|

市場調查報告書

商品編碼

1438370

飛機座椅驅動系統:市場佔有率分析、產業趨勢與統計、成長預測(2024-2029)Aircraft Seat Actuation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

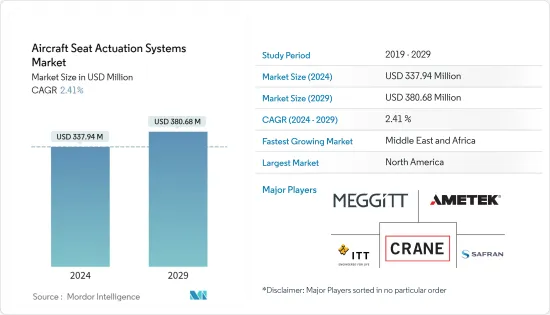

飛機座椅驅動系統市場規模預計到 2024 年為 3.3794 億美元,在預測期內(2024-2029 年)預計到 2029 年將達到 3.8068 億美元,複合年成長率為 2.41%。

2020年爆發的冠狀病毒感染疾病(COVID-19)大流行,嚴重影響了整個航空業。結果,多家飛機業者申請破產,影響了短期飛機需求和飛機座椅驅動系統。不過,隨著飛機交付數量較前一年增加,2021年市場逐漸復甦。類似的趨勢也體現在軍事和通用航空領域。

隨著各國疫苗接種增多,航空旅行限制放寬,航空旅客人數也逐漸增加。客運量的緩慢復甦正在鼓勵航空公司和承運商投資於機隊現代化併購買新飛機以擴大目的地。這主要推動預測期內的市場成長。

由於航空公司和航空公司增加了對客艙現代化的投資,以改善飛機上的乘客體驗,以及座椅製造商的座椅設計創新,以提供更高水平的乘客舒適度,預計將推動飛機座椅驅動系統市場的需求未來幾年。

為了降低製造零件的總重量和成本,投資積層製造等技術來生產薄板和其他片狀零件可以加速輕質片狀致動器和馬達的開發。

飛機座椅驅動系統市場趨勢

固定翼飛機部門將在 2021 年佔據主要收益佔有率

目前,固定翼飛機領域在市場上佔據主導地位。由於其比旋翼機更高的交付和座位要求,預計它們將繼續主導市場。隨著客運量和航空公司營運逐漸增加,2021 年新飛機交付較 2020 年有所改善。 2021年,空中巴士交付了611架民航機(2020年為566架),波音交付了340架民航機(2020年為157架),ATR交付了31架商用飛機(2020年為10架)。民航、公務航空需求的逐步恢復,進一步鼓勵了新飛機的採購。

同樣,隨著供應鏈問題的緩解,軍事領域固定翼飛機的交付也在增加。例如,洛克希德·馬丁公司交付了142架F-35戰鬥機(相比之下,2020年交付了123架),達梭航空出口了25架陣風戰鬥機(相比之下,2020年交付了13架)。飛機交付的增加預計將在預測期內推動市場成長。飛機座椅製造商也與飛機營運公司合作,改進設計以吸引新客戶。客艙內飾和座椅模組的此類創新預計將在未來幾年推動該區隔市場的成長。

預計中東和非洲地區將在預測期內實現最高成長

由於主要航空公司對寬體飛機的需求以及私人和包機公司對大型飛機的需求,預計中東和非洲地區對飛機座椅驅動系統市場的需求最高。例如,阿提哈德航空和阿拉伯聯合大公國航空擁有超過 270 架飛機的訂單(截至 2022 年 1 月),包括波音 777X、空中巴士 A350 系列、A380 和波音 787 系列飛機。同樣,隨著中東地區航空旅行需求的不斷成長,該地區的航空公司和航空公司正在投資擴大機持有,為該地區引入新的航線。

同樣,該地區恐怖主義的抬頭促使這些國家花費大量資金購買軍用飛機。 2021年8月,卡達埃米爾空軍(QEAF)接受了美國和波音公司與美國合作製造的第一批新一代F-15戰機。該飛機是根據該國 2017 年簽署的採購 36 架 F-15QA 戰鬥機的訂單交付的(還可以選擇額外購買 36 架飛機)。埃及、約旦、摩洛哥、阿爾及利亞和以色列空軍的類似飛機訂單預計將在預測期內加速座椅驅動系統市場的成長。

飛機座椅驅動系統產業概述

飛機座椅驅動系統市場是一個高度整合的市場,儘管市場上有許多零件供應商,但佔據很大佔有率的參與者卻很少。飛機座椅驅動系統市場的一些知名企業包括 Safran SA、Meggit PLC、Crane Co.、AMETEK Inc. 和 ITT Inc.。需求仍然強勁,預計不會受到經濟衰退或 COVID-19 疾病導致的市場波動的影響。從軍事方面看流行病。因此,製造商應專注於這一領域,以穩定和保障收益來源。目前航空業需求不斷成長的亞太和中東/非洲地區目前缺乏足夠的基礎設施和產品庫存來快速供應。因此,公司正在擴大其在當地綠地地區的業務,提供先發優勢,並受益於世界許多政府作為其合約義務一部分的抵銷條款。

其他福利

- Excel 格式的市場預測 (ME) 表

- 3 個月分析師支持

目錄

第1章簡介

- 研究假設和市場定義

- 調查範圍

- 美元貨幣匯率

第2章調查方法

第3章執行摘要

- 2018-2027 年全球市場規模與預測

- 2021 年依機制分類的市場佔有率

- 2021 年依飛機類型分類的市場佔有率

- 2021 年依地區分類的市場佔有率

- 市場結構及主要參與者

第4章市場動態

- 市場概況

- 市場促進因素

- 市場限制因素

- 波特五力分析

- 買方議價能力

- 供應商的議價能力

- 新進入者的威脅

- 替代產品的威脅

- 競爭公司之間的敵意強度

第5章市場區隔(市場規模與金額預測,2018-2027)

- 機制

- 線性

- 旋轉式

- 飛機類型

- 固定翼飛機

- 直升機

- 地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 法國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太地區

- 拉丁美洲

- 巴西

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

- 中東和非洲其他地區

- 北美洲

第6章 競爭形勢

- 供應商市場佔有率

- 公司簡介

- Lee Air Inc.

- Safran SA

- Astronics Corporation

- Crane Co.

- ITT Inc.

- CEF Industries LLC

- ElectroCraft Inc.

- NOOK Industries Inc.

- Rollon SpA

- Buhler Motor GmbH

- AMETEK Inc.

- Kyntronics

- Meggitt PLC

- OTM Servo Mechanisms Limited

第7章市場機會與未來趨勢

The Aircraft Seat Actuation Systems Market size is estimated at USD 337.94 million in 2024, and is expected to reach USD 380.68 million by 2029, growing at a CAGR of 2.41% during the forecast period (2024-2029).

The outbreak of the COVID-19 pandemic in 2020 severely impacted the entire aviation industry. It has resulted in several aircraft operators filing for bankruptcy, which affected the demand for aircraft in the short term and aircraft seat actuation systems. However, the market gradually recovered in 2021 due to the increasing aircraft deliveries compared to the previous year. A similar trend has been reflected in the military and general aviation sectors.

With the increasing vaccination in various countries, the air passenger traffic is gradually increasing as the regulations for air travel are alleviating. This gradual recovery in passenger traffic supports the airlines and aircraft operators to invest in the procurement of new aircraft for fleet modernization and destination expansion. This is majorly driving the growth of the market during the forecast period.

Growing investment for cabin modernization by airlines and aircraft operators to enhance passenger experience onboard aircraft and innovation in seat designs by the seat manufacturers for offering a higher level of passenger comfort is anticipated to propel the demand for the aircraft seat actuation systems market in the coming years.

The investments into technologies like additive manufacturing for manufacturing thin down panels and other seat components to reduce the overall weight and cost of manufacturing components are anticipated to promote the development of lightweight seat actuators and motors.

Aircraft Seat Actuation Systems Market Trends

The Fixed-wing Aircraft Segment Accounted for Major Revenue Share in 2021

The fixed-wing aircraft segment currently dominates the market. It is anticipated to continue its dominance over the market due to its higher deliveries and seat requirements than the rotary-wing aircraft. New aircraft deliveries improved in 2021 compared to 2020 due to gradual growth in passenger traffic and airline operations. In 2021, Airbus delivered 611 commercial aircraft (566 deliveries in 2020), Boeing delivered 340 commercial aircraft (157 deliveries in 2020), and ATR delivered 31 aircraft (10 deliveries in 2020). The gradual recovery in demand for commercial aviation and business and private aviation is further propelling the procurement of new aircraft.

Similarly, as the supply chain issues subsided, the fixed-wing aircraft deliveries in the military sector have witnessed growth. For instance, Lockheed Martin delivered 142 F-35 fighter aircraft (compared to 123 deliveries in 2020), and Dassault Aviation exported 25 Rafale fighter jets (compared to 13 deliveries in 2020). The growth in aircraft deliveries is anticipated to propel the market's growth during the forecast period. Also, in collaboration with aircraft operators, the aircraft seat manufacturers are working on enhancing their designs to attract new customers. Such innovation in cabin interiors and seating modules is expected to propel the segment's growth in the coming years.

The Middle-East and Africa Region Expected to Witness Highest Growth During the Forecast Period

The demand for the aircraft seat actuation systems market is anticipated to be highest in the Middle-East and African region due to demand for wide-body aircraft from major airlines and large-size aircraft demand from private and charter companies. For instance, Etihad and Emirates had an order book of more than 270 aircraft (as of January 2022), including Boeing 777X, Airbus A350 family, A380, and Boeing 787 family of aircraft. Similarly, with the growing demand for air travel in the Middle-East region, the airlines and aircraft operators in the region are investing in expanding their aircraft fleet to introduce new aircraft routes in the region.

Similarly, the growth in terrorism in this region has resulted in these countries spending a significant amount on military aircraft procurement. The Qatar Emiri Air Force (QEAF) received its first batch of the new generation F-15 combat aircraft in August 2021, produced by the United States and Boeing, in partnership with the Gulf state. The aircraft was delivered under an order signed by the country in 2017 to procure 36 F-15QA fighter aircraft with an option for an additional 36 aircraft. Similar aircraft orders from Air Forces of Egypt, Jordan, Morocco, Algeria, and Israel are anticipated to accelerate the growth of the seat actuation systems market during the forecast period.

Aircraft Seat Actuation Systems Industry Overview

The market of aircraft seat actuation systems is a highly consolidated market with very few players accounting for the majority share in the market despite the presence of the many component providers in the market. Some prominent players in the aircraft seat actuation systems market are Safran SA, Meggit PLC, Crane Co., AMETEK Inc., and ITT Inc. The demand is expected to remain robust and free from market fluctuations due to the economic downturn and COVID-19 pandemic from the military applications side. Thus manufacturers should focus on this segment to stabilize and secure their revenue sources. The Asia-Pacific and the Middle-East and Africa regions, which are currently experiencing demand in the aviation industry, presently lack adequate infrastructure and inventory of products to supply quickly. Therefore, the companies are expanding their presence in underdeveloped regions locally, as it would provide them the first-mover advantage and will also benefit from offset clauses that are being set forth by many governments globally as part of contract obligations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by Mechanism, 2021

- 3.3 Market Share by Aircraft Type, 2021

- 3.4 Market Share by Geography, 2021

- 3.5 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD million, 2018 - 2027)

- 5.1 Mechanism

- 5.1.1 Linear

- 5.1.2 Rotary

- 5.2 Aircraft Type

- 5.2.1 Fixed-wing Aircraft

- 5.2.2 Helicopters

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lee Air Inc.

- 6.2.2 Safran SA

- 6.2.3 Astronics Corporation

- 6.2.4 Crane Co.

- 6.2.5 ITT Inc.

- 6.2.6 CEF Industries LLC

- 6.2.7 ElectroCraft Inc.

- 6.2.8 NOOK Industries Inc.

- 6.2.9 Rollon SpA

- 6.2.10 Buhler Motor GmbH

- 6.2.11 AMETEK Inc.

- 6.2.12 Kyntronics

- 6.2.13 Meggitt PLC

- 6.2.14 OTM Servo Mechanisms Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

全球飛機座椅驅動系統市場規模、佔有率、成長分析、按產品、飛機、驅動機構 - 產業預測 2024-2031

全球飛機座椅驅動系統市場規模、佔有率、成長分析、按產品、飛機、驅動機構 - 產業預測 2024-2031 2024年飛機座椅表皮全球市場報告

2024年飛機座椅表皮全球市場報告 2024-2028 年全球汽車座椅驅動系統市場

2024-2028 年全球汽車座椅驅動系統市場 飛機座椅市場:按類別、材料、分銷管道和最終用戶分類 - 2024-2030 年全球預測

飛機座椅市場:按類別、材料、分銷管道和最終用戶分類 - 2024-2030 年全球預測 飛機座椅表皮市場:按材料類型、座椅套類型、座椅類型、飛機類型分類 - 2024-2030 年全球預測

飛機座椅表皮市場:按材料類型、座椅套類型、座椅類型、飛機類型分類 - 2024-2030 年全球預測 飛機座椅驅動系統市場:按類型、機制分類 - 2024-2030 年全球預測

飛機座椅驅動系統市場:按類型、機制分類 - 2024-2030 年全球預測 飛機座椅市場(飛機類型:支線噴射機、窄體飛機、小型寬體客機、中/大型客機寬體機和渦輪螺旋槳)- 全球產業分析、規模、佔有率、成長、趨勢和預測,2023 -2031 年

飛機座椅市場(飛機類型:支線噴射機、窄體飛機、小型寬體客機、中/大型客機寬體機和渦輪螺旋槳)- 全球產業分析、規模、佔有率、成長、趨勢和預測,2023 -2031 年 飛機座椅驅動系統市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測

飛機座椅驅動系統市場:2023-2028 年全球產業趨勢、佔有率、規模、成長、機會與預測 飛機座椅表皮市場 - 全球規模、佔有率、趨勢分析、機會、預測報告,2019-2029

飛機座椅表皮市場 - 全球規模、佔有率、趨勢分析、機會、預測報告,2019-2029 全球飛機乘客座椅市場,到 2030 年的市場預測:按類型、材料、技術、配銷通路、用途和地區進行的全球分析

全球飛機乘客座椅市場,到 2030 年的市場預測:按類型、材料、技術、配銷通路、用途和地區進行的全球分析