|

市場調查報告書

商品編碼

1438405

服裝物流 - 市場佔有率分析、產業趨勢與統計、成長預測(2024 - 2029)Apparel Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

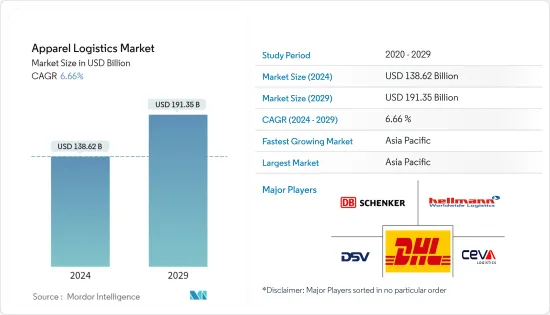

2024年服裝物流市場規模預估為1,386.2億美元,預估至2029年將達到1,913.5億美元,預測期(2024-2029年)CAGR為6.66%。

服裝業的快速補貨週期是推動市場成長的主要因素。從零售商到製造商,服裝供應鏈都在激烈競爭,以提供最新趨勢和最佳客戶體驗。同時,不斷變化的消費者期望和履行模式給服裝企業帶來壓力。

COVID-19 大流行導致跨地區的運輸組織封鎖、線路限制和崩潰。隨著案件數量的迅速增加,整個服裝物流市場正受到多方面的影響。勞動力的可及性正在擾亂服裝物流市場的庫存網路,因為封鎖和感染的蔓延迫使人們留在室內。

許多領先的時尚零售商已經接受了在單一設施內使用單一資訊系統進行多通路分銷的概念,從而顯著提高了勞動生產力和庫存最佳化。服裝市場正在不斷發展和重塑。新的銷售管道正在開發,要求企業不斷評估和重塑其物流和運輸網路。

由於不斷變化的時尚趨勢,全球服裝行業異常活躍。由於競爭激烈,服裝公司正在實施資料分析和人工智慧等新技術。服裝業擁有大量的外包業務,為物流企業提供了相當多的國內和國際營運機會,使其成為一個競爭激烈的行業。供應鏈的任何中斷都會對服裝公司造成巨大損失。因此,為了盡量減少對供應鏈的影響,服裝公司通常更願意將業務外包給物流公司。

服裝物流市場趨勢

線上服裝銷售的成長與消費者行為的改變

2021年6月,快時尚電商網站shein.com是全球時尚服飾類別中訪問量最大的網站,佔桌面流量的3.29%。瑞典服飾零售商HM的電商入口網站排名第二,訪問量為1.75%。 2020 年和 2021 年,線上服裝零售網站由於其數位市場的存在而實現了銷售額成長。這種影響推動了市場參與者的方式發生變化,預計這種變化可能會在未來幾年持續下去,更加重視電子商務、行動購物的成長以及滿足客戶不斷成長的個人期望。

根據網站流量的年度百分比成長,shein.com 在 2020 年第四季度成為美國領先的快時尚零售商網站。雖然消費者經常訪問網站來比較價格和產品,但全球在線平台計劃擴大其網站時尚品牌合作並發展額外的參與方法,以保持在數位購物領域的競爭力。為了處理不斷成長的線上訂單,第三方物流公司正在佔用數百萬平方英尺的空間,並將其出租給消費品、電子商務、製造和服裝公司。

不斷成長的服裝市場推動服裝物流的成長

在研究期間,服裝市場產生的收入穩定成長。 2020年,市場收入約為1.46兆美元。消費科技品牌長期以來一直瞄準澳洲、日本和韓國的線上購物者。然而,服裝和美容行業的品牌也瞄準了其他地區。因此,品牌可能會繼續專注於在地化並迎合千禧世代客戶,他們是這些產品的主要購買者。

2020年,服裝鞋類的年增率出現嚴重下滑。在COVID-19大流行的背景下,增速總計下降了10%以上。體育用品和大眾/俱樂部零售在2020 年實現成長。耐吉和阿迪達斯等全球運動服裝和鞋類品牌正在放棄其他地區,轉而增加在越南等新興東南亞國家的產量,這為運輸公司和其他第三方物流帶來了積極的前景服務供應商。

服裝物流業概況

服裝物流市場呈現分散化狀態,既有大型全球企業,也有中小型本土企業。一些主要參與者佔據了大部分市場佔有率。大多數全球物流企業都設有零售和服裝物流部門來滿足市場需求和需求。此外,本地企業正在不斷增強其在機隊規模、服務產品、處理的產品和技術方面的能力。電商銷售的激增為物流公司在速度、交付等方面帶來了機會和課題。擁有大量資本和資產的全球公司可以投資先進的倉儲空間和履行中心,並從這種情況中受益。另一方面,區域和本地參與者正在提出更好的行業解決方案來支持生產公司和零售商的需求。

額外的好處:

- Excel 格式的市場估算 (ME) 表

- 3 個月的分析師支持

目錄

第 1 章:簡介

- 研究假設和市場定義

- 研究範圍

第 2 章:研究方法

第 3 章:執行摘要

第 4 章:市場概覽

- 當前的市場狀況

- 市場動態

- 促進要素

- 限制

- 產業吸引力-波特五力分析

- 產業價值鏈分析

- 政府法規和舉措

- 聚焦全球物流業

- 全球服裝產業簡介

- 聚焦-電子商務對傳統服裝物流供應鏈的影響

- 退貨貨物流回顧與評論

- 服飾業快速補貨週期對物流市場的影響

- 聚焦合約物流與綜合物流需求

- COVID-19 對市場的影響

第 5 章:市場區隔

- 依服務

- 運輸

- 倉儲和庫存管理

- 其他加值服務

- 依地理

- 亞太

- 中國

- 日本

- 印度

- 韓國

- 東協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 巴西

- 墨西哥

- 美洲其他地區

- 歐洲

- 英國

- 德國

- 義大利

- 西班牙

- 法國

- 歐洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 中東和非洲其他地區

- 亞太

第 6 章:關鍵的定性和定量見解

- 依供應鏈流程

- 生產物流

- 銷售物流

- 逆向物流

- 依服務性質

- 企業物流

- 第三方物流

- 電商物流及即時配送

第 7 章:全球主要時尚零售商洞察(公司概況、產品組合、物流合作夥伴等)

- 印地紡 (ZARA)

- H&M

- 迅銷有限公司

- 蓋璞公司

- 安踏

- L 品牌公司

- PVH公司

- 拉爾夫勞倫公司*

第 8 章:競爭格局

- 公司簡介

- Ceva Logistics

- DB Schenker

- Deutsche Post DHL Group

- DSV

- Hellmann Worldwide Logistics

- Apparel Logistics Group Inc.

- Logwin AG

- PVS Fulfillment-Service GmbH

- Bollore Logistics

- GAC Group

- Nippon Express

- Genex Logistics

- Expeditors International of Washington Inc.

- Agility Logistics

- BGROUP SRL*

第 9 章:市場機會與未來趨勢

第 10 章:附錄

第 11 章:免責聲明

The Apparel Logistics Market size is estimated at USD 138.62 billion in 2024, and is expected to reach USD 191.35 billion by 2029, growing at a CAGR of 6.66% during the forecast period (2024-2029).

Rapid replenishment cycles of the apparel industry are the main factor driving the market's growth. From retailers to manufacturers, apparel supply chains compete strongly to provide the latest trends and the best customer experience. Meanwhile, changing consumer expectations and fulfillment models pressure apparel businesses.

The COVID-19 pandemic caused lockdowns, line limitations, and breakdown of transportation organizations across regions. With the rapidly increasing cases, the overall apparel logistics market is being influenced from multiple points of view. The accessibility of the labor force is disturbing the inventory network of the apparel logistics market, as the lockdowns and the spread of the infection are forcing individuals to remain indoors.

Many leading fashion retailers have embraced the concept of performing multi-channel distribution within a single facility with a single information system, achieving dramatic improvements in labor productivity and inventory optimization. The apparel marketplace is evolving and reinventing itself regularly. New sales channels are being developed, requiring companies to continuously evaluate and remodel their logistics and transportation networks.

The global apparel industry is extremely dynamic due to the ever-changing fashion trends. Due to the intense competition, apparel companies are implementing new technologies, such as data analytics and AI. The apparel industry has massive outsourcing operations that provide logistics players with considerable opportunities in domestic and international operations, making it a highly competitive industry. Any disruption in the supply chain leads to a huge loss for apparel companies. Thus, to have a minimal impact on their supply chain, apparel companies usually prefer outsourcing their operations to logistics players.

Apparel Logistics Market Trends

Growing Online Apparel Sales and Changing Consumer Behavior

In June 2021, the fast-fashion e-commerce site, shein.com, was the most visited in the fashion and apparel category worldwide, accounting for 3.29% of desktop traffic. The e-commerce portal of the Swedish clothing retailer HM ranked second, with 1.75% visits. In 2020 and 2021, online apparel retail sites experienced a sales increase due to their digital market presence. This effect has fuelled changes in the approach of the market players, which may be expected to continue in the coming years, with more emphasis on the growth of e-commerce, mobile shopping, and meeting ever-rising expectations of personalization among customers.

Based on the yearly percentage growth in terms of website traffic, shein.com emerged as the leading fast-fashion retailer website in the United States in Q4 2020. While consumers frequently visit websites to compare prices and products, global online platforms plan to expand their fashion brand partnerships and develop additional engagement methods to stay competitive in the digital shopping space. To handle the growing online orders, third-party logistics companies are absorbing millions of sq. ft of space and letting it out to consumer goods, e-commerce, manufacturing, and apparel companies.

Growing Apparel Market Boosting the Growth of Apparel Logistics

Revenue generated by the apparel market steadily increased through the study period. In 2020, the market revenue was approximately USD 1.46 trillion. Consumer technology brands have long targeted online shoppers in Australia, Japan, and South Korea. However, brands in the apparel and beauty sectors are also targeting other regions. Hence, brands may continue focusing on localization and catering to millennial customers who are the key buyers of these products.

The Y-o-Y growth rate for apparel and footwear experienced severe losses in 2020. Against the backdrop of the COVID-19 pandemic, growth declined by a total of over 10%. Sporting goods and mass/club retail grew in 2020. Global sports apparel and footwear brands like Nike and Adidas are ditching other regions and increasing their production in emerging Southeast Asian countries like Vietnam, offering a positive outlook for transportation companies and other third-party logistics service providers.

Apparel Logistics Industry Overview

The apparel logistics market is fragmented with the presence of large global players and small- and medium-sized local players. Some of the key players occupy most of the market share. Most global logistics players have a retail and apparel logistics division to meet the market needs and demand. Additionally, local players are increasingly enhancing their capabilities in terms of fleet size, service offerings, products handled, and technology. The surging e-commerce sales are creating opportunities and challenges for logistics companies in terms of speed, delivery, etc. Global companies with high capital and assets can invest in advanced storage spaces and fulfillment centers and benefit from this scenario. On the other hand, regional and local players are coming up with better sector solutions to support the needs of the production companies and retailers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Current Market Scenario

- 4.2 Market Dynamics

- 4.2.1 Drivers

- 4.2.2 Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4 Industry Value Chain Analysis

- 4.5 Government Regulations and Initiatives

- 4.6 Spotlight on Global Logistics Sector

- 4.7 Brief on Global Apparel Industry

- 4.8 Spotlight - Effect of E-commerce on Traditional Apparel Logistics Supply Chain

- 4.9 Review and Commentary on Return Logistics

- 4.10 Effect of Apparel Industry's Fast Replenishment Cycles on the Logistics Market

- 4.11 Spotlight on the Demand for Contract Logistics and Integrated Logistics

- 4.12 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Service

- 5.1.1 Transportation

- 5.1.2 Warehousing, and Inventory Management

- 5.1.3 Other Value-added Services

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 Japan

- 5.2.1.3 India

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Brazil

- 5.2.2.4 Mexico

- 5.2.2.5 Rest of Americas

- 5.2.3 Europe

- 5.2.3.1 United Kingdom

- 5.2.3.2 Germany

- 5.2.3.3 Italy

- 5.2.3.4 Spain

- 5.2.3.5 France

- 5.2.3.6 Rest of Europe

- 5.2.4 Middle-East and Africa

- 5.2.4.1 Saudi Arabia

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 KEY QUALITATIVE AND QUANTITATIVE INSIGHTS

- 6.1 By Supply Chain Process

- 6.1.1 Production Logistics

- 6.1.2 Sales Logistics

- 6.1.3 Reverse Logistics

- 6.2 By Nature of Service

- 6.2.1 Enterprise Logistics

- 6.2.2 Third-party Logistics

- 6.2.3 E-commerce logistics and Instant Delivery

7 INSIGHTS ON GLOBAL MAJOR FASHION RETAILERS (Company Overview, Product Portfolio, Logistics Partner, Etc.)

- 7.1 Inditex (ZARA)

- 7.2 H&M

- 7.3 Fast Retailing Co. Ltd

- 7.4 Gap Inc.

- 7.5 Anta

- 7.6 L Brands Inc.

- 7.7 PVH Corp.

- 7.8 Ralph Lauren Corporation*

8 COMPETITIVE LANDSCAPE

- 8.1 Overview (Market Concentration, Major Players)

- 8.2 Company Profiles

- 8.2.1 Ceva Logistics

- 8.2.2 DB Schenker

- 8.2.3 Deutsche Post DHL Group

- 8.2.4 DSV

- 8.2.5 Hellmann Worldwide Logistics

- 8.2.6 Apparel Logistics Group Inc.

- 8.2.7 Logwin AG

- 8.2.8 PVS Fulfillment-Service GmbH

- 8.2.9 Bollore Logistics

- 8.2.10 GAC Group

- 8.2.11 Nippon Express

- 8.2.12 Genex Logistics

- 8.2.13 Expeditors International of Washington Inc.

- 8.2.14 Agility Logistics

- 8.2.15 BGROUP SRL*

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

10 APPENDIX

11 DISCLAIMER

全球物流市場規模、佔有率、成長分析、依運輸方式、依物流模式(第一方物流、第二方物流)、依服務類型 - 產業預測 2024-2031

全球物流市場規模、佔有率、成長分析、依運輸方式、依物流模式(第一方物流、第二方物流)、依服務類型 - 產業預測 2024-2031 2024 年氫動力運輸全球市場報告

2024 年氫動力運輸全球市場報告 2024-2032 年按模型類型、運輸方式、航空公司和地區分類的物流市場報告

2024-2032 年按模型類型、運輸方式、航空公司和地區分類的物流市場報告 數位化物流市場報告:2030 年趨勢、預測與競爭分析

數位化物流市場報告:2030 年趨勢、預測與競爭分析 2024-2028年全球貨運服務市場

2024-2028年全球貨運服務市場 2024-2028 年全球救災物流市場

2024-2028 年全球救災物流市場 中程物流市場:按產品、營運型態和應用分類 - 2024-2030 年全球預測

中程物流市場:按產品、營運型態和應用分類 - 2024-2030 年全球預測 服裝物流市場:按運輸方式、服務和最終用戶分類 - 全球預測 2024-2030 年

服裝物流市場:按運輸方式、服務和最終用戶分類 - 全球預測 2024-2030 年 木材物流市場:按木材類型、服務和運輸模式分類 - 2024-2030 年全球預測

木材物流市場:按木材類型、服務和運輸模式分類 - 2024-2030 年全球預測 藝術品物流市場:按服務、運輸型態和最終用戶分類 - 全球預測 2024-2030

藝術品物流市場:按服務、運輸型態和最終用戶分類 - 全球預測 2024-2030