|

市場調查報告書

商品編碼

1438443

聚丙烯:市場佔有率分析、產業趨勢、成長預測(2024-2029)Polypropylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

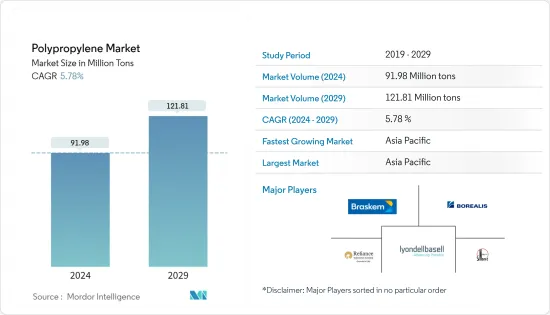

預計2024年聚丙烯市場規模為9,198萬噸,預計2029年將達到1,2,181萬噸,在預測期間(2024-2029年)年複合成長率為5.78%。

由於 COVID-19,聚丙烯的需求略有下降。對聚丙烯的需求很高的建築和汽車產業出現了顯著放緩。隨著主要終端用戶產業恢復營運,2022 年出現強勁復甦。

主要亮點

- 短期內,推動市場的主要因素是擴大使用塑膠來使汽車更輕、更省油,以及對軟包裝的需求不斷成長。

- 另一方面,市場上各種替代產品的存在是預計在預測期內抑制所涵蓋行業成長的主要因素。

- 再生聚丙烯的成長趨勢可能會成為未來的機會。

- 亞太地區在全球整體市場中佔據主導地位,預計在預測期內也將主導中國和印度等國家消費量最高的市場。

聚丙烯市場趨勢

射出成型需求的增加主導了應用領域

- 聚丙烯主要用於射出成型,並且主要以顆粒形式用於此應用。聚丙烯易於成型,並且由於熔體黏度低而具有優異的流動性。

- 射出成型技術用於製造廣泛用於電氣和電子應用的塑膠。這些塑膠廣泛用於製造電氣和電子設備。

- 聚丙烯的靈活性使其適用於多種產品類型。最常用的應用之一是活動鉸鏈,這是一種常用於瓶蓋等消費品的一體式鉸鏈設計。此過程製成的產品不計其數,包括兒童玩具、體育用品、瓶蓋、汽車應用、食品托盤、杯子、外帶容器、家居用品和洗碗機等消費性電子產品。

- 根據全球領先材料製造商之一的 HUBS 統計,聚丙烯佔全球射出成型產量的35-40%,而其他材料如ABS(25%)、聚乙烯(15%)和聚苯乙烯(10%)緊隨其後。它。

- 由於全球包裝和化學加工行業的高速成長,預計射出成型的市場前景良好。憑藉分佈到快速成長的亞太地區的地理優勢,射出成型托盤的消費量可能會大幅增加。

- 此外,汽車中採用輕質部件以提高燃油效率預計將有利於預測期內調查的市場需求。

- 所有上述因素預計將刺激市場需求。

亞太地區成長最快

- 在中國和印度等國家的帶動下,亞太地區的聚丙烯市場正在快速成長。聚丙烯廣泛應用於汽車、消費品、電子和包裝產業。由於這些行業的強勁成長和政府的支持,預計聚丙烯的需求在預測期內將以健康的速度成長。

- 中國是全球最大的汽車市場,並將持續保持年銷量和製造產量第一的地位,預計到2025年國內產量將達到3,500萬輛。

- 此外,根據OICA的數據,2021年中國汽車製造商將生產26,082,220輛汽車,較2020年成長3%。

- 據印度包裝工業協會 (PIAI) 稱,在印度,該行業正以每年 22% 至 25% 的速度成長,預計到 2025 年將達到 2,048.1 億美元。印度包裝產業在進出口方面擁有良好的記錄,推動了該國技術和創新的成長,並為各個製造業付加了價值。

- 包裝產業在推動印度聚丙烯市場的巨大成長方面發揮催化劑作用。此外,過去幾年,該國對包裝食品的需求量很大,預計這種情況在預測期內將持續下去,從而增加了對所研究市場的需求。

- 根據國家投資促進與便利化局統計,汽車產業對印度GDP的貢獻率為7.1%,對製造業GDP的貢獻率為49%。此外,根據國際汽車製造商組織的數據,印度汽車工業生產了4,399,112輛汽車,比2020年成長了近30%。

- 預計這些產業的成長將在預測期內推動亞太地區聚丙烯市場的發展。

聚丙烯產業概況

全球聚丙烯市場較為分散。以產能計算,前五大企業約佔全球市場佔有率的35%。該市場的主要企業包括中國石油化學集團公司 (SINOPEC)、LyondellBasell Industries Holdings BV、Borealis AG、Braskem 和 Reliance Industries Limited。

其他福利:

- Excel 格式的市場預測 (ME) 表

- 3 個月的分析師支持

目錄

第1章簡介

- 調查先決條件

- 調查範圍

第2章調查方法

第3章執行摘要

第4章市場動態

- 促進因素

- 增加塑膠的使用使汽車更輕並提高燃油效率

- 軟包裝需求不斷成長

- 抑制因素

- 替代產品的可用性

- 產業價值鏈分析

- 波特五力分析

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

- 價格趨勢

- 進出口趨勢

- 原料分析

- 技術簡介

第5章市場區隔

- 類型

- 均聚物

- 共聚物

- 目的

- 射出成型

- 纖維

- 薄膜片材

- 其他應用(擠壓塗布、吹塑成型)

- 最終用戶產業

- 包裝

- 車

- 消費性產品

- 電力/電子

- 其他最終用戶產業(紡織、建築)

- 地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東/非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭形勢

- 併購、合資、聯盟、協議

- 市場佔有率(%)分析

- 主要企業策略

- 公司簡介

- Borealis AG

- Braskem

- China National Petroleum Corporation

- China Petrochemical Corporation(SINOPEC)

- Daelim Co. Ltd

- Exxon Mobil Corporation

- Formosa Plastics Corporation

- INEOS

- LG Chem

- Lotte Chemical Corporation

- LyondellBasell Industries Holdings BV

- Mitsubishi Chemical Corporation

- Mitsui Chemicals Inc.(Prime Polymer Co. Ltd)

- Reliance Industries Limited

- SABIC

- SIBUR International GmbH

- Sumitomo Chemical Co. Ltd

- Total Energies

第7章 市場機會及未來趨勢

The Polypropylene Market size is estimated at 91.98 Million tons in 2024, and is expected to reach 121.81 Million tons by 2029, growing at a CAGR of 5.78% during the forecast period (2024-2029).

A slight decline in the demand for polypropylene has been observed due to COVID-19. A drastic slowdown was witnessed in the construction and automotive sector, where polypropylene is in high demand. With the resumption of operations in major end-user industries, it significantly recovered in 2022.

Key Highlights

- Over the short term, major factors driving the market studied are the increasing usage of plastics to reduce vehicle weight and enhance fuel economy and the growing demand for flexible packaging.

- On the other hand, the presence of different substitute products in the market is a key factor anticipated to restrain the growth of the target industry over the forecast period.

- The increasing trends of recycled polypropylene are likely to act as an opportunity in the future.

- The Asia-Pacific dominated the market across the world and is expected to dominate in the forecast period, with the largest consumption from countries such as China and India.

Polypropylene Market Trends

Increasing Demand for Injection Molding to Dominate the Application Segment

- Polypropylene is majorly used for injection molding and is mostly available for this application in the form of pellets. Polypropylene is easy to mold, and it flows very well because of its low melt viscosity.

- Injection molding technology is used to produce plastics that are used extensively in electrical and electronic applications. These plastics are widely used in the manufacturing of electrical and electronic devices.

- Polypropylene is well-suited to a wide range of product types due to its numerous flexible uses. One of the most frequent applications is the living hinge, a one-piece hinged design typically used in consumer items such as caps. Innumerable products made from the process include children's toys, sporting goods, closures, automotive applications, food trays, cups, to-go containers, household goods, and appliances like dishwashers.

- According to HUBS, a globally leading material manufacturing company, polypropylene accounts for 35-40% of worldwide injection molding output, followed by other materials such as ABS (25%), polyethylene (15%), and polystyrene (10%).

- The high growth of the packaging and chemical processing industries across the world is expected to offer a favorable market scenario for injection molding. Owing to the geographical advantage of distribution to the rapidly growing Asia-Pacific region, the consumption of injection-molded pallets may increase drastically.

- Moreover, the adoption of lightweight components for the automobile to increase fuel efficiency is expected to favor the demand for the market studied in the forecast period.

- All the aforementioned factors are expected to boost the market's demand.

Asia-Pacific to Register the Fastest Growth

- The Asia-pacific polypropylene market is growing at a fast pace, driven by countries like China and India. Polypropylene is widely used in the automotive, consumer products, electronics, and packaging industries. With robust growth in these industries and government support, the demand for polypropylene is projected to increase at a healthy pace during the forecast period.

- China is the world's largest vehicle market and will continue to be the largest market by both annual sales and manufacturing output, with domestic production expected to reach 35 million vehicles by 2025.

- Moreover, as per the OICA, Chinese automotive manufacturers manufactured 26,082,220 vehicles in 2021, registering a growth of 3% compared to 2020.

- In India, according to the Packaging Industry Association of India (PIAI), the sector is growing at 22% to 25% per annum and is expected to reach USD 204.81 billion by 2025. The Indian packaging industry made a mark with its exports and imports, driving technology and innovation growth in the country and adding value to the various manufacturing sectors.

- The packaging industry is enacting the role of catalyst in promoting the huge growth of the polypropylene market in India. Furthermore, the country has been exhibiting a significant demand for packed foods in the past few years, which is expected to continue during the forecast period, thus boosting the demand for the market studied.

- As per the National Investment Promotion & Facilitation Agency, the automobile industry contributes 7.1% of India's GDP and 49% of its manufacturing GDP. Moreover, according to Organisation Internationale des Constructeurs d'Automobiles, the Indian automotive industry manufactured 4,399,112 vehicles, which is almost 30% more than in 2020.

- Such growth in various industries is expected to drive the market for polypropylene in the Asia-Pacific region during the forecast period.

Polypropylene Industry Overview

The global polypropylene market is fragmented in nature. The top five companies hold around 35% of the global market share in terms of production capacities. Some of the major players in the market include China Petroleum & Chemical Corporation (SINOPEC), LyondellBasell Industries Holdings BV, Borealis AG, Braskem, and Reliance Industries Limited.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Usage of Plastics to Reduce Vehicle Weight and Enhance Fuel Economy

- 4.1.2 Growing Demand for Flexible Packaging

- 4.2 Restraints

- 4.2.1 Availability of Substitute Products

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Trends

- 4.6 Import-Export Trends

- 4.7 Feedstock Analysis

- 4.8 Technological Snapshot

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Homopolymer

- 5.1.2 Copolymer

- 5.2 Application

- 5.2.1 Injection Molding

- 5.2.2 Fiber

- 5.2.3 Film and Sheet

- 5.2.4 Other Applications (Extrusion Coating, Blow moulding)

- 5.3 End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive

- 5.3.3 Consumer Products

- 5.3.4 Electrical and Electronics

- 5.3.5 Other End-user industries (Textiles, Construction)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Borealis AG

- 6.4.2 Braskem

- 6.4.3 China National Petroleum Corporation

- 6.4.4 China Petrochemical Corporation (SINOPEC)

- 6.4.5 Daelim Co. Ltd

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 Formosa Plastics Corporation

- 6.4.8 INEOS

- 6.4.9 LG Chem

- 6.4.10 Lotte Chemical Corporation

- 6.4.11 LyondellBasell Industries Holdings BV

- 6.4.12 Mitsubishi Chemical Corporation

- 6.4.13 Mitsui Chemicals Inc. (Prime Polymer Co. Ltd)

- 6.4.14 Reliance Industries Limited

- 6.4.15 SABIC

- 6.4.16 SIBUR International GmbH

- 6.4.17 Sumitomo Chemical Co. Ltd

- 6.4.18 Total Energies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Recycled Polypropylene

2024-2032 年按類型、製程、應用、最終用戶和地區分類的聚丙烯市場報告

2024-2032 年按類型、製程、應用、最終用戶和地區分類的聚丙烯市場報告 全球聚丙烯三元共聚物 (Ter PP) 市場

全球聚丙烯三元共聚物 (Ter PP) 市場 生物基聚丙烯 (PP) 市場報告:2030 年趨勢、預測與競爭分析

生物基聚丙烯 (PP) 市場報告:2030 年趨勢、預測與競爭分析 聚丙烯三元共聚物的全球市場洞察與預測(截至2030年)

聚丙烯三元共聚物的全球市場洞察與預測(截至2030年) 改質聚丙烯市場:按類型、應用分類 - 2024-2030 年全球預測

改質聚丙烯市場:按類型、應用分類 - 2024-2030 年全球預測 全球聚丙烯 (PP) 市場 - 2023-2030

全球聚丙烯 (PP) 市場 - 2023-2030 聚丙烯市場(最終用途產業:包裝、汽車、消費品、電氣與電子、建築等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測

聚丙烯市場(最終用途產業:包裝、汽車、消費品、電氣與電子、建築等)- 2023-2031 年全球產業分析、規模、佔有率、成長、趨勢與預測 全球綠色聚丙烯市場研究報告 - 2023 年至 2030 年產業分析、規模、佔有率、成長、趨勢與預測

全球綠色聚丙烯市場研究報告 - 2023 年至 2030 年產業分析、規模、佔有率、成長、趨勢與預測 聚丙烯泡棉市場:按產品、等級和應用分類 - 2023-2030 年全球預測

聚丙烯泡棉市場:按產品、等級和應用分類 - 2023-2030 年全球預測 全球聚丙烯 (PP) 市場:工廠產能、產量、工藝、技術、利用率、需求和供應、最終用途、對外貿易、銷售渠道、區域需求、公司份額(2015-2030 年)

全球聚丙烯 (PP) 市場:工廠產能、產量、工藝、技術、利用率、需求和供應、最終用途、對外貿易、銷售渠道、區域需求、公司份額(2015-2030 年)