品成為主要能源來源。

- 重晶石的無腐蝕、無磨蝕性、不溶於水、惰性和高比重等特性,使其能夠在鑽井作業中用作填充劑,以清除鑽頭中的切屑並將切屑輸送到地面。減少鑽柱摩擦、控制壓力、防止井噴並提供潤滑。

- 石油業未來成長的前景表明,石油探勘將繼續成長,重晶石消費也將繼續成長。此外,碳氫化合物發現的生產力會隨著時間的推移而降低,因此每單位石油需要進行更多的鑽探。

- 國際能源總署的一份報告稱,隨著歐洲天然氣價格飆升,發電用石油用量大幅增加以及從天然氣轉向石油將推動2022年至2023年石油需求的成長軌跡。 2022 年全球需求成長預測每天上調 380 kb。儘管這些成長絕大多數集中在中東和歐洲,掩蓋了其他產業的相對疲軟,但到2022 年,需求將增加2.1 MB/天,達到99.7 MB/天;2023 年,需求將再增加2.1 MB/天,達到101.8 MB/天。 MB/天。

- 葡萄牙4月至5月燃料油使用量及直接原油發電量增加30kb/d,即173%,而西班牙、英國及日本月增15%至55%,呈逐步成長趨勢。

- 此外,根據國際能源總署的數據,2022年全球石油需求預計為170萬桶/日,達到9,920萬桶/日。在非經合組織國家強勁成長軌跡的推動下,預計 2023 年產量將進一步增加 210 萬桶/日。

- 此圖顯示,石油和天然氣產品的需求量逐年增加。 IEA預測,液化石油氣和乙烷的需求將從2022年的1432.1萬桶/日增加到2023年的1464.2萬桶/日。汽車汽油也出現類似趨勢,預計需求量將達到 26,137,000 桶/日。產量將從2022年的25,932,000桶/日增加到2023年的25,932,000桶/日。

- 因此,未來幾年的市場成長可能會受到全球石油和天然氣產業對重晶石需求不斷成長的推動。

北美地區佔據市場主導地位

- 美國電子市場規模全球最大,是研究市場的主要潛在區域之一。此外,由於先進技術的使用、研發中心數量的增加以及消費者需求的增加,預計在預測期內它將繼續保持主導市場的地位。

- 根據總統科學技術顧問委員會 (PCAST) 的報告,大約 12% 的半導體是在美國製造的。到 2021 年,大約 7% 用於製造商品的設備將位於北美。

- 根據皮尤研究中心的數據,85% 的美國擁有智慧型手機。此外,到 2021 年,平板電腦的擁有量將增加至 53%,而桌上型電腦或筆記型電腦的擁有量將增加至 77%。智慧型手機和其他電子產品銷售的成長正在為該地區的重晶石創造一個主要市場。

- 根據國際工業組織(OICA)的數據,2021年美國小客車銷售量為3,350,050輛。 2021年,加拿大和墨西哥的小客車銷量分別為320,605輛和520,112輛。

- 根據美國能源情報署數據,2022年9月原油產量為3.6804億桶,8月為3.71339億桶。

- 根據加拿大能源監管機構的數據,加拿大2022年1月的原油產量接近102,709/天,2月份的原油產量為105,354/天。

因此,由於各行業需求的增加,預計北美地區在預測期內對重晶石的需求將大幅增加。

重晶石行業概況

重晶石市場本質上是整合的。市場主要企業包括(排名不分先後)安得拉邦礦業開發公司、貴州天宏礦業公司、哈里伯頓能源服務公司、VariBrite、貝克休斯公司等。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 石油和天然氣產業需求激增

- 擴大在塑膠行業的使用

- 抑制因素

- 接近替代球員的可用性

- 其他限制

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 買方議價能力

- 新進入者的威脅

- 替代產品和服務的威脅

- 競爭程度

- 定價概覽

- 貿易概況

第5章市場區隔(市場規模(數量))

- 類型

- 帶床

- 靜脈和空腔的填充

- 殘留物

- 最終用戶產業

- 油和氣

- 化學品

- 填料

- 地區

- 亞太地區

- 中國

- 印度

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 北歐國家

- 俄羅斯

- 獨立國協國家

- 其他歐洲國家

- 南美洲

- 巴西

- 哥倫比亞

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 伊朗

- 科威特

- 奈及利亞

- 中東和非洲其他地區

- 生產分析

- 美國

- 中國

- 哈薩克

- 印度

- 墨西哥

- 寮國

- 巴基斯坦

- 摩洛哥

- 伊朗

- 其他

- 亞太地區

第6章 競爭形勢

- 合併、收購、合資、合作和協議

- 市場佔有率(%)**/排名分析

- 主要企業採取的策略

- 公司簡介

- Andhra Pradesh Mineral Development Corporation Ltd

- Baker Hughes Inc.

- Baribright Co. Ltd

- Cimbar Performance Minerals

- Guizhou Saboman Import and Export Co. Ltd

- Guizhou Tianhong Mining Co.

- Halliburton Energy Services Inc.

- International Earth Products LLC

- New Riverside Ochre

- Newpark Resources Inc.

- Pulapathuri

- PVS Global Trade Private Limited

- Sachtleben Minerals GmbH &Co. KG

- Schlumberger Limited

- The Kish Company Inc.

- Zhongrun Barium Industry Co. Ltd

第7章市場機會與未來趨勢

- 重晶石在塗料和醫療產業的應用逐漸增加

- 重晶石在石油天然氣產業中的重要作用

The Barite Market size is estimated at 7.45 Million tons in 2024, and is expected to reach 8.98 Million tons by 2029, growing at a CAGR of 3.80% during the forecast period (2024-2029).

The market was negatively impacted by COVID-19 in 2020. However, the market recovered significantly in the 2021-22 period, owing to rising consumption from various end-user industries such as oil and gas, chemicals, rubber, and others.

Key Highlights

- Over the long term, the major factors driving the barite market are the growing demand from oil and gas drilling activities and its growing usage in the plastics industry across the globe.

- However, the availability of close substitutes, such as celestite and iron ore, is restraining the growth of the barite market.

- The surge in the adoption of barite from the paint and medical industries and the role of barite in the oil and gas industry will likely provide new growth opportunities for the market.

North America is forecast to be the largest market for barite, owing to the growing oil and gas industry, where barite plays a very crucial role.

Barite Market Trends

High Demand from the Oil and Gas Industry

- Barite has huge demand in oil and gas drilling operations as a weighing agent in the drilling mud. It prevents the explosive release of oil and gas during drilling and has unique physical and chemical properties such as high specific gravity, chemical and physical inertness, low solubility, and magnetic neutrality.

- The majority of the global demand is from the petroleum industry. The worldwide demand for barite would continue until petroleum products are preferred as the chief source of energy, given their importance in the transportation and industrial end-use sectors.

- The properties of barite, such as its non-corrosiveness, non-abrasiveness, insolubility in water, inertness, and high specific gravity, allow it to be used as a weighting agent in drilling operations to remove cutting from bits, transport cutting to the surface to reduce friction in the drilling string, control pressure, prevent blow-out, and provide lubrication.

- The prospectus for the future growth of the petroleum industry suggests that petroleum exploration will continue to grow, as will the consumption of barite. Furthermore, more drilling must be done per unit of oil as hydrocarbon discoveries become less productive with time.

- According to a report by the International Energy Agency, surging oil use for power generation and gas-to-oil switching in the wake of soaring European natural gas prices are lifting the growth trajectory for oil demand over 2022 and into 2023. As a result, estimates for 2022 global demand growth have been raised by 380 kb/d. These gains, overwhelmingly concentrated in the Middle East and Europe, mask relative weakness in other sectors but will propel demand higher by 2.1 MB/d to 99.7 MB/d in 2022 and by a further 2.1 MB/d to 101.8 MB/d in 2023.

- Portugal's usage of fuel oil and direct crude use for power generation increased by 30 kb/d, or 173%, between April and May, while Spain, the United Kingdom, and Japan saw more moderate monthly increases of between 15% and 55%.

- Also, as per the International Energy Agency, global oil demand in 2022 was estimated at 1.7 million barrels per day, reaching 99.2 million barrels per day. A further 2.1 million barrels/day gain is expected in 2023, led by a strong growth trajectory in non-OECD countries.

- The graph suggests that the demand for oil and gas products is increasing year over year. The IEA predicts that the demand for LPG and ethane will increase from 14,321 thousand barrels per day in 2022 to 14,642 thousand barrels per day in 2023. A similar trend can be observed for motor gasoline, where the demand is predicted to reach 26,137 thousand barrels per day in 2023 from 25,932 thousand barrels per day in 2022.

- So, the growth of the market over the next few years is likely to be driven by the growing demand for barite from the oil and gas industry around the world.

The North America Region to Dominate the Market

- The United States electronics market is the largest in the world in terms of size, acting as one of the leading potential zones for the market studied. Furthermore, it is expected to remain the leading market over the forecast period due to the usage of advanced technology, an increase in the number of R&D centers, and rising demand from consumers.

- According to a report by the president's council of advisors on science and technology (PCAST), about 12 percent of semiconductors are manufactured in the United States. In 2021, about 7% of the equipment used to make things was going to be used in North America.

- According to the Pew Research Center, 85% of the overall population in the United States owns smartphones. In addition, tablet computer ownership has increased to 53% in 2021, while desktop or laptop computer ownership has increased to 77%.The increasing sales of smartphones and other electronic items are creating a major market in the region for barite.

- According to the International Organization of Motor Vehicle Manufacturers (OICA), the sales of passenger cars in the United States in 2021 were 3,350,050. In 2021, passenger car sales in Canada and Mexico were 320,605 and 520,112, respectively.

- According to the US Energy Information Administration, the crude oil production in September 2022 was 368,040 thousand barrels and 371,339 thousand barrels in August.

- According to the Canada Energy Regulator, Canada produced almost 102,709 m3/d of crude oil in January and 105,354 m3/d of crude oil in February 2022.

Hence, with the rising demand from various industries, the demand for barite is expected to grow considerably in the North American region over the forecast period.

Barite Industry Overview

The barite market is consolidated in nature. Some of the key companies in the market (not in particular order) include The Andhra Pradesh Mineral Development Corporation Ltd, Guizhou Tianhong Mining Co. Ltd, Halliburton Energy Services Inc., Baribright Co. Ltd, and Baker Hughes Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rapidly Increasing Demand from the Oil and Gas Industry

- 4.1.2 Growing Use in the Plastic Industry

- 4.2 Restraints

- 4.2.1 Availability of Close Substitutes

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Overview

- 4.6 Trade Overview

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Bedded

- 5.1.2 Vein and Cavity Filling

- 5.1.3 Residual

- 5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Chemical

- 5.2.3 Fillers

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 ASEAN Countries

- 5.3.1.4 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 NORDIC Countries

- 5.3.3.3 Russia

- 5.3.3.4 CIS Countries

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Colombia

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Iran

- 5.3.5.4 Kuwait

- 5.3.5.5 Nigeria

- 5.3.5.6 Rest of Middle-East and Africa

- 5.3.6 Production analysis

- 5.3.7 United States

- 5.3.8 China

- 5.3.9 Kazakhstan

- 5.3.10 India

- 5.3.11 Mexico

- 5.3.12 Laos

- 5.3.13 Pakistan

- 5.3.14 Morocco

- 5.3.15 Iran

- 5.3.16 Other Countries

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Andhra Pradesh Mineral Development Corporation Ltd

- 6.4.2 Baker Hughes Inc.

- 6.4.3 Baribright Co. Ltd

- 6.4.4 Cimbar Performance Minerals

- 6.4.5 Guizhou Saboman Import and Export Co. Ltd

- 6.4.6 Guizhou Tianhong Mining Co.

- 6.4.7 Halliburton Energy Services Inc.

- 6.4.8 International Earth Products LLC

- 6.4.9 New Riverside Ochre

- 6.4.10 Newpark Resources Inc.

- 6.4.11 Pulapathuri

- 6.4.12 PVS Global Trade Private Limited

- 6.4.13 Sachtleben Minerals GmbH & Co. KG

- 6.4.14 Schlumberger Limited

- 6.4.15 The Kish Company Inc.

- 6.4.16 Zhongrun Barium Industry Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Gradual Surge in Adoption of Barite from Paints & Medical Industry

- 7.2 Crucial Role of Barite in the Oil & Gas Industry

2024-2032 年按等級(最高 3.9、特殊等級 4.0、特殊等級 4.1、特殊等級 4.2、特殊等級 4.3 及以上)、應用(石油和天然氣、化學品、製藥等)和地區的重晶石市場報告

2024-2032 年按等級(最高 3.9、特殊等級 4.0、特殊等級 4.1、特殊等級 4.2、特殊等級 4.3 及以上)、應用(石油和天然氣、化學品、製藥等)和地區的重晶石市場報告 2024 年重晶石世界市場報告

2024 年重晶石世界市場報告 全球重晶石市場:規模、佔有率和趨勢分析報告 - 按應用程式、地區、細分市場預測,2024-2030 年

全球重晶石市場:規模、佔有率和趨勢分析報告 - 按應用程式、地區、細分市場預測,2024-2030 年 2024-2028年全球重晶石市場

2024-2028年全球重晶石市場 重晶石世界市場

重晶石世界市場 重晶石市場、份額、規模、趨勢、產業分析報告:按應用、地區、細分市場預測,2023-2032

重晶石市場、份額、規模、趨勢、產業分析報告:按應用、地區、細分市場預測,2023-2032 重晶石市場:按類型(佔用、殘留、礦脈)、品位分析(Gr.4.0、Gr.4.1、Gr.4.2)、按應用- COVID-19、俄羅斯-烏克蘭衝突和高通脹的累積影響- 世界預測2023-2030 年

重晶石市場:按類型(佔用、殘留、礦脈)、品位分析(Gr.4.0、Gr.4.1、Gr.4.2)、按應用- COVID-19、俄羅斯-烏克蘭衝突和高通脹的累積影響- 世界預測2023-2030 年 重晶石的全球市場調查報告-產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測

重晶石的全球市場調查報告-產業分析,規模,佔有率,成長,趨勢,2022年~2028年前的預測